Key Insights

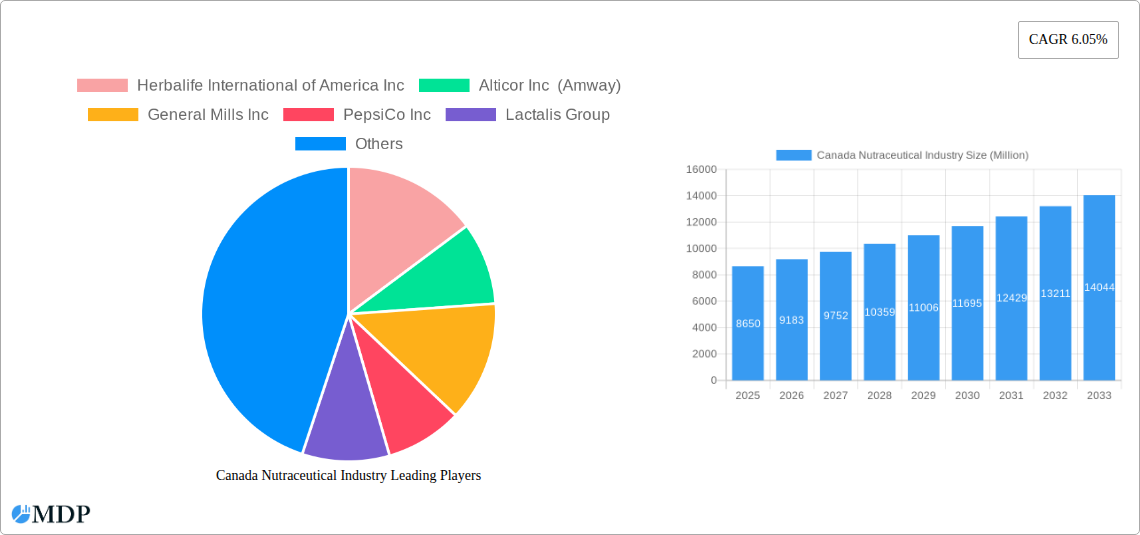

The Canadian nutraceutical market, valued at $8.65 billion in 2025, is projected to experience robust growth, exhibiting a compound annual growth rate (CAGR) of 6.05% from 2025 to 2033. This expansion is fueled by several key drivers. Increasing health consciousness among Canadians, coupled with rising prevalence of chronic diseases like diabetes and cardiovascular issues, is driving demand for preventative healthcare solutions offered by nutraceuticals. The growing popularity of functional foods and beverages, encompassing products fortified with vitamins, minerals, and other beneficial ingredients, further contributes to market growth. E-commerce penetration is also significantly impacting the sector, providing convenient access to a wider range of products and fostering market expansion. While the market faces challenges such as stringent regulatory requirements and concerns regarding product efficacy and safety, the overall positive trend towards proactive health management is expected to outweigh these limitations.

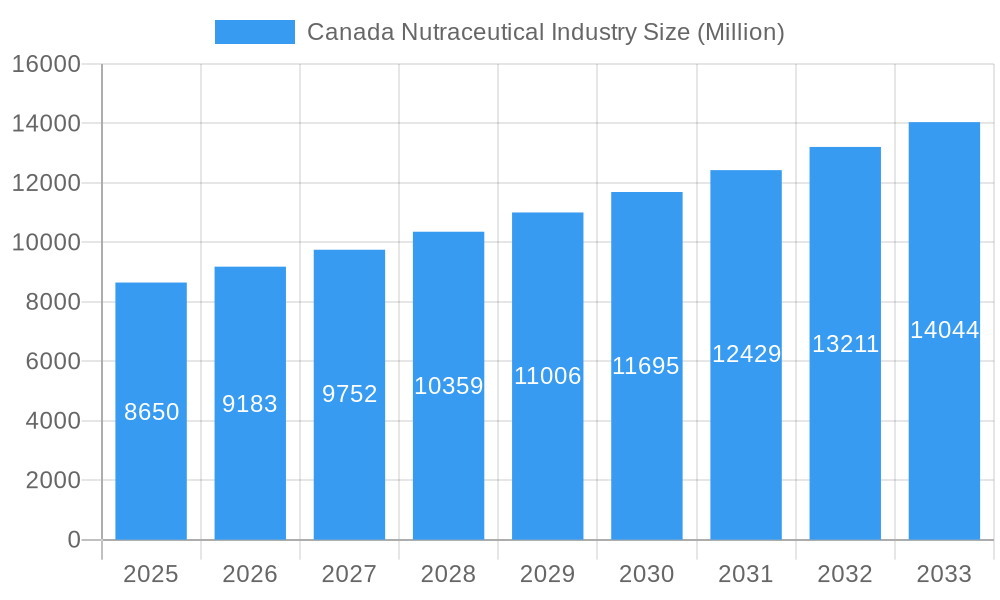

Canada Nutraceutical Industry Market Size (In Billion)

Segment-wise, functional foods constitute a significant portion of the market, with functional beverages (including dietary supplements) showing particularly strong growth. Distribution channels are diverse, with supermarkets/hypermarkets and online retail stores emerging as dominant players. Major players like Herbalife, Amway, General Mills, and PepsiCo hold substantial market share, but the presence of numerous smaller, specialized companies indicates a dynamic and competitive landscape. Regional variations within Canada exist, with Eastern, Western, and Central Canada exhibiting differing growth rates based on demographic factors and consumer preferences. The market's future growth trajectory is optimistic, driven by continuous innovation in product formulations, targeted marketing strategies, and the enduring consumer focus on well-being. Further expansion is expected through the development of novel delivery systems, personalized nutrition solutions, and an increased emphasis on scientific evidence supporting product efficacy.

Canada Nutraceutical Industry Company Market Share

Canada Nutraceutical Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Canadian nutraceutical market, offering valuable insights for industry stakeholders, investors, and strategists. With a focus on market dynamics, trends, leading players, and future opportunities, this report covers the period 2019-2033, utilizing data from the base year 2025 and projecting until 2033. The report leverages data to provide actionable intelligence for informed decision-making. The Canadian nutraceutical market, valued at xx Million in 2025, is poised for significant growth, driven by factors detailed within.

Canada Nutraceutical Industry Market Dynamics & Concentration

The Canadian nutraceutical market is characterized by a dynamic and evolving landscape, balancing the influence of established global leaders with the agility of specialized domestic players. Market concentration is a key aspect, shaped by powerful drivers such as strong brand equity, sophisticated distribution networks, and impactful marketing campaigns. Multinational giants like Nestlé S.A. and General Mills Inc. continue to leverage their extensive global reach and deeply ingrained brands to secure significant market positions. However, the market is far from monolithic, with a vibrant ecosystem of smaller companies carving out niches through specialized products, a focus on organic and natural ingredients, and innovative approaches to health and wellness. This competitive diversity fosters innovation and responsiveness to changing consumer needs. The regulatory environment, meticulously overseen by Health Canada with its stringent guidelines on labeling and product claims, plays a crucial role in shaping both product development and marketing strategies, ensuring consumer safety and transparency. Furthermore, a heightened consumer awareness regarding preventative healthcare and overall wellness is a powerful engine, driving robust demand for functional foods and dietary supplements. The presence of alternative health practices and conventional food options presents a continuous competitive challenge, encouraging continuous improvement and differentiation within the nutraceutical sector. Mergers and acquisitions (M&A) have been a significant factor in consolidating market share, with a notable xx major deals recorded between 2019 and 2024, indicating a strategic consolidation by key industry participants.

- Market Share Snapshot: Nestlé S.A. and General Mills Inc. collectively hold a substantial market share, estimated at approximately xx%, underscoring their dominant presence.

- M&A Deal Volume (2019-2024): A total of xx significant M&A deals have been completed within this period, reflecting strategic consolidation and expansion.

- Key Innovation Drivers: The market's innovation is fueled by a trifecta of consumer demands: specialized nutritional support, highly personalized health solutions, and a strong preference for transparent, "clean-label" products.

- Regulatory Framework: Health Canada's comprehensive regulations are paramount, dictating product claims, precise labeling requirements, and robust safety standards, guiding responsible market practices.

- End-User Trends: A significant shift is observed in consumer behavior, marked by an increasing focus on preventive healthcare, a surging demand for natural and organic offerings, and a growing appetite for customized and personalized nutrition plans.

Canada Nutraceutical Industry Industry Trends & Analysis

The Canadian nutraceutical market is on a remarkable growth trajectory, projected to reach an impressive xx Million by 2033. This expansion is anticipated to occur at a Compound Annual Growth Rate (CAGR) of xx% over the forecast period of 2025-2033. This robust growth is underpinned by a confluence of powerful factors: a rapidly expanding health-conscious demographic, an increase in disposable income enabling greater discretionary spending on wellness, and the persistently rising prevalence of chronic diseases, which drives demand for preventative and supportive health solutions. Technological advancements are proving to be transformative, with innovations in product formulation, the development of advanced delivery systems for enhanced bioavailability, and the rise of personalized nutrition solutions acting as significant catalysts for market expansion. Consumer preferences are demonstrably shifting towards products that are natural, organic, and ethically sourced, creating substantial opportunities for companies aligning with these values. This trend is also influencing packaging choices, with an increasing emphasis on eco-friendly materials to meet evolving consumer expectations for sustainability. The competitive landscape remains intensely fierce, characterized by established players consistently innovating and new entrants strategically challenging the status quo. The market penetration of functional foods and dietary supplements is steadily increasing, a clear indicator of the growing acceptance and integration of nutraceuticals into the daily lives of Canadians. Projections indicate that market penetration will reach xx% by 2033, signifying a maturing and widely adopted market.

Leading Markets & Segments in Canada Nutraceutical Industry

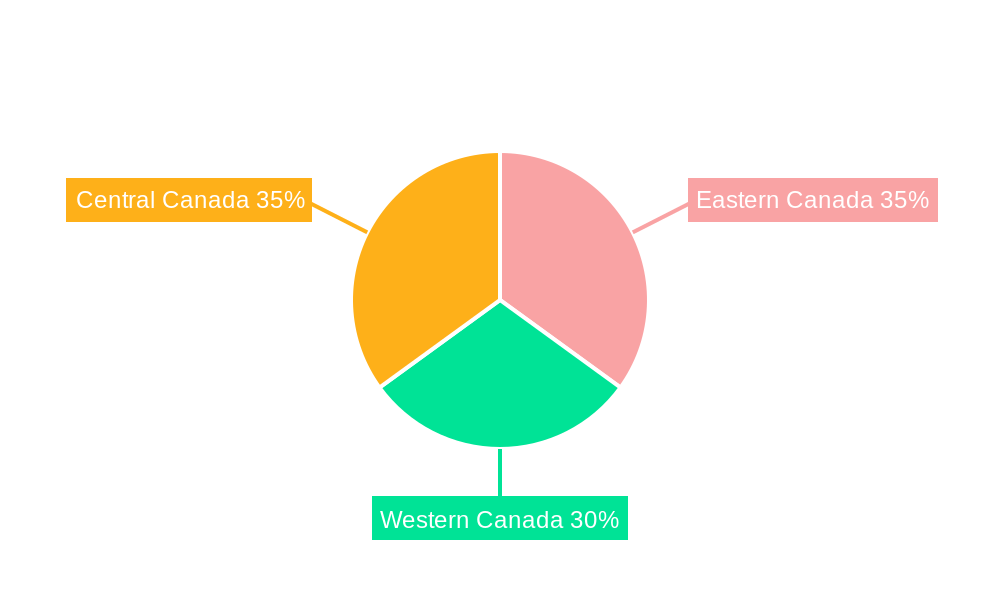

The Canadian nutraceutical market is geographically diverse, with significant demand across various regions. While specific regional dominance data is not readily available (xx), the distribution channels demonstrate a diversified landscape.

Distribution Channels:

- Supermarkets/Hypermarkets: High volume sales owing to readily accessible locations and wide customer base.

- Specialty Stores: Catering to a more health-conscious segment seeking specialized products and advice.

- Drug Stores/Pharmacies: Significant presence due to consumer trust in professional guidance and product accessibility.

- Online Retail Stores: Growing rapidly due to convenience and expanded product offerings.

- Convenience Stores: Offer limited but readily available options, particularly for impulse purchases.

Product Types:

- Functional Foods: Dominant segment driven by consumer demand for healthier food options with added benefits.

- Functional Beverages: Growing segment, with various options like protein shakes and functional drinks gaining popularity.

- Dietary Supplements: A significant portion of the market, offering targeted nutritional solutions.

Key Drivers:

- Growing awareness of the benefits of preventative healthcare

- Increasing prevalence of chronic diseases like diabetes and heart disease

- Rising disposable incomes enabling consumers to purchase premium products

- Government initiatives promoting healthy lifestyles

Canada Nutraceutical Industry Product Developments

Recent product innovations in the Canadian nutraceutical sector underscore a strong industry commitment to "clean labels," the use of natural ingredients, and the development of precisely tailored solutions for specific consumer needs. Nestlé's strategic entry with VitaBeans exemplifies the growing trend towards offering products that are vegetarian, gluten-free, and allergen-free, catering to a wider consumer base with dietary restrictions and preferences. Kellogg's organizational restructuring into specialized business units highlights a deliberate strategy to foster targeted product development across its diverse portfolio, including cereals, snacks, and plant-based food alternatives. Similarly, Lactalis' introduction of Astro Protein & Fibre Yogurt showcases a focused effort to enhance the nutritional profiles of established product categories, responding to consumer demand for more functional benefits. These strategic developments collectively demonstrate a sophisticated understanding of evolving consumer preferences and emerging health trends. The integration of cutting-edge technologies, particularly personalized nutrition algorithms, into the product development lifecycle signifies a pivotal shift towards delivering truly customized health and wellness solutions to Canadian consumers.

Key Drivers of Canada Nutraceutical Industry Growth

Several key factors drive the growth of Canada's nutraceutical industry:

- Rising health consciousness: Increased awareness of preventative healthcare and the benefits of functional foods and supplements.

- Technological advancements: Innovations in product formulation, delivery systems, and personalization.

- Favorable government policies: Regulations promoting health and wellness initiatives. Examples include targeted tax incentives for certain products or health-related advertising campaigns.

- Expanding distribution networks: Increased availability of nutraceutical products across diverse channels, leading to higher market penetration.

Challenges in the Canada Nutraceutical Industry Market

The Canadian nutraceutical market, while experiencing robust growth, is not without its significant challenges:

- Stringent Regulatory Hurdles: Navigating Health Canada's intricate and evolving regulations concerning product claims and labeling is a complex and resource-intensive process. This can disproportionately affect smaller companies with limited legal and compliance resources, acting as a barrier to entry and market expansion.

- Supply Chain Vulnerabilities: The industry remains susceptible to global events, geopolitical uncertainties, and economic fluctuations that can disrupt the availability and significantly impact the cost of essential raw materials, affecting production timelines and profit margins.

- Intense Market Competition: The Canadian nutraceutical sector is characterized by a highly competitive environment. Both established multinational corporations and agile new entrants are actively vying for market share, which often leads to increased pricing pressures and escalating marketing expenditures required to capture consumer attention.

- Consumer Skepticism and Trust: Despite growing awareness, a segment of consumers harbors skepticism regarding the authenticity and proven efficacy of nutraceutical products. Overcoming these perceptions requires sophisticated and transparent marketing strategies, robust scientific backing for claims, and a consistent focus on product quality to build and maintain consumer confidence.

Emerging Opportunities in Canada Nutraceutical Industry

Significant opportunities exist for growth within the Canadian nutraceutical industry. These include:

- Strategic partnerships: Collaborations between nutraceutical companies and healthcare providers to offer integrated solutions.

- Personalized nutrition: Developing customized products and services based on individual needs and genetic profiles using advanced technologies.

- Market expansion into new regions: Targeting underserved populations or geographical areas with increased marketing and distribution efforts.

- Innovation in product delivery systems: Developing novel and convenient ways to consume nutraceuticals, such as functional beverages or ingestible patches.

Leading Players in the Canada Nutraceutical Industry Sector

Key Milestones in Canada Nutraceutical Industry Industry

- September 2021: Lactalis Canada introduced Astro PROTEIN & FIBRE Yogurt, expanding the market for protein- and fibre-enhanced dairy products.

- June 2022: Kellogg Company announced a split into three companies, signaling potential strategic shifts in the Canadian cereal and snack markets.

- October 2022: Nestlé and Nature's Bounty launched the VitaBeans product line, marking a significant entry into the Canadian vitamins and supplements sector with a focus on vegetarian and allergen-free options.

Strategic Outlook for Canada Nutraceutical Industry Market

The Canadian nutraceutical market presents a promising outlook. Continued growth is expected, driven by increasing health consciousness, innovative product developments, and strategic partnerships. The market's future hinges on navigating regulatory complexities, addressing supply chain vulnerabilities, and capitalizing on the burgeoning demand for personalized nutrition. Companies embracing technological advancements and adapting to evolving consumer preferences will be best positioned for success in this dynamic and expanding market. The focus on sustainable practices and ethical sourcing will also play a critical role in shaping the future of the industry.

Canada Nutraceutical Industry Segmentation

-

1. Type

-

1.1. Functional Food

- 1.1.1. Functional Cereal

- 1.1.2. Functional Bakery & Confectionary

- 1.1.3. Functional Dairy

- 1.1.4. Functional Snacks

- 1.1.5. Other Functional Foods

-

1.2. Functional Beverage

- 1.2.1. Energy Drink

- 1.2.2. Sports Drink

- 1.2.3. Fortified Juice

- 1.2.4. Dairy and Dairy Alternative Beverage

- 1.2.5. Other Functional Beverages

-

1.3. Dietary Supplement

- 1.3.1. Vitamin

- 1.3.2. Mineral

- 1.3.3. Botanical

- 1.3.4. Enzyme

- 1.3.5. Fatty Acid

- 1.3.6. Protein

- 1.3.7. Other Dietary Supplements

-

1.1. Functional Food

-

2. Distribution Channel

- 2.1. Specialty Stores

- 2.2. Supermarkets/Hypermarkets

- 2.3. Convenience Stores

- 2.4. Drug Stores/Pharmacies

- 2.5. Online Retail Stores

- 2.6. Other Distribution Channels

Canada Nutraceutical Industry Segmentation By Geography

- 1. Canada

Canada Nutraceutical Industry Regional Market Share

Geographic Coverage of Canada Nutraceutical Industry

Canada Nutraceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.05% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Functional Food

- 5.1.1.1. Functional Cereal

- 5.1.1.2. Functional Bakery & Confectionary

- 5.1.1.3. Functional Dairy

- 5.1.1.4. Functional Snacks

- 5.1.1.5. Other Functional Foods

- 5.1.2. Functional Beverage

- 5.1.2.1. Energy Drink

- 5.1.2.2. Sports Drink

- 5.1.2.3. Fortified Juice

- 5.1.2.4. Dairy and Dairy Alternative Beverage

- 5.1.2.5. Other Functional Beverages

- 5.1.3. Dietary Supplement

- 5.1.3.1. Vitamin

- 5.1.3.2. Mineral

- 5.1.3.3. Botanical

- 5.1.3.4. Enzyme

- 5.1.3.5. Fatty Acid

- 5.1.3.6. Protein

- 5.1.3.7. Other Dietary Supplements

- 5.1.1. Functional Food

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Specialty Stores

- 5.2.2. Supermarkets/Hypermarkets

- 5.2.3. Convenience Stores

- 5.2.4. Drug Stores/Pharmacies

- 5.2.5. Online Retail Stores

- 5.2.6. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Canada Nutraceutical Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Functional Food

- 6.1.1.1. Functional Cereal

- 6.1.1.2. Functional Bakery & Confectionary

- 6.1.1.3. Functional Dairy

- 6.1.1.4. Functional Snacks

- 6.1.1.5. Other Functional Foods

- 6.1.2. Functional Beverage

- 6.1.2.1. Energy Drink

- 6.1.2.2. Sports Drink

- 6.1.2.3. Fortified Juice

- 6.1.2.4. Dairy and Dairy Alternative Beverage

- 6.1.2.5. Other Functional Beverages

- 6.1.3. Dietary Supplement

- 6.1.3.1. Vitamin

- 6.1.3.2. Mineral

- 6.1.3.3. Botanical

- 6.1.3.4. Enzyme

- 6.1.3.5. Fatty Acid

- 6.1.3.6. Protein

- 6.1.3.7. Other Dietary Supplements

- 6.1.1. Functional Food

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Specialty Stores

- 6.2.2. Supermarkets/Hypermarkets

- 6.2.3. Convenience Stores

- 6.2.4. Drug Stores/Pharmacies

- 6.2.5. Online Retail Stores

- 6.2.6. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Herbalife International of America Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Alticor Inc (Amway)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 General Mills Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PepsiCo Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Lactalis Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Magnum Nutraceuticals*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Red Bull GmbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Danone S A

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Natural Factors Nutritional Products Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Kellogg Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Pfizer Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Nestlé S A

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Herbalife International of America Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Nutraceutical Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Nutraceutical Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Nutraceutical Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Canada Nutraceutical Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Canada Nutraceutical Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Canada Nutraceutical Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Canada Nutraceutical Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Canada Nutraceutical Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Nutraceutical Industry?

The projected CAGR is approximately 6.05%.

2. Which companies are prominent players in the Canada Nutraceutical Industry?

Key companies in the market include Herbalife International of America Inc, Alticor Inc (Amway), General Mills Inc, PepsiCo Inc, Lactalis Group, Magnum Nutraceuticals*List Not Exhaustive, Red Bull GmbH, Danone S A, Natural Factors Nutritional Products Ltd, Kellogg Company, Pfizer Inc, Nestlé S A.

3. What are the main segments of the Canada Nutraceutical Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Popularity of On-the-Go Snacking Options; Trend Of Clean Label and Plant-Based Bars.

6. What are the notable trends driving market growth?

Increasing Expenditure on Health and Wellness.

7. Are there any restraints impacting market growth?

Availability of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

In October 2022, with the launch of the VitaBeans product line, Nestlé and Natures Bounty entered the Canadian vitamins and supplements market. Besides being vegetarian, the beans also contain no gluten or gelatin and no artificial colors or flavors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Nutraceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Nutraceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Nutraceutical Industry?

To stay informed about further developments, trends, and reports in the Canada Nutraceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence