Key Insights

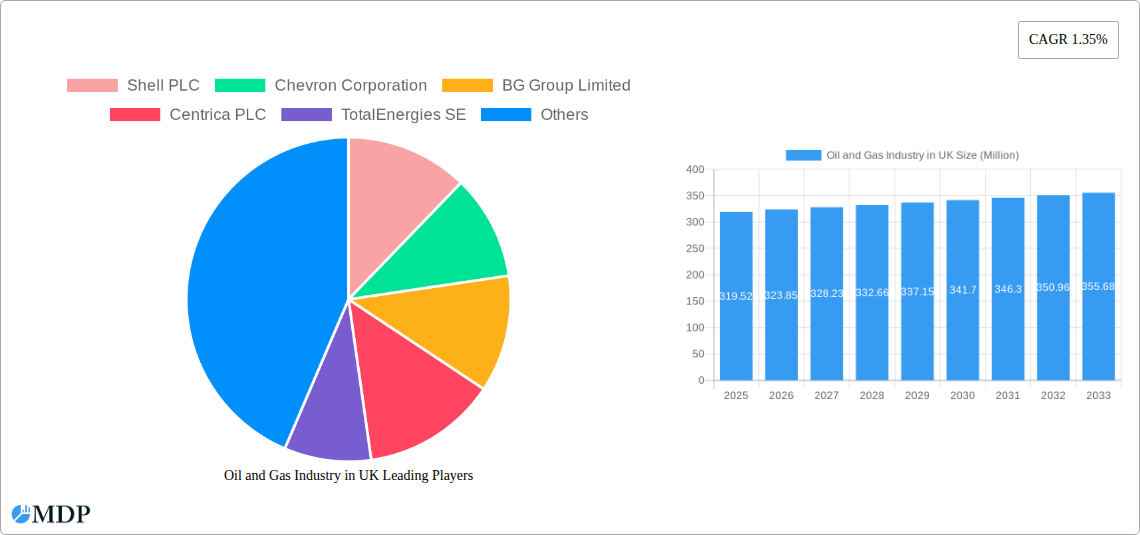

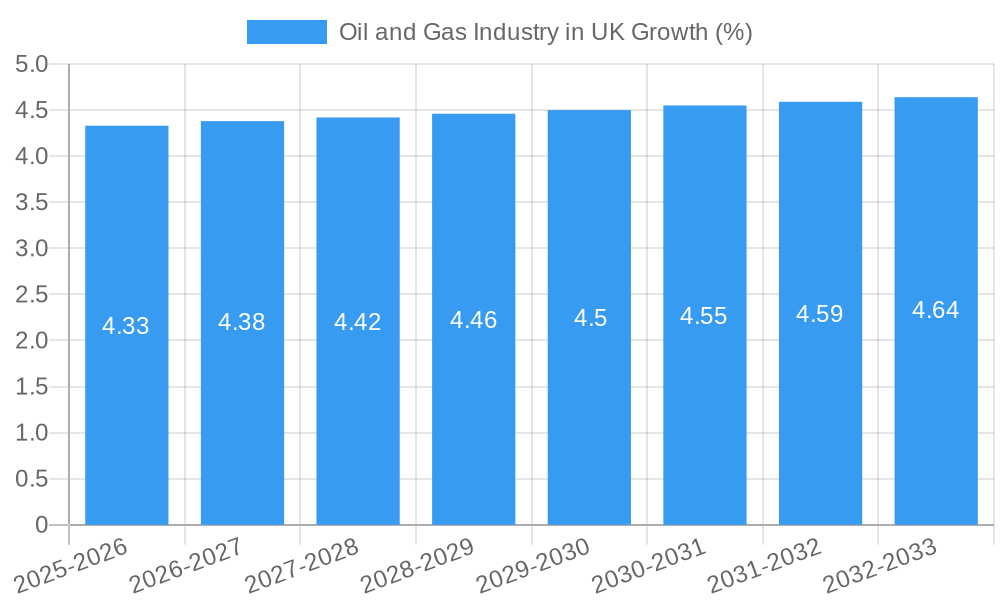

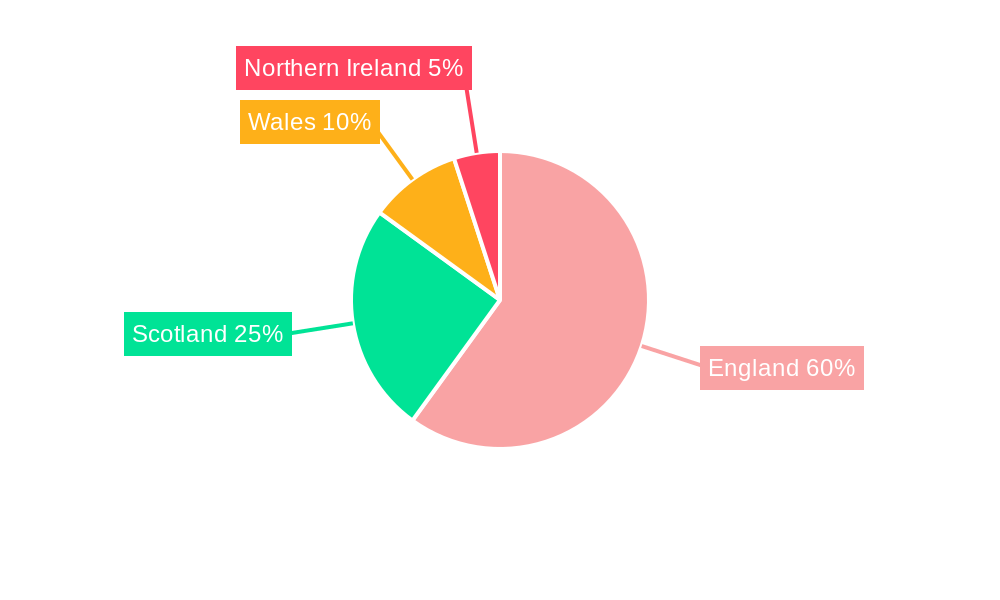

The UK oil and gas market, valued at £319.52 million in 2025, is projected to experience modest growth over the forecast period (2025-2033), with a Compound Annual Growth Rate (CAGR) of 1.35%. This relatively low growth reflects a complex interplay of factors. The upstream sector, encompassing exploration and production, faces challenges from declining North Sea reserves and increasing operational costs. While technological advancements in enhanced oil recovery and exploration techniques offer some potential for growth, the sector is likely to remain relatively stagnant, especially considering the UK's commitment to reducing carbon emissions. The midstream sector, focused on transportation and storage, faces pressure to adapt to changing energy demands and potentially decreasing volumes of oil and gas to handle. Investment in infrastructure upgrades and diversification of energy sources will be critical to maintain profitability in this segment. The downstream sector, encompassing refining and marketing, will likely exhibit more resilience due to persistent demand for refined products, however, pressure to transition towards cleaner energy sources and the promotion of electric vehicles might affect long-term growth. Major players such as Shell, BP, and TotalEnergies, along with smaller companies like Dana Petroleum, will need to strategically navigate these challenges by investing in renewable energy projects, optimizing operations, and pursuing strategic mergers and acquisitions to maintain their market share. Regional variations are expected, with England likely to maintain the largest share, followed by Scotland, Wales, and Northern Ireland. The government's policies regarding energy transition will significantly influence market trajectories, presenting opportunities for companies that successfully adapt to a lower-carbon future.

The historical period (2019-2024) likely saw a period of fluctuating market size, influenced by global oil price volatility and increased regulatory scrutiny. The current CAGR of 1.35% suggests a continued but gradual growth trend. This growth is likely to be driven by factors such as sustained domestic demand for energy, despite the increasing push for renewable energy sources, and strategic investments in infrastructure maintenance and upgrades. However, constraints include aging infrastructure in the North Sea, increasing environmental regulations, and pressure to transition towards cleaner energy sources. The market segmentation will remain crucial, with differing growth prospects depending on the sector. Competition remains fierce, requiring companies to focus on operational efficiency and innovation to remain competitive. The geographical distribution of oil and gas activities within the UK (England, Scotland, Wales, Northern Ireland) will continue to shape regional market dynamics.

UK Oil & Gas Industry Report: 2019-2033 Forecast

Unlocking Growth Opportunities in the UK's Dynamic Energy Sector

This comprehensive report provides an in-depth analysis of the UK oil and gas industry, offering invaluable insights for stakeholders across the upstream, midstream, and downstream sectors. With a focus on the 2019-2033 period (Base Year: 2025, Forecast Period: 2025-2033), this study examines market dynamics, leading players, technological advancements, and emerging opportunities. Discover actionable intelligence to navigate the complexities of this evolving landscape and capitalize on future growth. Market values are expressed in millions.

Oil and Gas Industry in UK Market Dynamics & Concentration

The UK oil and gas market exhibits a moderately concentrated structure, with major players like BP PLC, Shell PLC, and TotalEnergies SE holding significant market share, particularly in the upstream sector. However, the presence of smaller independent companies and increasing M&A activity contribute to a dynamic competitive landscape. Innovation is driven by the need for improved efficiency, enhanced safety measures, and reduced environmental impact. Stringent regulatory frameworks, including emissions reduction targets and licensing requirements, significantly influence industry operations. The rise of renewable energy sources presents a growing competitive pressure, acting as a substitute for traditional fossil fuels. End-user trends reveal a growing preference for cleaner energy sources, pushing oil and gas companies to diversify and adopt sustainable practices.

- Market Share (2024 Estimate): BP PLC (xx%), Shell PLC (xx%), TotalEnergies SE (xx%), Others (xx%).

- M&A Deal Count (2019-2024): xx deals.

- Key Regulatory Frameworks: OGUK (Oil and Gas UK) guidelines, UK government energy policies, EU regulations (where applicable).

Oil and Gas Industry in UK Industry Trends & Analysis

The UK oil and gas industry is experiencing a period of transformation driven by several key trends. Market growth is influenced by fluctuating global oil and gas prices, domestic energy demand, and government policies promoting energy security. Technological advancements, particularly in digitalization and automation, are improving operational efficiency and reducing costs. Consumer preferences are shifting towards cleaner energy solutions, necessitating a focus on emissions reduction and sustainable practices. Competitive dynamics are intense, driven by both established players and emerging companies entering the market.

- CAGR (2025-2033): xx% (Upstream), xx% (Midstream), xx% (Downstream).

- Market Penetration of Renewables (2024): xx%

Leading Markets & Segments in Oil and Gas Industry in UK

The North Sea remains a dominant region for upstream activities, driven by significant reserves and established infrastructure. The midstream segment exhibits strong growth, spurred by investments in pipeline networks and gas storage facilities. The downstream sector is marked by significant refining capacity and a well-developed distribution network catering to various end users.

Upstream:

- Key Drivers: North Sea reserves, technological advancements in offshore exploration, government incentives.

Midstream:

- Key Drivers: Investments in pipeline infrastructure, growing gas storage capacity, strategic partnerships.

Downstream:

- Key Drivers: Strong refining capacity, established distribution networks, demand from transportation and industrial sectors.

Oil and Gas Industry in UK Product Developments

Recent product developments emphasize improved efficiency, enhanced safety, and reduced environmental impact. This includes the adoption of advanced drilling technologies, optimized pipeline management systems, and cleaner refining processes. The integration of AI and big data analytics is playing a crucial role in enhancing exploration and production efficiency. These innovations are enhancing operational efficiency and enabling companies to better adapt to changing market conditions.

Key Drivers of Oil and Gas Industry in UK Growth

Growth in the UK oil and gas industry is propelled by several factors. Technological innovations, like AI-powered exploration and improved extraction techniques, are boosting efficiency and reducing costs. Continued domestic demand for energy, particularly natural gas, supports market growth. Supportive government policies aimed at ensuring energy security, and investment in infrastructure development play a vital role.

Challenges in the Oil and Gas Industry in UK Market

The UK oil and gas sector faces several significant hurdles. Stringent environmental regulations place increasing pressure on emissions reduction, potentially impacting profitability. Supply chain disruptions can cause operational delays and increased costs. Intense competition from renewable energy sources presents a significant challenge for market share. These factors combined pose challenges to the long term growth of the industry.

Emerging Opportunities in Oil and Gas Industry in UK

The UK oil and gas sector is poised for growth through several opportunities. Investment in carbon capture and storage technologies offers a pathway for emissions reduction. Strategic partnerships between oil and gas companies and renewable energy providers create synergies, and expansion into new markets, perhaps focusing on specific niche products or services, provides pathways for additional growth.

Leading Players in the Oil and Gas Industry in UK Sector

- Shell PLC

- Chevron Corporation

- BP PLC

- ESSO UK Limited

- TotalEnergies SE

- Centrica PLC

- Cadent Gas Ltd

- BG Group Limited (now part of Shell)

- Valaris PLC

- Dana Petroleum E&P Limited

Key Milestones in Oil and Gas Industry in UK Industry

- May 2023: Shell PLC partners with SparkCognition to leverage AI for enhanced offshore oil exploration and production.

- May 2022: BP PLC announces a USD 22.5 billion investment in North Sea oil and gas fields to boost production and improve efficiency.

Strategic Outlook for Oil and Gas Industry in UK Market

The future of the UK oil and gas industry hinges on its ability to adapt to evolving market demands and technological advancements. A focus on emissions reduction, strategic partnerships, and investment in innovative technologies will be crucial for long-term success. The industry's potential for growth lies in its ability to position itself as a provider of energy solutions that support the transition towards a lower-carbon future.

Oil and Gas Industry in UK Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

Oil and Gas Industry in UK Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Russia

- 1.7. Benelux

- 1.8. Nordics

- 1.9. Rest of Europe

Oil and Gas Industry in UK REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 1.35% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Domestic Oil and Gas Production4.; Investments in Oil and Gas Infrastructure Development

- 3.3. Market Restrains

- 3.3.1. 4.; Growth of Renewable Energy

- 3.4. Market Trends

- 3.4.1. Upstream Segment Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. England Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 7. Wales Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 8. Scotland Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 9. Northern Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 10. Ireland Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Shell PLC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Chevron Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BG Group Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Centrica PLC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 TotalEnergies SE

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Cadent Gas Ltd

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 BP PLC

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ESSO UK Limited

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Valaris PLC

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Dana Petroleum E&P Limited

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Shell PLC

List of Figures

- Figure 1: Oil and Gas Industry in UK Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Oil and Gas Industry in UK Share (%) by Company 2024

List of Tables

- Table 1: Oil and Gas Industry in UK Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Oil and Gas Industry in UK Revenue Million Forecast, by Sector 2019 & 2032

- Table 3: Oil and Gas Industry in UK Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Oil and Gas Industry in UK Revenue Million Forecast, by Country 2019 & 2032

- Table 5: England Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Wales Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Scotland Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Northern Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Ireland Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Oil and Gas Industry in UK Revenue Million Forecast, by Sector 2019 & 2032

- Table 11: Oil and Gas Industry in UK Revenue Million Forecast, by Country 2019 & 2032

- Table 12: United Kingdom Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Germany Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Italy Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Spain Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Russia Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Benelux Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Nordics Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Europe Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil and Gas Industry in UK?

The projected CAGR is approximately 1.35%.

2. Which companies are prominent players in the Oil and Gas Industry in UK?

Key companies in the market include Shell PLC, Chevron Corporation, BG Group Limited, Centrica PLC, TotalEnergies SE, Cadent Gas Ltd, BP PLC, ESSO UK Limited, Valaris PLC, Dana Petroleum E&P Limited.

3. What are the main segments of the Oil and Gas Industry in UK?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 319.52 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Domestic Oil and Gas Production4.; Investments in Oil and Gas Infrastructure Development.

6. What are the notable trends driving market growth?

Upstream Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growth of Renewable Energy.

8. Can you provide examples of recent developments in the market?

May 2023: Shell PLC, a major oil and gas company from the United Kingdom, and big-data analytics company SparkCognition announced their collaboration, stating that Shell will leverage artificial intelligence-based technology to enhance offshore oil exploration and production in deep-sea exploration and production.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oil and Gas Industry in UK," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oil and Gas Industry in UK report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oil and Gas Industry in UK?

To stay informed about further developments, trends, and reports in the Oil and Gas Industry in UK, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence