Key Insights

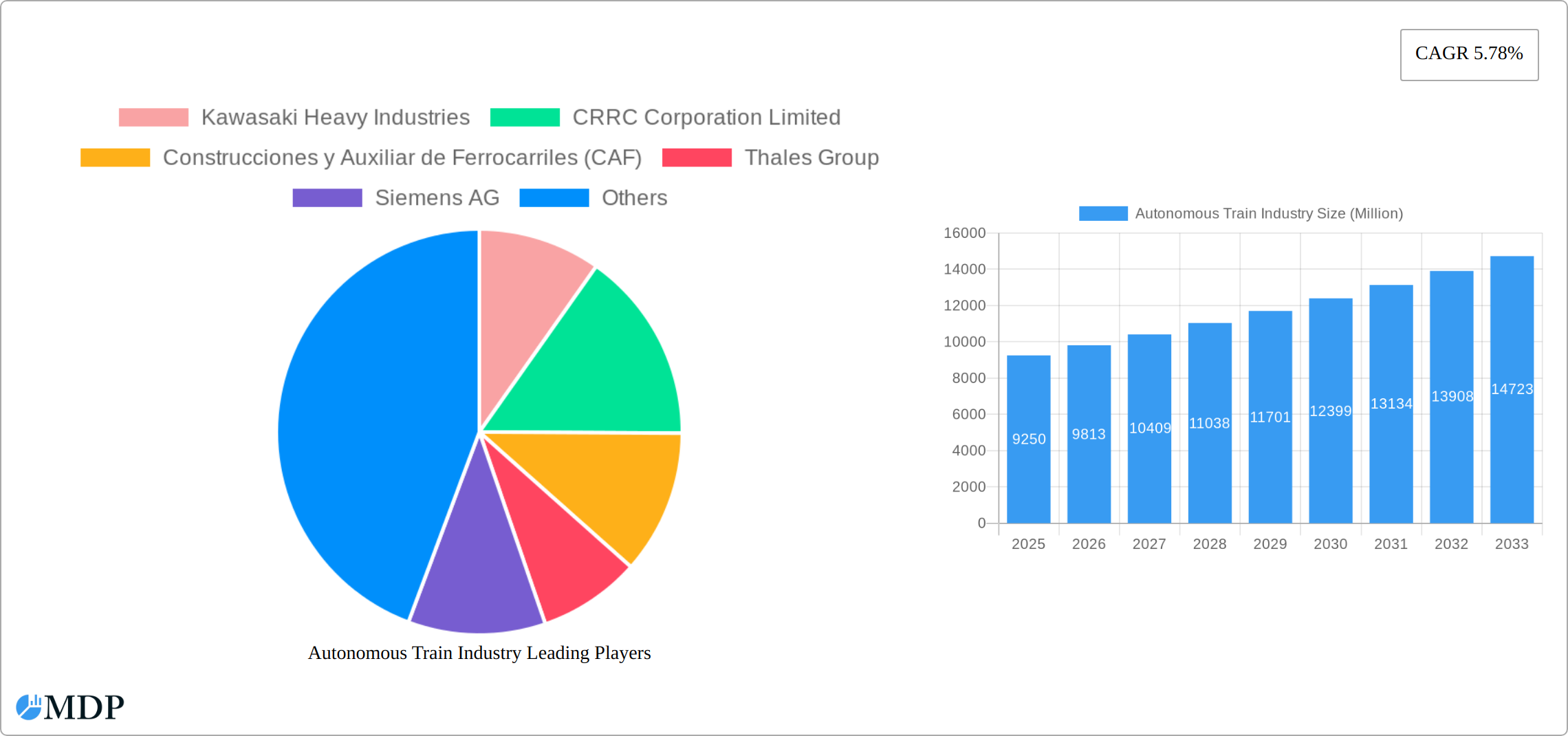

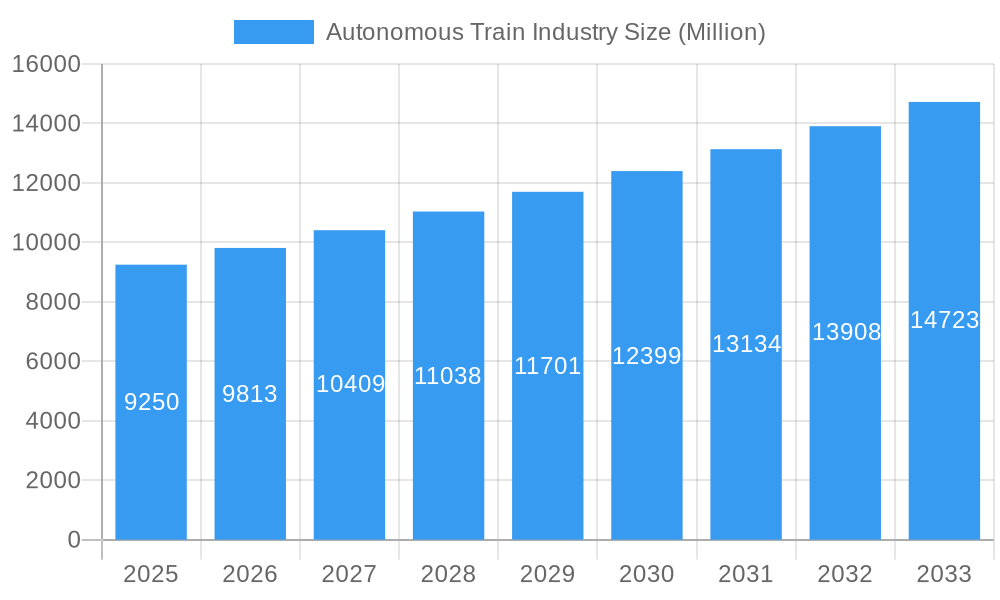

The autonomous train market, valued at $9.25 billion in 2025, is poised for significant growth, driven by increasing urbanization, rising passenger and freight transportation demands, and the need for improved efficiency and safety in rail operations. The market's Compound Annual Growth Rate (CAGR) of 5.78% from 2025 to 2033 projects substantial expansion, reaching an estimated value exceeding $15 billion by 2033. Key technological drivers include the adoption of advanced train control systems such as Communication-Based Train Control (CBTC), European Rail Traffic Management System (ERTMS), Automatic Train Control (ATC), and Positive Train Control (PTC). These systems enable automation across various train types, including metro/monorail, light rail, and high-speed rail, catering to both passenger and freight applications. Growth is further fueled by government initiatives promoting sustainable transportation and investments in infrastructure modernization globally. While initial infrastructure investments represent a significant restraint, the long-term cost savings and efficiency gains associated with autonomous operations are expected to outweigh these initial hurdles. Furthermore, the gradual expansion of autonomous train technologies across different automation grades (GoA levels 1-4) will facilitate a phased market adoption, fostering growth across the forecast period.

Autonomous Train Industry Market Size (In Billion)

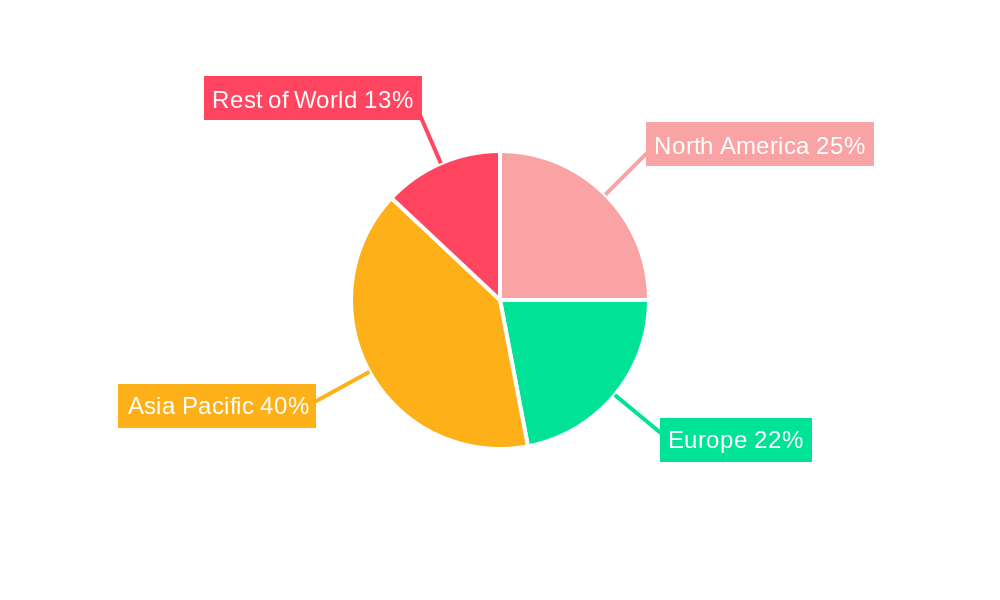

Segmentation analysis reveals a dynamic market landscape. While passenger transport currently dominates, the freight segment is experiencing considerable growth potential as autonomous systems enhance logistics efficiency. Geographically, the Asia-Pacific region is anticipated to lead the market due to extensive infrastructure development and high population density, followed by North America and Europe. Key players like Kawasaki Heavy Industries, CRRC Corporation Limited, and Siemens AG are driving innovation and competition, constantly improving technologies and expanding their global presence. The competitive landscape is marked by strategic partnerships, technological advancements, and a strong focus on meeting the evolving needs of diverse rail transportation sectors. This combination of technological advancements, increasing demand, and strategic investments points towards a future where autonomous trains play a crucial role in the global transportation landscape.

Autonomous Train Industry Company Market Share

Autonomous Train Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Autonomous Train Industry, projecting a market value of xx Million by 2033. It covers market dynamics, leading players, technological advancements, and future growth opportunities, offering actionable insights for stakeholders across the value chain. The report utilizes data from the historical period (2019-2024), base year (2025), and forecast period (2025-2033) to provide a robust and reliable outlook.

Autonomous Train Industry Market Dynamics & Concentration

The autonomous train market is experiencing robust growth fueled by increasing investments in public transportation infrastructure and a growing demand for efficient and safe transit systems. Market concentration is moderate, with several key players holding significant market share. However, the market is characterized by intense competition, driven by technological innovation and strategic partnerships.

Market Concentration: The top five players (Kawasaki Heavy Industries, CRRC Corporation Limited, CAF, Siemens AG, and Alstom SA) collectively hold an estimated xx% market share in 2025, indicating a moderately consolidated market. However, the presence of numerous smaller players, particularly in niche segments, prevents complete dominance by a few large corporations.

Innovation Drivers: Technological advancements in areas such as CBTC, ERTMS, ATC, and PTC are key innovation drivers, enabling higher levels of automation and operational efficiency. Government regulations promoting the adoption of autonomous technologies are further accelerating growth.

Regulatory Frameworks: Stringent safety regulations and standardization efforts are shaping the market landscape. Compliance with these standards is crucial for market entry and success. Variations in regulations across different regions may lead to localized opportunities.

Product Substitutes: While there are no direct substitutes for autonomous trains in their primary applications, competing transportation modes such as automated road transport systems and air travel represent indirect substitutes. The competitive advantage of autonomous trains lies in their capacity, efficiency, and environmental impact.

End-User Trends: Urbanization, increasing passenger volumes, and growing environmental concerns are driving the demand for efficient and sustainable mass transit solutions. End-users increasingly favor systems with enhanced passenger comfort, safety features, and reliable operations.

M&A Activities: The number of M&A deals in the autonomous train industry averaged xx per year during the period 2019-2024, reflecting strategic efforts by companies to expand their market reach and technological capabilities. These acquisitions often involve smaller technology companies specializing in specific automation components or software solutions.

Autonomous Train Industry Industry Trends & Analysis

The autonomous train market is experiencing substantial and accelerating growth, propelled by a confluence of transformative trends. Industry analysts project a robust Compound Annual Growth Rate (CAGR) of approximately **15-18%** during the forecast period (2025-2033), with market penetration expected to surge from an estimated **10-12%** in 2025 to a significant **35-40%** by 2033. This impressive expansion is underpinned by several pivotal factors:

- Technological Advancements & AI Integration: The industry is witnessing rapid innovation, particularly in the realm of artificial intelligence (AI) for predictive analytics, real-time decision-making, and advanced control systems. The integration of sophisticated sensor suites, including LiDAR, radar, and advanced vision systems, is crucial for enabling higher levels of automation, moving towards the fully automated Grade of Automation 4 (GoA 4). This technological evolution is not only enhancing performance but also opening new avenues for operational efficiency and safety.

- Governmental Support & Infrastructure Investment: Proactive government initiatives and substantial investments in smart infrastructure are key enablers. Many nations are prioritizing the adoption of autonomous train systems to enhance passenger safety, optimize operational efficiency, reduce human error, and achieve significant cost savings in the long run. This strategic push is creating a fertile ground for market expansion.

- Evolving Passenger Expectations: Passengers are increasingly demanding higher standards of safety, punctuality, and comfort. Autonomous train systems, with their potential for consistent performance, reduced delays, and enhanced onboard experiences, are well-positioned to meet these evolving preferences, driving strong public acceptance and market demand.

- Intensifying Competitive Landscape & Ecosystem Collaboration: The autonomous train sector is characterized by dynamic competition. Established industry giants are collaborating with innovative technology startups, fostering an environment of accelerated innovation. This competitive synergy is driving down costs, improving product offerings, and expanding the geographical reach of autonomous solutions.

Leading Markets & Segments in Autonomous Train Industry

The global autonomous train market is currently led by the Asia-Pacific region, fueled by extensive infrastructure development and rapid urbanization. Europe and North America follow closely, with increasing adoption driven by a focus on sustainable transportation and technological innovation. Within this dynamic landscape, significant growth opportunities are emerging across various segments:

- By Automation Grade: Systems achieving Grade of Automation 4 (GoA 4), representing fully automated operations, are experiencing the most rapid growth, particularly in high-density urban environments like metro and subway systems. GoA 3 (driverless operation with onboard supervision) is also seeing substantial traction as a stepping stone to full autonomy.

- By Application: While the passenger transportation segment currently dominates the market, the freight and logistics segment presents a compelling growth trajectory. The drive for greater efficiency, reliability, and safety in supply chains is accelerating the adoption of autonomous solutions for cargo transport.

- By Technology: Communication-Based Train Control (CBTC) and the European Rail Traffic Management System (ERTMS) remain the leading technologies, forming the backbone of many autonomous deployments. However, Positive Train Control (PTC) is experiencing rapid adoption in specific regions, especially North America. The continuous evolution and integration of advanced technologies, including 5G communication and edge computing, are expected to further shape market dynamics.

- By Train Type: Metro and monorail systems currently hold a dominant market share due to their established operational environments and high passenger volumes. However, significant investments and technological advancements are driving the expansion of autonomous capabilities into high-speed rail and light rail systems, promising enhanced efficiency and passenger experience across the board.

Key Growth Drivers by Region/Segment:

- Asia-Pacific: Unprecedented urbanization, substantial government investments in high-speed rail and metro networks, and a strong embrace of cutting-edge technologies are the primary catalysts for the region's market leadership.

- Europe: A strong commitment to sustainable mobility, pioneering advancements in railway infrastructure, and stringent safety regulations are compelling the widespread adoption of autonomous train solutions.

- North America: Significant investments in modernizing urban transit systems, coupled with a growing emphasis on improving the efficiency and capacity of existing rail infrastructure, are fostering robust growth in the autonomous train segment.

Autonomous Train Industry Product Developments

Recent product innovations in the autonomous train industry are sharply focused on elevating automation levels, enhancing passenger safety and comfort, and optimizing operational efficiency. Key advancements include the development of sophisticated AI-powered predictive maintenance systems that minimize downtime and maintenance costs, and the implementation of advanced communication and sensing technologies for seamless train-to-infrastructure and train-to-train interaction. Furthermore, solutions are emerging to improve energy efficiency through optimized acceleration and braking profiles. Companies are building competitive advantages through robust cybersecurity frameworks to protect sensitive operational data and by ensuring seamless integration with existing rail networks to facilitate widespread adoption.

Key Drivers of Autonomous Train Industry Growth

The autonomous train industry is propelled by a confluence of factors including:

- Technological advancements: AI, sensor technology, and advanced communication systems are driving improved automation capabilities and operational efficiency.

- Economic benefits: Automation offers significant cost reductions for railway operators through improved efficiency and reduced labor costs.

- Regulatory support: Government initiatives supporting the adoption of autonomous technologies accelerate market growth.

Challenges in the Autonomous Train Industry Market

Several factors hinder the market's growth, including:

- High initial investment costs: The substantial investment needed for infrastructure upgrades and system implementation can be a barrier to entry.

- Safety regulations and certification processes: Stringent safety regulations add complexity and time to deployment.

- Cybersecurity concerns: The increasing reliance on digital systems necessitates robust cybersecurity measures to mitigate potential risks.

Emerging Opportunities in Autonomous Train Industry

The long-term growth of the autonomous train industry is fueled by several key opportunities. Significant potential exists in expanding into underserved markets, developing advanced automation technologies, and forging strategic partnerships to accelerate market penetration.

Leading Players in the Autonomous Train Industry Sector

- Kawasaki Heavy Industries

- CRRC Corporation Limited

- Construcciones y Auxiliar de Ferrocarriles (CAF)

- Thales Group

- Siemens AG

- Alstom SA

- Hitachi Rail STS (formerly Ansaldo STS)

- Ingeteam Corporation S.A.

- Wabtec Corporation

- Mitsubishi Heavy Industries Ltd

Key Milestones in Autonomous Train Industry Industry

- May 2021: Kawasaki Heavy Industries introduced advanced remote track monitoring services, enhancing operational safety and efficiency in North America.

- July 2021: Ningbo Rail Transit Group, in collaboration with CRRC, unveiled the first smart metro train with fully autonomous operational capabilities, marking a significant leap in urban rail technology.

- August 2021: Siemens Mobility secured a pivotal contract to supply its cutting-edge CBTC technology for the high-profile Malaysia-Singapore cross-border rail link, facilitating seamless and efficient operations.

- September 2021: Mitsubishi Heavy Industries commenced operations of the fully automated Dubai Metro, showcasing a remarkable achievement in large-scale autonomous public transportation.

- June 2022: The German Aerospace Centre (DLR) and TU Berlin, in partnership with Alstom, initiated a collaborative project focused on developing advanced solutions for the digitization of German rail passenger transport, paving the way for future autonomous systems.

Strategic Outlook for Autonomous Train Industry Market

The autonomous train market holds significant future potential. Continued technological advancements, strategic partnerships, and government support will drive substantial growth, leading to wider adoption across various regions and applications. Companies focusing on innovation, integration, and robust safety standards are poised to benefit from this expanding market.

Autonomous Train Industry Segmentation

-

1. Automation Grade

- 1.1. GoA 1

- 1.2. GoA 2

- 1.3. GoA 3

- 1.4. GoA 4

-

2. Application

- 2.1. Passenger

- 2.2. Freight

-

3. Technology

- 3.1. CBTC

- 3.2. ERTMS

- 3.3. ATC

- 3.4. PTC

-

4. Train Type

- 4.1. Metro/Monorail

- 4.2. Light Rail

- 4.3. High-speed Rail

Autonomous Train Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Autonomous Train Industry Regional Market Share

Geographic Coverage of Autonomous Train Industry

Autonomous Train Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.78% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Automation Grade

- 5.1.1. GoA 1

- 5.1.2. GoA 2

- 5.1.3. GoA 3

- 5.1.4. GoA 4

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Passenger

- 5.2.2. Freight

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. CBTC

- 5.3.2. ERTMS

- 5.3.3. ATC

- 5.3.4. PTC

- 5.4. Market Analysis, Insights and Forecast - by Train Type

- 5.4.1. Metro/Monorail

- 5.4.2. Light Rail

- 5.4.3. High-speed Rail

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Automation Grade

- 6. Global Autonomous Train Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Automation Grade

- 6.1.1. GoA 1

- 6.1.2. GoA 2

- 6.1.3. GoA 3

- 6.1.4. GoA 4

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Passenger

- 6.2.2. Freight

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. CBTC

- 6.3.2. ERTMS

- 6.3.3. ATC

- 6.3.4. PTC

- 6.4. Market Analysis, Insights and Forecast - by Train Type

- 6.4.1. Metro/Monorail

- 6.4.2. Light Rail

- 6.4.3. High-speed Rail

- 6.1. Market Analysis, Insights and Forecast - by Automation Grade

- 7. North America Autonomous Train Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Automation Grade

- 7.1.1. GoA 1

- 7.1.2. GoA 2

- 7.1.3. GoA 3

- 7.1.4. GoA 4

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Passenger

- 7.2.2. Freight

- 7.3. Market Analysis, Insights and Forecast - by Technology

- 7.3.1. CBTC

- 7.3.2. ERTMS

- 7.3.3. ATC

- 7.3.4. PTC

- 7.4. Market Analysis, Insights and Forecast - by Train Type

- 7.4.1. Metro/Monorail

- 7.4.2. Light Rail

- 7.4.3. High-speed Rail

- 7.1. Market Analysis, Insights and Forecast - by Automation Grade

- 8. Europe Autonomous Train Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Automation Grade

- 8.1.1. GoA 1

- 8.1.2. GoA 2

- 8.1.3. GoA 3

- 8.1.4. GoA 4

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Passenger

- 8.2.2. Freight

- 8.3. Market Analysis, Insights and Forecast - by Technology

- 8.3.1. CBTC

- 8.3.2. ERTMS

- 8.3.3. ATC

- 8.3.4. PTC

- 8.4. Market Analysis, Insights and Forecast - by Train Type

- 8.4.1. Metro/Monorail

- 8.4.2. Light Rail

- 8.4.3. High-speed Rail

- 8.1. Market Analysis, Insights and Forecast - by Automation Grade

- 9. Asia Pacific Autonomous Train Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Automation Grade

- 9.1.1. GoA 1

- 9.1.2. GoA 2

- 9.1.3. GoA 3

- 9.1.4. GoA 4

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Passenger

- 9.2.2. Freight

- 9.3. Market Analysis, Insights and Forecast - by Technology

- 9.3.1. CBTC

- 9.3.2. ERTMS

- 9.3.3. ATC

- 9.3.4. PTC

- 9.4. Market Analysis, Insights and Forecast - by Train Type

- 9.4.1. Metro/Monorail

- 9.4.2. Light Rail

- 9.4.3. High-speed Rail

- 9.1. Market Analysis, Insights and Forecast - by Automation Grade

- 10. Rest of the World Autonomous Train Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Automation Grade

- 10.1.1. GoA 1

- 10.1.2. GoA 2

- 10.1.3. GoA 3

- 10.1.4. GoA 4

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Passenger

- 10.2.2. Freight

- 10.3. Market Analysis, Insights and Forecast - by Technology

- 10.3.1. CBTC

- 10.3.2. ERTMS

- 10.3.3. ATC

- 10.3.4. PTC

- 10.4. Market Analysis, Insights and Forecast - by Train Type

- 10.4.1. Metro/Monorail

- 10.4.2. Light Rail

- 10.4.3. High-speed Rail

- 10.1. Market Analysis, Insights and Forecast - by Automation Grade

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Kawasaki Heavy Industries

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 CRRC Corporation Limited

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Construcciones y Auxiliar de Ferrocarriles (CAF)

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Thales Group

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Siemens AG

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Alstom SA

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Hitachi Rail STS (Ansaldo STS)

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Ingeteam Corporation S

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Wabtec Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Mitsubishi Heavy Industries Ltd

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Kawasaki Heavy Industries

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Autonomous Train Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Autonomous Train Industry Revenue (Million), by Automation Grade 2025 & 2033

- Figure 3: North America Autonomous Train Industry Revenue Share (%), by Automation Grade 2025 & 2033

- Figure 4: North America Autonomous Train Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Autonomous Train Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Autonomous Train Industry Revenue (Million), by Technology 2025 & 2033

- Figure 7: North America Autonomous Train Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 8: North America Autonomous Train Industry Revenue (Million), by Train Type 2025 & 2033

- Figure 9: North America Autonomous Train Industry Revenue Share (%), by Train Type 2025 & 2033

- Figure 10: North America Autonomous Train Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Autonomous Train Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Autonomous Train Industry Revenue (Million), by Automation Grade 2025 & 2033

- Figure 13: Europe Autonomous Train Industry Revenue Share (%), by Automation Grade 2025 & 2033

- Figure 14: Europe Autonomous Train Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Europe Autonomous Train Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Autonomous Train Industry Revenue (Million), by Technology 2025 & 2033

- Figure 17: Europe Autonomous Train Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 18: Europe Autonomous Train Industry Revenue (Million), by Train Type 2025 & 2033

- Figure 19: Europe Autonomous Train Industry Revenue Share (%), by Train Type 2025 & 2033

- Figure 20: Europe Autonomous Train Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Autonomous Train Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Autonomous Train Industry Revenue (Million), by Automation Grade 2025 & 2033

- Figure 23: Asia Pacific Autonomous Train Industry Revenue Share (%), by Automation Grade 2025 & 2033

- Figure 24: Asia Pacific Autonomous Train Industry Revenue (Million), by Application 2025 & 2033

- Figure 25: Asia Pacific Autonomous Train Industry Revenue Share (%), by Application 2025 & 2033

- Figure 26: Asia Pacific Autonomous Train Industry Revenue (Million), by Technology 2025 & 2033

- Figure 27: Asia Pacific Autonomous Train Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Asia Pacific Autonomous Train Industry Revenue (Million), by Train Type 2025 & 2033

- Figure 29: Asia Pacific Autonomous Train Industry Revenue Share (%), by Train Type 2025 & 2033

- Figure 30: Asia Pacific Autonomous Train Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Autonomous Train Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Rest of the World Autonomous Train Industry Revenue (Million), by Automation Grade 2025 & 2033

- Figure 33: Rest of the World Autonomous Train Industry Revenue Share (%), by Automation Grade 2025 & 2033

- Figure 34: Rest of the World Autonomous Train Industry Revenue (Million), by Application 2025 & 2033

- Figure 35: Rest of the World Autonomous Train Industry Revenue Share (%), by Application 2025 & 2033

- Figure 36: Rest of the World Autonomous Train Industry Revenue (Million), by Technology 2025 & 2033

- Figure 37: Rest of the World Autonomous Train Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 38: Rest of the World Autonomous Train Industry Revenue (Million), by Train Type 2025 & 2033

- Figure 39: Rest of the World Autonomous Train Industry Revenue Share (%), by Train Type 2025 & 2033

- Figure 40: Rest of the World Autonomous Train Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Rest of the World Autonomous Train Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autonomous Train Industry Revenue Million Forecast, by Automation Grade 2020 & 2033

- Table 2: Global Autonomous Train Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Autonomous Train Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 4: Global Autonomous Train Industry Revenue Million Forecast, by Train Type 2020 & 2033

- Table 5: Global Autonomous Train Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Autonomous Train Industry Revenue Million Forecast, by Automation Grade 2020 & 2033

- Table 7: Global Autonomous Train Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Autonomous Train Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 9: Global Autonomous Train Industry Revenue Million Forecast, by Train Type 2020 & 2033

- Table 10: Global Autonomous Train Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Autonomous Train Industry Revenue Million Forecast, by Automation Grade 2020 & 2033

- Table 12: Global Autonomous Train Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 13: Global Autonomous Train Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 14: Global Autonomous Train Industry Revenue Million Forecast, by Train Type 2020 & 2033

- Table 15: Global Autonomous Train Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Autonomous Train Industry Revenue Million Forecast, by Automation Grade 2020 & 2033

- Table 17: Global Autonomous Train Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 18: Global Autonomous Train Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 19: Global Autonomous Train Industry Revenue Million Forecast, by Train Type 2020 & 2033

- Table 20: Global Autonomous Train Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Autonomous Train Industry Revenue Million Forecast, by Automation Grade 2020 & 2033

- Table 22: Global Autonomous Train Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 23: Global Autonomous Train Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 24: Global Autonomous Train Industry Revenue Million Forecast, by Train Type 2020 & 2033

- Table 25: Global Autonomous Train Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autonomous Train Industry?

The projected CAGR is approximately 5.78%.

2. Which companies are prominent players in the Autonomous Train Industry?

Key companies in the market include Kawasaki Heavy Industries, CRRC Corporation Limited, Construcciones y Auxiliar de Ferrocarriles (CAF), Thales Group, Siemens AG, Alstom SA, Hitachi Rail STS (Ansaldo STS), Ingeteam Corporation S, Wabtec Corporation, Mitsubishi Heavy Industries Ltd.

3. What are the main segments of the Autonomous Train Industry?

The market segments include Automation Grade, Application, Technology, Train Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.25 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Focus On Safety.

6. What are the notable trends driving market growth?

Metro/Monorail Dominating the Global Autonomous Train Market.

7. Are there any restraints impacting market growth?

High Initial Investment.

8. Can you provide examples of recent developments in the market?

June 2022: The German Aerospace Centre (DLR) and the TU Berlin, Alstom, is developing technical solutions to gradually digitize rail passenger transport in Germany. The project will explore the possibilities of automation in regional transport via the European Train Control System (ETCS).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autonomous Train Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autonomous Train Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autonomous Train Industry?

To stay informed about further developments, trends, and reports in the Autonomous Train Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence