Key Insights

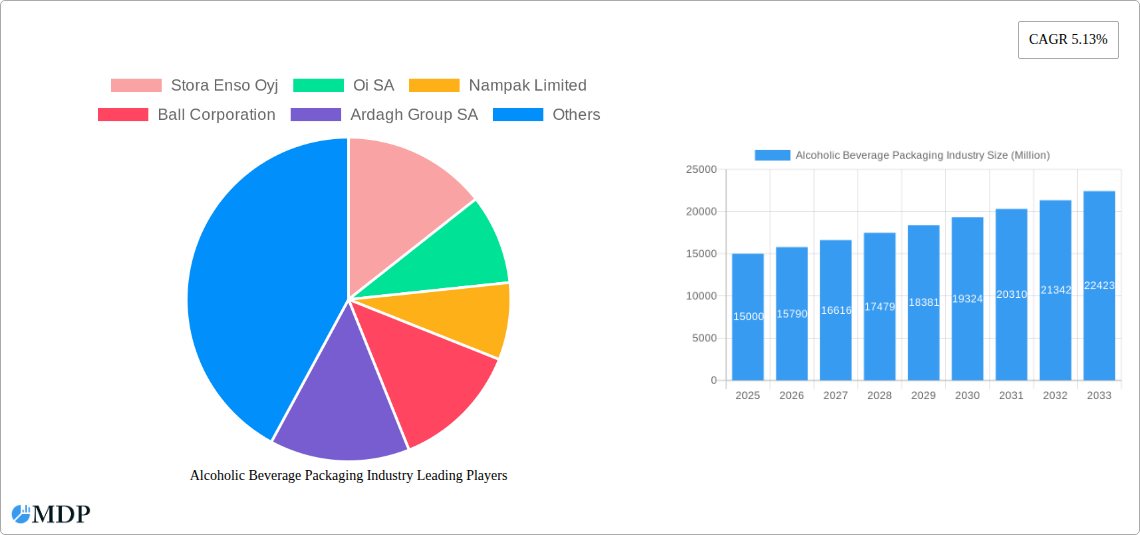

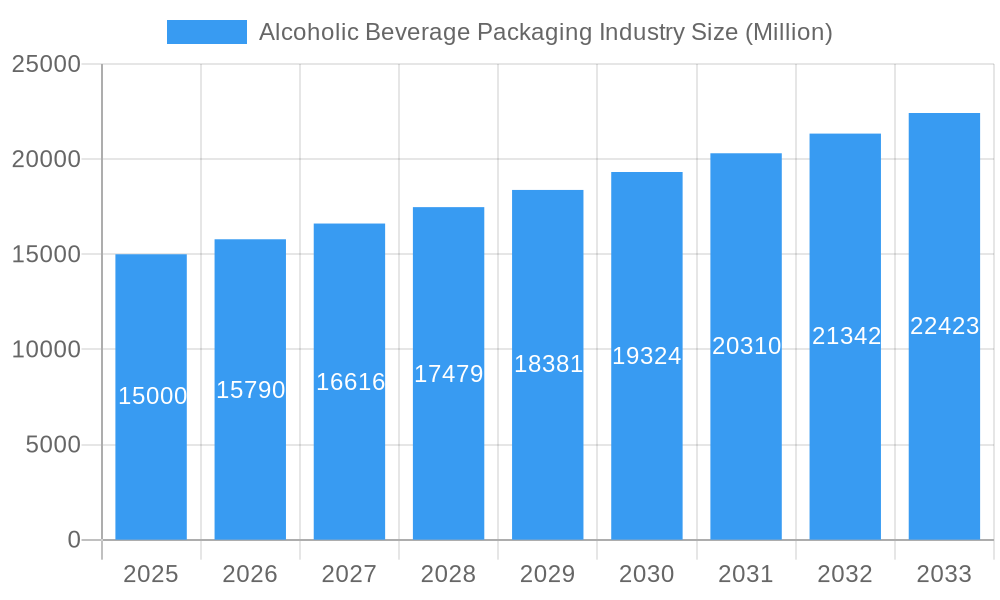

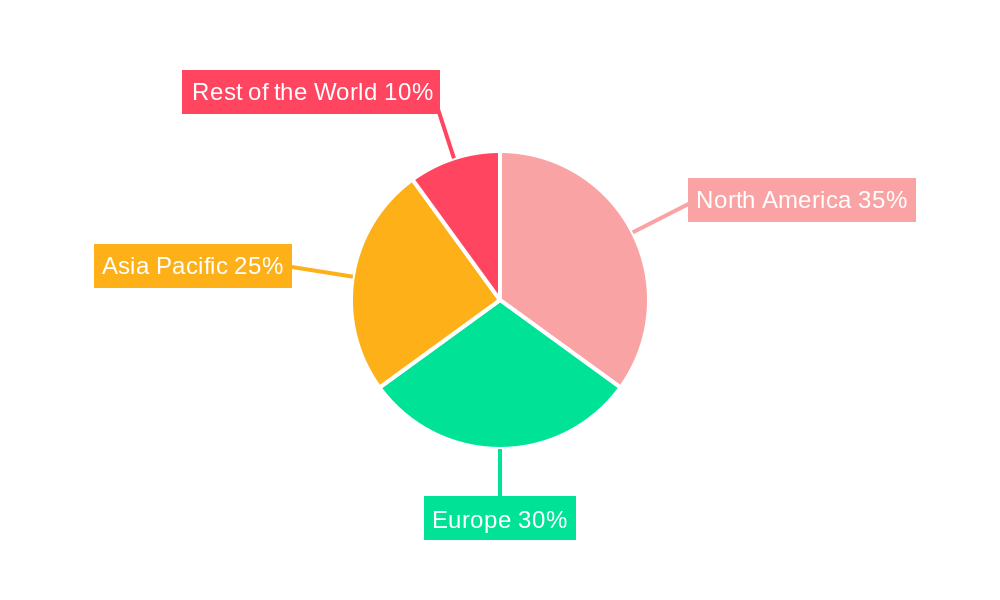

The alcoholic beverage packaging market, valued at approximately $XX million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 5.13% from 2025 to 2033. This expansion is driven by several key factors. The rising demand for alcoholic beverages globally, fueled by increasing disposable incomes and changing consumer preferences, is a significant contributor. Furthermore, the industry's continuous innovation in packaging materials, focusing on sustainability and enhanced consumer experience (e.g., lightweighting, improved recyclability, and unique designs), is boosting market growth. The shift towards premiumization, with consumers increasingly opting for higher-quality and more aesthetically appealing packaging, also presents significant opportunities. However, fluctuating raw material prices and stringent regulatory requirements regarding packaging materials, particularly concerning sustainability and environmental impact, pose considerable challenges to market players. The market segmentation reveals a strong preference for glass and metal packaging in premium segments, while plastic continues to dominate the mass-market segment. Geographic distribution shows a strong presence in North America and Europe, with rapidly expanding markets in Asia-Pacific, particularly China and India. The competitive landscape is characterized by a mix of large multinational corporations and regional players, all vying for market share through product innovation and strategic partnerships.

Alcoholic Beverage Packaging Industry Market Size (In Billion)

The forecast period (2025-2033) will witness a continued focus on sustainability. Companies are actively investing in research and development to create eco-friendly packaging options, including biodegradable and compostable materials. This trend is further accelerated by increasing consumer awareness of environmental concerns and stricter governmental regulations. The market will also see increased adoption of innovative packaging technologies, such as smart packaging and tamper-evident closures, to enhance product security and consumer trust. Competition will intensify as players strive to improve their supply chain efficiency and explore new market segments, such as craft beverages and ready-to-drink cocktails. Growth will be significantly influenced by evolving consumer preferences, technological advancements, and the overall economic landscape.

Alcoholic Beverage Packaging Industry Company Market Share

Alcoholic Beverage Packaging Market Report: 2019-2033 Forecast

This comprehensive report provides a detailed analysis of the Alcoholic Beverage Packaging industry, offering actionable insights for stakeholders across the value chain. The study period spans 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report covers key market segments, leading players, and emerging trends, providing a crucial roadmap for strategic decision-making. This report projects a market value exceeding $XX Million by 2033, driven by robust growth across key segments.

Alcoholic Beverage Packaging Industry Market Dynamics & Concentration

The alcoholic beverage packaging market is characterized by moderate concentration, with several major players holding significant market share. Stora Enso Oyj, Oi SA, Nampak Limited, Ball Corporation, Ardagh Group SA, Krones AG, Crown Holdings Inc, Amcor PLC, Mondi PLC, Gerresheimer AG, Berry Global Inc, and Sidel SA are key players, although the market also includes numerous smaller regional and niche players. Market share data reveals that the top 5 players collectively account for approximately 60% of the global market.

Key Dynamics:

- Innovation Drivers: Sustainable packaging solutions, lightweighting technologies, and enhanced barrier properties are key drivers.

- Regulatory Frameworks: Evolving regulations regarding material usage (e.g., plastic reduction) and labeling requirements are significantly impacting the industry.

- Product Substitutes: The rise of alternative packaging materials and innovations in closures constantly presents competitive challenges.

- End-User Trends: Growing demand for premiumization and convenience drives innovations in packaging design and functionality.

- M&A Activities: The last five years have seen approximately 200 M&A deals in the industry, indicating consolidation and expansion strategies amongst key players.

Alcoholic Beverage Packaging Industry Industry Trends & Analysis

The alcoholic beverage packaging market exhibits a strong growth trajectory, driven by increasing alcohol consumption globally, coupled with changing consumer preferences and technological advancements. The market is expected to register a Compound Annual Growth Rate (CAGR) of approximately 4% during the forecast period (2025-2033). Increased demand for convenient packaging formats, such as single-serve cans and ready-to-drink (RTD) bottles, significantly contributes to this growth. Technological disruptions such as the adoption of advanced printing techniques and smart packaging solutions are reshaping the market landscape.

Key Growth Drivers:

- Rising Disposable Incomes: Increased purchasing power, especially in developing economies, fuels demand for premium alcoholic beverages, often packaged in more sophisticated materials.

- E-commerce Growth: The rise of online alcohol sales necessitates packaging solutions that enhance product protection and durability during shipping.

- Sustainability Concerns: Growing consumer awareness of environmental issues drives demand for sustainable and recyclable packaging options.

- Premiumization: Consumers increasingly seek premium and sophisticated alcoholic beverages, often reflected in their packaging.

- Market Penetration: The penetration of innovative packaging formats, such as cans in the wine market, is constantly expanding.

Leading Markets & Segments in Alcoholic Beverage Packaging Industry

The alcoholic beverage packaging market is geographically diverse, with North America and Europe currently representing the largest regions. However, Asia-Pacific is demonstrating rapid growth, driven by increasing consumption and economic expansion.

By Material:

- Metal: Metal cans and bottles dominate the market, particularly in the beer and carbonated alcoholic beverage sectors. Key drivers include their superior barrier properties and recyclability.

- Glass: Glass bottles remain popular for premium spirits and wines, reflecting their perceived quality and elegance. However, concerns about weight and fragility are prompting the exploration of alternative solutions.

- Plastic: Plastic bottles are prevalent in the spirits, wine, and RTD segments, due to their lightweight nature and cost-effectiveness. However, sustainability concerns are driving the search for eco-friendly alternatives.

- Other Materials: Materials like cardboard and paperboard are increasingly used for secondary packaging and labels, reflecting growing sustainability trends.

By Product:

- Bottles: Bottles continue to be the dominant packaging format, particularly in the wine and spirits sectors.

- Cans: The popularity of cans, particularly aluminum cans, is rapidly expanding, fueled by their portability, convenience, and recyclability. This is particularly prominent in the beer and RTD segments.

- Other Products: Pouches, kegs, and other packaging formats cater to specialized segments.

Key Regional Drivers:

- North America: Strong consumer demand, coupled with robust economic conditions and innovation in packaging solutions, is driving significant growth.

- Europe: Mature markets with established regulatory frameworks influence packaging choices and adoption of sustainable solutions.

- Asia-Pacific: Rapid economic growth, coupled with rising disposable incomes and increasing alcohol consumption, fuel market expansion.

Alcoholic Beverage Packaging Industry Product Developments

Recent innovations focus on lightweighting, improved barrier properties, enhanced recyclability, and the integration of smart packaging features. Examples include the development of innovative closures that improve tamper evidence and enhance convenience, as well as the use of recycled materials and biodegradable alternatives. These trends directly address consumer demand for sustainable and convenient packaging solutions, boosting market competitiveness.

Key Drivers of Alcoholic Beverage Packaging Growth

Technological advancements, particularly in material science and printing technologies, are key growth drivers. Economic factors, such as rising disposable incomes and changing consumer preferences, also play a crucial role. Moreover, favorable regulatory environments promoting sustainability are fostering the adoption of eco-friendly packaging solutions.

Challenges in the Alcoholic Beverage Packaging Industry Market

The industry faces challenges related to fluctuating raw material prices, stringent regulatory requirements regarding material composition and labeling, and the growing pressure to minimize environmental impact. Supply chain disruptions, exacerbated by global events, also pose significant risks. Intense competition, both domestically and internationally, forces continuous innovation and cost optimization. These factors may collectively impact industry growth by approximately 2% annually.

Emerging Opportunities in Alcoholic Beverage Packaging Industry

The industry is poised for growth through strategic partnerships, focusing on collaborative R&D to develop sustainable packaging solutions. Market expansion into rapidly developing economies, coupled with the exploration of new packaging formats and technologies (e.g., active and intelligent packaging), presents significant long-term opportunities.

Leading Players in the Alcoholic Beverage Packaging Industry Sector

- Stora Enso Oyj

- Oi SA

- Nampak Limited

- Ball Corporation

- Ardagh Group SA

- Krones AG

- Crown Holdings Inc

- Amcor PLC

- Mondi PLC

- Gerresheimer AG

- Berry Global Inc

- Sidel SA

Key Milestones in Alcoholic Beverage Packaging Industry Industry

- 2020: Increased focus on sustainable packaging solutions driven by heightened environmental concerns.

- 2021: Several major players announced significant investments in recycling infrastructure and the development of eco-friendly materials.

- 2022: New regulations related to plastic packaging came into effect in several key markets.

- 2023: Several innovative closures and packaging formats were launched, addressing consumer demand for convenience and sustainability.

Strategic Outlook for Alcoholic Beverage Packaging Market

The alcoholic beverage packaging market is poised for continued growth, driven by technological advancements, changing consumer preferences, and a growing focus on sustainability. Strategic partnerships and investments in R&D will be crucial for navigating industry challenges and capitalizing on emerging opportunities. The market's future potential lies in the development and adoption of innovative, sustainable, and convenient packaging solutions.

Alcoholic Beverage Packaging Industry Segmentation

-

1. Material

- 1.1. Glass

- 1.2. Metal

- 1.3. Plastic

- 1.4. Other Materials

-

2. Product

- 2.1. Cans

- 2.2. Bottles

- 2.3. Other Products

Alcoholic Beverage Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. Unites States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. Latin America

- 4.2. Middle East

Alcoholic Beverage Packaging Industry Regional Market Share

Geographic Coverage of Alcoholic Beverage Packaging Industry

Alcoholic Beverage Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Glass

- 5.1.2. Metal

- 5.1.3. Plastic

- 5.1.4. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Cans

- 5.2.2. Bottles

- 5.2.3. Other Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Global Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Glass

- 6.1.2. Metal

- 6.1.3. Plastic

- 6.1.4. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Cans

- 6.2.2. Bottles

- 6.2.3. Other Products

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. North America Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Glass

- 7.1.2. Metal

- 7.1.3. Plastic

- 7.1.4. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Cans

- 7.2.2. Bottles

- 7.2.3. Other Products

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Europe Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Glass

- 8.1.2. Metal

- 8.1.3. Plastic

- 8.1.4. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Cans

- 8.2.2. Bottles

- 8.2.3. Other Products

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Asia Pacific Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Glass

- 9.1.2. Metal

- 9.1.3. Plastic

- 9.1.4. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Cans

- 9.2.2. Bottles

- 9.2.3. Other Products

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Rest of the World Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Glass

- 10.1.2. Metal

- 10.1.3. Plastic

- 10.1.4. Other Materials

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Cans

- 10.2.2. Bottles

- 10.2.3. Other Products

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Stora Enso Oyj

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Oi SA

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Nampak Limited

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Ball Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Ardagh Group SA

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Krones AG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Crown Holdings Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Amcor PLC

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Mondi PLC

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Gerresheimer AG*List Not Exhaustive

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Berry Global Inc

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Sidel SA

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 Stora Enso Oyj

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Alcoholic Beverage Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Alcoholic Beverage Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 3: North America Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 4: North America Alcoholic Beverage Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 5: North America Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Alcoholic Beverage Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Alcoholic Beverage Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 9: Europe Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 10: Europe Alcoholic Beverage Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 11: Europe Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 12: Europe Alcoholic Beverage Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Alcoholic Beverage Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 15: Asia Pacific Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 16: Asia Pacific Alcoholic Beverage Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 17: Asia Pacific Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 18: Asia Pacific Alcoholic Beverage Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Alcoholic Beverage Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 21: Rest of the World Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 22: Rest of the World Alcoholic Beverage Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 23: Rest of the World Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 24: Rest of the World Alcoholic Beverage Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 2: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 3: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 5: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 6: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Unites States Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 10: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 11: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Germany Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: United Kingdom Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 17: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 18: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: China Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Japan Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: India Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 24: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 25: Global Alcoholic Beverage Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Latin America Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Middle East Alcoholic Beverage Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Alcoholic Beverage Packaging Industry?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Alcoholic Beverage Packaging Industry?

Key companies in the market include Stora Enso Oyj, Oi SA, Nampak Limited, Ball Corporation, Ardagh Group SA, Krones AG, Crown Holdings Inc, Amcor PLC, Mondi PLC, Gerresheimer AG*List Not Exhaustive, Berry Global Inc, Sidel SA.

3. What are the main segments of the Alcoholic Beverage Packaging Industry?

The market segments include Material, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 157.28 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Consumption of Alcoholic Beverages; Increased Focus on Recycling; Rising Demand for Long Shelf Life of the Product.

6. What are the notable trends driving market growth?

Glass Packaging Segment to Account for a Crucial Share.

7. Are there any restraints impacting market growth?

; Implementation of Stringent Regulations on Packaging Materials.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Alcoholic Beverage Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Alcoholic Beverage Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Alcoholic Beverage Packaging Industry?

To stay informed about further developments, trends, and reports in the Alcoholic Beverage Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence