Key Insights

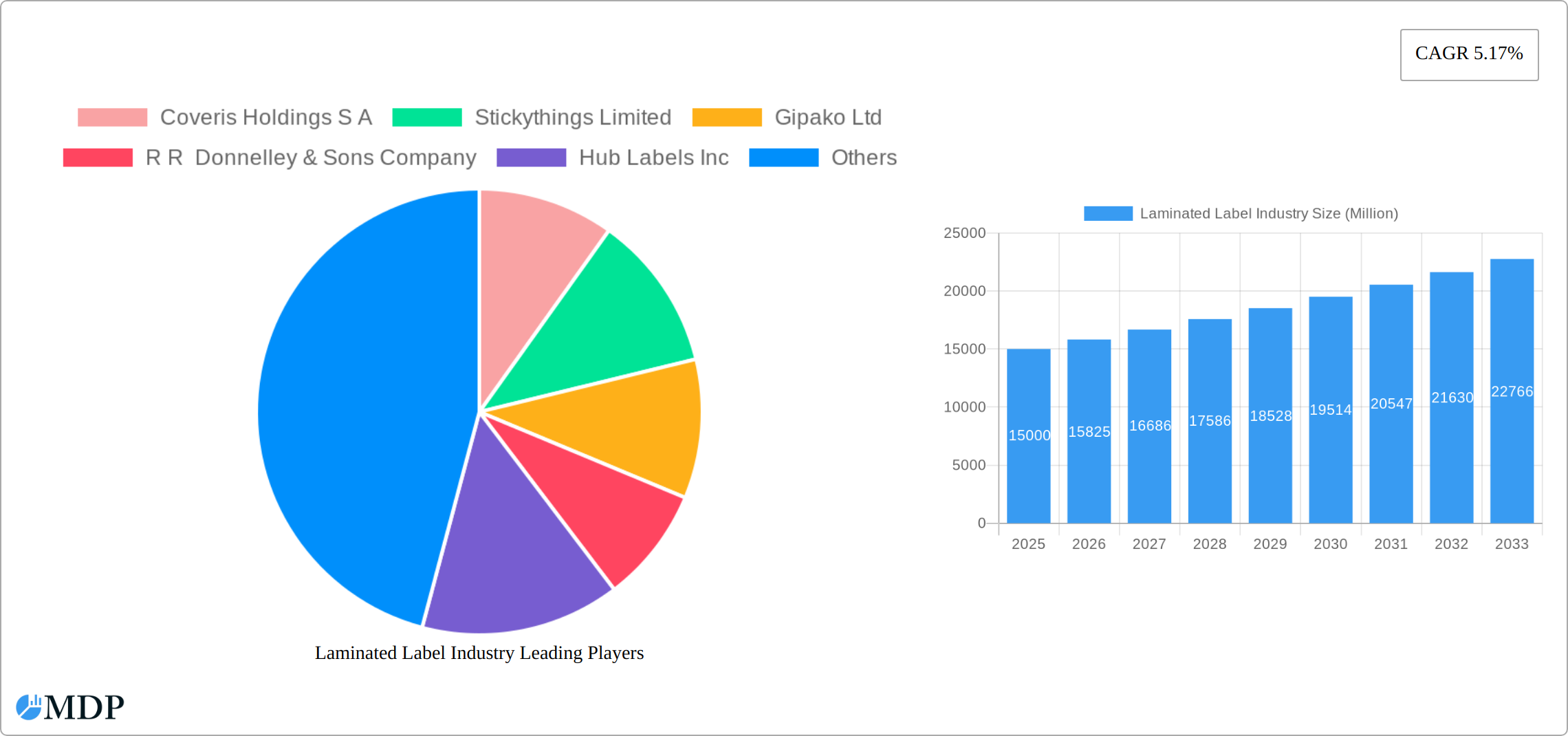

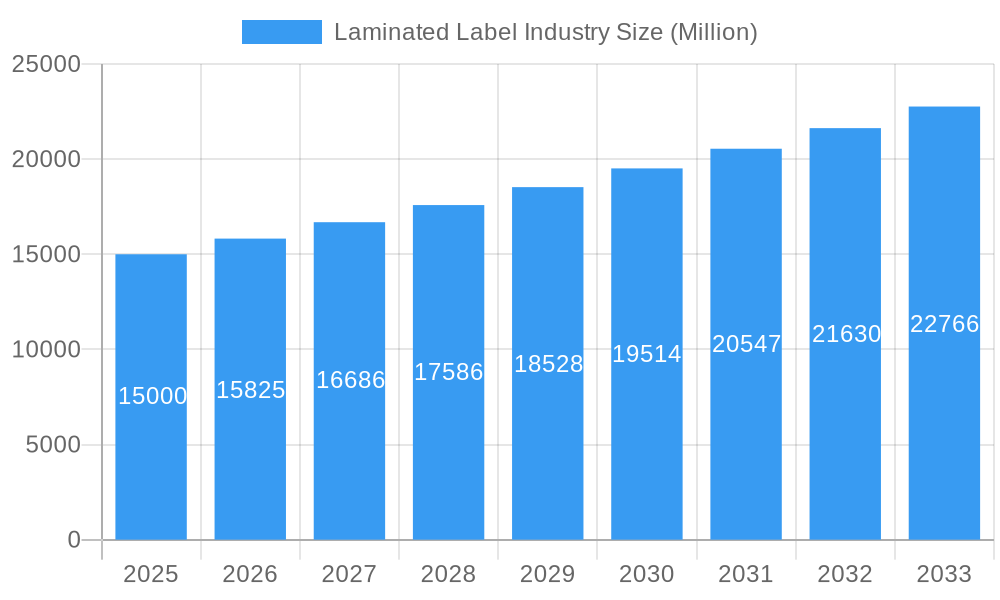

The laminated label market, valued at approximately $XX million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 5.17% from 2025 to 2033. This expansion is fueled by several key drivers. The burgeoning e-commerce sector necessitates high-quality, durable labels for efficient product identification and tracking. Simultaneously, the increasing demand for sophisticated and aesthetically pleasing labels across diverse sectors like FMCG, pharmaceuticals, and electronics is driving innovation and market growth. Furthermore, the ongoing trend toward sustainable and eco-friendly labeling materials is shaping product development and influencing consumer choices. While challenges such as fluctuating raw material prices and stringent regulatory compliance pose some restraints, the overall market outlook remains positive. Segmentation analysis reveals that the adhesive component holds a significant share, driven by the need for secure adhesion across various substrates. Among applications, FMCG and retail labels dominate, reflecting the high volume of packaged goods consumed globally. Polyester and polypropylene materials are widely used due to their durability and printability, while roll format remains prevalent for high-speed labeling processes. Major players like Avery Dennison, 3M, and CCL Industries are strategically investing in R&D and expanding their global reach to capitalize on the growing opportunities presented by this dynamic market.

Laminated Label Industry Market Size (In Billion)

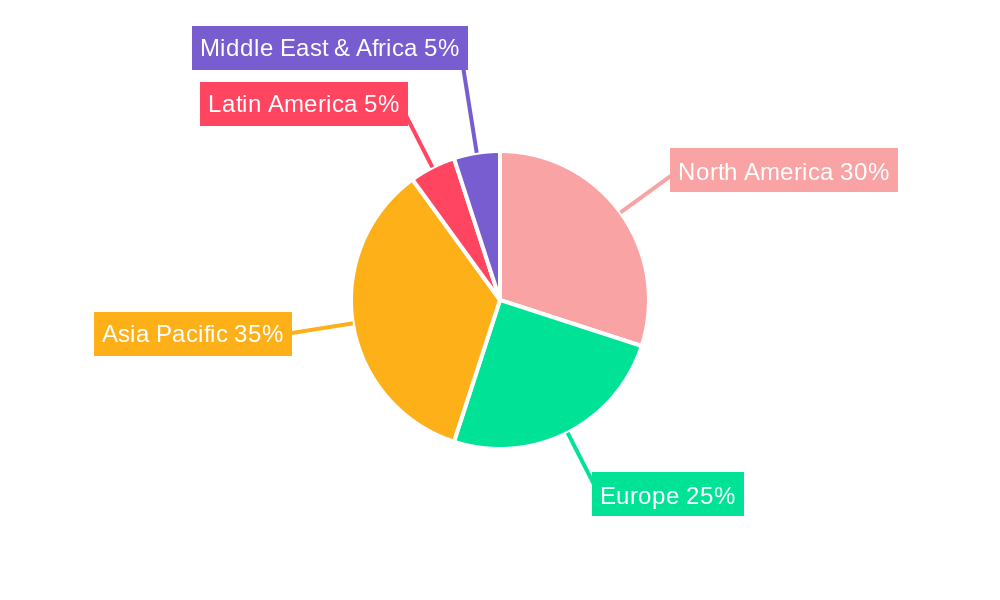

The geographical distribution of the market reveals strong growth potential in Asia Pacific, particularly in rapidly developing economies like China and India, driven by increasing industrialization and consumer spending. North America and Europe, while mature markets, continue to contribute significantly due to established manufacturing sectors and high consumer demand for branded products. The competitive landscape is characterized by both established multinational corporations and specialized regional players. Competition is fierce, prompting ongoing innovation in label materials, printing technologies, and application methods to enhance product differentiation and meet evolving customer needs. Future growth will likely be driven by the adoption of smart labels with embedded technologies and the increased use of sustainable materials to meet environmental regulations and consumer preferences. The market's trajectory suggests sustained growth, albeit with a need for companies to adapt to changing market dynamics and consumer expectations.

Laminated Label Industry Company Market Share

Laminated Label Industry: Market Report 2019-2033

Unlocking Growth Potential in the Multi-Billion Dollar Laminated Label Market: A Comprehensive Analysis

This comprehensive report provides an in-depth analysis of the global laminated label industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is essential for strategic decision-making. The market is segmented by composition (adhesive, facestock, release liner), application (FMCG, manufacturing, fashion and apparel, electronics and appliance, pharmaceuticals, retail labels, other applications), material type (polyester, polypropylene, vinyl, other material types), and form (rolls, sheets). The report features a detailed analysis of key players, including Coveris Holdings S.A., Stickythings Limited, Gipako Ltd, R.R. Donnelley & Sons Company, Hub Labels Inc, Constantia Flexibles Group GmbH, Ravenwood Packaging Ltd, Cenveo Corporation, 3M Company, CCL Industries Inc, Torraspapel Adestor, Avery Dennison Corporation, Flexcon Company Inc, and Reflex Labels Ltd. The total market value is predicted to reach xx Million by 2033.

Laminated Label Industry Market Dynamics & Concentration

The global laminated label market is characterized by a moderately consolidated structure, with a select group of leading companies dominating a significant portion of the market share. The collective market share of the top five players is estimated to be around **xx%**, indicating a competitive yet concentrated landscape. Innovation is a pivotal force, continuously propelling the development of advanced materials, superior adhesives, and cutting-edge printing technologies that enhance label functionality and aesthetic appeal. Stringent regulatory frameworks, particularly concerning material safety and environmental sustainability, exert a considerable influence on industry practices, pushing manufacturers towards more responsible production methods. While product substitutes like direct digital printing and alternative packaging solutions present a moderate competitive threat, the demand for high-quality laminated labels remains robust. A significant trend shaping demand is the end-user preference for sustainable, eco-friendly, and highly customizable labeling solutions that cater to specific brand identities and consumer expectations. Mergers and acquisitions (M&A) activity has been moderately active in recent years, with an estimated **xx M&A deals** successfully concluded between 2019 and 2024, signifying strategic consolidations and market expansion efforts.

- Market Concentration: The top 5 players collectively command approximately **xx%** of the market share, highlighting a concentrated market structure.

- Innovation Drivers: Key drivers of innovation include advancements in adhesive technology for enhanced performance, sophisticated printing techniques for vibrant graphics, and the development of sustainable and recyclable materials.

- Regulatory Frameworks: The industry is heavily influenced by compliance with evolving environmental regulations and stringent food safety standards, particularly for labels used in the food and beverage sector.

- Product Substitutes: Potential competitive threats arise from direct digital printing, alternative packaging solutions, and other specialized label types that may offer specific advantages.

- End-User Trends: There is a discernible and growing preference among end-users for labels that are not only visually appealing and informative but also environmentally sustainable, customizable to brand needs, and possess high-performance characteristics.

- M&A Activity: The market has witnessed a moderate level of M&A activity, with an estimated **xx M&A deals** completed between 2019 and 2024, indicating strategic consolidation and growth.

Laminated Label Industry Industry Trends & Analysis

The laminated label market is currently experiencing a phase of robust and consistent growth. This expansion is primarily fueled by the escalating demand for packaged goods across a diverse array of sectors, including food and beverage, pharmaceuticals, personal care, and industrial products. The increasing adoption of advanced printing technologies, with a particular emphasis on the transformative impact of digital printing, is reshaping the manufacturing landscape, enabling greater flexibility, shorter runs, and enhanced personalization. Consumer preferences for visually appealing, informative, and durable labels are significantly influencing product development strategies, pushing manufacturers to create labels that not only protect and identify products but also enhance brand perception. The intense competition among market participants is fostering a dynamic environment characterized by price pressures and a relentless pursuit of innovation. The Compound Annual Growth Rate (CAGR) for the forecast period spanning 2025-2033 is projected to be **xx%**, signifying substantial market expansion. Furthermore, market penetration is expected to witness a significant surge in emerging economies as their consumer bases and manufacturing capacities grow.

Leading Markets & Segments in Laminated Label Industry

The FMCG sector is the largest application segment, accounting for xx% of the market in 2025. Geographically, North America and Europe hold significant market share, driven by strong consumer demand and established packaging industries. Polyester is the dominant material type, owing to its durability and versatility. Rolls remain the preferred form of laminated labels.

- Key Drivers by Segment:

- FMCG: High volume consumption, diverse product range driving demand.

- Manufacturing: Increasing industrial automation and product identification needs.

- Polyester: Superior strength, printability, and chemical resistance.

- Rolls: Efficiency in high-speed label application.

- Regional Dominance: North America and Europe represent the largest markets.

- North America: High per capita consumption, strong manufacturing base, and established retail infrastructure.

- Europe: Large FMCG sector, sophisticated consumer base, and robust regulatory environment.

Laminated Label Industry Product Developments

Recent innovations include the development of sustainable materials, such as bio-based polymers and recycled content, responding to growing environmental concerns. Advances in digital printing technologies are enabling greater customization and reduced lead times. Products offering enhanced durability, tamper evidence, and improved adhesion are gaining traction.

Key Drivers of Laminated Label Industry Growth

The upward trajectory of the laminated label market is propelled by a confluence of influential factors. Foremost among these is the escalating demand stemming from the rapidly expanding Fast-Moving Consumer Goods (FMCG) and pharmaceutical sectors, which rely heavily on effective and durable labeling. The increasing consumer preference for branded, high-quality products further fuels this demand, as labels play a crucial role in product differentiation and brand storytelling. Concurrently, ongoing technological advancements are continuously enhancing label features, such as improved durability, specialized finishes, and advanced printing capabilities, leading to more sophisticated and functional labels. Additionally, government regulations that promote sustainable packaging initiatives are acting as a significant catalyst, encouraging the adoption of eco-friendly labeling solutions.

Challenges in the Laminated Label Industry Market

Despite its growth, the laminated label market navigates several significant challenges that can impact its trajectory. Fluctuations in the prices of raw materials, including films, adhesives, and inks, directly affect production costs and, consequently, profitability, creating an environment of cost volatility. Supply chain disruptions, which have become increasingly prevalent in recent years, can lead to material shortages and delivery delays, impacting operational efficiency. The intensifying competition, both from established industry leaders and agile new entrants, puts pressure on pricing and necessitates continuous investment in innovation. Furthermore, the evolving landscape of environmental regulations requires manufacturers to invest in sustainable practices and materials, adding to operational complexity and potential upfront costs. These multifaceted challenges collectively have an estimated impact of **xx%** on the overall market growth.

Emerging Opportunities in Laminated Label Industry

The laminated label industry is ripe with emerging opportunities that promise significant growth and innovation. The burgeoning adoption of "smart labels," which integrate technologies like Radio-Frequency Identification (RFID) and Near-Field Communication (NFC), presents a vast potential for enhanced supply chain management, inventory tracking, and consumer engagement. Strategic partnerships with leading technology providers can further unlock this potential, facilitating the development and implementation of groundbreaking solutions. Moreover, the expansion into emerging markets, characterized by burgeoning FMCG and manufacturing sectors, offers substantial untapped potential for market penetration and revenue generation, as these regions increasingly demand sophisticated labeling solutions to support their growing economies.

Leading Players in the Laminated Label Industry Sector

- Coveris Holdings S.A. [Link to website if available]

- Stickythings Limited [Link to website if available]

- Gipako Ltd [Link to website if available]

- R R Donnelley & Sons Company [Link to website if available]

- Hub Labels Inc [Link to website if available]

- Constantia Flexibles Group GmbH [Link to website if available]

- Ravenwood Packaging Ltd [Link to website if available]

- Cenveo Corporation [Link to website if available]

- 3M Company [Link to website if available]

- CCL Industries Inc [Link to website if available]

- Torraspapel Adestor [Link to website if available]

- Avery Dennison Corporation [Link to website if available]

- Flexcon Company Inc [Link to website if available]

- Reflex Labels Ltd [Link to website if available]

- List Not Exhaustive

Key Milestones in Laminated Label Industry Industry

- 2020: Increased focus on sustainable label materials and production methods.

- 2021: Several key players invested in digital printing technologies to improve efficiency and customization.

- 2022: Launch of innovative tamper-evident labels for enhanced product security.

- 2023: A significant M&A deal reshaped the competitive landscape. (Specific details of the deal would go here if available).

- 2024: Several new product launches focused on high-performance adhesives.

Strategic Outlook for Laminated Label Industry Market

The laminated label market is poised for continued growth, driven by technological innovations, rising consumer demand for high-quality products and sustainable packaging solutions. Strategic partnerships and expansion into new markets will play a critical role in capturing future opportunities. Market expansion in developing economies remains a key area of growth.

Laminated Label Industry Segmentation

-

1. Material Type

- 1.1. Polyester

- 1.2. Polypropylene

- 1.3. Vinyl

- 1.4. Other Material Types

-

2. Form

- 2.1. Rolls

- 2.2. Sheets

-

3. Composition

- 3.1. Adhesive

- 3.2. Facestock

- 3.3. Release Liner

-

4. Application

- 4.1. FMCG

- 4.2. Manufacturing

- 4.3. Fashion and Apparel

- 4.4. Electronics and Appliance

- 4.5. Pharmaceuticals

- 4.6. Retail Labels

- 4.7. Other Applications

Laminated Label Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. France

- 2.3. United Kingdom

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Rest of Latin America

- 5. Middle East

-

6. South Africa

- 6.1. Rest of Middle East

Laminated Label Industry Regional Market Share

Geographic Coverage of Laminated Label Industry

Laminated Label Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Polyester

- 5.1.2. Polypropylene

- 5.1.3. Vinyl

- 5.1.4. Other Material Types

- 5.2. Market Analysis, Insights and Forecast - by Form

- 5.2.1. Rolls

- 5.2.2. Sheets

- 5.3. Market Analysis, Insights and Forecast - by Composition

- 5.3.1. Adhesive

- 5.3.2. Facestock

- 5.3.3. Release Liner

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. FMCG

- 5.4.2. Manufacturing

- 5.4.3. Fashion and Apparel

- 5.4.4. Electronics and Appliance

- 5.4.5. Pharmaceuticals

- 5.4.6. Retail Labels

- 5.4.7. Other Applications

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East

- 5.5.6. South Africa

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Laminated Label Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Polyester

- 6.1.2. Polypropylene

- 6.1.3. Vinyl

- 6.1.4. Other Material Types

- 6.2. Market Analysis, Insights and Forecast - by Form

- 6.2.1. Rolls

- 6.2.2. Sheets

- 6.3. Market Analysis, Insights and Forecast - by Composition

- 6.3.1. Adhesive

- 6.3.2. Facestock

- 6.3.3. Release Liner

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. FMCG

- 6.4.2. Manufacturing

- 6.4.3. Fashion and Apparel

- 6.4.4. Electronics and Appliance

- 6.4.5. Pharmaceuticals

- 6.4.6. Retail Labels

- 6.4.7. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America Laminated Label Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Polyester

- 7.1.2. Polypropylene

- 7.1.3. Vinyl

- 7.1.4. Other Material Types

- 7.2. Market Analysis, Insights and Forecast - by Form

- 7.2.1. Rolls

- 7.2.2. Sheets

- 7.3. Market Analysis, Insights and Forecast - by Composition

- 7.3.1. Adhesive

- 7.3.2. Facestock

- 7.3.3. Release Liner

- 7.4. Market Analysis, Insights and Forecast - by Application

- 7.4.1. FMCG

- 7.4.2. Manufacturing

- 7.4.3. Fashion and Apparel

- 7.4.4. Electronics and Appliance

- 7.4.5. Pharmaceuticals

- 7.4.6. Retail Labels

- 7.4.7. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Europe Laminated Label Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Polyester

- 8.1.2. Polypropylene

- 8.1.3. Vinyl

- 8.1.4. Other Material Types

- 8.2. Market Analysis, Insights and Forecast - by Form

- 8.2.1. Rolls

- 8.2.2. Sheets

- 8.3. Market Analysis, Insights and Forecast - by Composition

- 8.3.1. Adhesive

- 8.3.2. Facestock

- 8.3.3. Release Liner

- 8.4. Market Analysis, Insights and Forecast - by Application

- 8.4.1. FMCG

- 8.4.2. Manufacturing

- 8.4.3. Fashion and Apparel

- 8.4.4. Electronics and Appliance

- 8.4.5. Pharmaceuticals

- 8.4.6. Retail Labels

- 8.4.7. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Asia Pacific Laminated Label Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Polyester

- 9.1.2. Polypropylene

- 9.1.3. Vinyl

- 9.1.4. Other Material Types

- 9.2. Market Analysis, Insights and Forecast - by Form

- 9.2.1. Rolls

- 9.2.2. Sheets

- 9.3. Market Analysis, Insights and Forecast - by Composition

- 9.3.1. Adhesive

- 9.3.2. Facestock

- 9.3.3. Release Liner

- 9.4. Market Analysis, Insights and Forecast - by Application

- 9.4.1. FMCG

- 9.4.2. Manufacturing

- 9.4.3. Fashion and Apparel

- 9.4.4. Electronics and Appliance

- 9.4.5. Pharmaceuticals

- 9.4.6. Retail Labels

- 9.4.7. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Latin America Laminated Label Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Polyester

- 10.1.2. Polypropylene

- 10.1.3. Vinyl

- 10.1.4. Other Material Types

- 10.2. Market Analysis, Insights and Forecast - by Form

- 10.2.1. Rolls

- 10.2.2. Sheets

- 10.3. Market Analysis, Insights and Forecast - by Composition

- 10.3.1. Adhesive

- 10.3.2. Facestock

- 10.3.3. Release Liner

- 10.4. Market Analysis, Insights and Forecast - by Application

- 10.4.1. FMCG

- 10.4.2. Manufacturing

- 10.4.3. Fashion and Apparel

- 10.4.4. Electronics and Appliance

- 10.4.5. Pharmaceuticals

- 10.4.6. Retail Labels

- 10.4.7. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Middle East Laminated Label Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. Polyester

- 11.1.2. Polypropylene

- 11.1.3. Vinyl

- 11.1.4. Other Material Types

- 11.2. Market Analysis, Insights and Forecast - by Form

- 11.2.1. Rolls

- 11.2.2. Sheets

- 11.3. Market Analysis, Insights and Forecast - by Composition

- 11.3.1. Adhesive

- 11.3.2. Facestock

- 11.3.3. Release Liner

- 11.4. Market Analysis, Insights and Forecast - by Application

- 11.4.1. FMCG

- 11.4.2. Manufacturing

- 11.4.3. Fashion and Apparel

- 11.4.4. Electronics and Appliance

- 11.4.5. Pharmaceuticals

- 11.4.6. Retail Labels

- 11.4.7. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. South Africa Laminated Label Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Material Type

- 12.1.1. Polyester

- 12.1.2. Polypropylene

- 12.1.3. Vinyl

- 12.1.4. Other Material Types

- 12.2. Market Analysis, Insights and Forecast - by Form

- 12.2.1. Rolls

- 12.2.2. Sheets

- 12.3. Market Analysis, Insights and Forecast - by Composition

- 12.3.1. Adhesive

- 12.3.2. Facestock

- 12.3.3. Release Liner

- 12.4. Market Analysis, Insights and Forecast - by Application

- 12.4.1. FMCG

- 12.4.2. Manufacturing

- 12.4.3. Fashion and Apparel

- 12.4.4. Electronics and Appliance

- 12.4.5. Pharmaceuticals

- 12.4.6. Retail Labels

- 12.4.7. Other Applications

- 12.1. Market Analysis, Insights and Forecast - by Material Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Coveris Holdings S A

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Stickythings Limited

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Gipako Ltd

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 R R Donnelley & Sons Company

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Hub Labels Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Constantia Flexibles Group GmbH

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Ravenwood Packaging Ltd

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Cenveo Corporation

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 3M Company

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 CCL Industries Inc

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Torraspapel Adestor

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Avery Dennison Corporation

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Flexcon Company Inc

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Reflex Labels Ltd *List Not Exhaustive

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.1 Coveris Holdings S A

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Laminated Label Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Laminated Label Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 3: North America Laminated Label Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America Laminated Label Industry Revenue (Million), by Form 2025 & 2033

- Figure 5: North America Laminated Label Industry Revenue Share (%), by Form 2025 & 2033

- Figure 6: North America Laminated Label Industry Revenue (Million), by Composition 2025 & 2033

- Figure 7: North America Laminated Label Industry Revenue Share (%), by Composition 2025 & 2033

- Figure 8: North America Laminated Label Industry Revenue (Million), by Application 2025 & 2033

- Figure 9: North America Laminated Label Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Laminated Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Laminated Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Laminated Label Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 13: Europe Laminated Label Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 14: Europe Laminated Label Industry Revenue (Million), by Form 2025 & 2033

- Figure 15: Europe Laminated Label Industry Revenue Share (%), by Form 2025 & 2033

- Figure 16: Europe Laminated Label Industry Revenue (Million), by Composition 2025 & 2033

- Figure 17: Europe Laminated Label Industry Revenue Share (%), by Composition 2025 & 2033

- Figure 18: Europe Laminated Label Industry Revenue (Million), by Application 2025 & 2033

- Figure 19: Europe Laminated Label Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Europe Laminated Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Laminated Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Laminated Label Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 23: Asia Pacific Laminated Label Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 24: Asia Pacific Laminated Label Industry Revenue (Million), by Form 2025 & 2033

- Figure 25: Asia Pacific Laminated Label Industry Revenue Share (%), by Form 2025 & 2033

- Figure 26: Asia Pacific Laminated Label Industry Revenue (Million), by Composition 2025 & 2033

- Figure 27: Asia Pacific Laminated Label Industry Revenue Share (%), by Composition 2025 & 2033

- Figure 28: Asia Pacific Laminated Label Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Asia Pacific Laminated Label Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Laminated Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Laminated Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Laminated Label Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 33: Latin America Laminated Label Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 34: Latin America Laminated Label Industry Revenue (Million), by Form 2025 & 2033

- Figure 35: Latin America Laminated Label Industry Revenue Share (%), by Form 2025 & 2033

- Figure 36: Latin America Laminated Label Industry Revenue (Million), by Composition 2025 & 2033

- Figure 37: Latin America Laminated Label Industry Revenue Share (%), by Composition 2025 & 2033

- Figure 38: Latin America Laminated Label Industry Revenue (Million), by Application 2025 & 2033

- Figure 39: Latin America Laminated Label Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Latin America Laminated Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Laminated Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East Laminated Label Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 43: Middle East Laminated Label Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 44: Middle East Laminated Label Industry Revenue (Million), by Form 2025 & 2033

- Figure 45: Middle East Laminated Label Industry Revenue Share (%), by Form 2025 & 2033

- Figure 46: Middle East Laminated Label Industry Revenue (Million), by Composition 2025 & 2033

- Figure 47: Middle East Laminated Label Industry Revenue Share (%), by Composition 2025 & 2033

- Figure 48: Middle East Laminated Label Industry Revenue (Million), by Application 2025 & 2033

- Figure 49: Middle East Laminated Label Industry Revenue Share (%), by Application 2025 & 2033

- Figure 50: Middle East Laminated Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East Laminated Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 52: South Africa Laminated Label Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 53: South Africa Laminated Label Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 54: South Africa Laminated Label Industry Revenue (Million), by Form 2025 & 2033

- Figure 55: South Africa Laminated Label Industry Revenue Share (%), by Form 2025 & 2033

- Figure 56: South Africa Laminated Label Industry Revenue (Million), by Composition 2025 & 2033

- Figure 57: South Africa Laminated Label Industry Revenue Share (%), by Composition 2025 & 2033

- Figure 58: South Africa Laminated Label Industry Revenue (Million), by Application 2025 & 2033

- Figure 59: South Africa Laminated Label Industry Revenue Share (%), by Application 2025 & 2033

- Figure 60: South Africa Laminated Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 61: South Africa Laminated Label Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Laminated Label Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Global Laminated Label Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 3: Global Laminated Label Industry Revenue Million Forecast, by Composition 2020 & 2033

- Table 4: Global Laminated Label Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 5: Global Laminated Label Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Laminated Label Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 7: Global Laminated Label Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 8: Global Laminated Label Industry Revenue Million Forecast, by Composition 2020 & 2033

- Table 9: Global Laminated Label Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Global Laminated Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United States Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Canada Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Laminated Label Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 14: Global Laminated Label Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 15: Global Laminated Label Industry Revenue Million Forecast, by Composition 2020 & 2033

- Table 16: Global Laminated Label Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 17: Global Laminated Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Germany Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: France Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: United Kingdom Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Laminated Label Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 23: Global Laminated Label Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 24: Global Laminated Label Industry Revenue Million Forecast, by Composition 2020 & 2033

- Table 25: Global Laminated Label Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 26: Global Laminated Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 27: China Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Japan Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: India Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Asia Pacific Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Laminated Label Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 32: Global Laminated Label Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 33: Global Laminated Label Industry Revenue Million Forecast, by Composition 2020 & 2033

- Table 34: Global Laminated Label Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 35: Global Laminated Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Brazil Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Rest of Latin America Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Global Laminated Label Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 39: Global Laminated Label Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 40: Global Laminated Label Industry Revenue Million Forecast, by Composition 2020 & 2033

- Table 41: Global Laminated Label Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 42: Global Laminated Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 43: Global Laminated Label Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 44: Global Laminated Label Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 45: Global Laminated Label Industry Revenue Million Forecast, by Composition 2020 & 2033

- Table 46: Global Laminated Label Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 47: Global Laminated Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Rest of Middle East Laminated Label Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Laminated Label Industry?

The projected CAGR is approximately 5.17%.

2. Which companies are prominent players in the Laminated Label Industry?

Key companies in the market include Coveris Holdings S A, Stickythings Limited, Gipako Ltd, R R Donnelley & Sons Company, Hub Labels Inc, Constantia Flexibles Group GmbH, Ravenwood Packaging Ltd, Cenveo Corporation, 3M Company, CCL Industries Inc, Torraspapel Adestor, Avery Dennison Corporation, Flexcon Company Inc, Reflex Labels Ltd *List Not Exhaustive.

3. What are the main segments of the Laminated Label Industry?

The market segments include Material Type, Form, Composition, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Augmented Demand for Packaged Foods & Beverages; Increasing Consumer Awareness About Information of the Product.

6. What are the notable trends driving market growth?

Laminated Labels are being Widely Adopted by the FMCG Industry.

7. Are there any restraints impacting market growth?

; Rising Use of Metallized Foils; Increase in Prices of Raw Material and Diminished Profit.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Laminated Label Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Laminated Label Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Laminated Label Industry?

To stay informed about further developments, trends, and reports in the Laminated Label Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence