Key Insights

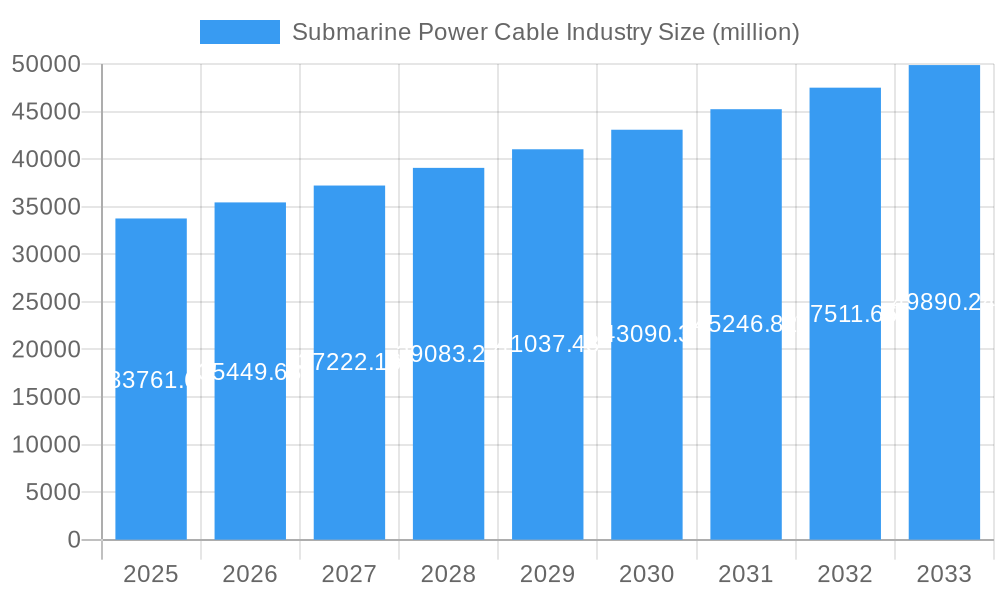

The Submarine Power Cable industry is poised for substantial expansion, driven by a critical need for enhanced grid connectivity and the burgeoning demand for renewable energy integration. With an estimated market size of $33,761.6 million in 2025, the sector is projected to experience a Compound Annual Growth Rate (CAGR) of 5% over the forecast period of 2025-2033. This growth is primarily fueled by significant investments in offshore wind farms, which necessitate robust and reliable submarine power cable systems to transmit electricity to onshore grids. Furthermore, the increasing development of interconnector cables between countries and regions to bolster energy security and optimize power distribution across diverse geographical locations acts as a significant catalyst. The ongoing modernization of aging electrical infrastructure globally, coupled with advancements in cable technology offering higher voltage capacity and improved durability, also underpins this positive market trajectory.

Submarine Power Cable Industry Market Size (In Billion)

The industry landscape is characterized by a dynamic interplay of opportunities and challenges. While the expansion of renewable energy sources and the need for enhanced grid resilience are strong market drivers, certain restraints could temper the pace of growth. These may include the high capital expenditure required for manufacturing and installation of submarine power cables, coupled with the inherent complexities and risks associated with offshore projects, such as challenging marine environments and regulatory hurdles. The market is segmented into High Voltage Direct Current (HVDC) and High Voltage Alternating Current (HVAC) cables, with the demand for HVDC cables expected to rise due to its efficiency in transmitting power over long distances with minimal loss, especially relevant for offshore wind power transmission. Key players like Prysmian Group, Nexans SA, and Sumitomo Electric Industries Limited are actively engaged in technological innovation and strategic partnerships to secure a larger market share and meet the escalating global demand.

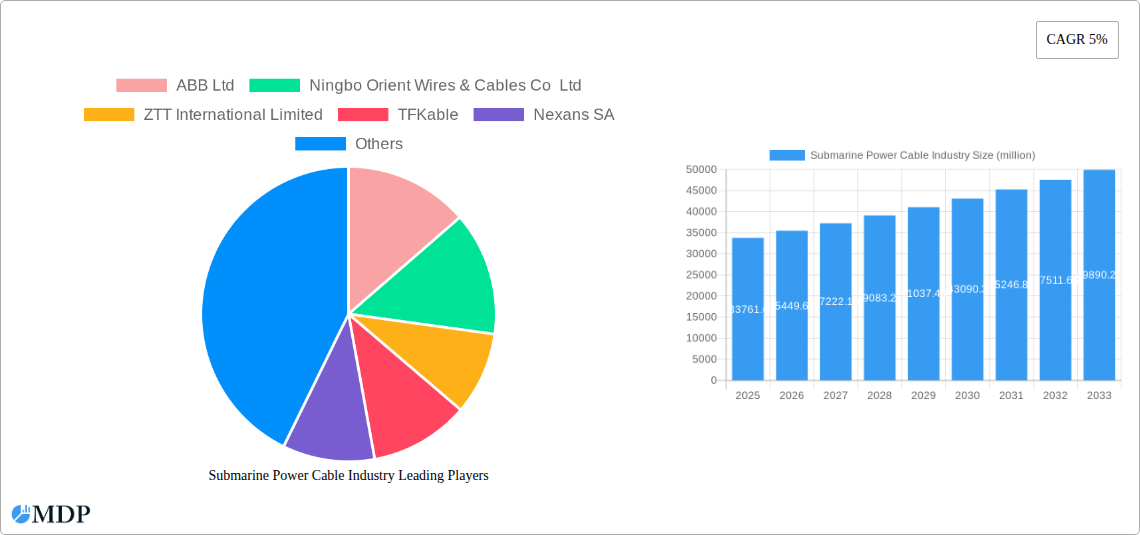

Submarine Power Cable Industry Company Market Share

Submarine Power Cable Industry Market Dynamics & Concentration

The global submarine power cable market is characterized by a moderate to high concentration, with a few dominant players controlling a significant portion of the market share. In 2025, the market share of the top five companies is estimated to exceed 60%, reflecting substantial investment and technological expertise required for this capital-intensive industry. Innovation remains a key driver, fueled by the increasing demand for renewable energy integration and the expansion of offshore wind farms, which necessitate high-capacity, long-distance power transmission. Regulatory frameworks, particularly those promoting decarbonization and grid modernization, play a crucial role in shaping market growth. While direct product substitutes are limited, advancements in onshore grid infrastructure and alternative energy storage solutions can indirectly influence demand. End-user trends are largely dictated by governmental initiatives, utility investment cycles, and the evolving energy landscape. Mergers and acquisitions (M&A) are prominent, driven by the desire to consolidate market position, acquire specialized technologies, and expand geographical reach. The number of significant M&A deals in the historical period (2019-2024) is projected to be around 15-20, with values often in the hundreds of millions. Companies like Prysmian Group, Nexans SA, and Sumitomo Electric Industries Limited are consistently involved in strategic collaborations and acquisitions to maintain their competitive edge.

Submarine Power Cable Industry Industry Trends & Analysis

The submarine power cable industry is experiencing robust growth, driven by several interconnected trends. A primary catalyst is the accelerating global transition towards renewable energy sources, particularly offshore wind. The need to transmit electricity from vast offshore wind farms to onshore grids has created an insatiable demand for high-voltage direct current (HVDC) and high-voltage alternating current (HVAC) submarine cables. Market penetration for offshore wind power is projected to grow by over 15% annually through the forecast period (2025-2033), directly translating into increased demand for these specialized cables. The compound annual growth rate (CAGR) for the overall submarine power cable market is anticipated to be around 7.5% during the study period. Technological disruptions are focused on increasing cable capacity, extending transmission distances, and improving reliability and durability in harsh marine environments. Innovations in cable insulation materials, manufacturing processes, and installation techniques are continuously being developed. Consumer preferences, in this context, are more about utility needs and governmental mandates for clean energy rather than direct consumer choice. Utilities and grid operators are prioritizing solutions that offer cost-effectiveness, minimal environmental impact, and long-term performance. Competitive dynamics are intense, with leading players investing heavily in research and development, expanding manufacturing capacities, and forming strategic partnerships to secure large-scale projects. The industry is also witnessing a trend towards greater vertical integration, with some companies extending their services to include project design, installation, and maintenance. The estimated market size for submarine power cables in 2025 is approximately 15,000 million, with projections reaching over 30,000 million by 2033.

Leading Markets & Segments in Submarine Power Cable Industry

The High-Voltage Direct Current (HVDC) segment is emerging as a dominant force within the submarine power cable industry, driven by its inherent advantages for long-distance and high-capacity power transmission. In 2025, HVDC cables are expected to account for over 55% of the total market revenue, a share projected to grow to over 65% by 2033.

- HVDC Dominance Drivers:

- Efficiency over Long Distances: HVDC technology offers significantly lower transmission losses compared to HVAC for distances exceeding approximately 80 kilometers, making it ideal for connecting offshore wind farms located far from shore.

- Interconnection of Grids: HVDC cables are crucial for interconnecting asynchronous AC grids, enabling better grid stability, energy trading, and the integration of diverse power sources.

- Environmental Benefits: Reduced land use requirements for substations and the ability to transmit more power with fewer cables contribute to environmental advantages.

- Governmental Support for Renewables: Policies promoting offshore wind development and grid modernization directly translate into increased demand for HVDC infrastructure.

The primary geographical markets driving this segment are Europe, particularly countries with extensive offshore wind development like the UK, Germany, and Denmark, and increasingly, Asia-Pacific, with China and other nations investing heavily in offshore energy. The estimated market size for the HVDC segment in 2025 is around 8,250 million, projected to reach over 19,500 million by 2033.

While HVAC continues to be important for shorter distances and traditional grid connections, its growth is more moderate. The HVAC segment is estimated to hold a market size of approximately 6,750 million in 2025, with projected growth to around 10,500 million by 2033. Key drivers for HVAC include its established infrastructure, lower initial cost for shorter links, and its role in connecting offshore platforms and islands to the main grid where distance is not a primary concern. However, the trend towards larger and more distant offshore wind farms consistently favors the expansion of HVDC technology.

Submarine Power Cable Industry Product Developments

Product developments in the submarine power cable industry are intensely focused on enhancing performance, reliability, and sustainability. Innovations include advanced insulation materials like cross-linked polyethylene (XLPE) with improved thermal and electrical properties, enabling higher power transmission capabilities. Superconducting cables are an emerging area, promising near-zero resistance and significantly higher power density, though still in early commercialization stages. Increased cable lengths and diameters are being developed to meet the demands of massive offshore wind projects. Manufacturers are also focusing on more robust sheathing and armoring to withstand extreme marine conditions, reducing maintenance needs and extending operational lifespans. The competitive advantage lies in offering complete solutions, from cable design and manufacturing to installation and after-sales support, ensuring seamless integration and long-term system integrity.

Key Drivers of Submarine Power Cable Industry Growth

The submarine power cable industry's growth is propelled by a confluence of powerful drivers. The global surge in renewable energy, particularly offshore wind power, is a paramount factor, necessitating extensive subsea transmission infrastructure. Government mandates for decarbonization and grid modernization are creating substantial investment opportunities. Technological advancements in HVDC transmission technology enable more efficient and longer-distance power delivery. Furthermore, the increasing demand for intercontinental power grid interconnections to enhance energy security and facilitate international energy trading plays a significant role. The ongoing expansion of offshore oil and gas platforms also requires reliable subsea power supply.

Challenges in the Submarine Power Cable Industry Market

Despite its robust growth, the submarine power cable industry faces several challenges. High capital expenditure for manufacturing facilities and specialized vessels creates a significant barrier to entry. Complex and lengthy permitting processes, especially for offshore projects, can lead to project delays and cost overruns. Supply chain disruptions for critical raw materials, such as copper and specialized polymers, can impact production timelines and costs. Environmental regulations, while driving demand for renewables, can also introduce stringent requirements for cable manufacturing and installation, increasing compliance costs. Moreover, the high competition among a few dominant players can lead to price pressures on large-scale projects.

Emerging Opportunities in Submarine Power Cable Industry

Emerging opportunities in the submarine power cable industry are diverse and promising. The burgeoning floating offshore wind market, which extends power generation capabilities into deeper waters, presents new demands for specialized, flexible subsea cables. The development of inter-regional grid interconnections, such as those planned between continents or across major seas, will require massive investments in high-capacity submarine cables. Advancements in cable monitoring and diagnostic technologies, including artificial intelligence and sensor integration, offer opportunities for predictive maintenance and enhanced system reliability, creating new service revenue streams. The increasing focus on grid resilience and the integration of diverse energy sources will continue to fuel demand for robust and flexible subsea power transmission solutions.

Leading Players in the Submarine Power Cable Industry Sector

- ABB Ltd

- Ningbo Orient Wires & Cables Co Ltd

- ZTT International Limited

- TFKable

- Nexans SA

- Furukawa Electric Co Ltd

- NKT A/S

- Prysmian Group

- Sumitomo Electric Industries Limited

- KEI Industries Limited

- LS Cable & System Ltd

Key Milestones in Submarine Power Cable Industry Industry

- November 2022: South Korea's leading cable manufacturer, LS Cable & System Ltd., became the largest shareholder of KT Submarine Co., a company specializing in undersea cable construction. This strategic investment aimed to strengthen LS Cable's position in the submarine cable market and expand its capabilities in undersea cable projects.

- 2023: Significant investments announced by major players for expanding manufacturing capacity for high-voltage subsea cables to meet the anticipated surge in offshore wind projects.

- 2024: Increased focus on research and development of advanced insulation materials and more robust cable designs to enhance durability and performance in increasingly challenging marine environments.

- 2025 (Estimated): Anticipated launch of pilot projects for next-generation superconducting submarine cables, promising revolutionary power transmission capabilities.

- 2027 (Projected): Completion of several large-scale offshore wind farm grid connections, demonstrating the growing scale and complexity of subsea power infrastructure.

- 2030 (Projected): Significant growth in the interconnector market, with multiple new subsea links planned to enhance energy security and facilitate cross-border power trading.

Strategic Outlook for Submarine Power Cable Industry Market

The strategic outlook for the submarine power cable industry is exceptionally strong, driven by the global imperative to transition to renewable energy and modernize energy grids. The increasing scale and geographical reach of offshore wind farms will continue to be a primary growth accelerator, demanding higher capacity and longer-length subsea cables. Investments in interconnector projects, facilitating energy security and market integration, will offer substantial opportunities. The industry's strategic focus will remain on technological innovation to enhance cable performance, reliability, and cost-effectiveness. Furthermore, companies that can offer integrated solutions, encompassing manufacturing, installation, and maintenance, will be well-positioned to capture market share and drive sustainable long-term growth in this dynamic sector.

Submarine Power Cable Industry Segmentation

-

1. Type of Current

- 1.1. HVDC

- 1.2. HVAC

Submarine Power Cable Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. South America

- 5. Middle East and Africa

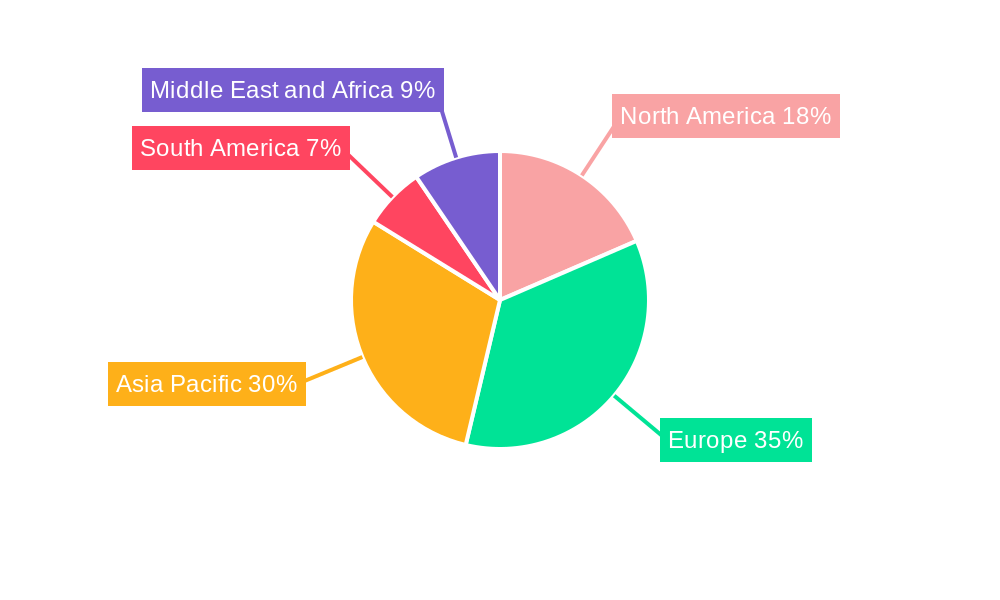

Submarine Power Cable Industry Regional Market Share

Geographic Coverage of Submarine Power Cable Industry

Submarine Power Cable Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Current

- 5.1.1. HVDC

- 5.1.2. HVAC

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type of Current

- 6. Global Submarine Power Cable Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Current

- 6.1.1. HVDC

- 6.1.2. HVAC

- 6.1. Market Analysis, Insights and Forecast - by Type of Current

- 7. North America Submarine Power Cable Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Current

- 7.1.1. HVDC

- 7.1.2. HVAC

- 7.1. Market Analysis, Insights and Forecast - by Type of Current

- 8. Europe Submarine Power Cable Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Current

- 8.1.1. HVDC

- 8.1.2. HVAC

- 8.1. Market Analysis, Insights and Forecast - by Type of Current

- 9. Asia Pacific Submarine Power Cable Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Current

- 9.1.1. HVDC

- 9.1.2. HVAC

- 9.1. Market Analysis, Insights and Forecast - by Type of Current

- 10. South America Submarine Power Cable Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Current

- 10.1.1. HVDC

- 10.1.2. HVAC

- 10.1. Market Analysis, Insights and Forecast - by Type of Current

- 11. Middle East and Africa Submarine Power Cable Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Current

- 11.1.1. HVDC

- 11.1.2. HVAC

- 11.1. Market Analysis, Insights and Forecast - by Type of Current

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ABB Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ningbo Orient Wires & Cables Co Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ZTT International Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 TFKable

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Nexans SA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Furukawa Electric Co Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 NKT A/S

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Prysmian Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sumitomo Electric Industries Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 KEI Industries Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 LS Cable & System Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 ABB Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Submarine Power Cable Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Submarine Power Cable Industry Revenue (million), by Type of Current 2025 & 2033

- Figure 3: North America Submarine Power Cable Industry Revenue Share (%), by Type of Current 2025 & 2033

- Figure 4: North America Submarine Power Cable Industry Revenue (million), by Country 2025 & 2033

- Figure 5: North America Submarine Power Cable Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Submarine Power Cable Industry Revenue (million), by Type of Current 2025 & 2033

- Figure 7: Europe Submarine Power Cable Industry Revenue Share (%), by Type of Current 2025 & 2033

- Figure 8: Europe Submarine Power Cable Industry Revenue (million), by Country 2025 & 2033

- Figure 9: Europe Submarine Power Cable Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Submarine Power Cable Industry Revenue (million), by Type of Current 2025 & 2033

- Figure 11: Asia Pacific Submarine Power Cable Industry Revenue Share (%), by Type of Current 2025 & 2033

- Figure 12: Asia Pacific Submarine Power Cable Industry Revenue (million), by Country 2025 & 2033

- Figure 13: Asia Pacific Submarine Power Cable Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Submarine Power Cable Industry Revenue (million), by Type of Current 2025 & 2033

- Figure 15: South America Submarine Power Cable Industry Revenue Share (%), by Type of Current 2025 & 2033

- Figure 16: South America Submarine Power Cable Industry Revenue (million), by Country 2025 & 2033

- Figure 17: South America Submarine Power Cable Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Submarine Power Cable Industry Revenue (million), by Type of Current 2025 & 2033

- Figure 19: Middle East and Africa Submarine Power Cable Industry Revenue Share (%), by Type of Current 2025 & 2033

- Figure 20: Middle East and Africa Submarine Power Cable Industry Revenue (million), by Country 2025 & 2033

- Figure 21: Middle East and Africa Submarine Power Cable Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Submarine Power Cable Industry Revenue million Forecast, by Type of Current 2020 & 2033

- Table 2: Global Submarine Power Cable Industry Revenue million Forecast, by Region 2020 & 2033

- Table 3: Global Submarine Power Cable Industry Revenue million Forecast, by Type of Current 2020 & 2033

- Table 4: Global Submarine Power Cable Industry Revenue million Forecast, by Country 2020 & 2033

- Table 5: Global Submarine Power Cable Industry Revenue million Forecast, by Type of Current 2020 & 2033

- Table 6: Global Submarine Power Cable Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: Global Submarine Power Cable Industry Revenue million Forecast, by Type of Current 2020 & 2033

- Table 8: Global Submarine Power Cable Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: Global Submarine Power Cable Industry Revenue million Forecast, by Type of Current 2020 & 2033

- Table 10: Global Submarine Power Cable Industry Revenue million Forecast, by Country 2020 & 2033

- Table 11: Global Submarine Power Cable Industry Revenue million Forecast, by Type of Current 2020 & 2033

- Table 12: Global Submarine Power Cable Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Submarine Power Cable Industry?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the Submarine Power Cable Industry?

Key companies in the market include ABB Ltd, Ningbo Orient Wires & Cables Co Ltd, ZTT International Limited, TFKable, Nexans SA, Furukawa Electric Co Ltd, NKT A/S, Prysmian Group, Sumitomo Electric Industries Limited, KEI Industries Limited, LS Cable & System Ltd.

3. What are the main segments of the Submarine Power Cable Industry?

The market segments include Type of Current.

4. Can you provide details about the market size?

The market size is estimated to be USD 33761.6 million as of 2022.

5. What are some drivers contributing to market growth?

HVDC submarine cables are increasingly preferred for long-distance power transmission due to their efficiency and lower energy losses compared to alternating current (AC) systems. The adoption of HVDC technology is a significant driver in the submarine power cable market..

6. What are the notable trends driving market growth?

There is a notable trend towards integrating renewable energy sources. such as offshore wind and solar power. into existing power grids. Submarine power cables play a crucial role in this integration by connecting remote renewable energy sites to onshore grids.

7. Are there any restraints impacting market growth?

The deployment and maintenance of submarine power cables involve substantial financial investments. The complex installation procedures. specialized equipment requirements. and the need for expert personnel contribute to these high costs..

8. Can you provide examples of recent developments in the market?

In November 2022, South Korea's leading cable manufacturer, LS Cable & System Ltd., became the largest shareholder of KT Submarine Co., a company specializing in undersea cable construction. This strategic investment aimed to strengthen LS Cable's position in the submarine cable market and expand its capabilities in undersea cable projects.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Submarine Power Cable Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Submarine Power Cable Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Submarine Power Cable Industry?

To stay informed about further developments, trends, and reports in the Submarine Power Cable Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence