Key Insights

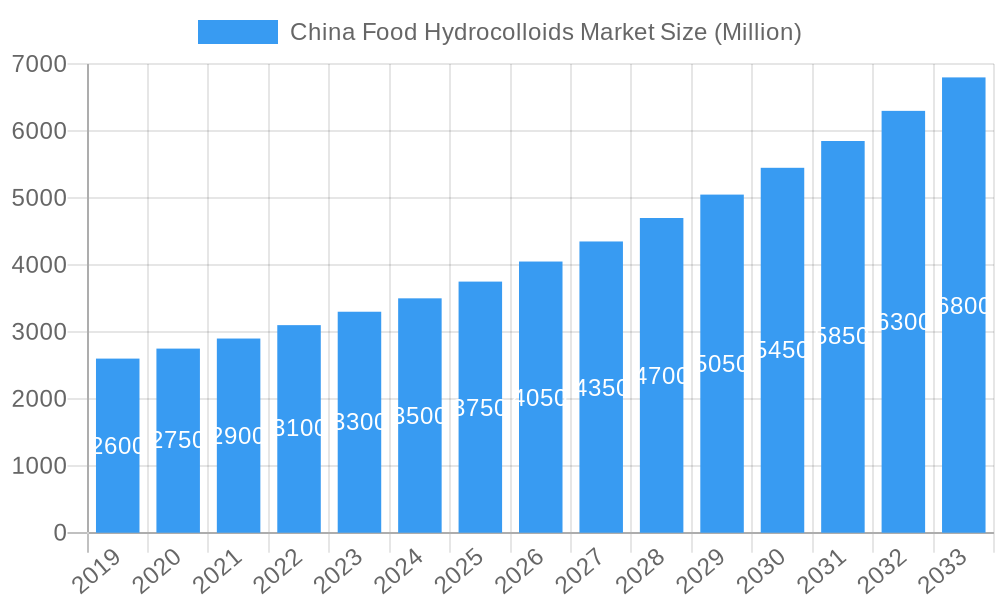

The China Food Hydrocolloids Market is projected for significant expansion, fueled by escalating demand for processed foods, a growing focus on texture and stability in food products, and ongoing innovation in food formulations. The market, valued at approximately 2.36 billion in the base year 2023, is forecasted to grow at a Compound Annual Growth Rate (CAGR) of 5.8% from 2024 to 2033, reaching an estimated 2.36 billion by 2033. Key growth drivers include the expanding middle class, evolving dietary habits, increased adoption of functional foods, and the growth of the food processing sector nationwide. Additionally, the health and wellness trend is indirectly stimulating hydrocolloid usage as manufacturers enhance the appeal of healthier options, such as low-sugar and low-fat products.

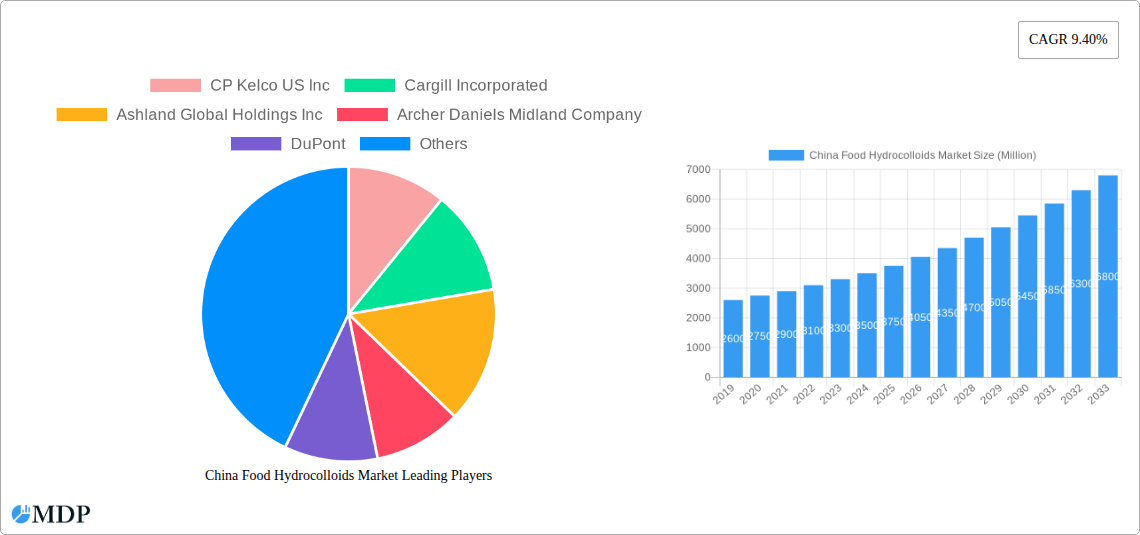

China Food Hydrocolloids Market Market Size (In Billion)

Market dynamics are also influenced by a strong trend towards natural and plant-based hydrocolloids, such as pectin and xanthan gum, aligning with consumer preferences for clean labels and sustainable sourcing. Key end-use segments, including dairy and frozen products, bakery, and beverages, will continue to be major consumers, utilizing hydrocolloids for thickening, gelling, and stabilization to improve product quality and shelf-life. Potential restraints include price volatility of raw materials and evolving regulatory environments. Nevertheless, consistent demand from an urbanizing population and the expansion of online food sales channels are expected to drive market growth. Innovations in specialized hydrocolloid applications and increased adoption by smaller food manufacturers will further contribute to market diversification.

China Food Hydrocolloids Market Company Market Share

China Food Hydrocolloids Market: A Comprehensive Analysis & Growth Outlook (2019–2033)

This in-depth report provides a meticulously researched overview of the China Food Hydrocolloids Market, offering critical insights for stakeholders navigating this dynamic sector. Covering the Study Period: 2019–2033, with a Base Year: 2025, Estimated Year: 2025, and Forecast Period: 2025–2033, this analysis delves into historical trends (Historical Period: 2019–2024) to project future trajectories. Explore key market dynamics, segment-specific growth, product innovations, leading players, and strategic opportunities within the burgeoning Chinese food industry. This report is essential for manufacturers, suppliers, distributors, investors, and regulatory bodies seeking to understand and capitalize on the China Food Hydrocolloids Market.

China Food Hydrocolloids Market Market Dynamics & Concentration

The China Food Hydrocolloids Market exhibits a moderate to high concentration, with key players like CP Kelco US Inc, Cargill Incorporated, Ashland Global Holdings Inc, Archer Daniels Midland Company, DuPont, Behn Meyer Holding A, and Koninklijke DSM NV holding significant market share. Innovation drivers are primarily focused on developing novel hydrocolloid applications, improving functionalities (e.g., texture modification, stabilization, emulsification), and catering to growing demand for natural and clean-label ingredients. Regulatory frameworks, overseen by bodies like the National Medical Products Administration (NMPA) and the Standardization Administration of China (SAC), are continuously evolving to ensure food safety and quality standards, impacting product development and market entry strategies. Product substitutes, while present, are often limited in their ability to replicate the specific functionalities and cost-effectiveness of hydrocolloids in certain applications. End-user trends reveal a strong preference for processed foods, convenience items, and healthier alternatives, all of which rely heavily on the functional properties of hydrocolloids. Merger and acquisition (M&A) activities, though not extensively documented for specific deal counts in this segment, are anticipated to play a crucial role in market consolidation and expansion as companies seek to broaden their product portfolios and geographical reach. The market share distribution among the leading players is estimated to be dynamic, with continuous efforts to gain competitive advantage through product differentiation and strategic alliances.

China Food Hydrocolloids Market Industry Trends & Analysis

The China Food Hydrocolloids Market is poised for robust growth, driven by a confluence of economic, social, and technological factors. The burgeoning Chinese population, coupled with increasing disposable incomes, fuels a sustained demand for a wider array of processed and convenience foods, thereby escalating the consumption of food hydrocolloids. This demographic shift is a primary market growth driver. Technological disruptions are continuously shaping the industry, with advancements in extraction, purification, and modification techniques leading to the development of higher-performing and more specialized hydrocolloids. These innovations are crucial for meeting the evolving demands of food manufacturers seeking to enhance product texture, stability, and shelf-life. Consumer preferences are increasingly leaning towards healthier, natural, and functional food products. This trend is boosting the demand for plant-based hydrocolloids like pectin and gums derived from natural sources, while simultaneously pushing for cleaner ingredient labels. The competitive dynamics within the China Food Hydrocolloids Market are characterized by intense rivalry among global and domestic players, who are vying for market share through product innovation, strategic partnerships, and aggressive marketing strategies. The market penetration of various hydrocolloids is steadily increasing across diverse food applications. The Compound Annual Growth Rate (CAGR) for the China Food Hydrocolloids Market is projected to be in the range of 6.5% to 8.0% over the forecast period, indicating a healthy expansion trajectory. Key industry trends include the rising adoption of hydrocolloids in plant-based meat alternatives, the development of allergen-free formulations, and the increasing use of hydrocolloids for microencapsulation of active ingredients in functional foods. The shift towards sustainable sourcing and production methods is also gaining traction, influencing procurement decisions and R&D efforts.

Leading Markets & Segments in China Food Hydrocolloids Market

The China Food Hydrocolloids Market is dominated by several key segments, with significant growth potential across all applications.

Type Segment Dominance:

- Gelatin Gum: Holds a substantial market share due to its wide applicability in confectionery, dairy, and meat products, owing to its gelling, thickening, and stabilizing properties. Economic policies supporting the growth of the confectionery and dairy sectors in China directly bolster demand for gelatin gum.

- Pectin: Experiencing significant growth driven by the increasing demand for natural ingredients and its widespread use in jams, jellies, and beverages. Consumer preference for low-sugar and fruit-based products further fuels pectin consumption.

- Xanthan Gum: A leading hydrocolloid, its dominance is attributed to its excellent thickening and stabilizing capabilities across a broad pH range, making it indispensable in dressings, sauces, and bakery products. Technological advancements in fermentation processes have improved its cost-effectiveness.

- Guar Gum: Widely used in the food industry for its thickening and binding properties, particularly in dairy products, bakery, and processed foods. Its cost-effectiveness and natural origin make it a popular choice.

- Carrageenan: Primarily utilized in dairy and frozen products for its gelling, thickening, and emulsifying properties. The expanding market for dairy alternatives and frozen desserts contributes to its demand.

- Other Types: This category, encompassing hydrocolloids like alginates and cellulose derivatives, is also showing steady growth due to specialized applications and ongoing R&D efforts.

Distribution Channel Segment Dominance:

- Dairy and Frozen Products: Represents the largest distribution channel, with hydrocolloids playing a crucial role in enhancing the texture, stability, and mouthfeel of products like ice cream, yogurt, and processed cheese. The expanding middle class and changing dietary habits in China are key drivers.

- Bakery: A significant segment where hydrocolloids are used to improve dough handling, crumb structure, and shelf-life of baked goods. The growing demand for convenient and ready-to-eat bakery items propels this segment.

- Beverages: Hydrocolloids are essential for viscosity control, suspension of pulp, and mouthfeel in various beverages, including juices, carbonated drinks, and functional beverages. The expanding beverage market in China is a major contributor.

- Confectionery: A historically strong segment where hydrocolloids are used for gelling, texture modification, and stabilization in candies, chocolates, and other sweet treats.

- Meat and Seafood Products: Hydrocolloids are employed for water binding, texture improvement, and emulsification in processed meats and seafood. The increasing consumption of processed meat products is a key driver.

- Oils and Fats: Used as emulsifiers and stabilizers in various food products containing oils and fats.

- Other Applications: This encompasses a range of niche uses, including sauces, dressings, and pet food, which are collectively contributing to market growth.

China Food Hydrocolloids Market Product Developments

Product innovations in the China Food Hydrocolloids Market are focused on enhancing functionality, sustainability, and consumer appeal. Companies are developing specialized blends of hydrocolloids to achieve precise textural attributes and improved stability in complex food matrices. There's a growing emphasis on clean-label, plant-derived hydrocolloids that meet consumer demand for natural ingredients. Key advancements include the development of hydrocolloids with improved thermal stability, shear resistance, and controlled gelling kinetics. These innovations offer competitive advantages by enabling manufacturers to create novel food products and improve the performance of existing ones, catering to evolving market needs.

Key Drivers of China Food Hydrocolloids Market Growth

Several interconnected factors are propelling the growth of the China Food Hydrocolloids Market:

- Rising Demand for Processed and Convenience Foods: The increasing urbanization and busy lifestyles in China are leading to a higher consumption of convenient, ready-to-eat food products that rely on hydrocolloids for texture, stability, and shelf-life.

- Growing Health and Wellness Trends: Consumer demand for functional foods, plant-based alternatives, and products with cleaner ingredient labels is driving the adoption of natural and specialized hydrocolloids.

- Technological Advancements: Innovations in production technologies and product development are leading to the creation of more versatile and high-performance hydrocolloids, expanding their application spectrum.

- Expanding Food & Beverage Industry: The overall growth of China's food and beverage sector, fueled by a large population and rising disposable incomes, directly translates to increased demand for food ingredients like hydrocolloids.

Challenges in the China Food Hydrocolloids Market Market

Despite its promising outlook, the China Food Hydrocolloids Market faces several challenges:

- Stringent Regulatory Landscape: Evolving food safety regulations and compliance requirements can pose hurdles for new market entrants and require continuous adaptation from existing players.

- Price Volatility of Raw Materials: Fluctuations in the prices of natural raw materials used for hydrocolloid production can impact manufacturing costs and profit margins.

- Competition and Price Pressures: The market is highly competitive, with intense price pressures from both domestic and international players, requiring companies to focus on cost optimization and value-added offerings.

- Supply Chain Disruptions: Global and regional supply chain vulnerabilities can affect the availability and cost of raw materials and finished products, posing risks to consistent market supply.

Emerging Opportunities in China Food Hydrocolloids Market

The China Food Hydrocolloids Market presents several compelling opportunities for growth and innovation:

- Growth in Plant-Based and Alternative Proteins: The booming market for plant-based meats and dairy alternatives offers significant opportunities for hydrocolloids that can mimic animal-derived textures and functionalities.

- Development of Functional and Fortified Foods: Hydrocolloids are crucial for the encapsulation and delivery of vitamins, minerals, and other bioactive compounds in fortified foods, catering to the growing health-conscious consumer base.

- Expansion into Emerging Food Categories: Opportunities exist in novel food categories like ready-to-drink smoothies, specialized sauces, and premium dairy desserts, where specific textural and stabilizing properties are highly valued.

- Sustainable Sourcing and Production: Companies focusing on sustainable sourcing of raw materials and environmentally friendly production processes can gain a competitive edge and appeal to increasingly eco-conscious consumers.

Leading Players in the China Food Hydrocolloids Market Sector

- CP Kelco US Inc

- Cargill Incorporated

- Ashland Global Holdings Inc

- Archer Daniels Midland Company

- DuPont

- Behn Meyer Holding A

- Koninklijke DSM NV

Key Milestones in China Food Hydrocolloids Market Industry

- 2019: Increased focus on natural and clean-label ingredients, driving innovation in plant-based hydrocolloids.

- 2020: Heightened demand for functional foods and beverages, boosting the application of hydrocolloids for enhanced nutrition and health benefits.

- 2021: Growing influence of e-commerce on food distribution channels, necessitating efficient supply chain solutions for hydrocolloids.

- 2022: Intensified research and development in novel hydrocolloid applications for plant-based meat and dairy alternatives.

- 2023: Significant advancements in biotechnological production methods for select hydrocolloids, aiming for cost reduction and improved sustainability.

- 2024: The market witnessed a growing emphasis on regulatory compliance and food safety standards, influencing product formulations and market entry strategies.

Strategic Outlook for China Food Hydrocolloids Market Market

The China Food Hydrocolloids Market is set for continued expansion, driven by persistent consumer demand for processed and convenient foods, coupled with the rising trend towards healthier and plant-based alternatives. Strategic focus on innovation in high-demand segments like dairy, bakery, and beverages, along with targeted R&D in functional hydrocolloids, will be crucial. Companies that can effectively navigate the evolving regulatory landscape, ensure sustainable sourcing, and leverage emerging opportunities in plant-based foods and functional ingredients are well-positioned for long-term success and market leadership.

China Food Hydrocolloids Market Segmentation

-

1. Type

- 1.1. Gelatin Gum

- 1.2. Pectin

- 1.3. Xanthan Gum

- 1.4. Guar Gum

- 1.5. Carrageenan

- 1.6. Other Types

-

2. Distribution Channel

- 2.1. Dairy and Frozen Products

- 2.2. Bakery

- 2.3. Beverages

- 2.4. Confectionery

- 2.5. Meat and Seafood Products

- 2.6. Oils and Fats

- 2.7. Other Applications

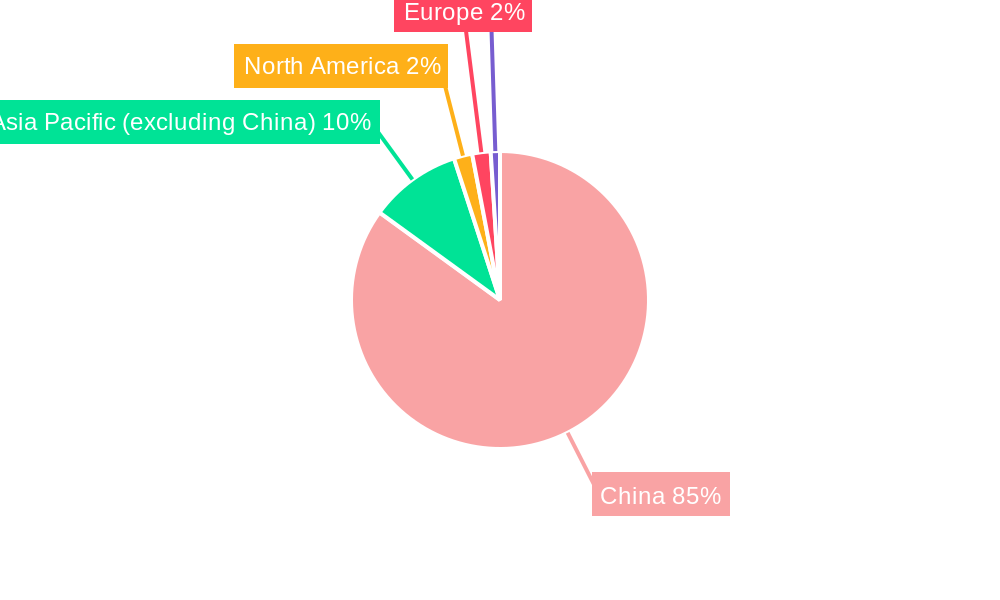

China Food Hydrocolloids Market Segmentation By Geography

- 1. China

China Food Hydrocolloids Market Regional Market Share

Geographic Coverage of China Food Hydrocolloids Market

China Food Hydrocolloids Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Low-Fat and Low-Calorie Food; Increasing Product Innovation

- 3.3. Market Restrains

- 3.3.1. ; Threat of New Entrants; Bargaining Power of Buyers/Consumers; Bargaining Power of Suppliers; Threat of Substitute Products; Degree Of Competition

- 3.4. Market Trends

- 3.4.1. Growing Consumption of Plant-based Food

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Food Hydrocolloids Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Gelatin Gum

- 5.1.2. Pectin

- 5.1.3. Xanthan Gum

- 5.1.4. Guar Gum

- 5.1.5. Carrageenan

- 5.1.6. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Dairy and Frozen Products

- 5.2.2. Bakery

- 5.2.3. Beverages

- 5.2.4. Confectionery

- 5.2.5. Meat and Seafood Products

- 5.2.6. Oils and Fats

- 5.2.7. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 CP Kelco US Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Cargill Incorporated

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Ashland Global Holdings Inc

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Archer Daniels Midland Company

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 DuPont

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Behn Meyer Holding A

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Koninklijke DSM NV

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.1 CP Kelco US Inc

List of Figures

- Figure 1: China Food Hydrocolloids Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Food Hydrocolloids Market Share (%) by Company 2025

List of Tables

- Table 1: China Food Hydrocolloids Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: China Food Hydrocolloids Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: China Food Hydrocolloids Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: China Food Hydrocolloids Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: China Food Hydrocolloids Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: China Food Hydrocolloids Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Food Hydrocolloids Market?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the China Food Hydrocolloids Market?

Key companies in the market include CP Kelco US Inc, Cargill Incorporated, Ashland Global Holdings Inc, Archer Daniels Midland Company, DuPont, Behn Meyer Holding A, Koninklijke DSM NV.

3. What are the main segments of the China Food Hydrocolloids Market?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.36 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Low-Fat and Low-Calorie Food; Increasing Product Innovation.

6. What are the notable trends driving market growth?

Growing Consumption of Plant-based Food.

7. Are there any restraints impacting market growth?

; Threat of New Entrants; Bargaining Power of Buyers/Consumers; Bargaining Power of Suppliers; Threat of Substitute Products; Degree Of Competition.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Food Hydrocolloids Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Food Hydrocolloids Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Food Hydrocolloids Market?

To stay informed about further developments, trends, and reports in the China Food Hydrocolloids Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence