Key Insights

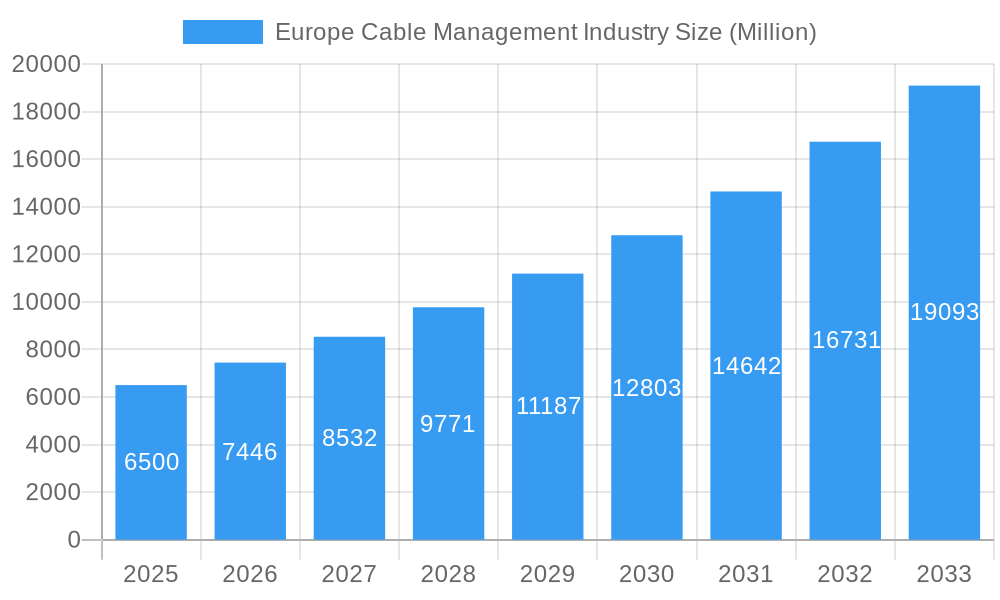

The Europe Cable Management Market is projected for significant expansion, expected to reach USD 6.59 billion by 2025, driven by a robust CAGR of 6.48% from 2025 to 2033. Key growth catalysts include escalating investments in digital infrastructure and the increasing demand for efficient data center solutions across the continent. The adoption of smart building technologies and the continuous evolution of the IT and Telecommunication sectors are major contributors, necessitating sophisticated cable management for operational reliability and safety. Furthermore, the energy transition, expansion of renewable energy projects, and ongoing retrofitting and new construction in industrial and commercial sectors significantly boost sustained demand for these essential components. The emphasis on enhanced safety standards and the need for organized, easily maintainable electrical and data networks across all end-user industries will continue to propel market advancements.

Europe Cable Management Industry Market Size (In Billion)

Market segmentation highlights the dominance of Cable Trays and Cable Raceways, driven by their widespread application in new installations and upgrades within Construction, Energy, and Manufacturing sectors. The increasing complexity of IT networks also fuels demand for specialized solutions like Cable Conduits and Junction/Distribution Boxes. Non-metallic materials, especially PVC, are gaining traction due to cost-effectiveness, durability, and ease of installation in residential and commercial settings. Metallic solutions remain crucial for industrial and high-demand environments requiring robustness and fire resistance. Leading players such as Schneider Electric SE, Eaton Corporation PLC, and Thomas & Betts Corporation (ABB Ltd) are driving innovation and serving the evolving European market through diverse product portfolios and strategic regional expansions in the United Kingdom, Germany, and France.

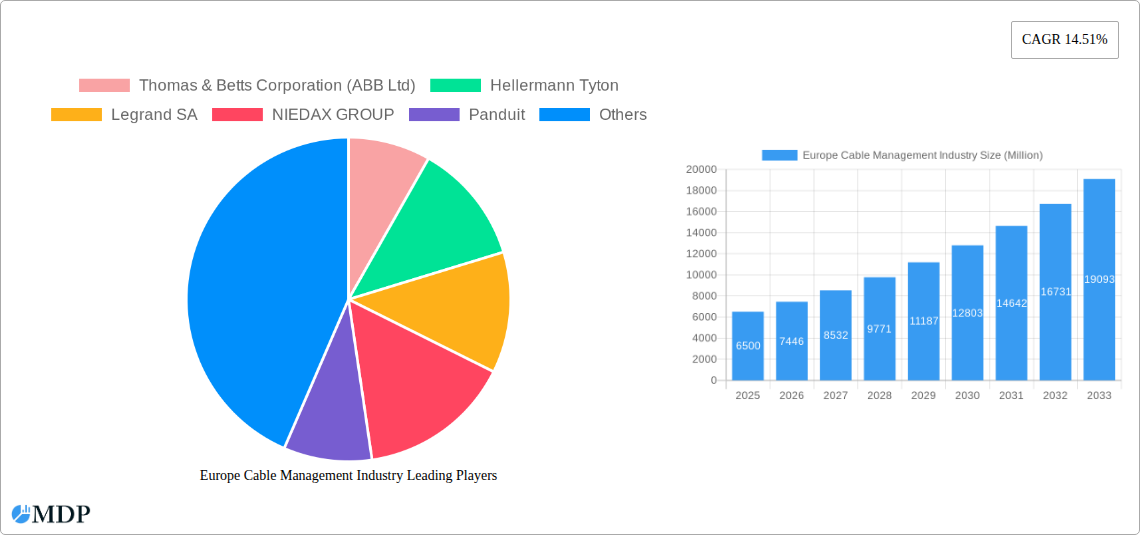

Europe Cable Management Industry Company Market Share

This comprehensive report offers definitive analysis of the Europe Cable Management Market, providing critical insights into market dynamics, growth trajectories, and competitive landscapes. Covering the forecast period from 2019 to 2033, with a base year of 2025, this report is essential for stakeholders aiming to understand the present state and future potential of this vital sector. We delve into product types including Cable Trays, Cable Raceways, Cable Conduits, Connectors and Glands, Cable Carriers, Cable Lugs, and Junction/Distribution Boxes. Key end-user industries analyzed are IT and Telecommunication, Construction, Energy and Utility, Manufacturing, and Commercial applications. Material insights will explore both Metallic and Non-metallic options such as PVC, PP, and PE.

Europe Cable Management Industry Market Dynamics & Concentration

The Europe Cable Management Industry exhibits a moderate to high concentration, with a few key players holding significant market share. Innovation remains a critical driver, fueled by the escalating demand for efficient and safe wire and cable routing solutions across various sectors. Regulatory frameworks, particularly those concerning electrical safety and environmental standards, play a crucial role in shaping product development and market entry. While product substitutes exist, particularly for lower-end applications, the specialized nature of advanced cable management systems limits their widespread adoption. End-user trends are increasingly emphasizing smart, integrated, and sustainable solutions, pushing manufacturers towards the adoption of advanced materials and design principles. Mergers and acquisitions (M&A) activities are notable, as larger companies seek to expand their product portfolios and geographic reach. For instance, recent M&A deal counts indicate a strategic consolidation phase. Key players like ABB Ltd, Hellermann Tyton, Legrand SA, and Schneider Electric SE are actively involved in shaping the market through strategic acquisitions and organic growth initiatives. The market share distribution among the top five players is estimated to be around 65-70%, underscoring the influence of these dominant entities.

Europe Cable Management Industry Industry Trends & Analysis

The Europe Cable Management Industry is experiencing robust growth, driven by several interconnected trends. The insatiable demand from the IT and Telecommunication sector, fueled by 5G rollout and data center expansion, is a primary growth engine. Similarly, the booming Construction industry, particularly in urban infrastructure development and residential building, necessitates extensive cable management solutions. Furthermore, the global push towards renewable energy sources is significantly impacting the Energy and Utility sector, requiring sophisticated and durable cable management for solar farms, wind turbines, and grid infrastructure. Technological disruptions are at the forefront, with the integration of smart features, enhanced fire safety, and improved electromagnetic compatibility becoming key differentiators. Consumer preferences are leaning towards solutions that offer ease of installation, flexibility, and aesthetic appeal, especially in commercial and residential applications. The competitive dynamics are characterized by intense product innovation, strategic partnerships, and a focus on cost-effectiveness. The compound annual growth rate (CAGR) for the Europe Cable Management Industry is projected to be in the range of 5.5% to 6.5% over the forecast period. Market penetration is deepening, with an increasing adoption of specialized cable management systems beyond basic routing, extending to data security and operational efficiency. The manufacturing sector's drive for automation and Industry 4.0 adoption also contributes to the demand for organized and protected cabling.

Leading Markets & Segments in Europe Cable Management Industry

The Europe Cable Management Industry is characterized by dominant regions and segments that are shaping its overall trajectory.

Dominant Regions & Countries:

- Germany stands out as a leading market due to its strong industrial base, significant investments in infrastructure, and a robust manufacturing sector.

- The United Kingdom follows closely, driven by its thriving construction industry and rapid advancements in the IT and telecommunication sectors.

- France also represents a significant market, particularly with its focus on renewable energy projects and extensive infrastructure development.

- Other notable markets include Italy, the Netherlands, and the Nordic countries, each contributing to the overall growth and diversification of the industry.

Dominant Product Types:

- Cable Trays and Cable Raceways collectively hold a substantial market share, essential for organizing and supporting cables in a multitude of applications. Their widespread use in construction and industrial settings makes them a cornerstone of the industry.

- Connectors and Glands are also critical, ensuring secure and protected connections, particularly in harsh environments and specialized applications within the Energy & Utility and Manufacturing sectors.

- Cable Conduits are vital for protecting cables from damage and ensuring electrical safety, especially in exposed or demanding environments.

Dominant End-User Industries:

- The Construction industry remains a primary driver, with continuous infrastructure projects and building expansions demanding extensive cable management. Key drivers include urbanization, government spending on infrastructure, and private sector development.

- The IT and Telecommunication sector's growth, fueled by digital transformation initiatives and the expansion of data centers and 5G networks, is a significant contributor.

- The Energy and Utility sector, particularly with the ongoing transition to renewable energy, requires robust and reliable cable management for power distribution and grid connectivity.

Dominant Applications:

- Industrial applications dominate due to the complex cabling needs of manufacturing plants, power generation facilities, and large-scale infrastructure projects.

- Commercial applications are also substantial, driven by the need for organized and safe cabling in office buildings, retail spaces, and public facilities.

Dominant Materials:

- Metallic materials, such as steel and aluminum, are favored in industrial and outdoor applications due to their strength, durability, and fire resistance.

- Non-metallic materials, including PVC, PP, and PE, are widely used in residential, commercial, and specific industrial settings due to their cost-effectiveness, ease of installation, and resistance to corrosion.

Europe Cable Management Industry Product Developments

Recent product innovations in the Europe Cable Management Industry are focused on enhancing safety, efficiency, and sustainability. Developments like HellermannTyton's Hela DoubleGuardSruglit Conduit, a two-piece corrugated protection solution, exemplify the trend towards easier installation and improved cable shielding. Nexans' award for providing medium voltage power distribution services and cables, including EDRMAX cables for renewable energy connections, highlights the industry's role in supporting sustainable electrification and grid modernization. These innovations aim to address evolving industry needs for robust, flexible, and environmentally conscious cable management solutions, offering competitive advantages through advanced materials and integrated functionalities.

Key Drivers of Europe Cable Management Industry Growth

The Europe Cable Management Industry's growth is propelled by several interconnected factors. The burgeoning demand for robust and reliable infrastructure across Construction, Energy and Utility, and IT and Telecommunication sectors is a primary driver. Technological advancements, including the integration of smart capabilities for monitoring and diagnostics, are increasing the adoption of advanced cable management solutions. Government initiatives promoting renewable energy and digital infrastructure further stimulate market expansion. Economic recovery and increasing industrial output in key European nations also contribute significantly. The focus on workplace safety and stringent regulatory compliance, particularly concerning fire safety and electrical integrity, necessitates the use of high-quality cable management systems, acting as a constant growth accelerator.

Challenges in the Europe Cable Management Industry Market

Despite robust growth, the Europe Cable Management Industry faces several challenges. Stringent and evolving regulatory landscapes across different European nations can create compliance complexities and increase product development costs. Fluctuations in raw material prices, particularly for metals and plastics, can impact profit margins. Intense competition from both established players and new entrants leads to pricing pressures, especially in commoditized segments. Furthermore, supply chain disruptions, as seen in recent global events, can affect the availability and timely delivery of essential components and finished goods. The need for specialized training for installers of advanced systems can also present a barrier to adoption in some markets.

Emerging Opportunities in Europe Cable Management Industry

Emerging opportunities within the Europe Cable Management Industry lie in the growing demand for smart and connected infrastructure. The expansion of data centers, the rollout of 5G networks, and the increasing adoption of Industry 4.0 technologies are creating a need for high-performance, intelligent cable management solutions. The continuous growth in renewable energy projects, requiring specialized and resilient cable management systems for solar and wind farms, presents a significant opportunity. Furthermore, the focus on sustainability and circular economy principles is driving innovation in eco-friendly materials and recyclable cable management products. Strategic partnerships between cable management manufacturers and infrastructure developers, as well as technology providers, will be crucial for tapping into these nascent markets.

Leading Players in the Europe Cable Management Industry Sector

- Thomas & Betts Corporation (ABB Ltd)

- Hellermann Tyton

- Legrand SA

- NIEDAX GROUP

- Panduit

- Vantrunk International

- Marco Cable Management

- TE Connectivity

- Schneider Electric SE

- Eaton Corporation PLC

- Leviton Manufacturing UK Limited

- Hubbell

Key Milestones in Europe Cable Management Industry Industry

- August 2022 - HellermannTyton announced the launch of Hela DoubleGuardSruglit Conduit. The two-piece solution is composed of one rigid tube that attaches to the other and wraps itself in a bundle of cables or wires. This means that, in addition to the wires which are already connected at one end, flexible corrugated protection can be added, enhancing cable protection and ease of installation.

- May 2022 - Nexans was awarded a contract by Enedis for the next 4 years to provide medium voltage power distribution services and cables worth USD 100 million. This agreement strengthens Nexans' position as a long-term partner of Enedis in France and makes it an important player with regard to sustainable electrification. This contract includes an additional quantity of EDRMAX cables, mainly used for connecting inland wind and solar farms to the network, in line with the continued development of renewable energies in France, underscoring the industry's role in supporting the energy transition.

Strategic Outlook for Europe Cable Management Industry Market

The strategic outlook for the Europe Cable Management Industry remains highly positive, driven by sustained investment in infrastructure, digital transformation, and the transition to sustainable energy. Key growth accelerators include the increasing complexity of electrical and data networks, demanding more sophisticated and integrated cable management solutions. The industry will see a continued emphasis on smart technologies for enhanced monitoring and predictive maintenance, alongside a growing demand for environmentally friendly and recyclable products. Companies that focus on innovation, strategic partnerships, and expanding their offerings to meet the evolving needs of sectors like renewable energy and advanced manufacturing will be well-positioned for long-term success. The market is expected to witness further consolidation and a drive towards specialization, creating opportunities for both large-scale players and niche solution providers.

Europe Cable Management Industry Segmentation

-

1. Product Type

- 1.1. Cable Trays

- 1.2. Cable Raceways

- 1.3. Cable Conduits

- 1.4. Connectors and Glands

- 1.5. Cable Carriers

- 1.6. Cable Lugs

- 1.7. Junction/Distribution Boxes

- 1.8. Other Pr

-

2. End-User Industry

- 2.1. IT and Telecommunication

- 2.2. Construction

- 2.3. Energy and Utility

- 2.4. Manufacturing

- 2.5. Commercial

- 2.6. Other End-User Industries

-

3. Application

- 3.1. Residential

- 3.2. Commercial

- 3.3. Industrial

-

4. Material

- 4.1. Metallic

-

4.2. Non-metallic

- 4.2.1. PVC

- 4.2.2. PP

- 4.2.3. PE

- 4.2.4. Other Materials

Europe Cable Management Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

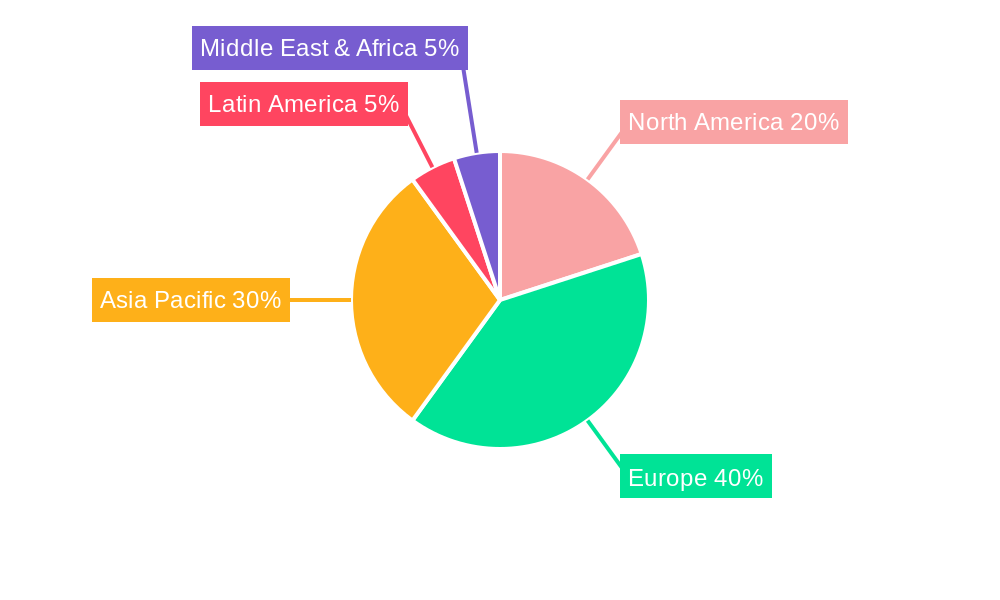

Europe Cable Management Industry Regional Market Share

Geographic Coverage of Europe Cable Management Industry

Europe Cable Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.48% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Cable Trays

- 5.1.2. Cable Raceways

- 5.1.3. Cable Conduits

- 5.1.4. Connectors and Glands

- 5.1.5. Cable Carriers

- 5.1.6. Cable Lugs

- 5.1.7. Junction/Distribution Boxes

- 5.1.8. Other Pr

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. IT and Telecommunication

- 5.2.2. Construction

- 5.2.3. Energy and Utility

- 5.2.4. Manufacturing

- 5.2.5. Commercial

- 5.2.6. Other End-User Industries

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Residential

- 5.3.2. Commercial

- 5.3.3. Industrial

- 5.4. Market Analysis, Insights and Forecast - by Material

- 5.4.1. Metallic

- 5.4.2. Non-metallic

- 5.4.2.1. PVC

- 5.4.2.2. PP

- 5.4.2.3. PE

- 5.4.2.4. Other Materials

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Europe Cable Management Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Cable Trays

- 6.1.2. Cable Raceways

- 6.1.3. Cable Conduits

- 6.1.4. Connectors and Glands

- 6.1.5. Cable Carriers

- 6.1.6. Cable Lugs

- 6.1.7. Junction/Distribution Boxes

- 6.1.8. Other Pr

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. IT and Telecommunication

- 6.2.2. Construction

- 6.2.3. Energy and Utility

- 6.2.4. Manufacturing

- 6.2.5. Commercial

- 6.2.6. Other End-User Industries

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Residential

- 6.3.2. Commercial

- 6.3.3. Industrial

- 6.4. Market Analysis, Insights and Forecast - by Material

- 6.4.1. Metallic

- 6.4.2. Non-metallic

- 6.4.2.1. PVC

- 6.4.2.2. PP

- 6.4.2.3. PE

- 6.4.2.4. Other Materials

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Thomas & Betts Corporation (ABB Ltd)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Hellermann Tyton

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Legrand SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 NIEDAX GROUP

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Panduit

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Vantrunk International

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Marco Cable Management

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 TE Connectivity

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Schneider Electric SE

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Eaton Corporation PLC

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Leviton Manufacturing UK Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Hubbell*List Not Exhaustive

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Thomas & Betts Corporation (ABB Ltd)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Cable Management Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Cable Management Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Cable Management Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Europe Cable Management Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 3: Europe Cable Management Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Europe Cable Management Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 5: Europe Cable Management Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Europe Cable Management Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: Europe Cable Management Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 8: Europe Cable Management Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Europe Cable Management Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 10: Europe Cable Management Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United Kingdom Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Germany Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: France Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Italy Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Spain Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Netherlands Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Belgium Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Sweden Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Norway Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Poland Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Denmark Europe Cable Management Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Cable Management Industry?

The projected CAGR is approximately 6.48%.

2. Which companies are prominent players in the Europe Cable Management Industry?

Key companies in the market include Thomas & Betts Corporation (ABB Ltd), Hellermann Tyton, Legrand SA, NIEDAX GROUP, Panduit, Vantrunk International, Marco Cable Management, TE Connectivity, Schneider Electric SE, Eaton Corporation PLC, Leviton Manufacturing UK Limited, Hubbell*List Not Exhaustive.

3. What are the main segments of the Europe Cable Management Industry?

The market segments include Product Type, End-User Industry, Application, Material.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.59 billion as of 2022.

5. What are some drivers contributing to market growth?

Innovation and Development in the Cable Management Market; Upgrade and Renewal of Existing Networks in the Developed Economies.

6. What are the notable trends driving market growth?

IT and Telecom Industry to drive the market.

7. Are there any restraints impacting market growth?

Fluctuating Market Demands and Customization Issues.

8. Can you provide examples of recent developments in the market?

August 2022 - HellermannTytonh has announced the launch of Hela DoubleGuardSruglit Conduit. The twopiece solution is composed of one rigid tube that attaches to the other and wraps itself in a bundle of cables or wires. This means that, in addition to the wires which are already connected at one end, flexible corrugated protection can be added.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Cable Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Cable Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Cable Management Industry?

To stay informed about further developments, trends, and reports in the Europe Cable Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence