Key Insights

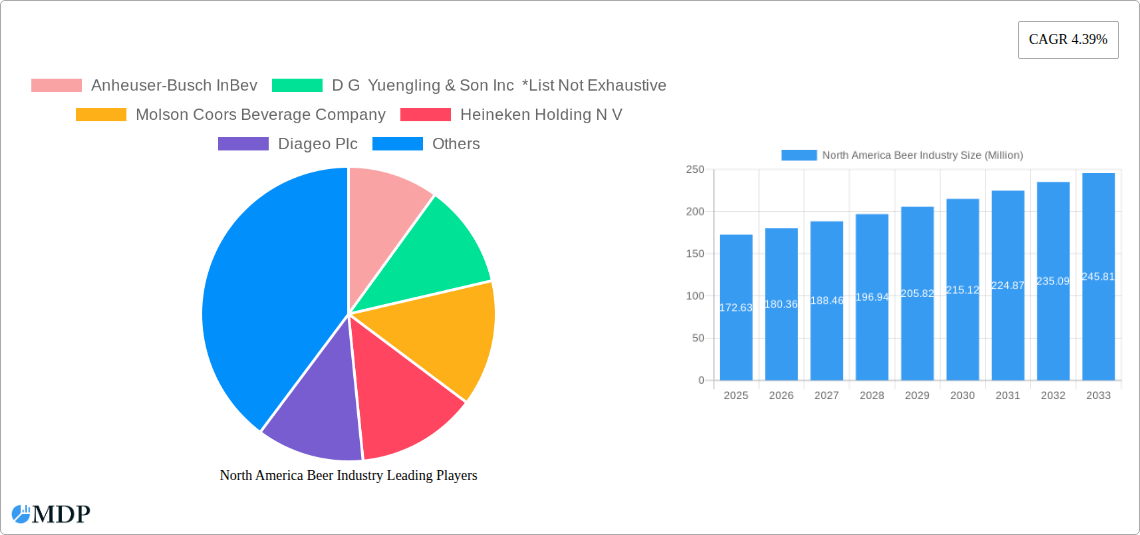

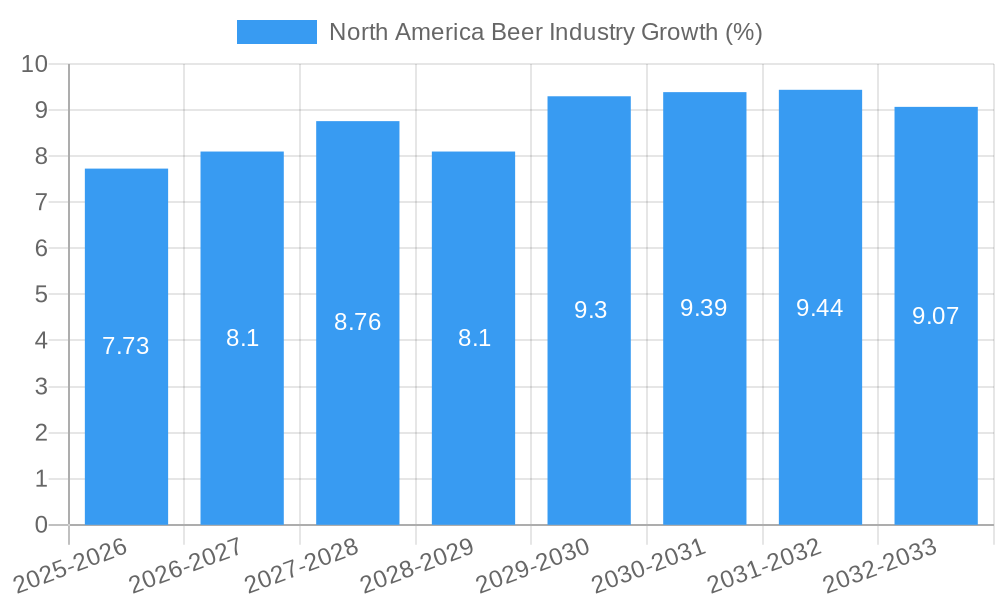

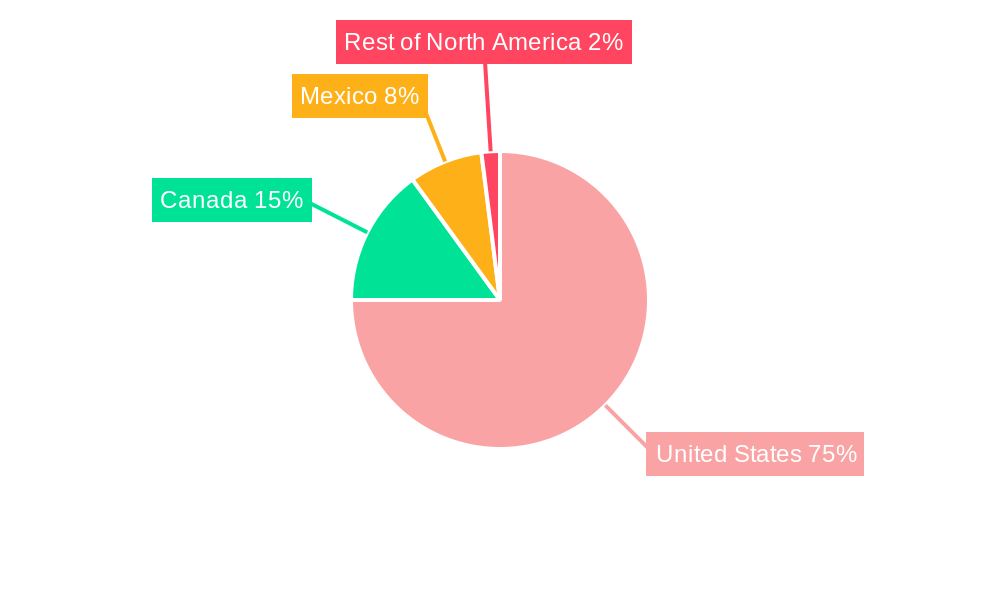

The North American beer market, valued at $172.63 million in 2025, is projected to experience steady growth, driven by several key factors. The increasing popularity of craft beers and diverse flavor profiles caters to evolving consumer preferences, fueling market expansion. Furthermore, strategic marketing campaigns emphasizing premiumization and experiences, coupled with the rise of e-commerce and direct-to-consumer models, are reshaping distribution channels and enhancing accessibility. The on-trade segment, encompassing bars and restaurants, continues to be significant, though the off-trade (retail stores) segment is witnessing robust growth due to convenience and changing consumption habits. While increased excise taxes and health concerns pose challenges, the market's resilience is apparent in its consistent CAGR of 4.39%. Competition remains fierce, with established players like Anheuser-Busch InBev and Molson Coors alongside emerging craft breweries vying for market share. Growth is expected across all major segments, including Lager, Ale, and "Others" (representing specialty beers and imports), with a geographical concentration primarily in the United States, followed by Canada and Mexico.

The forecast period (2025-2033) anticipates a continued expansion of the North American beer market, driven by sustained demand and product innovation. Growth will be fueled by successful branding strategies that leverage social media and targeted advertising to reach specific demographics. The industry is expected to witness increased investment in sustainable practices and eco-friendly packaging in response to consumer concerns. However, potential headwinds, such as economic downturns impacting consumer spending and potential shifts in regulatory frameworks regarding alcohol sales, must be considered. Companies are likely to focus on diversification, strategic partnerships, and innovation to maintain competitiveness and capitalize on emerging opportunities within this dynamic landscape. The market segmentation by distribution channel and beer type will continue to be crucial for understanding consumer behavior and informing targeted strategies.

North America Beer Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the North America beer industry, covering market dynamics, trends, leading players, and future growth prospects. With a focus on the United States, Canada, and Mexico, this report offers crucial insights for industry stakeholders, investors, and strategic decision-makers. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. Key segments analyzed include Lager, Ale, and Others, across On-Trade and Off-Trade distribution channels. The report features data on key players such as Anheuser-Busch InBev, Molson Coors Beverage Company, and Heineken Holding N.V., among others. Projected market values are in Millions.

North America Beer Industry Market Dynamics & Concentration

The North American beer market exhibits a complex interplay of factors influencing its dynamics and concentration. Market share is largely dominated by a few major players, although the craft beer segment continues to carve a niche. The industry faces a constantly evolving regulatory landscape, including alcohol taxes and advertising restrictions. Consumer preferences shift towards premiumization, craft beers, and healthier options, impacting product innovation and competition. Meanwhile, significant M&A activity shapes the competitive landscape.

- Market Concentration: The top 5 players hold approximately xx% of the market share in 2024. This concentration is expected to remain relatively stable, with minor shifts due to M&A activity and emerging craft breweries.

- Innovation Drivers: Consumer demand for diverse flavors, healthier options (low-carb, gluten-free), and unique brewing techniques drive innovation. Technological advancements in brewing and packaging also play a vital role.

- Regulatory Frameworks: Varying regulations across different states and provinces influence production, distribution, and marketing. Compliance costs and restrictions impact smaller players disproportionately.

- Product Substitutes: The rise of hard seltzers, ready-to-drink cocktails, and non-alcoholic beverages poses a competitive threat, forcing brewers to adapt and innovate.

- End-User Trends: Health-conscious consumers are driving demand for lower-calorie and healthier options. Experiential consumption, with a focus on craft breweries and taprooms, also shapes market trends.

- M&A Activities: The number of M&A deals in the North American beer industry averaged xx per year between 2019 and 2024. These deals reflect strategic consolidation and expansion efforts by major players.

North America Beer Industry Industry Trends & Analysis

The North American beer market experienced a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024). Market growth is driven by factors like increasing disposable incomes in some segments, a growing young adult population, and evolving consumer preferences towards premium and craft beers. Technological disruptions, such as the adoption of automated brewing systems and innovative packaging solutions, contribute to efficiency and product diversification. The market penetration of craft beers continues to rise, although it is still a niche segment in overall consumption. Intense competition necessitates continuous innovation and strategic marketing to attract and retain customers.

Leading Markets & Segments in North America Beer Industry

The United States remains the dominant market in North America, accounting for approximately xx% of total volume in 2024. However, Canada and Mexico also show significant growth potential.

Dominant Region: United States.

Key Drivers (United States): Strong consumer spending, established distribution networks, and diverse regional preferences.

Key Drivers (Canada): Growing craft beer scene, government regulations on alcohol sales (regional impacts).

Key Drivers (Mexico): High domestic consumption, increasing tourism.

Dominant Segment (Type): Lager remains the most dominant type, although Ale and “Others” (including craft beer styles) are showing substantial growth.

Dominant Segment (Distribution Channel): Off-trade (retail sales) accounts for a larger market share than On-trade (restaurants and bars).

Detailed Dominance Analysis: The US market's dominance is attributed to its large population, robust economy, and well-established distribution channels. Canadian growth is propelled by its thriving craft beer sector. Mexico's large population and robust domestic consumption make it an important market. The dominance of the Lager segment is primarily driven by its wide appeal and established market share. The growth of the "Others" segment reflects the rising popularity of craft beers and specialized brews.

North America Beer Industry Product Developments

Recent product innovations focus on premiumization, diversification of flavors, and health-conscious options. Technological advancements in brewing, such as precise fermentation control and innovative packaging materials, improve quality, extend shelf life, and enhance consumer experience. The increasing demand for unique and artisanal brews drives the expansion of the craft beer segment, further diversifying the product landscape. The market fit for new products depends heavily on aligning with current consumer trends.

Key Drivers of North America Beer Industry Growth

Several factors fuel the growth of the North American beer industry. Firstly, rising disposable incomes across various demographic segments positively impact spending on premium beverages. Secondly, technological advancements lead to increased efficiency and reduced production costs. Lastly, favorable government policies in certain regions encourage investment and expansion in the brewing sector.

Challenges in the North America Beer Industry Market

The industry faces challenges such as intense competition, stringent regulatory hurdles, and increasing input costs (raw materials, packaging). Fluctuations in raw material prices and supply chain disruptions can impact profitability and product availability. Furthermore, the growing popularity of alternative beverages intensifies competitive pressures, necessitating continuous innovation and marketing efforts. These factors collectively contribute to a xx% decrease in profit margins for smaller companies from 2020 to 2024.

Emerging Opportunities in North America Beer Industry

Long-term growth is driven by several opportunities including expansion into emerging markets within North America, strategic partnerships with distributors and retailers, and the exploration of innovative product lines like ready-to-drink cocktails. Technological breakthroughs and sustainable brewing practices offer added advantages in appealing to environmentally and health-conscious consumers.

Leading Players in the North America Beer Industry Sector

- Anheuser-Busch InBev

- D G Yuengling & Son Inc

- Molson Coors Beverage Company

- Heineken Holding N.V.

- Diageo Plc

- Constellation Brands Inc

- Suntory Beverage & Food Limited

- FIFCO USA

- Carlsberg Group

- Boston Beer Company

Key Milestones in North America Beer Industry Industry

- November 2022: Goose Island Beer Company launches the 2022 edition of Bourbon County Stout in the US.

- July 2022: Royal Unibrew acquires Amsterdam Brewery Co. Ltd., expanding its Canadian capacity.

- March 2022: Modelo launches Modelo Oro premium light beer in Mexico.

Strategic Outlook for North America Beer Industry Market

The North American beer industry presents significant growth potential, fueled by evolving consumer preferences, technological advancements, and strategic partnerships. Further market expansion, particularly in the craft beer segment, promises substantial returns. Adapting to changing consumer demands, embracing sustainable practices, and effectively leveraging digital marketing strategies will be key to success in this dynamic market.

North America Beer Industry Segmentation

-

1. Type

- 1.1. Lager

- 1.2. Ale

- 1.3. Others

-

2. Distribution Channel

- 2.1. On-Trade

- 2.2. Off-Trade

North America Beer Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Beer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.39% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend

- 3.3. Market Restrains

- 3.3.1. Stringent Government Regulations and Product Guidelines

- 3.4. Market Trends

- 3.4.1. Growing Demand for Beer Across the United States

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Lager

- 5.1.2. Ale

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-Trade

- 5.2.2. Off-Trade

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Anheuser-Busch InBev

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 D G Yuengling & Son Inc *List Not Exhaustive

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Molson Coors Beverage Company

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Heineken Holding N V

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Diageo Plc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Constellation Brands Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Suntory Beverage & Food Limited

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 FIFCO USA

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Carlsberg Group

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Boston Beer Company

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Anheuser-Busch InBev

List of Figures

- Figure 1: North America Beer Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Beer Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Beer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Beer Industry Volume liter Forecast, by Region 2019 & 2032

- Table 3: North America Beer Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: North America Beer Industry Volume liter Forecast, by Type 2019 & 2032

- Table 5: North America Beer Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: North America Beer Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 7: North America Beer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: North America Beer Industry Volume liter Forecast, by Region 2019 & 2032

- Table 9: North America Beer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: North America Beer Industry Volume liter Forecast, by Country 2019 & 2032

- Table 11: United States North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United States North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 13: Canada North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Mexico North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 17: Rest of North America North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Rest of North America North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 19: North America Beer Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 20: North America Beer Industry Volume liter Forecast, by Type 2019 & 2032

- Table 21: North America Beer Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 22: North America Beer Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 23: North America Beer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: North America Beer Industry Volume liter Forecast, by Country 2019 & 2032

- Table 25: United States North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: United States North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 27: Canada North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Canada North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 29: Mexico North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Mexico North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Beer Industry?

The projected CAGR is approximately 4.39%.

2. Which companies are prominent players in the North America Beer Industry?

Key companies in the market include Anheuser-Busch InBev, D G Yuengling & Son Inc *List Not Exhaustive, Molson Coors Beverage Company, Heineken Holding N V, Diageo Plc, Constellation Brands Inc, Suntory Beverage & Food Limited, FIFCO USA, Carlsberg Group, Boston Beer Company.

3. What are the main segments of the North America Beer Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 172.63 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend.

6. What are the notable trends driving market growth?

Growing Demand for Beer Across the United States.

7. Are there any restraints impacting market growth?

Stringent Government Regulations and Product Guidelines.

8. Can you provide examples of recent developments in the market?

In November 2022, Goose Island Beer Company's Canada branch announced the launch of the 2022 edition of Bourbon County Stout. It was officially introduced in the United States on Black Friday. The 2022 Original Bourbon County Stout was aged in a mix of bourbon barrels from Buffalo Trace, Heaven Hill, and Wild Turkey distilleries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Beer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Beer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Beer Industry?

To stay informed about further developments, trends, and reports in the North America Beer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence