Key Insights

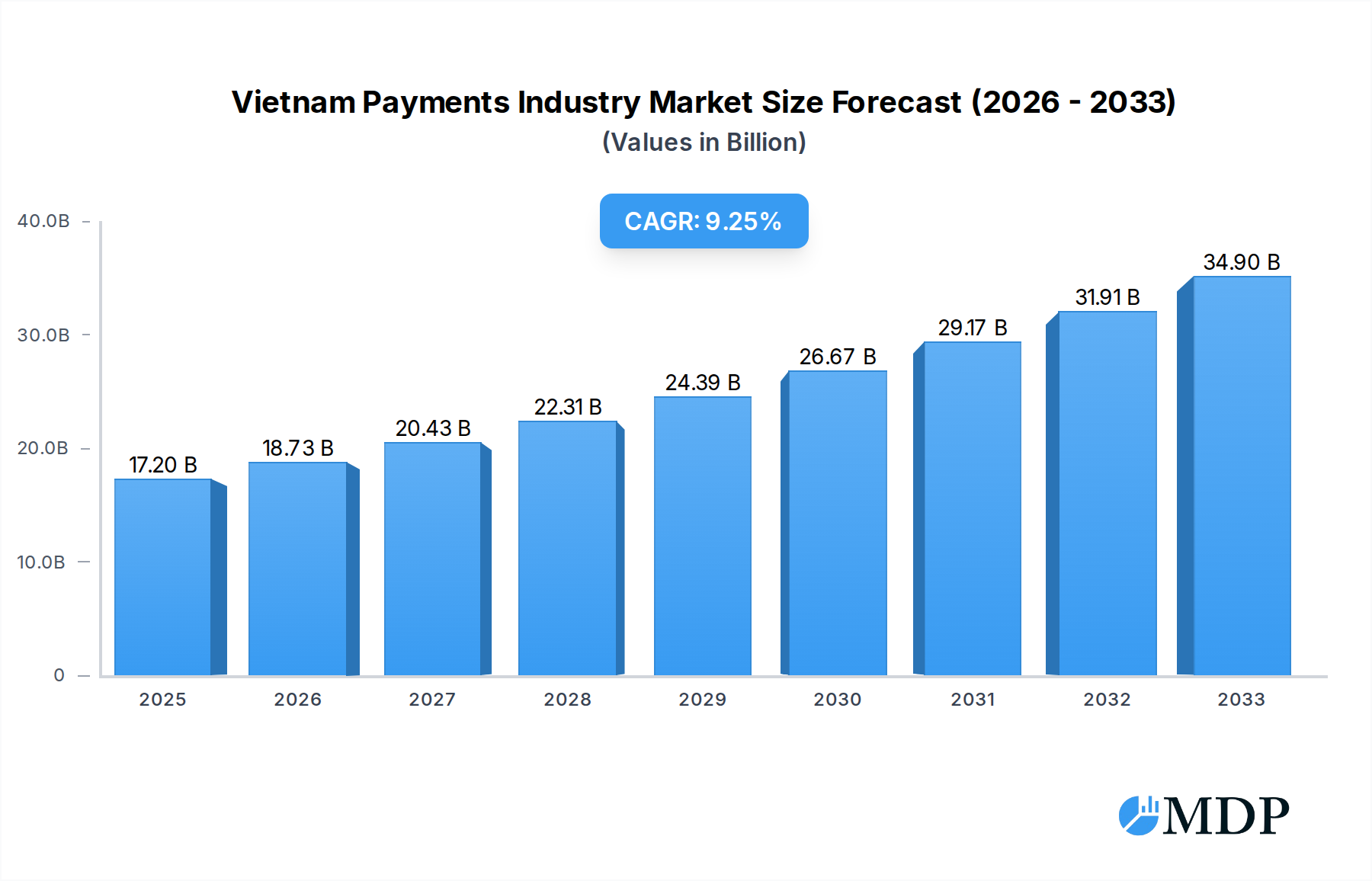

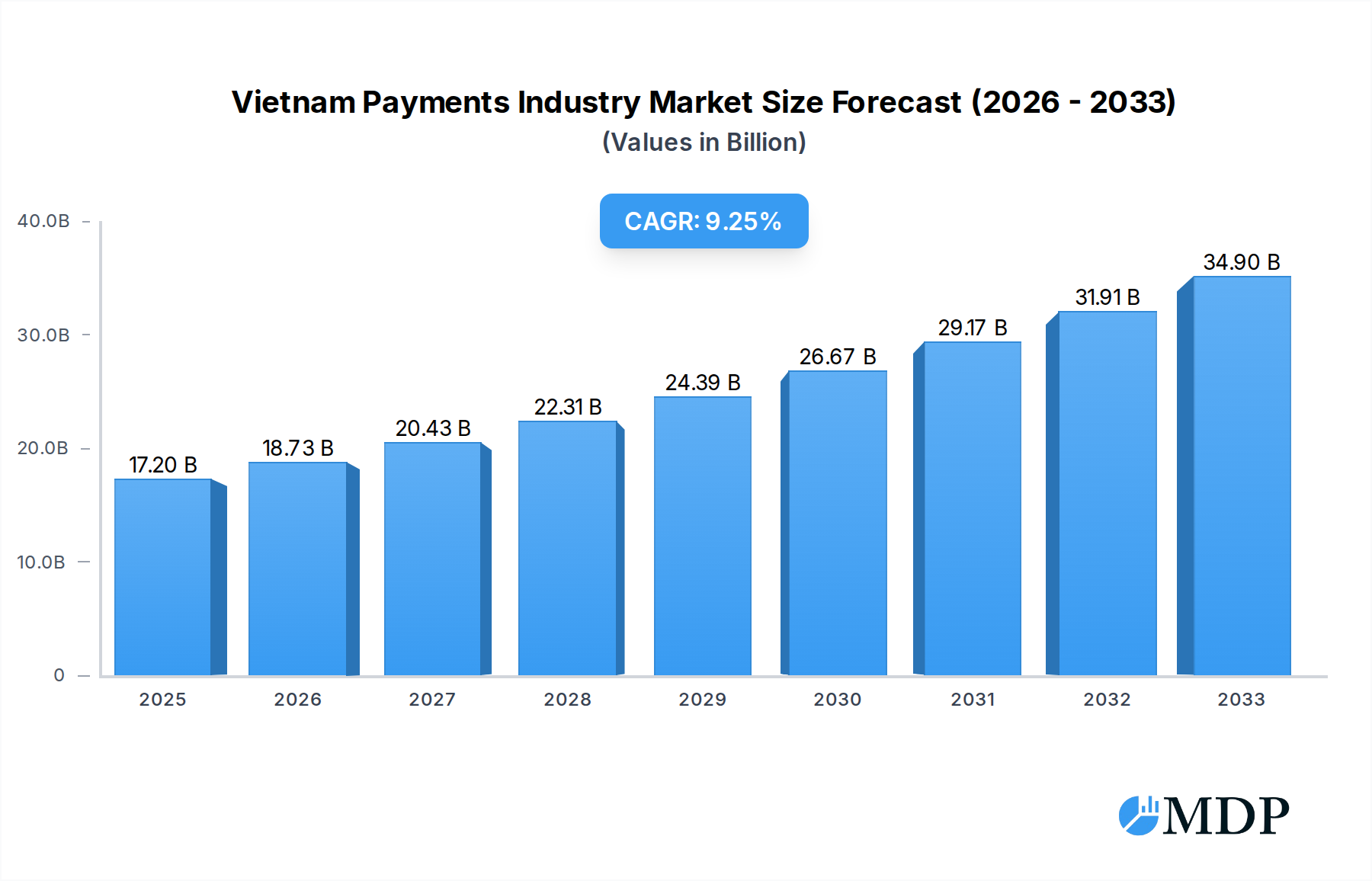

The Vietnam Payments Industry is experiencing robust growth, projected to reach an estimated USD 17.2 billion in 2025 with a compelling Compound Annual Growth Rate (CAGR) of 8.96% from 2025 to 2033. This expansion is propelled by a confluence of factors, including the increasing adoption of digital payment methods, a burgeoning young and tech-savvy population, and supportive government initiatives aimed at fostering a cashless society. The widespread availability of smartphones and internet connectivity across urban and rural areas further fuels this digital transformation. Key drivers include the rapid evolution of fintech solutions, enhanced security features bolstering consumer confidence, and the growing e-commerce landscape demanding seamless and convenient transaction experiences. Moreover, the hospitality and retail sectors are increasingly leveraging digital payments to streamline operations and improve customer satisfaction, contributing significantly to market expansion.

Vietnam Payments Industry Market Size (In Billion)

The market is characterized by a dynamic shift away from traditional cash transactions towards more sophisticated payment modes. Point of Sale (POS) transactions are seeing significant growth, with digital wallets, including mobile wallets, emerging as dominant forces, outpacing traditional card payments in many segments. Online sales, while still evolving, are also contributing to the overall growth, with the "Others" category for online payment methods indicating innovation and emerging solutions. Restraints, such as the digital divide in certain remote regions and lingering consumer trust concerns in some demographics, are gradually being addressed through greater financial literacy programs and improved cybersecurity infrastructure. The competitive landscape is vibrant, featuring established banking institutions like Vietcombank and VietinBank Group, alongside prominent fintech players such as VNPAY, MoMo, and ZaloPay, all vying for market share through innovative product offerings and strategic partnerships.

Vietnam Payments Industry Company Market Share

Vietnam Payments Industry Market Analysis: Unlocking Billion-Dollar Growth Opportunities (2019-2033)

Dive deep into the burgeoning Vietnam payments industry with this comprehensive market report. Explore key drivers, emerging trends, and strategic opportunities shaping this dynamic landscape. Understand the competitive ecosystem, from established banking giants to innovative digital wallet providers, and gain insights into the future of digital transactions in Vietnam. This report is an essential resource for payment processors, financial institutions, technology providers, investors, and all stakeholders seeking to capitalize on Vietnam's accelerating digital transformation.

Vietnam Payments Industry Market Dynamics & Concentration

The Vietnam payments industry is characterized by a dynamic market environment with significant growth potential, driven by increasing digital adoption and favorable government initiatives. Market concentration is evolving, with traditional financial institutions like Vietcombank and VietinBank Group holding substantial shares, while agile FinTech players such as VNPAY, MoMo, and ZaloPay rapidly gaining traction, particularly in the digital wallet segment. The competitive landscape is intensifying, fueled by innovation and strategic partnerships. Key innovation drivers include the proliferation of smartphones, expanding internet penetration, and a growing demand for convenient and secure payment solutions. Regulatory frameworks are progressively supporting the growth of digital payments, with initiatives aimed at fostering cashless transactions and enhancing financial inclusion. Product substitutes are emerging, with Buy Now Pay Later (BNPL) options gaining popularity alongside traditional card payments and cash. End-user trends indicate a strong preference for mobile-first payment experiences across various sectors, including retail, entertainment, and hospitality. Merger and acquisition (M&A) activities are on the rise as established players seek to acquire new technologies and expand their customer base, and FinTechs aim to scale their operations. For instance, there have been xx M&A deals recorded within the historical period (2019-2024), indicating robust consolidation and strategic realignment. Market share in the digital wallet segment is significantly influenced by user acquisition strategies and the breadth of services offered.

Vietnam Payments Industry Industry Trends & Analysis

The Vietnam payments industry is experiencing a period of robust expansion, propelled by a confluence of technological advancements, evolving consumer behavior, and proactive government policies. The market is projected to witness significant growth, with an estimated Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025–2033). This growth is underpinned by a rapidly expanding digital economy and increasing internet and smartphone penetration, which stood at xx% and xx% respectively in the base year 2025. Technological disruptions, such as the integration of Artificial Intelligence (AI) and Machine Learning (ML) for fraud detection and personalized financial services, are reshaping the payment landscape. Contactless payment technologies are gaining widespread adoption, particularly in urban centers, driven by enhanced security and convenience. Consumer preferences are shifting towards seamless, integrated payment experiences, favoring mobile wallets and online payment gateways over traditional cash transactions. The competitive dynamics are characterized by intense rivalry between established banks and agile FinTech startups. Companies like VNPAY are leveraging their extensive merchant networks, while MoMo and ZaloPay are focusing on expanding their service offerings to include bill payments, remittances, and e-commerce integrations. The government's commitment to promoting cashless payments, as evidenced by the scheme for the growth of cashless payment in Vietnam from 2021 to 2025, is a critical market growth driver. This initiative aims to make cashless payments a habit for citizens, progressively extending the reach to rural and remote areas, thereby fostering greater financial inclusion and reducing the reliance on cash. The penetration of digital payments in the retail sector alone is expected to reach xx% by 2033, signaling a profound transformation in consumer spending habits. The growing e-commerce market also acts as a significant catalyst, demanding efficient and secure online payment solutions.

Leading Markets & Segments in Vietnam Payments Industry

The Vietnam payments industry is segmented by modes of payment and end-user industries, with significant variations in dominance and growth potential. In terms of Mode of Payment, the Digital Wallet segment, encompassing mobile wallets, is emerging as the most dominant and fastest-growing category. This surge is propelled by its user-friendliness, extensive merchant acceptance, and the integration of value-added services. Mobile wallets, such as MoMo and ZaloPay, have achieved substantial market penetration, particularly among younger demographics and in urban areas, with an estimated xx% of all transactions occurring via digital wallets in 2025. Card Pay remains a significant player, especially in Point of Sale (POS) transactions, driven by the continuous expansion of POS terminal networks by banks like Vietcombank and VietinBank Group. However, its growth is being outpaced by digital wallets. Cash, while still prevalent in some segments and rural areas, is progressively declining as a primary payment method, aligning with the government's cashless initiatives.

Within End-user Industries, Retail is the largest and most impactful sector for payment services. The burgeoning e-commerce market and the increasing adoption of digital payments by brick-and-mortar stores are key drivers. Retailers are actively integrating various payment options to cater to diverse customer preferences. The Entertainment sector, encompassing online gaming, streaming services, and ticketing, also shows substantial growth, with a high propensity for digital transactions. Hospitality is another key segment witnessing a shift towards cashless payments, with hotels and restaurants adopting POS systems and mobile payment solutions to enhance guest experience. The Healthcare sector, while traditionally slower to adopt digital payments, is showing increasing potential for growth, driven by the demand for convenient appointment booking and bill payment solutions. The government’s focus on digital transformation across all sectors is expected to further accelerate the adoption of digital payments in these industries. Economic policies promoting digital adoption, the development of robust payment infrastructure, and targeted government incentives are crucial economic drivers contributing to the dominance of these segments.

Vietnam Payments Industry Product Developments

Product development in the Vietnam payments industry is heavily influenced by technological innovation and the pursuit of enhanced user experience. Key developments include the integration of biometric authentication for secure and swift transactions, the introduction of unified payment interfaces (UPIs) for seamless cross-platform payments, and the expansion of Buy Now Pay Later (BNPL) options to boost online sales. Mobile wallet providers are continuously rolling out new features, such as peer-to-peer transfers, bill payment aggregation, and loyalty program integrations, thereby increasing customer stickiness. Traditional banks are investing in upgrading their mobile banking applications, offering more intuitive interfaces and advanced functionalities. The focus is on creating an integrated ecosystem where payments are just one part of a broader digital financial service offering.

Key Drivers of Vietnam Payments Industry Growth

The Vietnam payments industry is experiencing remarkable growth driven by a trifecta of technological, economic, and regulatory factors. Technological advancements, particularly the widespread adoption of smartphones and high-speed internet, have laid the foundation for digital payment proliferation. The increasing availability of advanced payment technologies like QR codes, NFC, and contactless payments enhances convenience and security. Economic growth and a burgeoning middle class with higher disposable incomes are fueling consumer spending, with a growing preference for digital payment methods that offer speed and ease. The government's proactive regulatory stance and supportive policies, aimed at promoting a cashless society and fostering financial inclusion, are critical accelerators. Initiatives such as the national digital transformation program and specific schemes for cashless payment growth are creating a conducive environment for innovation and adoption.

Challenges in the Vietnam Payments Industry Market

Despite its rapid growth, the Vietnam payments industry faces several challenges that could temper its trajectory. Regulatory hurdles and evolving compliance requirements can pose complexities for FinTech companies and established institutions alike, especially concerning data privacy and anti-money laundering (AML) regulations. Cybersecurity threats remain a persistent concern, with the potential to erode consumer trust and lead to significant financial losses. Ensuring robust security measures for digital transactions is paramount. Infrastructure gaps, particularly in rural and remote areas, can limit the reach and adoption of digital payment services. While progress is being made, a significant portion of the population may still lack access to reliable internet or smartphone ownership. Intense competition among a growing number of players, including traditional banks, FinTech startups, and international players, can lead to pricing pressures and reduced profit margins.

Emerging Opportunities in Vietnam Payments Industry

The Vietnam payments industry is ripe with emerging opportunities poised to fuel long-term growth. The untapped potential in rural and semi-urban areas presents a significant market for expansion, offering opportunities for financial inclusion and the adoption of basic digital payment services. Strategic partnerships between FinTechs and traditional banks, as well as collaborations with e-commerce platforms and logistics providers, can create synergistic ecosystems and expand service offerings. Technological breakthroughs such as the increasing integration of AI for personalized financial advice and predictive analytics, and the exploration of blockchain technology for enhanced security and transparency, offer avenues for differentiation and innovation. The growing demand for specialized payment solutions for niche industries like agriculture, education, and healthcare, presents further avenues for market penetration and revenue generation.

Leading Players in the Vietnam Payments Industry Sector

- Vietcombank

- VNPAY

- MoMo

- ZaloPay

- Vietnam Bank for Agriculture and Rural Development

- PayPal

- VietinBank Group

- VTC pay

- Bank for Investment and Development of Vietnam

- Samsung Pay

Key Milestones in Vietnam Payments Industry Industry

- June 2022: Vietnam Posts and Telecommunications Group (VNPT) and the Joint Stock Commercial Bank for Foreign Trade of Vietnam (Vietcombank) inked a collaboration agreement (VNPT). This bilateral cooperation focuses on the development of digital payment services and platforms, signaling a significant step towards enhanced digital finance solutions.

- November 2021: Le Minh Khai, the Deputy Prime Minister, signed a resolution authorizing a scheme for the growth of cashless payment in Vietnam from 2021 to 2025. This pivotal initiative aims to promote cashless payment adoption, make it a habit for urban inhabitants, progressively expand to rural areas, and reduce cash-related expenditures, fundamentally shaping the market's future.

Strategic Outlook for Vietnam Payments Industry Market

The strategic outlook for the Vietnam payments industry is overwhelmingly positive, projecting continued robust expansion and transformation. The market is poised to benefit from the ongoing digital revolution, with increasing consumer adoption of digital payment methods. Key growth accelerators include the government's continued commitment to fostering a cashless society, which will drive further innovation in payment technologies and services. The increasing integration of FinTech solutions with traditional banking infrastructure will lead to more comprehensive and user-friendly financial ecosystems. Strategic opportunities lie in expanding digital payment services to underserved rural populations, developing specialized payment solutions for emerging industries, and leveraging AI and data analytics to enhance customer personalization and security. The evolving landscape suggests a future where digital payments are not just a convenience but an indispensable part of daily life in Vietnam.

Vietnam Payments Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Vietnam Payments Industry Segmentation By Geography

- 1. Vietnam

Vietnam Payments Industry Regional Market Share

Geographic Coverage of Vietnam Payments Industry

Vietnam Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Vietnam

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Vietnam Payments Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6.1.1. Point of Sale

- 6.1.1.1. Card Pay

- 6.1.1.2. Digital Wallet (includes Mobile Wallets)

- 6.1.1.3. Cash

- 6.1.1.4. Others

- 6.1.2. Online Sale

- 6.1.2.1. Others (

- 6.1.1. Point of Sale

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. Entertainment

- 6.2.3. Healthcare

- 6.2.4. Hospitality

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Vietcombank

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 VNPAY

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 MoMo

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ZaloPay*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Vietnam Bank for Agriculture and Rural Development

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PayPal

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 VietinBank Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 VTC pay

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Bank for Investment and Development of Vietnam

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Samsung Pay

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Vietcombank

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Vietnam Payments Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Vietnam Payments Industry Share (%) by Company 2025

List of Tables

- Table 1: Vietnam Payments Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 2: Vietnam Payments Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Vietnam Payments Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Vietnam Payments Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 5: Vietnam Payments Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Vietnam Payments Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vietnam Payments Industry?

The projected CAGR is approximately 8.96%.

2. Which companies are prominent players in the Vietnam Payments Industry?

Key companies in the market include Vietcombank, VNPAY, MoMo, ZaloPay*List Not Exhaustive, Vietnam Bank for Agriculture and Rural Development, PayPal, VietinBank Group, VTC pay, Bank for Investment and Development of Vietnam, Samsung Pay.

3. What are the main segments of the Vietnam Payments Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.2 billion as of 2022.

5. What are some drivers contributing to market growth?

High Proliferation of E-commerce. including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power; Enablement Programs by Key Retailers and Government encouraging digitization of the market; Growth of Real-time Payments. especially Buy Now Pay Later in the country.

6. What are the notable trends driving market growth?

Digital Wallets to Drive the Payment Market.

7. Are there any restraints impacting market growth?

High Installation Costs Coupled with Maintenance Costs.

8. Can you provide examples of recent developments in the market?

June 2022 - Vietnam Posts and Telecommunications Group (VNPT) and the Joint Stock Commercial Bank for Foreign Trade of Vietnam (Vietcombank) have inked a collaboration agreement (VNPT). The development of digital payment services and platforms is covered under this bilateral cooperation agreement.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vietnam Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vietnam Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vietnam Payments Industry?

To stay informed about further developments, trends, and reports in the Vietnam Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence