Key Insights

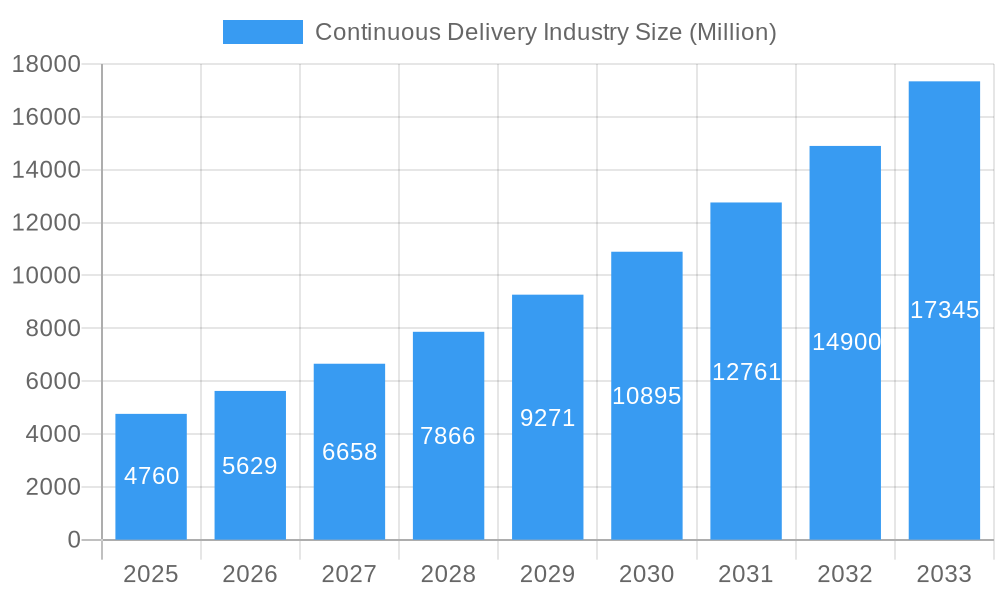

The Continuous Delivery market is poised for significant expansion, projected to reach an estimated $4.76 billion in 2025, with an impressive Compound Annual Growth Rate (CAGR) of 17.84% through 2033. This robust growth is fueled by the increasing adoption of DevOps practices across industries, driven by the imperative for faster software releases, improved application quality, and enhanced operational efficiency. Organizations are recognizing that streamlined and automated delivery pipelines are crucial for maintaining a competitive edge in today's rapidly evolving digital landscape. Key drivers include the growing complexity of software applications, the demand for continuous innovation, and the need to reduce time-to-market for new features and updates. The shift towards cloud-native architectures and microservices further propels the adoption of continuous delivery solutions, enabling greater agility and scalability.

Continuous Delivery Industry Market Size (In Billion)

The market is segmented across various deployment types, with both Cloud and On-premise solutions catering to diverse organizational needs. Large enterprises and small to medium-sized businesses (SMBs) alike are investing in continuous delivery tools and platforms to optimize their software development lifecycle. The end-user industry landscape is broad, with BFSI, Telecom and IT, Retail, Healthcare, Manufacturing, and Government sectors all recognizing the strategic importance of efficient software delivery. Emerging trends highlight the integration of AI and machine learning for intelligent automation within delivery pipelines, enhanced security integration (DevSecOps), and a greater focus on observability and feedback loops. While the market is experiencing strong momentum, challenges such as resistance to change within organizations, the need for skilled talent, and initial implementation costs could present minor headwinds for sustained, uninterrupted growth across all segments.

Continuous Delivery Industry Company Market Share

Continuous Delivery Industry Report: Accelerating Digital Transformation with Next-Gen Deployment Strategies (2019-2033)

This comprehensive Continuous Delivery Industry report delves into the dynamic landscape of modern software deployment, offering in-depth analysis and actionable insights for BFSI, Telecom and IT, Retail and Consumer Goods, Healthcare and Life Sciences, Manufacturing, and Government and Defense sectors. With a robust market size projected to reach hundreds of billions by 2033, this study covers the study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033. We explore the market dynamics, key trends, leading segments, product developments, growth drivers, challenges, and emerging opportunities shaping the future of CI/CD pipelines and DevOps solutions. The report provides an exhaustive overview of Cloud and On-premise deployment types, catering to Large Enterprises and Small and Medium-sized Enterprises, and highlights strategic initiatives from industry giants like Wipro Limited, Accenture PLC, Electric Cloud Inc (CloudBees Inc ), Atlassian Corporation PLC, Salesforce Inc, IBM Corporation (Red Hata Inc ), XebiaLabs (DIGITAL AI), Clarive Software Inc, Microsoft Corporation, Flexagon LLC, and Broadcom Inc (CA Technologie).

Continuous Delivery Industry Market Dynamics & Concentration

The Continuous Delivery Industry is characterized by a moderate to high market concentration, driven by the strategic dominance of a few key players and the increasing adoption of advanced DevOps practices. Innovation drivers are primarily fueled by the relentless demand for faster time-to-market, enhanced application reliability, and improved developer productivity. Regulatory frameworks, particularly within sensitive sectors like Healthcare and Life Sciences and Government and Defense, are increasingly influencing the adoption of standardized and secure continuous integration and continuous delivery (CI/CD) solutions. Product substitutes, such as traditional manual deployment methods, are rapidly losing ground as the efficiency and scalability of automated CD tools become undeniable. End-user trends underscore a significant shift towards cloud-native architectures and microservices, necessitating sophisticated continuous deployment strategies. Mergers and acquisitions (M&A) activities remain a significant force in shaping market concentration, with an estimated hundreds of deals annually focused on acquiring innovative DevOps platforms and expanding service portfolios. The market share of leading vendors is estimated to be in the tens of billions each, reflecting the substantial value chain within this sector.

Continuous Delivery Industry Industry Trends & Analysis

The Continuous Delivery Industry is experiencing exponential growth, with a projected Compound Annual Growth Rate (CAGR) of approximately 20-25% over the forecast period. This robust expansion is fundamentally driven by the pervasive need for accelerated digital transformation across all business verticals. Organizations are increasingly recognizing the strategic imperative of adopting DevOps methodologies to remain competitive in an agile marketplace. Technological disruptions, particularly the maturation of Kubernetes, containerization, and serverless computing, are acting as powerful catalysts, enabling more efficient and scalable continuous delivery pipelines. Consumer preferences are evolving towards applications that are constantly updated with new features and bug fixes, pushing companies to streamline their release cycles. The competitive dynamics within the industry are intensifying, with established players investing heavily in research and development of AI-powered CI/CD tools, predictive analytics for deployment success, and enhanced security features. Market penetration for continuous delivery solutions is rapidly increasing, with an estimated over 80% of Large Enterprises already implementing some form of CI/CD strategy, while Small and Medium-sized Enterprises are increasingly adopting these solutions to bridge the digital gap. The global market for continuous delivery is anticipated to surpass hundreds of billions in value by 2033, fueled by the constant evolution of software development and deployment paradigms.

Leading Markets & Segments in Continuous Delivery Industry

The Cloud deployment type currently dominates the Continuous Delivery Industry, accounting for an estimated over 70% of the market share, driven by its inherent scalability, flexibility, and cost-effectiveness. Within this segment, BFSI and Telecom and IT sectors are the leading end-user industries, collectively representing an estimated over 40% of the market revenue.

Deployment Type:

- Cloud: Dominant due to its ability to support rapid scaling, reduce infrastructure overhead, and facilitate remote collaboration essential for DevOps teams. Key drivers include the increasing adoption of cloud-native applications and the demand for agile development environments.

- On-premise: While experiencing slower growth, it remains relevant for organizations with stringent data security and regulatory compliance requirements, particularly in the Government and Defense and certain Healthcare and Life Sciences sub-segments.

Organization Size:

- Large Enterprises: Represent the largest market segment, leveraging continuous delivery to manage complex application portfolios, accelerate product innovation, and maintain competitive advantage. Their investment capacity and the scale of their operations make them prime adopters of comprehensive CI/CD platforms.

- Small and Medium-sized Enterprises (SMEs): Exhibiting the fastest growth rate, SMEs are increasingly adopting continuous delivery solutions to democratize access to advanced development practices and compete effectively with larger organizations.

End User Industry:

- BFSI: A frontrunner due to the critical need for rapid deployment of new financial services, enhanced security, and compliance with evolving regulations. The demand for real-time transaction processing and personalized customer experiences fuels the adoption of agile development and continuous delivery.

- Telecom and IT: Driven by the constant need for network upgrades, new service launches, and software-defined infrastructure management. The competitive landscape necessitates swift adaptation to market demands and rapid iteration of software solutions.

- Retail and Consumer Goods: Experiencing significant growth as businesses focus on e-commerce optimization, personalized customer journeys, and supply chain efficiency, all of which benefit from rapid software updates.

- Healthcare and Life Sciences: Adoption is accelerating due to the increasing digitization of healthcare records, the development of telehealth platforms, and the need for secure and compliant software updates for medical devices.

- Manufacturing: Increasingly leveraging continuous delivery for the Industrial Internet of Things (IIoT), smart factory solutions, and automation, aiming to improve operational efficiency and product quality.

- Government and Defense: Adopting CI/CD for modernization of legacy systems, development of secure citizen-facing applications, and rapid deployment of critical defense software, albeit with a more cautious and compliance-driven approach.

Continuous Delivery Industry Product Developments

The Continuous Delivery Industry is witnessing a surge in product innovations focused on enhancing automation, intelligence, and security within CI/CD pipelines. Key developments include the integration of AI and machine learning for predictive analytics in deployment success, automated testing across diverse environments, and intelligent remediation of deployment failures. Companies are emphasizing declarative continuous delivery services, offering greater control and transparency over release processes, as exemplified by Google Cloud Deploys. Furthermore, the emergence of continuous delivery-as-a-service (CDaaS) solutions aims to abstract away the complexity of underlying infrastructure, making advanced DevOps practices more accessible to a broader range of organizations, including SMEs. Competitive advantages are being built around seamless integration with existing toolchains, robust security features, and comprehensive observability capabilities, catering to the evolving needs of modern software development.

Key Drivers of Continuous Delivery Industry Growth

The Continuous Delivery Industry is propelled by several key drivers that are reshaping the software development landscape.

- Technological Advancements: The widespread adoption of cloud computing, microservices, containerization (Docker, Kubernetes), and serverless architectures directly necessitates efficient and automated continuous delivery pipelines.

- Business Agility and Time-to-Market: Organizations across all sectors are under immense pressure to innovate rapidly and deliver new features and updates to customers faster than their competitors. CI/CD is crucial for achieving this agility.

- Improved Software Quality and Reliability: Automated testing and continuous feedback loops inherent in continuous delivery lead to fewer bugs, higher application stability, and a better user experience, reducing downtime and associated costs.

- Cost Optimization: By automating manual processes, reducing errors, and enabling faster issue resolution, continuous delivery solutions contribute to significant operational cost savings.

Challenges in the Continuous Delivery Industry Market

Despite its rapid growth, the Continuous Delivery Industry faces several challenges that can hinder widespread adoption and impact market expansion.

- Cultural and Organizational Resistance: Shifting from traditional development methodologies to a DevOps culture requires significant changes in mindset, team structures, and collaboration, which can be a major hurdle for many organizations.

- Complexity of Integration: Integrating various CI/CD tools and aligning them with existing IT infrastructure can be complex and require specialized expertise, particularly for organizations with diverse legacy systems.

- Security and Compliance Concerns: Ensuring robust security measures and compliance with industry-specific regulations throughout the continuous delivery pipeline remains a critical concern for many businesses, especially in highly regulated sectors.

- Skill Gap: A shortage of skilled DevOps engineers and CI/CD specialists can impede the effective implementation and management of continuous delivery solutions.

Emerging Opportunities in Continuous Delivery Industry

Several emerging opportunities are poised to fuel long-term growth in the Continuous Delivery Industry. The increasing demand for AI-powered CI/CD tools that offer predictive analytics for release success and automated issue resolution presents a significant avenue for innovation. Strategic partnerships between DevOps tool providers and cloud service providers are creating more integrated and comprehensive solutions. Furthermore, the expansion of continuous delivery into new industries, such as the Internet of Medical Things (IoMT) and advanced manufacturing, offers substantial market penetration potential. The growing adoption of GitOps principles and the continued evolution of microservices architectures will also drive the need for more sophisticated and automated deployment strategies.

Leading Players in the Continuous Delivery Industry Sector

- Wipro Limited

- Accenture PLC

- Electric Cloud Inc (CloudBees Inc )

- Atlassian Corporation PLC

- Salesforce Inc

- IBM Corporation (Red Hata Inc )

- XebiaLabs (DIGITAL AI)

- Clarive Software Inc

- Microsoft Corporation

- Flexagon LLC

- Broadcom Inc (CA Technologie)

Key Milestones in Continuous Delivery Industry Industry

- February 2022: Google announced the GA release of Google Cloud Deploys, their managed continuous delivery service for the Google Kubernetes engine. The service offers declarative builds that stay with a given release, the ability to connect external workflows, and detailed security and auditing controls, enhancing the ease of adopting cloud-native CI/CD.

- January 2022: Harness created the first continuous delivery-as-a-service solution to tackle modern software delivery. With this launch, Harness aims to help enterprises and small businesses deploy new technologies faster and more confidently by abstracting away the complexity of new technologies, significantly broadening access to advanced CD capabilities.

Strategic Outlook for Continuous Delivery Industry Market

The strategic outlook for the Continuous Delivery Industry remains exceptionally bright, driven by the ongoing digital transformation initiatives across all global sectors. The market is expected to witness continued growth in the adoption of AI and machine learning within CI/CD platforms to enhance predictive capabilities and automation. The increasing demand for DevSecOps solutions, integrating security seamlessly into the development lifecycle, will also be a key growth accelerator. Furthermore, the expansion of continuous delivery into edge computing and IoT environments presents significant new market opportunities. Strategic investments in talent development and the creation of more user-friendly, integrated DevOps ecosystems will be crucial for sustained market leadership and value creation.

Continuous Delivery Industry Segmentation

-

1. Deployment Type

- 1.1. Cloud

- 1.2. On-premise

-

2. Organization Size

- 2.1. Large Enterprises

- 2.2. Small and Medium-sized Enterprises

-

3. End User Industry

- 3.1. BFSI

- 3.2. Telecom and IT

- 3.3. Retail and Consumer Goods

- 3.4. Healthcare and Life Sciences

- 3.5. Manufacturing

- 3.6. Government and Defense

- 3.7. Other End User Industries

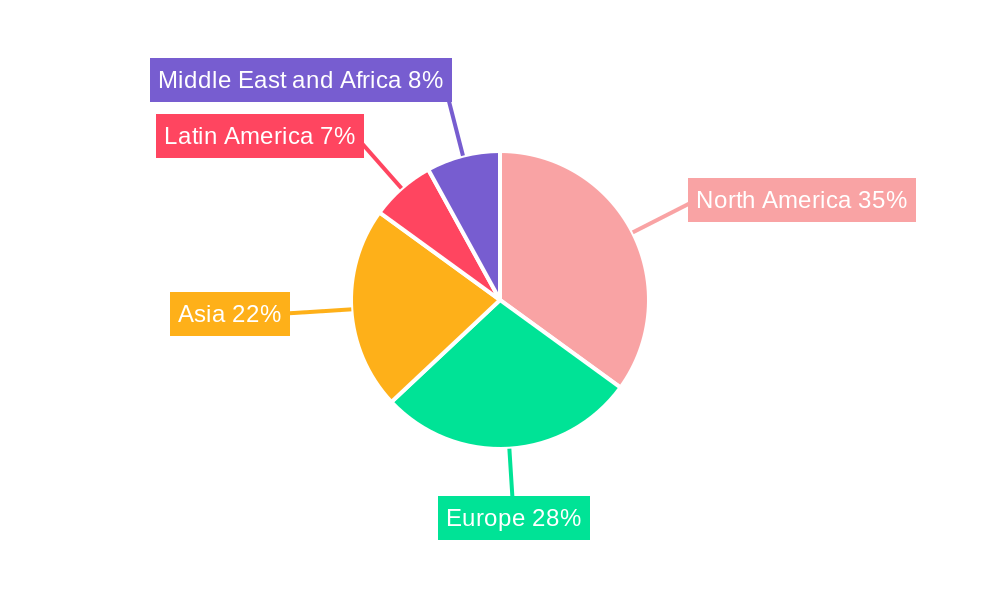

Continuous Delivery Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Latin America

- 5. Middle East and Africa

Continuous Delivery Industry Regional Market Share

Geographic Coverage of Continuous Delivery Industry

Continuous Delivery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 23.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand For Automation Across Business Processes; Increasing Adoption Of Cloud Technology

- 3.3. Market Restrains

- 3.3.1. Maintaining Data Security And Privacy

- 3.4. Market Trends

- 3.4.1. Increasing Adoption of Cloud Technology in the Continuous Delivery Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Continuous Delivery Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 5.1.1. Cloud

- 5.1.2. On-premise

- 5.2. Market Analysis, Insights and Forecast - by Organization Size

- 5.2.1. Large Enterprises

- 5.2.2. Small and Medium-sized Enterprises

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. BFSI

- 5.3.2. Telecom and IT

- 5.3.3. Retail and Consumer Goods

- 5.3.4. Healthcare and Life Sciences

- 5.3.5. Manufacturing

- 5.3.6. Government and Defense

- 5.3.7. Other End User Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6. North America Continuous Delivery Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6.1.1. Cloud

- 6.1.2. On-premise

- 6.2. Market Analysis, Insights and Forecast - by Organization Size

- 6.2.1. Large Enterprises

- 6.2.2. Small and Medium-sized Enterprises

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. BFSI

- 6.3.2. Telecom and IT

- 6.3.3. Retail and Consumer Goods

- 6.3.4. Healthcare and Life Sciences

- 6.3.5. Manufacturing

- 6.3.6. Government and Defense

- 6.3.7. Other End User Industries

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7. Europe Continuous Delivery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7.1.1. Cloud

- 7.1.2. On-premise

- 7.2. Market Analysis, Insights and Forecast - by Organization Size

- 7.2.1. Large Enterprises

- 7.2.2. Small and Medium-sized Enterprises

- 7.3. Market Analysis, Insights and Forecast - by End User Industry

- 7.3.1. BFSI

- 7.3.2. Telecom and IT

- 7.3.3. Retail and Consumer Goods

- 7.3.4. Healthcare and Life Sciences

- 7.3.5. Manufacturing

- 7.3.6. Government and Defense

- 7.3.7. Other End User Industries

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8. Asia Continuous Delivery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8.1.1. Cloud

- 8.1.2. On-premise

- 8.2. Market Analysis, Insights and Forecast - by Organization Size

- 8.2.1. Large Enterprises

- 8.2.2. Small and Medium-sized Enterprises

- 8.3. Market Analysis, Insights and Forecast - by End User Industry

- 8.3.1. BFSI

- 8.3.2. Telecom and IT

- 8.3.3. Retail and Consumer Goods

- 8.3.4. Healthcare and Life Sciences

- 8.3.5. Manufacturing

- 8.3.6. Government and Defense

- 8.3.7. Other End User Industries

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9. Latin America Continuous Delivery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9.1.1. Cloud

- 9.1.2. On-premise

- 9.2. Market Analysis, Insights and Forecast - by Organization Size

- 9.2.1. Large Enterprises

- 9.2.2. Small and Medium-sized Enterprises

- 9.3. Market Analysis, Insights and Forecast - by End User Industry

- 9.3.1. BFSI

- 9.3.2. Telecom and IT

- 9.3.3. Retail and Consumer Goods

- 9.3.4. Healthcare and Life Sciences

- 9.3.5. Manufacturing

- 9.3.6. Government and Defense

- 9.3.7. Other End User Industries

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10. Middle East and Africa Continuous Delivery Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10.1.1. Cloud

- 10.1.2. On-premise

- 10.2. Market Analysis, Insights and Forecast - by Organization Size

- 10.2.1. Large Enterprises

- 10.2.2. Small and Medium-sized Enterprises

- 10.3. Market Analysis, Insights and Forecast - by End User Industry

- 10.3.1. BFSI

- 10.3.2. Telecom and IT

- 10.3.3. Retail and Consumer Goods

- 10.3.4. Healthcare and Life Sciences

- 10.3.5. Manufacturing

- 10.3.6. Government and Defense

- 10.3.7. Other End User Industries

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Wipro Limited

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Accenture PLC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Electric Cloud Inc (CloudBees Inc )

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Atlassian Corporation PLC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Salesforce Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 IBM Corporation (Red Hata Inc )

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 XebiaLabs (DIGITAL AI)

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Clarive Software Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Microsoft Corporation

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Flexagon LLC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Broadcom Inc (CA Technologie)

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Wipro Limited

List of Figures

- Figure 1: Global Continuous Delivery Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Continuous Delivery Industry Revenue (undefined), by Deployment Type 2025 & 2033

- Figure 3: North America Continuous Delivery Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 4: North America Continuous Delivery Industry Revenue (undefined), by Organization Size 2025 & 2033

- Figure 5: North America Continuous Delivery Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 6: North America Continuous Delivery Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 7: North America Continuous Delivery Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 8: North America Continuous Delivery Industry Revenue (undefined), by Country 2025 & 2033

- Figure 9: North America Continuous Delivery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Continuous Delivery Industry Revenue (undefined), by Deployment Type 2025 & 2033

- Figure 11: Europe Continuous Delivery Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 12: Europe Continuous Delivery Industry Revenue (undefined), by Organization Size 2025 & 2033

- Figure 13: Europe Continuous Delivery Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 14: Europe Continuous Delivery Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 15: Europe Continuous Delivery Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 16: Europe Continuous Delivery Industry Revenue (undefined), by Country 2025 & 2033

- Figure 17: Europe Continuous Delivery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Continuous Delivery Industry Revenue (undefined), by Deployment Type 2025 & 2033

- Figure 19: Asia Continuous Delivery Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 20: Asia Continuous Delivery Industry Revenue (undefined), by Organization Size 2025 & 2033

- Figure 21: Asia Continuous Delivery Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 22: Asia Continuous Delivery Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 23: Asia Continuous Delivery Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 24: Asia Continuous Delivery Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Asia Continuous Delivery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Continuous Delivery Industry Revenue (undefined), by Deployment Type 2025 & 2033

- Figure 27: Latin America Continuous Delivery Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 28: Latin America Continuous Delivery Industry Revenue (undefined), by Organization Size 2025 & 2033

- Figure 29: Latin America Continuous Delivery Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 30: Latin America Continuous Delivery Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 31: Latin America Continuous Delivery Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 32: Latin America Continuous Delivery Industry Revenue (undefined), by Country 2025 & 2033

- Figure 33: Latin America Continuous Delivery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Continuous Delivery Industry Revenue (undefined), by Deployment Type 2025 & 2033

- Figure 35: Middle East and Africa Continuous Delivery Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 36: Middle East and Africa Continuous Delivery Industry Revenue (undefined), by Organization Size 2025 & 2033

- Figure 37: Middle East and Africa Continuous Delivery Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 38: Middle East and Africa Continuous Delivery Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 39: Middle East and Africa Continuous Delivery Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 40: Middle East and Africa Continuous Delivery Industry Revenue (undefined), by Country 2025 & 2033

- Figure 41: Middle East and Africa Continuous Delivery Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Continuous Delivery Industry Revenue undefined Forecast, by Deployment Type 2020 & 2033

- Table 2: Global Continuous Delivery Industry Revenue undefined Forecast, by Organization Size 2020 & 2033

- Table 3: Global Continuous Delivery Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 4: Global Continuous Delivery Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: Global Continuous Delivery Industry Revenue undefined Forecast, by Deployment Type 2020 & 2033

- Table 6: Global Continuous Delivery Industry Revenue undefined Forecast, by Organization Size 2020 & 2033

- Table 7: Global Continuous Delivery Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 8: Global Continuous Delivery Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: Global Continuous Delivery Industry Revenue undefined Forecast, by Deployment Type 2020 & 2033

- Table 10: Global Continuous Delivery Industry Revenue undefined Forecast, by Organization Size 2020 & 2033

- Table 11: Global Continuous Delivery Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 12: Global Continuous Delivery Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Global Continuous Delivery Industry Revenue undefined Forecast, by Deployment Type 2020 & 2033

- Table 14: Global Continuous Delivery Industry Revenue undefined Forecast, by Organization Size 2020 & 2033

- Table 15: Global Continuous Delivery Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 16: Global Continuous Delivery Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 17: Global Continuous Delivery Industry Revenue undefined Forecast, by Deployment Type 2020 & 2033

- Table 18: Global Continuous Delivery Industry Revenue undefined Forecast, by Organization Size 2020 & 2033

- Table 19: Global Continuous Delivery Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 20: Global Continuous Delivery Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 21: Global Continuous Delivery Industry Revenue undefined Forecast, by Deployment Type 2020 & 2033

- Table 22: Global Continuous Delivery Industry Revenue undefined Forecast, by Organization Size 2020 & 2033

- Table 23: Global Continuous Delivery Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 24: Global Continuous Delivery Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Continuous Delivery Industry?

The projected CAGR is approximately 23.6%.

2. Which companies are prominent players in the Continuous Delivery Industry?

Key companies in the market include Wipro Limited, Accenture PLC, Electric Cloud Inc (CloudBees Inc ), Atlassian Corporation PLC, Salesforce Inc, IBM Corporation (Red Hata Inc ), XebiaLabs (DIGITAL AI), Clarive Software Inc, Microsoft Corporation, Flexagon LLC, Broadcom Inc (CA Technologie).

3. What are the main segments of the Continuous Delivery Industry?

The market segments include Deployment Type, Organization Size, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand For Automation Across Business Processes; Increasing Adoption Of Cloud Technology.

6. What are the notable trends driving market growth?

Increasing Adoption of Cloud Technology in the Continuous Delivery Market.

7. Are there any restraints impacting market growth?

Maintaining Data Security And Privacy.

8. Can you provide examples of recent developments in the market?

February 2022: Google announced the GA release of Google Cloud Deploys, their managed continuous delivery service for the Google Kubernetes engine. The service offers declarative builds that stay with a given release, the ability to connect external workflows, and detailed security and auditing controls.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Continuous Delivery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Continuous Delivery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Continuous Delivery Industry?

To stay informed about further developments, trends, and reports in the Continuous Delivery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence