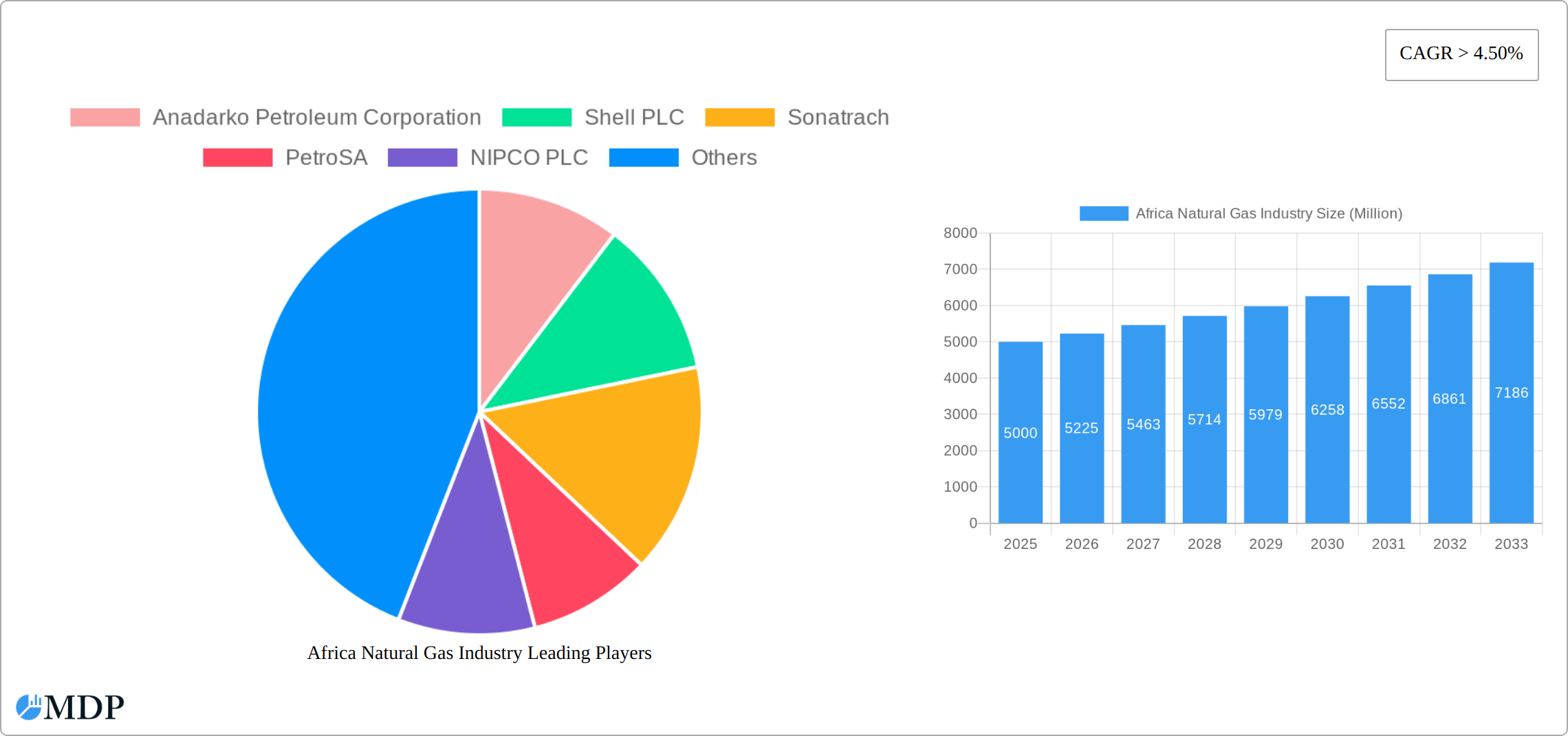

Key Insights

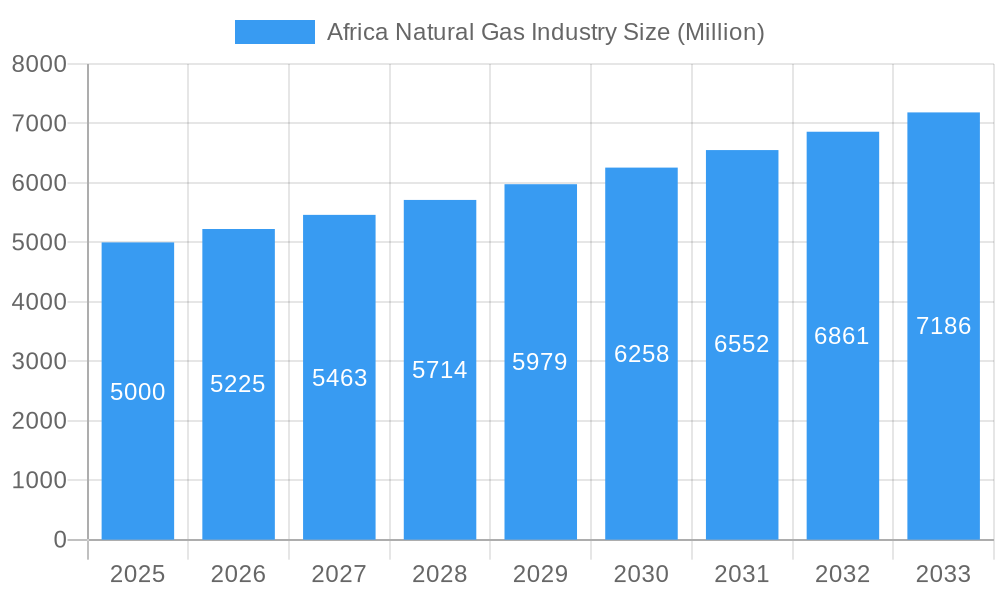

The African natural gas industry is experiencing robust growth, projected to maintain a Compound Annual Growth Rate (CAGR) exceeding 4.50% from 2025 to 2033. This expansion is fueled by several key drivers. Firstly, increasing energy demand across diverse sectors—power generation, industrial processes, and residential consumption—is creating a strong pull for natural gas as a cleaner and more efficient alternative to traditional fuels. Secondly, significant investments in infrastructure development, including pipelines and processing facilities, are enhancing the sector's capacity to meet this rising demand. Furthermore, supportive government policies aimed at diversifying energy sources and attracting foreign investment are playing a crucial role. However, challenges remain. These include the geographical complexities of infrastructure development across diverse African terrains, security concerns in certain regions impacting project implementation, and fluctuations in global natural gas prices.

Africa Natural Gas Industry Market Size (In Billion)

Despite these restraints, the market presents substantial opportunities, particularly in rapidly developing economies. South Africa, Sudan, Uganda, Tanzania, and Kenya represent key growth markets within the continent. Segment analysis reveals strong performance across all end-user categories, with power generation and industrial sectors anticipated as major consumers. Leading players like Shell PLC, TotalEnergies SE, and Sonatrach are actively involved, reflecting the industry's attractiveness. The market's segmentation further reveals opportunities across company sizes, with large, medium, and small companies all participating in the value chain. Looking ahead, focusing on sustainable practices, regional cooperation to overcome infrastructure hurdles, and consistent investment in exploration and production are crucial for unlocking the full potential of Africa's natural gas resources. The market’s size in 2025 is estimated at $XX million (assuming a plausible market size based on available information, but specifics need to be inserted).

Africa Natural Gas Industry Company Market Share

Africa Natural Gas Industry: Market Report 2019-2033

Unlocking the Potential of Africa's Natural Gas Sector: A Comprehensive Market Analysis

This comprehensive report provides an in-depth analysis of the Africa Natural Gas Industry, covering the period 2019-2033, with a focus on market dynamics, leading players, and future growth prospects. The report leverages extensive data analysis to offer actionable insights for industry stakeholders, investors, and policymakers. With a base year of 2025 and a forecast period extending to 2033, this study offers a crucial roadmap for navigating the complexities and opportunities within this dynamic sector.

Africa Natural Gas Industry Market Dynamics & Concentration

The African natural gas market presents a dynamic landscape shaped by a complex interplay of factors influencing its concentration, innovation, and overall growth trajectory. While a few multinational energy giants, including Shell PLC, TotalEnergies SE, and Eni SpA, hold substantial market share, creating a moderately concentrated market, the participation of numerous national oil companies (NOCs) and smaller independent players ensures a competitive environment. Innovation is pivotal, driven by the imperative for enhanced exploration and extraction technologies, improved infrastructure development (including pipeline networks and LNG facilities), and a growing emphasis on cleaner energy solutions to mitigate environmental impact. The regulatory landscape varies significantly across African nations, impacting investment decisions, market entry strategies, and overall operational efficiency. The rise of substitute fuels, particularly renewable energy sources, presents a notable challenge to natural gas's dominance, necessitating strategic adaptation and diversification within the industry. End-user demand is predominantly driven by power generation and industrial applications, although residential consumption is experiencing growth in specific regions. Mergers and acquisitions (M&A) activity has seen moderate levels in recent years, with approximately [Insert Precise Number] M&A deals recorded between 2019 and 2024, resulting in a [Insert Precise Percentage]% change in market share concentration. This activity reflects the ongoing consolidation and strategic repositioning within the sector.

- Market Share (Approximate, Year): Shell PLC ([Insert Percentage]%), TotalEnergies SE ([Insert Percentage]%), Eni SpA ([Insert Percentage]%), Others ([Insert Percentage]%)

- M&A Activity (2019-2024): [Insert Precise Number] deals, [Insert Precise Percentage]% change in market concentration

- Regulatory Frameworks: Diverse and often inconsistent across nations, influencing investment attractiveness and operational complexities.

- Product Substitutes: Renewable energy sources (solar, wind, hydro) pose a significant and increasing competitive threat, demanding strategic responses from natural gas companies.

- Innovation Drivers: Advanced exploration and extraction techniques (e.g., improved seismic imaging, horizontal drilling), efficient infrastructure development (e.g., pipeline optimization, LNG export terminals), and carbon capture, utilization, and storage (CCUS) technologies.

Africa Natural Gas Industry Industry Trends & Analysis

The African natural gas market is experiencing significant growth, driven by rising energy demand, expanding infrastructure, and increasing investment in exploration and production. The Compound Annual Growth Rate (CAGR) is projected at xx% during the forecast period (2025-2033), with market penetration increasing from xx% in 2025 to xx% in 2033. Technological disruptions, particularly in exploration and extraction technologies, are leading to increased efficiency and reduced costs. Consumer preferences are shifting towards cleaner energy solutions, prompting the adoption of gas-based technologies that produce fewer emissions. Competitive dynamics are shaping the market landscape with established players focusing on efficiency and innovation, while smaller companies seek niche opportunities.

Leading Markets & Segments in Africa Natural Gas Industry

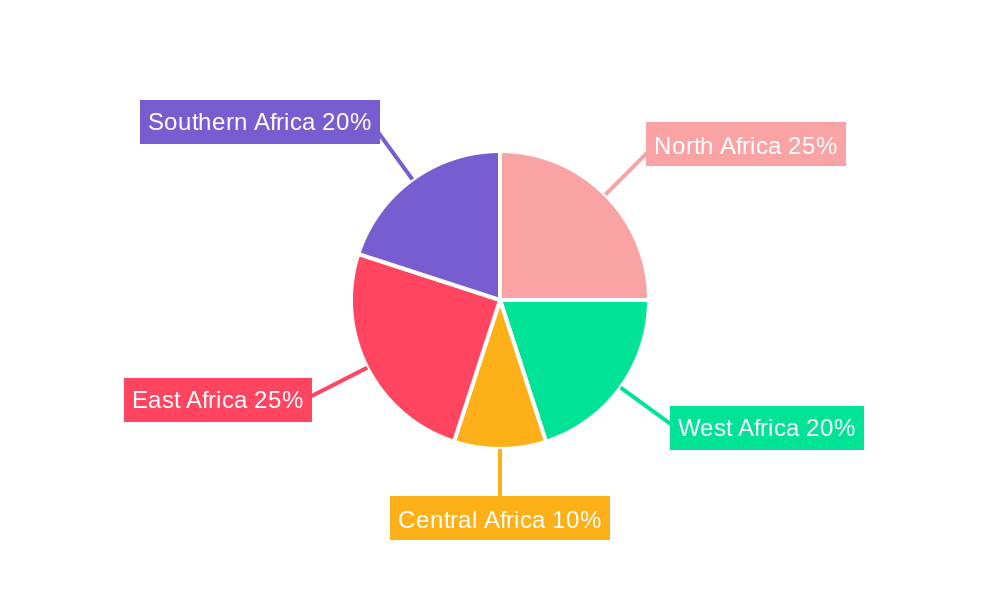

- Dominant Region: North Africa, driven by significant reserves and established infrastructure.

- Dominant Country: Algeria, due to its substantial gas reserves and export capabilities.

- Dominant End-User Segment: Power generation, due to growing electricity demands across the continent.

Key Drivers for Dominant Regions/Segments:

- North Africa: Existing infrastructure, established export routes, and substantial reserves.

- Algeria: Large gas reserves, established export infrastructure (Transmed pipeline), and government support.

- Power Generation: Increasing electricity demand and government initiatives to enhance energy access.

Detailed Dominance Analysis: North Africa's dominance stems from its mature infrastructure and extensive reserves, while Algeria benefits from its large gas fields and strategic location. Power generation remains the leading end-user segment because of rising electricity consumption.

Africa Natural Gas Industry Product Developments

Significant advancements in exploration and extraction technologies are unlocking previously inaccessible gas reserves across the African continent. Innovative solutions, including the application of advanced data analytics and automation, are being deployed to optimize efficiency, reduce operational costs, and minimize environmental footprints. A notable trend is the growing investment in liquefied natural gas (LNG) infrastructure, facilitating both domestic supply and the expansion of export capabilities to global markets. These technological advancements are significantly enhancing the market competitiveness of natural gas, particularly within the power generation and industrial sectors.

Key Drivers of Africa Natural Gas Industry Growth

The growth of Africa's natural gas industry is propelled by several key factors. The burgeoning energy demand fueled by rapid industrialization and sustained population growth represents a significant driver of consumption. Substantial investments in infrastructure development, encompassing pipeline networks, LNG processing facilities, and related infrastructure, are enhancing the sector's capacity and efficiency. Supportive government policies and regulatory frameworks, in regions where they exist, are encouraging exploration, production, and investment. Importantly, the discovery of new and substantial gas reserves provides a robust foundation for increased production and supply to meet growing demand.

Challenges in the Africa Natural Gas Industry Market

Despite its substantial potential, the African natural gas market faces several significant challenges. Inadequate infrastructure in many regions hinders effective distribution, leading to increased transportation costs and logistical hurdles. Political and regulatory uncertainties, including inconsistent policy environments and bureaucratic delays, can significantly impact investment decisions and exploration activities. The intensifying competition from renewable energy sources exerts continuous pressure on natural gas prices and market share, necessitating innovative responses. Security concerns, including pipeline vandalism and geopolitical instability in certain regions, pose risks to supply chain reliability and operational safety. These combined challenges contribute to an estimated [Insert Precise Percentage]% reduction in the industry's potential annual revenue.

Emerging Opportunities in Africa Natural Gas Industry

The African natural gas sector presents significant opportunities for growth. New discoveries of offshore and onshore reserves are creating potential for expansion and increased production. Strategic partnerships between international and national companies can boost investments and knowledge transfer. The development of regional gas pipelines and LNG infrastructure opens export opportunities to international markets. Government initiatives and investment in gas-related technologies can further promote the industry's development.

Leading Players in the Africa Natural Gas Industry Sector

- Anadarko Petroleum Corporation

- Shell PLC

- Sonatrach

- PetroSA

- NIPCO PLC

- TotalEnergies SE

- Egyptian Natural Gas Holding Company

- Eni SpA

- Nigerian National Petroleum Corporation

- Chevron Corporation

Key Milestones in Africa Natural Gas Industry Industry

- September 2022: Nigerian National Petroleum Company Limited (NNPCL) announced plans for a 7,000-kilometer Nigeria-Morocco gas pipeline, aiming to supply 3 Billion standard cubic feet of gas to Europe. This significantly expands export potential and regional cooperation.

- May 2022: Sonatrach and Eni signed an MoU to accelerate gas field development in Algeria, aiming for 3 Billion cubic meters of annual gas export via the Transmed pipeline. This signifies increased production and export capacity for Algeria.

Strategic Outlook for Africa Natural Gas Industry Market

The African natural gas market possesses substantial long-term potential. Sustained exploration and development of gas reserves, coupled with concerted efforts to improve infrastructure and foster regional cooperation, will be key drivers of future growth. Strategic partnerships between international energy companies and African NOCs, combined with targeted investments in advanced gas-related technologies, will be crucial for unlocking the sector's full potential. The market is well-positioned for significant expansion, presenting attractive investment opportunities for both domestic and international players who are prepared to navigate the complexities of the African energy landscape.

Africa Natural Gas Industry Segmentation

-

1. Geography

- 1.1. Nigeria

- 1.2. Algeria

- 1.3. Egypt

- 1.4. South Africa

- 1.5. Rest of Africa

Africa Natural Gas Industry Segmentation By Geography

- 1. Nigeria

- 2. Algeria

- 3. Egypt

- 4. South Africa

- 5. Rest of Africa

Africa Natural Gas Industry Regional Market Share

Geographic Coverage of Africa Natural Gas Industry

Africa Natural Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 4.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 5.1.1. Nigeria

- 5.1.2. Algeria

- 5.1.3. Egypt

- 5.1.4. South Africa

- 5.1.5. Rest of Africa

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Nigeria

- 5.2.2. Algeria

- 5.2.3. Egypt

- 5.2.4. South Africa

- 5.2.5. Rest of Africa

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 6. Africa Natural Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 6.1.1. Nigeria

- 6.1.2. Algeria

- 6.1.3. Egypt

- 6.1.4. South Africa

- 6.1.5. Rest of Africa

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 7. Nigeria Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 7.1.1. Nigeria

- 7.1.2. Algeria

- 7.1.3. Egypt

- 7.1.4. South Africa

- 7.1.5. Rest of Africa

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 8. Algeria Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 8.1.1. Nigeria

- 8.1.2. Algeria

- 8.1.3. Egypt

- 8.1.4. South Africa

- 8.1.5. Rest of Africa

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 9. Egypt Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 9.1.1. Nigeria

- 9.1.2. Algeria

- 9.1.3. Egypt

- 9.1.4. South Africa

- 9.1.5. Rest of Africa

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 10. South Africa Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 10.1.1. Nigeria

- 10.1.2. Algeria

- 10.1.3. Egypt

- 10.1.4. South Africa

- 10.1.5. Rest of Africa

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 11. Rest of Africa Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 11.1.1. Nigeria

- 11.1.2. Algeria

- 11.1.3. Egypt

- 11.1.4. South Africa

- 11.1.5. Rest of Africa

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Anadarko Petroleum Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Shell PLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sonatrach

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 PetroSA

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NIPCO PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 TotalEnergies SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Egyptian Natural Gas Holding Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Eni SpA

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nigerian National Petroleum Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Chevron Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Anadarko Petroleum Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Africa Natural Gas Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Africa Natural Gas Industry Share (%) by Company 2025

List of Tables

- Table 1: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 2: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 3: Africa Natural Gas Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Africa Natural Gas Industry Volume Tonnes Forecast, by Region 2020 & 2033

- Table 5: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 7: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 8: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 9: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 10: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 11: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 13: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 15: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 17: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 19: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 21: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 23: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Natural Gas Industry?

The projected CAGR is approximately > 4.50%.

2. Which companies are prominent players in the Africa Natural Gas Industry?

Key companies in the market include Anadarko Petroleum Corporation, Shell PLC, Sonatrach, PetroSA, NIPCO PLC, TotalEnergies SE, Egyptian Natural Gas Holding Company, Eni SpA, Nigerian National Petroleum Corporation, Chevron Corporation.

3. What are the main segments of the Africa Natural Gas Industry?

The market segments include Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Amount of Waste Generation. Growing Concern for Waste Management to Meet the Needs for Sustainable Urban Living4.; Increasing Focus on Non-fossil Fuel Sources of Energy.

6. What are the notable trends driving market growth?

Governments Moving Towards the Cleaner Energy Sources is Driving the Market.

7. Are there any restraints impacting market growth?

4.; Expensive Nature of Incinerators.

8. Can you provide examples of recent developments in the market?

In September 2022, The Nigerian National Petroleum Company Limited (NNPCL) announced its intention to sign a Memorandum of Understanding (MoU) on developing a gas pipeline with Morocco's National Office of Hydrocarbons and Mines and the commission of the Economic Community of West African States (ECOWAS). As a result of the MoU, the 7,000-kilometre Nigeria-Morocco gas pipeline project is expected to ramp up gas supply to Europe. Upon the project completion, 3 billion standard cubic feet of gas is expected to be supplied along the coast of West Africa from Nigeria, Benin, Togo, Ghana, Cote d'Ivoire, Liberia, Sierra Leone, Guinea, Guinea Bissau, Gambia, Senegal, Mauritania to Morocco.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Natural Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Natural Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Natural Gas Industry?

To stay informed about further developments, trends, and reports in the Africa Natural Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence