Key Insights

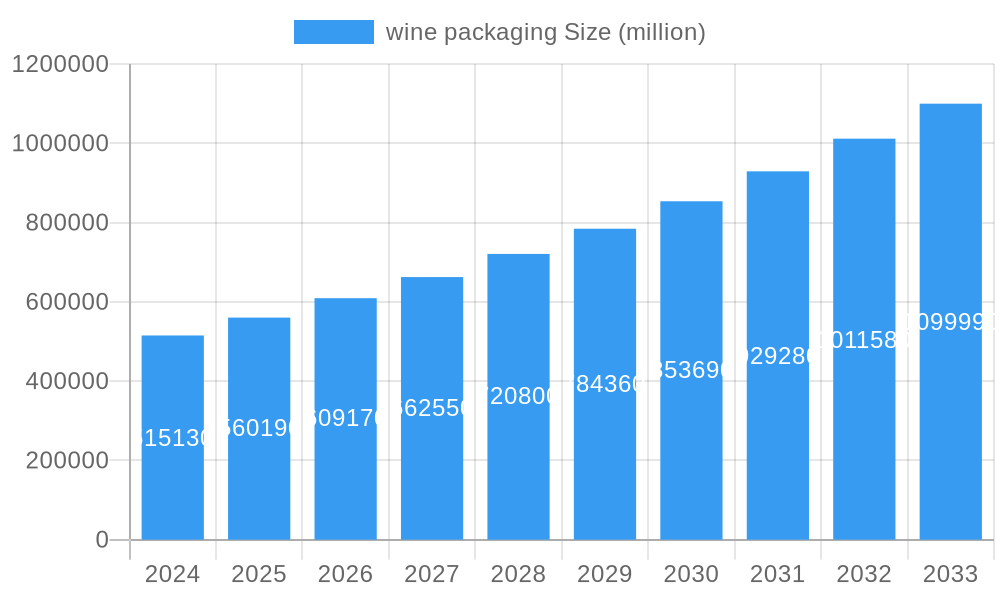

The global wine packaging market is poised for robust expansion, estimated to reach USD 515.13 billion in 2024 and projected to grow at a Compound Annual Growth Rate (CAGR) of 8.8% through 2033. This significant market size underscores the critical role of effective and appealing packaging in the wine industry's value chain. Key growth drivers fueling this expansion include the increasing global demand for wine, particularly from emerging economies, and a rising consumer preference for premium and specialty wines that necessitate distinctive packaging. Furthermore, advancements in packaging materials and technologies, offering enhanced preservation, portability, and aesthetic appeal, are also contributing to market dynamism. The industry is witnessing a substantial shift towards sustainable and eco-friendly packaging solutions, driven by growing environmental consciousness among consumers and stricter regulatory frameworks. This trend is spurring innovation in materials like recyclable glass, biodegradable plastics, and responsibly sourced wood.

wine packaging Market Size (In Billion)

The wine packaging market is segmented by application and type, reflecting diverse industry needs. In terms of application, the Wine Manufacturing Industry remains the dominant segment, driven by the sheer volume of production and the need for bulk and individual bottle packaging. However, the Retail segment is experiencing accelerated growth as brands increasingly focus on direct-to-consumer sales and in-store presentation, utilizing eye-catching and informative packaging to capture consumer attention. The "Others" category likely encompasses niche applications such as gift packaging and promotional items. By type, Glass Bottles continue to be the preferred choice for premium wines due to their inert nature and perceived quality, though their weight and fragility present challenges. Plastic Bottles are gaining traction for their lighter weight, reduced shipping costs, and shatterproof qualities, particularly for certain market segments and distribution channels. Plastic Bags are emerging for single-serve portions and convenience-oriented products. While Wood Bottles are less common, they cater to a niche market for luxury or artisanal wines. The "Others" category would likely include innovative solutions like aluminum cans and alternative closures. Key players in this competitive landscape are continuously innovating to meet evolving consumer demands and regulatory landscapes.

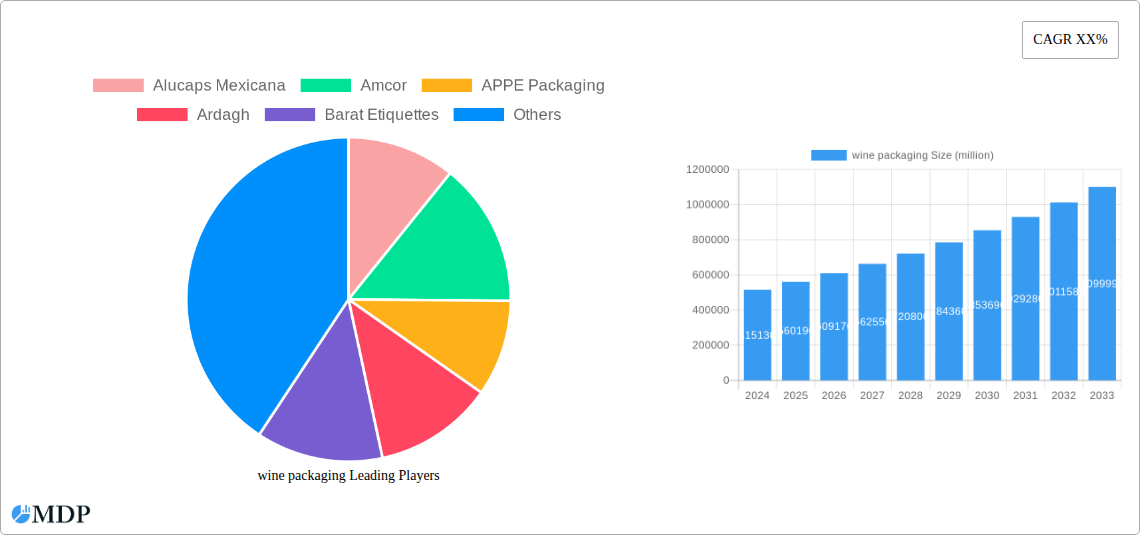

wine packaging Company Market Share

This in-depth report delivers unparalleled insights into the global wine packaging market, analyzing its evolution from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this study is an indispensable resource for industry stakeholders seeking to understand current dynamics and capitalize on future opportunities. Leveraging high-traffic keywords, this report is optimized for maximum search visibility, attracting professionals across the wine manufacturing, retail, and packaging sectors. Discover market trends, key drivers, emerging opportunities, and the strategic landscape shaping the future of wine packaging.

wine packaging Market Dynamics & Concentration

The global wine packaging market exhibits a moderate concentration, characterized by the presence of several key players alongside a multitude of smaller, regional manufacturers. The competitive landscape is influenced by innovation drivers such as the increasing demand for sustainable packaging solutions, the rise of premiumization in wine offerings, and evolving consumer preferences for convenience and aesthetic appeal. Regulatory frameworks, particularly those concerning food-grade materials, recycling initiatives, and labeling requirements, play a significant role in shaping market entry and product development strategies. Product substitutes, including alternative beverage containers and novel closure systems, continuously challenge traditional packaging formats. End-user trends indicate a growing preference for lightweight, recyclable, and visually appealing packaging that enhances brand storytelling and consumer experience. Merger and acquisition (M&A) activities, while not as intense as in some other industries, are present, with strategic consolidations aimed at expanding product portfolios, geographical reach, and technological capabilities. The market share of leading companies is dynamic, with significant players holding substantial portions while agile innovators carve out niche segments. M&A deal counts are projected to remain steady, focusing on acquiring innovative technologies and market access.

wine packaging Industry Trends & Analysis

The wine packaging industry is experiencing robust growth, driven by a confluence of factors including an expanding global wine consumption base, rising disposable incomes in emerging economies, and an increasing appreciation for wine as a lifestyle beverage. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period (2025–2033). Market penetration is deepening across all segments, with a notable surge in demand for innovative and sustainable packaging solutions. Technological disruptions are at the forefront, with advancements in materials science leading to the development of lighter, more durable, and environmentally friendly packaging options. This includes the growing adoption of recycled glass, plant-based plastics, and advanced barrier films to preserve wine quality and extend shelf life. Consumer preferences are increasingly shifting towards personalized and premium packaging experiences. This translates into a demand for custom-designed bottles, unique closures, and high-quality label printing that reflects the brand's identity and the wine's origin. The rise of e-commerce for wine sales has also necessitated packaging that is not only aesthetically pleasing but also robust enough to withstand the rigors of shipping and handling. Competitive dynamics are intensifying, with companies investing heavily in research and development to differentiate their offerings. Strategic alliances and partnerships are becoming crucial for accessing new markets and technologies. The ongoing focus on sustainability is a powerful market driver, pushing companies to adopt circular economy principles and invest in recyclable and reusable packaging materials. The premiumization trend in the wine sector further fuels demand for high-end packaging, including specialized glass bottles, elegant labels, and sophisticated closures, contributing to an overall market value estimated to reach billions by 2033. The industry is witnessing significant innovation in areas like smart packaging, which can provide authentication, track provenance, and even monitor storage conditions.

Leading Markets & Segments in wine packaging

The Wine Manufacturing Industry segment holds a dominant position within the global wine packaging market, acting as the primary consumer of packaging solutions. This dominance is fueled by consistent demand for bulk packaging, primary containment, and promotional materials directly from wineries and vineyards. Within this segment, Glass Bottles remain the undisputed leader, accounting for an estimated xx% of the total market share due to their perceived premium quality, inertness, and recyclability, which are crucial for wine preservation and consumer trust. The economic policies of major wine-producing and consuming nations, such as tax incentives for sustainable manufacturing and trade agreements, significantly influence the purchasing decisions within this segment. Infrastructure development, particularly in logistics and supply chain networks for raw materials and finished goods, further supports the dominance of this segment.

The Retail segment is the second-largest consumer, with increasing emphasis on eye-catching and functional packaging that drives impulse purchases and enhances the in-store and online shopping experience. Here, the demand for aesthetically pleasing labels, multipack options, and gift-ready packaging is high. Economic growth and consumer spending power directly correlate with the growth of this segment.

In terms of Types of packaging, Glass Bottles continue to lead due to their established reputation and widespread acceptance. However, Plastic Bottles are gaining traction, particularly for convenience-sized formats and for export markets where weight and breakage are significant concerns. The development of advanced, high-barrier plastics is mitigating concerns about wine quality. Plastic Bags, while less dominant for traditional wine sales, are finding niche applications in bulk dispensers and for certain ready-to-drink wine products. Wood Bottles, though a premium and niche offering, cater to specific artisanal and luxury wine segments, offering unique branding opportunities. The Others category, encompassing innovative materials and formats, is expected to witness the highest growth rate as the industry explores novel solutions.

wine packaging Product Developments

Recent product developments in wine packaging are heavily influenced by sustainability and consumer experience. Innovations in lightweight glass bottles are reducing transportation costs and environmental impact without compromising on durability. Advanced barrier coatings for plastic bottles are now effectively preserving wine quality, making them a viable alternative to glass. Smart labels incorporating NFC technology for provenance tracking and anti-counterfeiting are emerging, offering added value to consumers and brands. The development of biodegradable and compostable materials for secondary packaging and closures is also gaining momentum, aligning with global environmental initiatives and enhancing brand reputation.

Key Drivers of wine packaging Growth

The wine packaging market is propelled by several key growth drivers. The escalating global demand for wine, driven by evolving consumer lifestyles and increasing disposable incomes, directly fuels packaging consumption. Technological advancements in material science and manufacturing processes are enabling the creation of more sustainable, cost-effective, and aesthetically appealing packaging solutions. The growing emphasis on environmental sustainability is a significant catalyst, pushing for the adoption of recyclable, reusable, and biodegradable materials. Furthermore, the premiumization trend in the wine industry encourages investment in high-quality, innovative packaging that enhances brand perception and consumer appeal.

Challenges in the wine packaging Market

Despite robust growth, the wine packaging market faces several challenges. Stringent regulatory requirements concerning food safety, material composition, and labeling can increase compliance costs and slow down product innovation. Supply chain disruptions, geopolitical instability, and fluctuations in raw material prices, such as glass and aluminum, can impact production costs and availability. Intense competition from established players and emerging innovators necessitates continuous investment in R&D and marketing, putting pressure on profit margins. Furthermore, the perception of certain alternative packaging materials regarding wine quality and shelf-life can hinder their widespread adoption.

Emerging Opportunities in wine packaging

Emerging opportunities in the wine packaging market are centered around innovation and sustainability. The increasing consumer demand for eco-friendly products presents a significant opportunity for companies offering recyclable, reusable, and biodegradable packaging solutions. Technological breakthroughs in material science are enabling the development of novel packaging formats with enhanced barrier properties and reduced environmental footprints. Strategic partnerships and collaborations between packaging manufacturers, wineries, and technology providers can lead to the co-creation of innovative solutions and expanded market reach. Market expansion into untapped emerging economies with growing wine consumption also represents a substantial growth avenue.

Leading Players in the wine packaging Sector

- Alucaps Mexicana

- Amcor

- APPE Packaging

- Ardagh

- Barat Etiquettes

- Bevcan

- Bonar Plastics

- Collotype Labels International Proprietary

- Color

- Corticeira Amorim SGPS

- Crown Holdings

- DIAM Bouchage

- EMPAQUE

- FAMOSA

- Gallo (E&J) Winery

- Global Closure Systems

- G3

- Mala Verschluss-Systeme

- Mr. Labels Proprietary

- Nampak

Key Milestones in wine packaging Industry

- 2019: Increased global adoption of lightweight glass bottle technology, reducing shipping emissions and costs.

- 2020: Rise of e-commerce for wine sales, leading to innovations in protective and attractive shipping packaging.

- 2021: Growing consumer demand for sustainable packaging drives investment in recycled glass and plant-based materials.

- 2022: Introduction of advanced barrier films for plastic bottles, improving wine preservation capabilities.

- 2023: Increased focus on smart packaging solutions, including NFC tags for authentication and provenance tracking.

- 2024: Stringent new regulations on single-use plastics in several major markets, accelerating the shift towards reusable and recyclable alternatives.

Strategic Outlook for wine packaging Market

The strategic outlook for the wine packaging market is highly positive, driven by a strong emphasis on sustainability, technological innovation, and evolving consumer preferences. The market is poised for continued growth, with an increasing demand for eco-friendly, premium, and convenient packaging solutions. Companies that invest in research and development, embrace circular economy principles, and forge strategic partnerships will be well-positioned to capitalize on future market potential. The integration of smart technologies and the expansion into emerging markets will be key growth accelerators.

wine packaging Segmentation

-

1. Application

- 1.1. Wine Manufacturing Industry

- 1.2. Retail

- 1.3. Others

-

2. Types

- 2.1. Glass Bottles

- 2.2. Plastic Bottles

- 2.3. Plastic Bags

- 2.4. Wood Bottles

- 2.5. Others

wine packaging Segmentation By Geography

- 1. CA

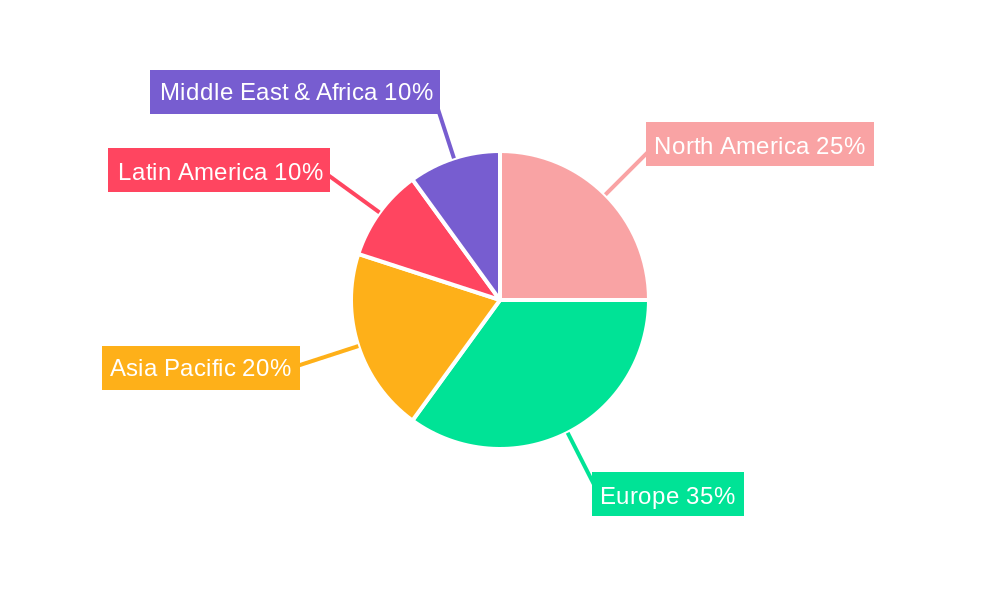

wine packaging Regional Market Share

Geographic Coverage of wine packaging

wine packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. wine packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Wine Manufacturing Industry

- 5.1.2. Retail

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Glass Bottles

- 5.2.2. Plastic Bottles

- 5.2.3. Plastic Bags

- 5.2.4. Wood Bottles

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Alucaps Mexicana

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Amcor

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 APPE Packaging

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Ardagh

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Barat Etiquettes

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Bevcan

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Bonar Plastics

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Collotype Labels International Proprietary

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Color

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Corticeira Amorim SGPS

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Crown Holdings

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 DIAM Bouchage

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 EMPAQUE

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 FAMOSA

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 Gallo (E&J) Winery

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 Global Closure Systems

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 G3

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 Mala Verschluss-Systeme

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 Mr. Labels Proprietary

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 Nampak

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.1 Alucaps Mexicana

List of Figures

- Figure 1: wine packaging Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: wine packaging Share (%) by Company 2025

List of Tables

- Table 1: wine packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: wine packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: wine packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: wine packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: wine packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: wine packaging Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the wine packaging?

The projected CAGR is approximately 8.8%.

2. Which companies are prominent players in the wine packaging?

Key companies in the market include Alucaps Mexicana, Amcor, APPE Packaging, Ardagh, Barat Etiquettes, Bevcan, Bonar Plastics, Collotype Labels International Proprietary, Color, Corticeira Amorim SGPS, Crown Holdings, DIAM Bouchage, EMPAQUE, FAMOSA, Gallo (E&J) Winery, Global Closure Systems, G3, Mala Verschluss-Systeme, Mr. Labels Proprietary, Nampak.

3. What are the main segments of the wine packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "wine packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the wine packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the wine packaging?

To stay informed about further developments, trends, and reports in the wine packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence