Key Insights

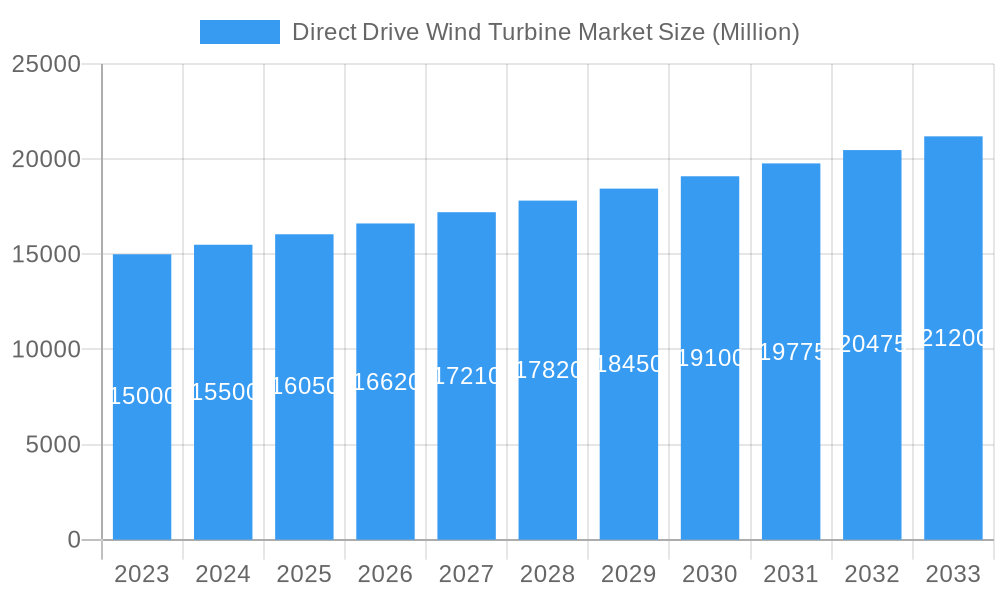

The Direct Drive Wind Turbine Market is projected for significant expansion, propelled by the escalating global demand for renewable energy and advancements in technology enhancing efficiency and reliability. The market is expected to reach a size of 36.8 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 11.8%. Direct drive systems, by eliminating gearboxes, offer inherent advantages including reduced wear and tear, lower failure rates, and quieter operation, making them increasingly favored by onshore and offshore wind farm developers. Key growth drivers include supportive government policies, growing environmental awareness, and the pursuit of energy independence.

Direct Drive Wind Turbine Market Market Size (In Billion)

The market segments effectively, with a notable focus on turbines ranging from 1 MW to 3 MW, ideal for diverse utility-scale projects. Emerging trends also indicate a rise in larger capacity turbines and innovative hybrid systems, further expanding market opportunities. The competitive landscape features established global players and emerging innovators focused on research and development and strategic collaborations. Leading companies such as Siemens Gamesa Renewable Energy SA, Goldwind Science & Technology Co Ltd, and ABB Ltd are at the forefront of offering advanced direct drive solutions. Challenges, including initial higher capital investment and grid integration complexities in remote areas, are being mitigated through technological progress and economies of scale. North America and Europe currently lead the market due to mature renewable infrastructure and stringent emission regulations, though the Asia Pacific region is anticipated to experience the fastest growth, driven by substantial wind power investments and supportive industrial policies. The direct drive wind turbine market will be instrumental in achieving global decarbonization targets.

Direct Drive Wind Turbine Market Company Market Share

This comprehensive report analyzes the dynamic Direct Drive Wind Turbine Market, providing in-depth insights into market dynamics, growth drivers, key trends, and leading players. With a study period from 2019 to 2033 and a base year of 2025, this report offers critical intelligence for industry stakeholders navigating the rapidly evolving renewable energy generation landscape. Key data points include market size projections of 36.8 billion by 2025 and a projected CAGR of 11.8%. Leveraging high-traffic keywords such as "direct drive wind turbines," "offshore wind power," "renewable energy market," and "wind turbine technology," this analysis ensures maximum visibility for essential industry participants. Explore market size forecasts, technological advancements, and strategic opportunities shaping the future of wind energy.

Direct Drive Wind Turbine Market Market Dynamics & Concentration

The Direct Drive Wind Turbine Market exhibits a moderate to high concentration, with a few key players holding significant market share. Innovation remains a primary driver, fueled by continuous research and development in drivetrain technology, enhanced aerodynamic efficiency, and advanced control systems. Regulatory frameworks globally are increasingly favorable towards renewable energy, driving adoption through incentives, mandates, and carbon reduction targets. Product substitutes, while present in the form of geared wind turbines, are increasingly being displaced by direct drive technology due to its inherent advantages in reliability and reduced maintenance. End-user trends highlight a growing preference for direct drive systems, particularly in offshore applications, owing to their robustness and lower operational costs. Mergers and acquisitions (M&A) activity, though sporadic, has played a role in consolidating market power and expanding geographical reach. For instance, an estimated XX M&A deals were recorded between 2019 and 2024, signaling strategic consolidations. Key market share holders are projected to maintain their dominance through technological leadership and strategic partnerships.

- Market Concentration: Moderate to High.

- Innovation Drivers: Drivetrain efficiency, blade aerodynamics, smart grid integration, predictive maintenance.

- Regulatory Frameworks: Government incentives, renewable portfolio standards, emissions trading schemes.

- Product Substitutes: Geared wind turbines.

- End-User Trends: Growing preference for direct drive in offshore and onshore applications, demand for higher capacity turbines.

- M&A Activities: Strategic consolidations, capacity expansion through acquisitions.

Direct Drive Wind Turbine Market Industry Trends & Analysis

The Direct Drive Wind Turbine Market is experiencing robust growth, propelled by an escalating global demand for clean and sustainable energy solutions. This upward trajectory is underpinned by significant market growth drivers, including supportive government policies aimed at decarbonization and energy independence, coupled with declining levelized cost of energy (LCOE) for wind power. Technological disruptions are at the forefront of this expansion, with advancements in permanent magnet synchronous generators (PMSGs) and superconducting technologies promising increased efficiency and reduced reliance on rare-earth materials. Consumer preferences are increasingly leaning towards renewable energy sources, driven by environmental consciousness and the desire for stable, long-term energy prices. Competitive dynamics within the market are characterized by intense innovation and strategic collaborations between turbine manufacturers, component suppliers, and energy developers. The market penetration of direct drive technology is steadily increasing, particularly in the offshore wind sector where its inherent reliability and reduced maintenance requirements offer substantial operational advantages. Projections indicate a Compound Annual Growth Rate (CAGR) of approximately XX% for the forecast period, driven by substantial investments in new wind farm developments. The market is witnessing a surge in demand for higher capacity turbines, with the "Greater than 3 MW" segment experiencing the most significant expansion. The total market value is estimated to reach over $XX Billion by 2033.

Leading Markets & Segments in Direct Drive Wind Turbine Market

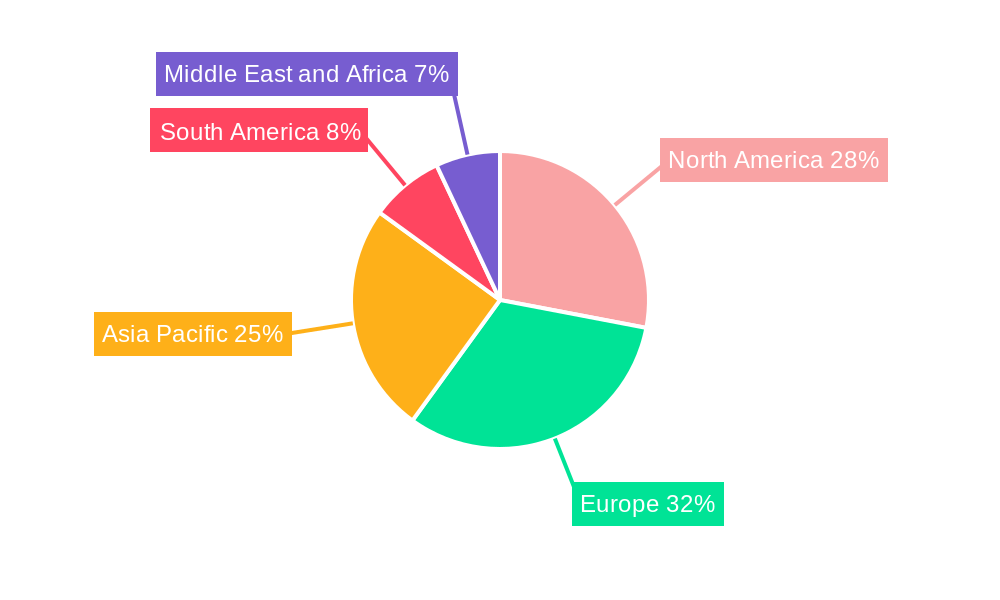

The Direct Drive Wind Turbine Market is witnessing significant regional dominance, with Europe and Asia-Pacific emerging as the leading markets. This leadership is attributed to strong government initiatives supporting renewable energy deployment, substantial investments in offshore wind infrastructure, and favorable economic policies. Within the Capacity segment, turbines Greater than 3 MW are experiencing the most rapid growth, driven by the economies of scale they offer and the increasing demand for higher energy output from wind farms. This dominance is further fueled by the technological advancements enabling the development of larger, more efficient direct drive turbines capable of operating in diverse wind conditions.

Dominant Regions:

- Europe: Driven by ambitious renewable energy targets, supportive regulatory frameworks, and significant offshore wind development, particularly in countries like Germany, the UK, and Denmark. The region benefits from established supply chains and a skilled workforce.

- Asia-Pacific: Experiencing rapid growth due to increasing energy demand, government investments in renewable energy, and declining manufacturing costs. China, in particular, is a major player in both manufacturing and installation of direct drive wind turbines.

Leading Capacity Segment:

- Greater than 3 MW: This segment dominates due to its ability to generate substantial amounts of electricity, leading to a lower LCOE and making wind energy more competitive with conventional power sources. Key drivers include:

- Technological Advancements: Development of larger, more efficient direct drive generators and robust turbine designs.

- Economies of Scale: Larger turbines require fewer installations for the same energy output, reducing installation and maintenance costs per megawatt.

- Offshore Wind Deployment: The offshore environment often favors larger turbines due to higher and more consistent wind speeds, and the higher capacity reduces the number of turbines needed, simplifying logistics and maintenance in challenging conditions.

- Government Support: Policies encouraging large-scale wind farm development and grid integration.

- Greater than 3 MW: This segment dominates due to its ability to generate substantial amounts of electricity, leading to a lower LCOE and making wind energy more competitive with conventional power sources. Key drivers include:

The 1 MW - 3 MW segment also maintains a significant market share, particularly for onshore applications and in regions with less consistent wind speeds or specific grid constraints. The Less than 1 MW segment, while smaller, continues to be relevant for distributed generation, remote communities, and smaller-scale industrial applications.

Direct Drive Wind Turbine Market Product Developments

Product development in the Direct Drive Wind Turbine Market is characterized by a relentless pursuit of enhanced efficiency, reliability, and cost-effectiveness. Innovations are focused on lightweight materials for nacelles and blades, advanced gearbox-less drivetrains utilizing superconducting magnets, and intelligent control systems for optimized power output. These developments provide competitive advantages by reducing maintenance needs, increasing energy capture in variable wind conditions, and lowering the overall cost of electricity generation. The market is witnessing the integration of advanced sensors and predictive maintenance algorithms, further boosting operational longevity and minimizing downtime.

Key Drivers of Direct Drive Wind Turbine Market Growth

The Direct Drive Wind Turbine Market is propelled by a confluence of powerful growth drivers. Technologically, the inherent advantages of direct drive systems—namely, fewer moving parts leading to increased reliability and reduced maintenance costs—are paramount. Economically, declining manufacturing costs, coupled with government incentives and subsidies promoting renewable energy adoption, make direct drive wind turbines increasingly attractive investments. Regulatory factors, such as stringent emission reduction targets and the growing global commitment to combating climate change, create a favorable policy environment for wind energy expansion. The escalating demand for clean electricity to meet growing energy needs further fuels market growth, with direct drive technology being a key enabler of large-scale wind power generation.

Challenges in the Direct Drive Wind Turbine Market Market

Despite its robust growth, the Direct Drive Wind Turbine Market faces several significant challenges. Regulatory hurdles can arise from complex permitting processes, grid connection delays, and inconsistent policy support in certain regions, impacting project timelines and investment certainty. Supply chain issues, particularly concerning the availability and cost of critical raw materials like rare earth elements for permanent magnets, can pose production constraints and price volatility. Furthermore, intense competitive pressures from both established geared turbine manufacturers and emerging direct drive players necessitate continuous innovation and cost optimization to maintain market share. Installation costs, especially for very large offshore turbines, remain a considerable factor, requiring ongoing advancements in logistics and installation techniques.

Emerging Opportunities in Direct Drive Wind Turbine Market

The Direct Drive Wind Turbine Market is ripe with emerging opportunities that will catalyze long-term growth. Technological breakthroughs in areas such as advanced materials for turbine components, improved generator designs, and enhanced grid integration solutions are poised to drive further efficiency gains. Strategic partnerships between turbine manufacturers, component suppliers, and energy developers are crucial for large-scale project development and market penetration. Market expansion into untapped geographical regions with favorable wind resources and supportive policy frameworks represents another significant opportunity. The growing trend towards hybrid renewable energy systems and the increasing demand for offshore wind power projects, particularly floating offshore wind, present substantial avenues for future growth and innovation in direct drive technology.

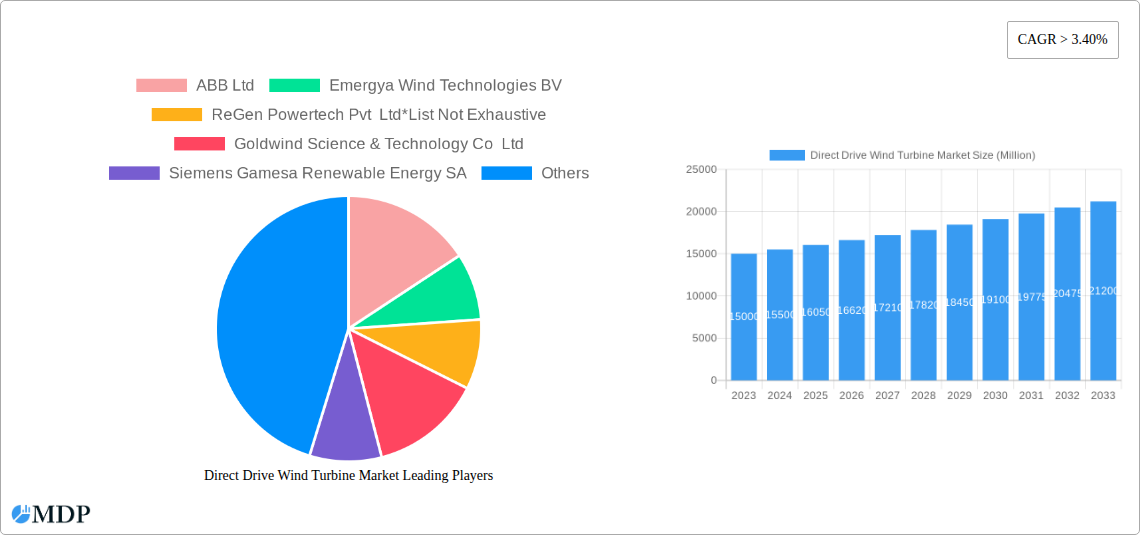

Leading Players in the Direct Drive Wind Turbine Market Sector

- ABB Ltd

- Emergya Wind Technologies BV

- ReGen Powertech Pvt Ltd

- Goldwind Science & Technology Co Ltd

- Siemens Gamesa Renewable Energy SA

- Avantis Energy Group

- Northern Power System

- Bachmann electronic GmbH

- Rockwell Automation Inc

- M Torres Olvega Industrial

- Enercon GmbH

Key Milestones in Direct Drive Wind Turbine Market Industry

- December 2021: Siemens Gamesa received an order from Orsted for a German offshore wind power project to supply 23 Siemens Gamesa 11.0-200 direct drive offshore wind turbines. The scope of the order includes a five-year service agreement. This order may enhance the company's presence in the German offshore wind industry.

- 2020: Vestas launched its V236-15.0 MW offshore wind turbine, featuring a direct drive system, marking a significant step in turbine capacity.

- 2019: GE Renewable Energy announced plans for its Haliade-X offshore wind turbine, a 12 MW direct drive model, underscoring the trend towards larger direct drive turbines.

- 2022: Goldwind achieved a significant milestone in its offshore wind development, securing multiple large-scale project orders, highlighting its growing market share.

- Ongoing: Continuous advancements in materials science and manufacturing processes by various players are enabling lighter, more efficient, and cost-effective direct drive components.

Strategic Outlook for Direct Drive Wind Turbine Market Market

The strategic outlook for the Direct Drive Wind Turbine Market is exceptionally promising, driven by several key growth accelerators. The ongoing global transition towards renewable energy, coupled with government mandates for carbon neutrality, will continue to fuel demand. Technological innovation in areas like advanced materials, digital twin technology for predictive maintenance, and enhanced grid integration solutions will further improve efficiency and reduce costs. Strategic partnerships and collaborations will be vital for scaling up manufacturing capacities and executing complex offshore wind projects. Furthermore, the expanding scope of offshore wind, including the development of floating offshore wind farms, presents a substantial opportunity for direct drive turbines to demonstrate their reliability and performance in challenging environments, solidifying their position as a cornerstone of future clean energy infrastructure.

Direct Drive Wind Turbine Market Segmentation

-

1. Capacity

- 1.1. Less than 1 MW

- 1.2. 1 MW - 3 MW

- 1.3. Greater than 3 MW

Direct Drive Wind Turbine Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. South America

- 5. Middle East and Africa

Direct Drive Wind Turbine Market Regional Market Share

Geographic Coverage of Direct Drive Wind Turbine Market

Direct Drive Wind Turbine Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Less than 1 MW

- 5.1.2. 1 MW - 3 MW

- 5.1.3. Greater than 3 MW

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. Global Direct Drive Wind Turbine Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. Less than 1 MW

- 6.1.2. 1 MW - 3 MW

- 6.1.3. Greater than 3 MW

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. North America Direct Drive Wind Turbine Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. Less than 1 MW

- 7.1.2. 1 MW - 3 MW

- 7.1.3. Greater than 3 MW

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Europe Direct Drive Wind Turbine Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. Less than 1 MW

- 8.1.2. 1 MW - 3 MW

- 8.1.3. Greater than 3 MW

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. Asia Pacific Direct Drive Wind Turbine Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. Less than 1 MW

- 9.1.2. 1 MW - 3 MW

- 9.1.3. Greater than 3 MW

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. South America Direct Drive Wind Turbine Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 10.1.1. Less than 1 MW

- 10.1.2. 1 MW - 3 MW

- 10.1.3. Greater than 3 MW

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 11. Middle East and Africa Direct Drive Wind Turbine Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Capacity

- 11.1.1. Less than 1 MW

- 11.1.2. 1 MW - 3 MW

- 11.1.3. Greater than 3 MW

- 11.1. Market Analysis, Insights and Forecast - by Capacity

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ABB Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Emergya Wind Technologies BV

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ReGen Powertech Pvt Ltd*List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Goldwind Science & Technology Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Siemens Gamesa Renewable Energy SA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Avantis Energy Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Northern Power System

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Bachmann electronic GmbH

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Rockwell Automation Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 M Torres Olvega Industrial

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Enercon GmbH

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 ABB Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Direct Drive Wind Turbine Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Direct Drive Wind Turbine Market Revenue (billion), by Capacity 2025 & 2033

- Figure 3: North America Direct Drive Wind Turbine Market Revenue Share (%), by Capacity 2025 & 2033

- Figure 4: North America Direct Drive Wind Turbine Market Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Direct Drive Wind Turbine Market Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Direct Drive Wind Turbine Market Revenue (billion), by Capacity 2025 & 2033

- Figure 7: Europe Direct Drive Wind Turbine Market Revenue Share (%), by Capacity 2025 & 2033

- Figure 8: Europe Direct Drive Wind Turbine Market Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Direct Drive Wind Turbine Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Direct Drive Wind Turbine Market Revenue (billion), by Capacity 2025 & 2033

- Figure 11: Asia Pacific Direct Drive Wind Turbine Market Revenue Share (%), by Capacity 2025 & 2033

- Figure 12: Asia Pacific Direct Drive Wind Turbine Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Direct Drive Wind Turbine Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Direct Drive Wind Turbine Market Revenue (billion), by Capacity 2025 & 2033

- Figure 15: South America Direct Drive Wind Turbine Market Revenue Share (%), by Capacity 2025 & 2033

- Figure 16: South America Direct Drive Wind Turbine Market Revenue (billion), by Country 2025 & 2033

- Figure 17: South America Direct Drive Wind Turbine Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Direct Drive Wind Turbine Market Revenue (billion), by Capacity 2025 & 2033

- Figure 19: Middle East and Africa Direct Drive Wind Turbine Market Revenue Share (%), by Capacity 2025 & 2033

- Figure 20: Middle East and Africa Direct Drive Wind Turbine Market Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East and Africa Direct Drive Wind Turbine Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 2: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 4: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 6: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 8: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 10: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 12: Global Direct Drive Wind Turbine Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Direct Drive Wind Turbine Market?

The projected CAGR is approximately 11.8%.

2. Which companies are prominent players in the Direct Drive Wind Turbine Market?

Key companies in the market include ABB Ltd, Emergya Wind Technologies BV, ReGen Powertech Pvt Ltd*List Not Exhaustive, Goldwind Science & Technology Co Ltd, Siemens Gamesa Renewable Energy SA, Avantis Energy Group, Northern Power System, Bachmann electronic GmbH, Rockwell Automation Inc, M Torres Olvega Industrial, Enercon GmbH.

3. What are the main segments of the Direct Drive Wind Turbine Market?

The market segments include Capacity.

4. Can you provide details about the market size?

The market size is estimated to be USD 36.8 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Substantial Investments and Efforts to Modernize the T&D Grid.

6. What are the notable trends driving market growth?

Offshore Segment to Witness Growth for Turbine Capacity of 1 MW – 3 MW.

7. Are there any restraints impacting market growth?

4.; Expansion of High Voltage Direct Current (HVDC) Networks.

8. Can you provide examples of recent developments in the market?

In December 2021, Siemens Gamesa received an order from Orsted for a German offshore wind power project to supply 23 Siemens Gamesa 11.0-200 direct drive offshore wind turbines. The scope of the order includes a five-year service agreement. This order may enhance the company's presence in the German offshore wind industry.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Direct Drive Wind Turbine Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Direct Drive Wind Turbine Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Direct Drive Wind Turbine Market?

To stay informed about further developments, trends, and reports in the Direct Drive Wind Turbine Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence