Key Insights

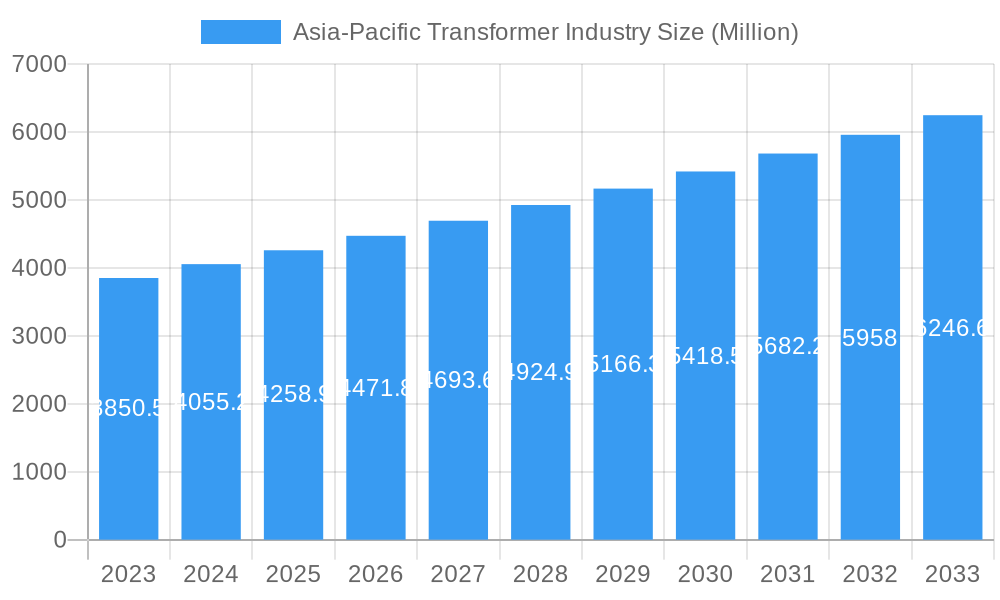

The Asia-Pacific transformer market is projected to reach USD 70.9 billion by 2025, exhibiting a strong compound annual growth rate (CAGR) of 9.95%. This expansion is driven by escalating electricity demand from burgeoning populations and rapid industrialization, particularly in China and India. The transition to renewable energy sources necessitates advanced transformer technologies for grid integration and power distribution. Government initiatives supporting grid modernization, rural electrification, and smart grid development are further stimulating market growth. An emphasis on energy efficiency and reduced transmission losses also bolsters demand for sophisticated and reliable transformer solutions.

Asia-Pacific Transformer Industry Market Size (In Billion)

Market segmentation highlights significant opportunities across various power ratings and cooling types. While large transformers will dominate due to large-scale power projects, medium and small transformers will experience consistent demand from distributed generation, commercial, and residential sectors. Air-cooled transformers are expected to lead due to cost-effectiveness and environmental benefits, although oil-cooled transformers remain crucial for high-capacity industrial and transmission systems. China and India will spearhead market growth, supported by extensive infrastructure development and rising power consumption. Japan's focus on advanced technology and grid modernization will also contribute significantly. Emerging trends include the integration of digital technologies for enhanced monitoring and predictive maintenance, development of compact and efficient designs, and a growing emphasis on sustainable materials and manufacturing processes.

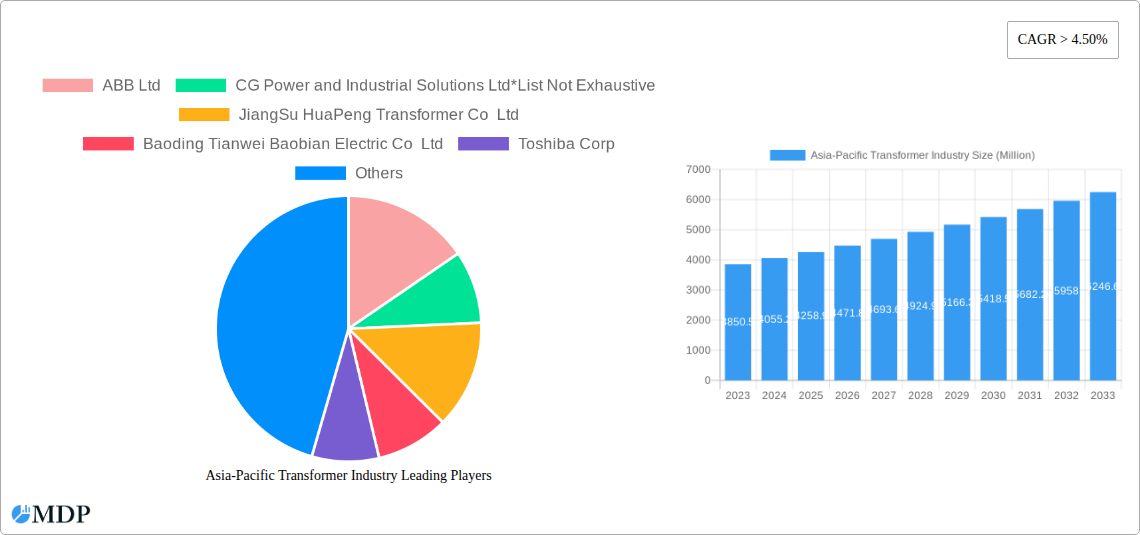

Asia-Pacific Transformer Industry Company Market Share

This comprehensive report offers a strategic analysis of the Asia-Pacific Transformer Industry, a vital sector supporting the region's economic expansion and energy transition. Covering the period from 2019 to 2033, with 2025 as the base and estimated year, and a forecast period of 2025-2033, this analysis examines market dynamics, industry trends, key segments, product advancements, growth drivers, challenges, emerging opportunities, and the competitive landscape. Utilizing high-traffic keywords such as "Asia-Pacific transformer market," "power transformer market," "distribution transformer market," "transformer manufacturing," and "electrical transformer industry," this report provides actionable insights for manufacturers, suppliers, investors, and policymakers. Key players examined include ABB Ltd, CG Power and Industrial Solutions Ltd, JiangSu HuaPeng Transformer Co Ltd, Baoding Tianwei Baobian Electric Co Ltd, Toshiba Corp, Hitachi Ltd, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, General Electric Company, and Panasonic Corporation.

Asia-Pacific Transformer Industry Market Dynamics & Concentration

The Asia-Pacific transformer industry exhibits a moderately concentrated market landscape, with a few dominant global players alongside a significant number of regional and local manufacturers. Innovation drivers are primarily focused on enhancing efficiency, reliability, and sustainability of transformers, driven by increasing grid modernization efforts and the integration of renewable energy sources. Regulatory frameworks, though varying by country, generally promote the adoption of advanced transformer technologies and stringent safety standards. Product substitutes are limited, with transformers being essential components in power transmission and distribution. End-user trends indicate a growing demand for smart transformers with advanced monitoring and control capabilities, as well as those designed for high-voltage direct current (HVDC) applications. Merger and acquisition (M&A) activities, though not at an extremely high volume, are strategically focused on expanding market reach, acquiring technological capabilities, and consolidating market share. The M&A deal count is estimated to be in the range of 10-15 over the forecast period, with market share of top 5 players hovering around 45-55%.

- Key Market Drivers:

- Aging grid infrastructure requiring upgrades and replacements.

- Rapid urbanization and industrialization boosting electricity demand.

- Government initiatives promoting renewable energy integration.

- Technological advancements in transformer design and materials.

- Key Restraints:

- High capital investment for new manufacturing facilities.

- Fluctuations in raw material prices, especially copper and steel.

- Complex regulatory approval processes in some countries.

- End-User Segmentation:

- Utilities (dominant segment).

- Industrial sector (manufacturing, mining, oil & gas).

- Commercial sector (data centers, large buildings).

- Renewable energy projects.

Asia-Pacific Transformer Industry Industry Trends & Analysis

The Asia-Pacific transformer industry is poised for robust growth, driven by an insatiable demand for electricity across its diverse economies and a monumental shift towards sustainable energy solutions. The compound annual growth rate (CAGR) for the overall market is projected to be approximately 6.8% during the forecast period. This expansion is fueled by extensive investments in power infrastructure, including the development of new power plants, the expansion of transmission and distribution networks, and the modernization of existing grids. Technological disruptions are playing a pivotal role, with a significant push towards smart transformers equipped with advanced monitoring, control, and communication capabilities, enabling better grid management and predictive maintenance. The increasing integration of renewable energy sources like solar and wind power necessitates transformers capable of handling intermittent power flows and voltage fluctuations, driving innovation in this space.

Consumer preferences are shifting towards energy-efficient and environmentally friendly transformer solutions. Manufacturers are investing in research and development to reduce losses, minimize environmental impact, and enhance the lifespan of their products. The competitive dynamics within the industry are intensifying, characterized by strategic partnerships, technological collaborations, and aggressive market penetration strategies by both established global players and emerging regional manufacturers. The report highlights that market penetration of advanced transformer technologies is expected to rise significantly, from an estimated 35% in the base year to over 55% by the end of the forecast period. Countries like China and India are leading this surge due to massive infrastructure development projects and ambitious renewable energy targets. The rising adoption of electric vehicles (EVs) is also creating a new demand segment for specialized transformers in charging infrastructure.

Leading Markets & Segments in Asia-Pacific Transformer Industry

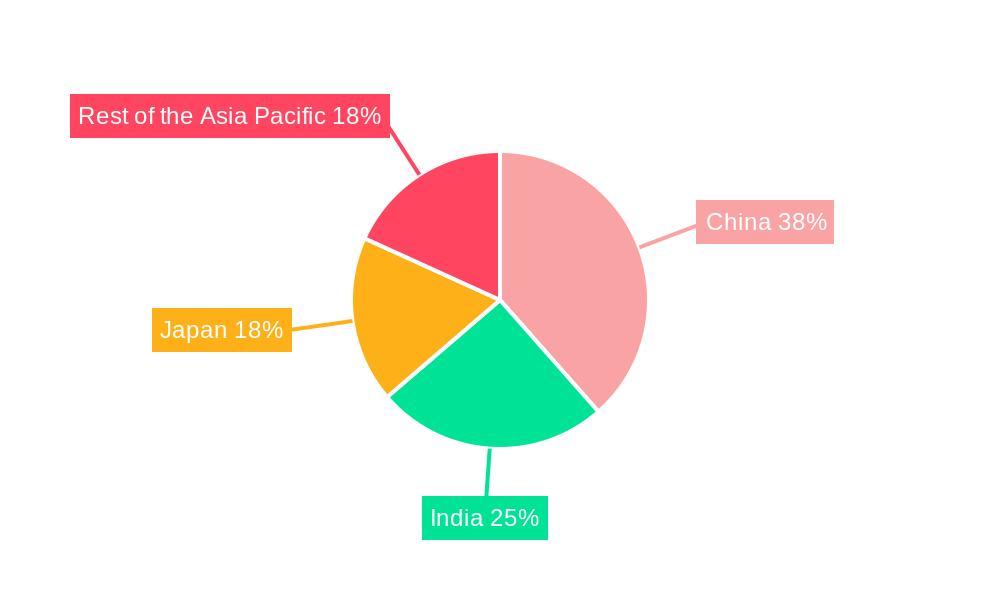

China emerges as the dominant market within the Asia-Pacific transformer industry, driven by its colossal manufacturing base, rapid urbanization, and extensive investments in both conventional and renewable energy infrastructure. The country's sheer scale of electricity consumption and its proactive stance on grid modernization make it a primary demand hub. India follows closely, characterized by its ambitious renewable energy targets, a growing industrial sector, and continuous efforts to electrify remote areas, all of which necessitate substantial transformer deployments. Japan, while a mature market, continues to be a significant contributor, focusing on high-end, technologically advanced transformers and grid resilience solutions, especially in the wake of natural disaster preparedness needs. The Rest of the Asia-Pacific region, encompassing countries like South Korea, Southeast Asian nations, and Australia, presents a mosaic of growth opportunities, each with unique drivers such as expanding industrialization, infrastructure development, and renewable energy adoption.

Among the transformer types, Power Transformers represent the largest segment by value, given their critical role in transmitting electricity over long distances from power generation sources. However, Distribution Transformers are witnessing substantial growth due to the ongoing expansion and upgrading of power distribution networks to meet the increasing demand from residential, commercial, and industrial consumers.

In terms of power rating, Large Power Transformers dominate the market share due to their application in major power generation and transmission substations. Nevertheless, Medium and Small Power Transformers are experiencing steady growth, driven by decentralized power generation, microgrids, and the increasing electrification of various industries.

For cooling types, Oil-Cooled Transformers remain the predominant technology due to their cost-effectiveness and superior cooling capabilities for high-capacity applications. However, Air-Cooled Transformers are gaining traction, particularly in indoor installations and where environmental concerns or fire safety are paramount, showcasing a trend towards more sustainable and environmentally conscious solutions.

- Dominant Regions:

- China: Massive infrastructure projects, smart grid initiatives, and leading renewable energy adoption.

- India: Significant government investment in power infrastructure, rural electrification, and renewable energy expansion.

- Leading Segments:

- Transformer Type: Power Transformers (due to transmission needs), Distribution Transformers (due to network expansion).

- Power Rating: Large Power Transformers (for core transmission), Medium and Small Power Transformers (for decentralized and industrial applications).

- Cooling Type: Oil-Cooled Transformers (dominant for high capacity), Air-Cooled Transformers (growing for specific applications).

Asia-Pacific Transformer Industry Product Developments

Product development in the Asia-Pacific transformer industry is sharply focused on enhancing efficiency, intelligence, and environmental sustainability. Manufacturers are innovating with advanced insulation materials and designs to reduce energy losses and prolong transformer life. The integration of digital technologies is leading to the development of smart transformers equipped with IoT sensors, real-time monitoring systems, and predictive analytics capabilities for enhanced grid management and fault detection. Furthermore, there's a growing emphasis on developing transformers that can seamlessly integrate with renewable energy sources, offering greater flexibility and responsiveness. Competitive advantages are being built through superior performance, enhanced safety features, reduced environmental footprint, and the ability to offer customized solutions for specific grid requirements.

Key Drivers of Asia-Pacific Transformer Industry Growth

The Asia-Pacific transformer industry's growth is propelled by several interconnected factors. Firstly, the escalating demand for electricity, fueled by population growth, urbanization, and industrial expansion, necessitates continuous investment in power generation, transmission, and distribution infrastructure. Secondly, the global imperative for decarbonization is driving massive investments in renewable energy sources, which require robust and adaptable transformer solutions for grid integration. Government policies and supportive regulatory frameworks, including subsidies and incentives for renewable energy and grid modernization, are further accelerating this growth. Technological advancements in transformer design, materials, and digital integration are enabling more efficient, reliable, and intelligent grid operations, creating a demand for newer, advanced transformer units.

Challenges in the Asia-Pacific Transformer Industry Market

Despite the robust growth prospects, the Asia-Pacific transformer industry faces several significant challenges. Intense competition, both from global giants and numerous local players, can lead to price wars and pressure on profit margins, estimated to impact profit margins by up to 15%. The fluctuating prices of key raw materials, such as copper, aluminum, and specialized steel, pose a significant risk to manufacturing costs and supply chain stability. Navigating complex and sometimes inconsistent regulatory landscapes across different countries can create hurdles for market entry and product standardization. Furthermore, the significant capital investment required for establishing and upgrading manufacturing facilities, coupled with the need for specialized skilled labor, presents a substantial barrier to entry for new players and requires continuous investment from existing ones, potentially exceeding USD 50 Million for new advanced facilities.

Emerging Opportunities in Asia-Pacific Transformer Industry

The Asia-Pacific transformer industry is ripe with emerging opportunities, primarily driven by the ongoing energy transition and digital transformation of power grids. The rapid expansion of renewable energy projects, particularly solar and wind farms, is creating a substantial demand for specialized transformers designed for grid integration and power conditioning. The global push towards smart grids presents a significant avenue for growth, with opportunities in developing and deploying intelligent transformers that offer advanced monitoring, control, and communication capabilities, thereby improving grid efficiency and reliability. The increasing adoption of electric vehicles (EVs) is spurring demand for transformers in charging infrastructure, both at commercial and residential levels. Furthermore, strategic partnerships and collaborations between technology providers and transformer manufacturers can unlock new markets and accelerate the development of cutting-edge solutions.

Leading Players in the Asia-Pacific Transformer Industry Sector

- ABB Ltd

- CG Power and Industrial Solutions Ltd

- JiangSu HuaPeng Transformer Co Ltd

- Baoding Tianwei Baobian Electric Co Ltd

- Toshiba Corp

- Hitachi Ltd

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- General Electric Company

- Panasonic Corporation

Key Milestones in Asia-Pacific Transformer Industry Industry

- October 2022: Hitachi Energy India announced that it has been given a contract by NTPC Renewable Energy, the wholly-owned subsidiary of Gujarat's future 4.75 gigawatts (GW) renewable energy plant, to provide power transformers, signaling a significant win in the renewable energy integration sector.

- February 2022: The Indian Ministry of Power and New and Renewable Energy approved a power distribution network project worth USD 4.12 billion under the Integrated Power Distribution Programme (IPDS). The program aims to improve the quality and reliability of power supply to consumers through a financially sustainable and operationally efficient distribution sector, a substantial development for the distribution transformer market.

Strategic Outlook for Asia-Pacific Transformer Industry Market

The strategic outlook for the Asia-Pacific transformer industry is exceptionally positive, characterized by sustained growth and a significant technological evolution. The ongoing massive investments in power infrastructure, coupled with the accelerating transition to renewable energy, will continue to be primary growth accelerators. The increasing adoption of smart grid technologies presents a substantial opportunity for manufacturers to innovate and differentiate by offering intelligent, connected transformer solutions. Strategic partnerships and collaborations will be crucial for market players to expand their technological capabilities, geographical reach, and product portfolios. Furthermore, a focus on developing energy-efficient and environmentally sustainable transformers will be key to meeting evolving regulatory demands and customer preferences, ensuring long-term market leadership and competitiveness in this vital industrial sector.

Asia-Pacific Transformer Industry Segmentation

-

1. Power Rating

- 1.1. Small

- 1.2. Large

- 1.3. Medium

-

2. Cooling Type

- 2.1. Air-Cooled

- 2.2. Oil-Cooled

-

3. Transformer Type

- 3.1. Power Transformer

- 3.2. Distribution Transformer

-

4. Geography

- 4.1. China

- 4.2. India

- 4.3. Japan

- 4.4. Rest of the Asia-Pacific

Asia-Pacific Transformer Industry Segmentation By Geography

- 1. China

- 2. India

- 3. Japan

- 4. Rest of the Asia Pacific

Asia-Pacific Transformer Industry Regional Market Share

Geographic Coverage of Asia-Pacific Transformer Industry

Asia-Pacific Transformer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.95% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Power Rating

- 5.1.1. Small

- 5.1.2. Large

- 5.1.3. Medium

- 5.2. Market Analysis, Insights and Forecast - by Cooling Type

- 5.2.1. Air-Cooled

- 5.2.2. Oil-Cooled

- 5.3. Market Analysis, Insights and Forecast - by Transformer Type

- 5.3.1. Power Transformer

- 5.3.2. Distribution Transformer

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. China

- 5.4.2. India

- 5.4.3. Japan

- 5.4.4. Rest of the Asia-Pacific

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. China

- 5.5.2. India

- 5.5.3. Japan

- 5.5.4. Rest of the Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Power Rating

- 6. Asia-Pacific Transformer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Power Rating

- 6.1.1. Small

- 6.1.2. Large

- 6.1.3. Medium

- 6.2. Market Analysis, Insights and Forecast - by Cooling Type

- 6.2.1. Air-Cooled

- 6.2.2. Oil-Cooled

- 6.3. Market Analysis, Insights and Forecast - by Transformer Type

- 6.3.1. Power Transformer

- 6.3.2. Distribution Transformer

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. China

- 6.4.2. India

- 6.4.3. Japan

- 6.4.4. Rest of the Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Power Rating

- 7. China Asia-Pacific Transformer Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Power Rating

- 7.1.1. Small

- 7.1.2. Large

- 7.1.3. Medium

- 7.2. Market Analysis, Insights and Forecast - by Cooling Type

- 7.2.1. Air-Cooled

- 7.2.2. Oil-Cooled

- 7.3. Market Analysis, Insights and Forecast - by Transformer Type

- 7.3.1. Power Transformer

- 7.3.2. Distribution Transformer

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. China

- 7.4.2. India

- 7.4.3. Japan

- 7.4.4. Rest of the Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Power Rating

- 8. India Asia-Pacific Transformer Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Power Rating

- 8.1.1. Small

- 8.1.2. Large

- 8.1.3. Medium

- 8.2. Market Analysis, Insights and Forecast - by Cooling Type

- 8.2.1. Air-Cooled

- 8.2.2. Oil-Cooled

- 8.3. Market Analysis, Insights and Forecast - by Transformer Type

- 8.3.1. Power Transformer

- 8.3.2. Distribution Transformer

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. China

- 8.4.2. India

- 8.4.3. Japan

- 8.4.4. Rest of the Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Power Rating

- 9. Japan Asia-Pacific Transformer Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Power Rating

- 9.1.1. Small

- 9.1.2. Large

- 9.1.3. Medium

- 9.2. Market Analysis, Insights and Forecast - by Cooling Type

- 9.2.1. Air-Cooled

- 9.2.2. Oil-Cooled

- 9.3. Market Analysis, Insights and Forecast - by Transformer Type

- 9.3.1. Power Transformer

- 9.3.2. Distribution Transformer

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. China

- 9.4.2. India

- 9.4.3. Japan

- 9.4.4. Rest of the Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Power Rating

- 10. Rest of the Asia Pacific Asia-Pacific Transformer Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Power Rating

- 10.1.1. Small

- 10.1.2. Large

- 10.1.3. Medium

- 10.2. Market Analysis, Insights and Forecast - by Cooling Type

- 10.2.1. Air-Cooled

- 10.2.2. Oil-Cooled

- 10.3. Market Analysis, Insights and Forecast - by Transformer Type

- 10.3.1. Power Transformer

- 10.3.2. Distribution Transformer

- 10.4. Market Analysis, Insights and Forecast - by Geography

- 10.4.1. China

- 10.4.2. India

- 10.4.3. Japan

- 10.4.4. Rest of the Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Power Rating

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 ABB Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 CG Power and Industrial Solutions Ltd*List Not Exhaustive

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 JiangSu HuaPeng Transformer Co Ltd

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Baoding Tianwei Baobian Electric Co Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Toshiba Corp

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Hitachi Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Mitsubishi Electric Corporation

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Siemens AG

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Schneider Electric SE

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 General Electric Company

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Panasonic Corporation

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.1 ABB Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Transformer Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Transformer Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Transformer Industry Revenue billion Forecast, by Power Rating 2020 & 2033

- Table 2: Asia-Pacific Transformer Industry Volume K Units Forecast, by Power Rating 2020 & 2033

- Table 3: Asia-Pacific Transformer Industry Revenue billion Forecast, by Cooling Type 2020 & 2033

- Table 4: Asia-Pacific Transformer Industry Volume K Units Forecast, by Cooling Type 2020 & 2033

- Table 5: Asia-Pacific Transformer Industry Revenue billion Forecast, by Transformer Type 2020 & 2033

- Table 6: Asia-Pacific Transformer Industry Volume K Units Forecast, by Transformer Type 2020 & 2033

- Table 7: Asia-Pacific Transformer Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Asia-Pacific Transformer Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 9: Asia-Pacific Transformer Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 10: Asia-Pacific Transformer Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 11: Asia-Pacific Transformer Industry Revenue billion Forecast, by Power Rating 2020 & 2033

- Table 12: Asia-Pacific Transformer Industry Volume K Units Forecast, by Power Rating 2020 & 2033

- Table 13: Asia-Pacific Transformer Industry Revenue billion Forecast, by Cooling Type 2020 & 2033

- Table 14: Asia-Pacific Transformer Industry Volume K Units Forecast, by Cooling Type 2020 & 2033

- Table 15: Asia-Pacific Transformer Industry Revenue billion Forecast, by Transformer Type 2020 & 2033

- Table 16: Asia-Pacific Transformer Industry Volume K Units Forecast, by Transformer Type 2020 & 2033

- Table 17: Asia-Pacific Transformer Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 18: Asia-Pacific Transformer Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 19: Asia-Pacific Transformer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Asia-Pacific Transformer Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 21: Asia-Pacific Transformer Industry Revenue billion Forecast, by Power Rating 2020 & 2033

- Table 22: Asia-Pacific Transformer Industry Volume K Units Forecast, by Power Rating 2020 & 2033

- Table 23: Asia-Pacific Transformer Industry Revenue billion Forecast, by Cooling Type 2020 & 2033

- Table 24: Asia-Pacific Transformer Industry Volume K Units Forecast, by Cooling Type 2020 & 2033

- Table 25: Asia-Pacific Transformer Industry Revenue billion Forecast, by Transformer Type 2020 & 2033

- Table 26: Asia-Pacific Transformer Industry Volume K Units Forecast, by Transformer Type 2020 & 2033

- Table 27: Asia-Pacific Transformer Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 28: Asia-Pacific Transformer Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 29: Asia-Pacific Transformer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Asia-Pacific Transformer Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 31: Asia-Pacific Transformer Industry Revenue billion Forecast, by Power Rating 2020 & 2033

- Table 32: Asia-Pacific Transformer Industry Volume K Units Forecast, by Power Rating 2020 & 2033

- Table 33: Asia-Pacific Transformer Industry Revenue billion Forecast, by Cooling Type 2020 & 2033

- Table 34: Asia-Pacific Transformer Industry Volume K Units Forecast, by Cooling Type 2020 & 2033

- Table 35: Asia-Pacific Transformer Industry Revenue billion Forecast, by Transformer Type 2020 & 2033

- Table 36: Asia-Pacific Transformer Industry Volume K Units Forecast, by Transformer Type 2020 & 2033

- Table 37: Asia-Pacific Transformer Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 38: Asia-Pacific Transformer Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 39: Asia-Pacific Transformer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Asia-Pacific Transformer Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 41: Asia-Pacific Transformer Industry Revenue billion Forecast, by Power Rating 2020 & 2033

- Table 42: Asia-Pacific Transformer Industry Volume K Units Forecast, by Power Rating 2020 & 2033

- Table 43: Asia-Pacific Transformer Industry Revenue billion Forecast, by Cooling Type 2020 & 2033

- Table 44: Asia-Pacific Transformer Industry Volume K Units Forecast, by Cooling Type 2020 & 2033

- Table 45: Asia-Pacific Transformer Industry Revenue billion Forecast, by Transformer Type 2020 & 2033

- Table 46: Asia-Pacific Transformer Industry Volume K Units Forecast, by Transformer Type 2020 & 2033

- Table 47: Asia-Pacific Transformer Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 48: Asia-Pacific Transformer Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 49: Asia-Pacific Transformer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Asia-Pacific Transformer Industry Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Transformer Industry?

The projected CAGR is approximately 9.95%.

2. Which companies are prominent players in the Asia-Pacific Transformer Industry?

Key companies in the market include ABB Ltd, CG Power and Industrial Solutions Ltd*List Not Exhaustive, JiangSu HuaPeng Transformer Co Ltd, Baoding Tianwei Baobian Electric Co Ltd, Toshiba Corp, Hitachi Ltd, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, General Electric Company, Panasonic Corporation.

3. What are the main segments of the Asia-Pacific Transformer Industry?

The market segments include Power Rating, Cooling Type, Transformer Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 70.9 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Natural Gas Demand4.; Rising Pipeline Network and Associated Infrastructure Development.

6. What are the notable trends driving market growth?

Distribution Transformer Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Shift toward Renewable Energy.

8. Can you provide examples of recent developments in the market?

October 2022: Hitachi Energy India announced that it has been given a contract by NTPC Renewable Energy, the wholly-owned subsidiary of Gujarat's future 4.75 gigawatts (GW) renewable energy plant, to provide power transformers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Transformer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Transformer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Transformer Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Transformer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence