Key Insights

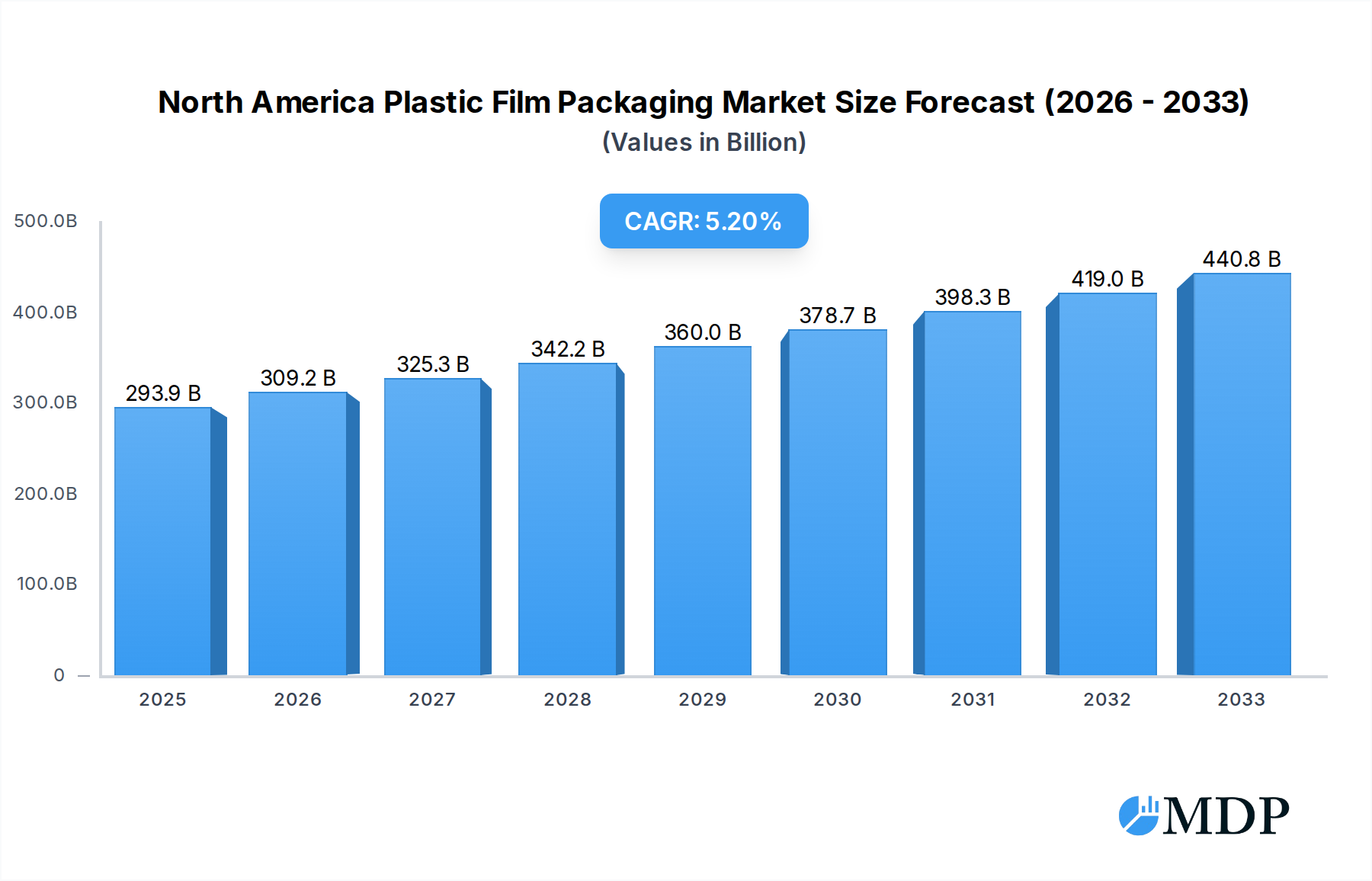

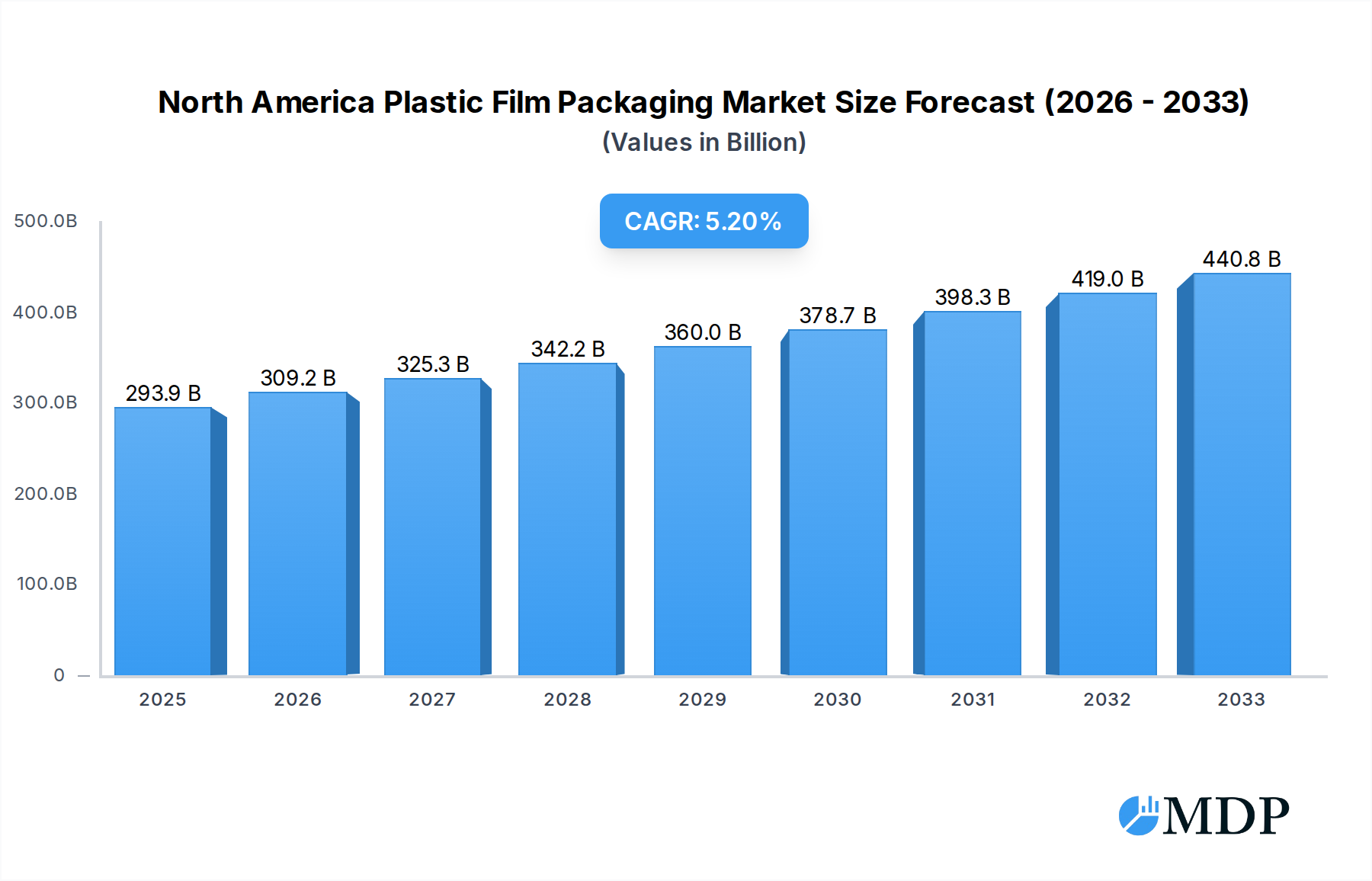

The North America Plastic Film Packaging Market is poised for robust expansion, projected to reach an estimated $293.92 billion in 2025. This growth is propelled by a CAGR of 5.3% through 2033, indicating a sustained upward trajectory driven by increasing demand across diverse end-user industries. The food sector, a significant consumer, will continue to be a primary driver, with a growing preference for flexible packaging solutions that extend shelf life and enhance product appeal for items ranging from fresh produce and dairy to confectionery and frozen foods. The healthcare industry's demand for sterile and protective packaging, coupled with the personal care and home care segments’ reliance on convenient and aesthetically pleasing films, further bolsters market vitality. The industrial packaging segment also contributes, driven by the need for durable and resilient film solutions. Key trends include the rising adoption of sustainable packaging alternatives, such as bio-based films, and innovative multi-layer film structures offering enhanced barrier properties.

North America Plastic Film Packaging Market Market Size (In Billion)

The market's dynamism is also shaped by evolving consumer preferences and regulatory landscapes. While the demand for traditional polymers like Polypropylene and Polyethylene remains strong due to their cost-effectiveness and versatility, there's a noticeable shift towards specialized films. Polystyrene and PETG films are gaining traction for their specific application benefits. The market faces challenges, including fluctuations in raw material prices and increasing environmental concerns and regulations surrounding plastic waste. However, technological advancements in film manufacturing, such as improved barrier technologies and lighter-weight materials, are mitigating these restraints and fostering innovation. Companies like Profol Americas Inc., TEKRA LLC, and Cosmo Films Inc. are at the forefront, investing in research and development to offer advanced film solutions that meet the stringent requirements of various industries and align with sustainability goals, ensuring continued market growth and evolution.

North America Plastic Film Packaging Market Company Market Share

This in-depth report provides a definitive analysis of the North America Plastic Film Packaging Market, a critical sector experiencing robust growth driven by evolving consumer demands and technological advancements. Covering the historical period from 2019 to 2024 and projecting through 2033, with a base and estimated year of 2025, this report offers unparalleled insights into market dynamics, industry trends, leading players, and strategic opportunities. With an estimated market size of $XX billion in 2025, expected to reach $XX billion by 2033, the North America plastic film packaging market is poised for significant expansion. Our analysis meticulously examines key segments, including various film types like Polypropylene (Polyprop), Polyethylene (Polyethy), Polystyrene, Bio-Based, PVC, EVOH, PETG, and Other Film Types, alongside crucial end-user industries such as Food (Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, and Seafood, Pet Food, Other Food), Healthcare, Personal Care & Home Care, Industrial Packaging, and Other End-User Industries. This report is an indispensable resource for stakeholders seeking to navigate the complexities and capitalize on the opportunities within this dynamic market.

North America Plastic Film Packaging Market Market Dynamics & Concentration

The North America Plastic Film Packaging Market is characterized by a moderate to high degree of concentration, with a few dominant players holding significant market share. Innovation remains a key driver, fueled by the continuous pursuit of enhanced barrier properties, sustainability, and cost-effectiveness in plastic films. Regulatory frameworks, particularly concerning plastic waste and recycling, are increasingly influencing market strategies and product development, pushing for the adoption of recyclable and bio-based alternatives. Product substitutes, such as rigid packaging and paper-based solutions, present a constant challenge, necessitating ongoing innovation in plastic film performance and environmental credentials. End-user trends, especially the demand for extended shelf life and convenient packaging in the food sector, are significant growth accelerators. Merger and acquisition (M&A) activities are strategically employed by major players to expand their product portfolios, geographical reach, and technological capabilities. The number of significant M&A deals in the sector has been xx in the historical period.

- Market Concentration: Dominated by key global players with established manufacturing capacities and distribution networks.

- Innovation Drivers: Focus on high-barrier films, lightweighting, sustainable materials (e.g., recycled content, bio-plastics), and advanced printing technologies.

- Regulatory Frameworks: Increasing emphasis on Extended Producer Responsibility (EPR) schemes, single-use plastic bans, and recyclability standards across North America.

- Product Substitutes: Competition from glass, metal, paper, and emerging biodegradable packaging materials.

- End-User Trends: Growing demand for flexible, on-the-go packaging solutions, enhanced food safety, and aesthetically pleasing designs.

- M&A Activities: Strategic acquisitions to consolidate market share, gain access to new technologies, and diversify product offerings.

North America Plastic Film Packaging Market Industry Trends & Analysis

The North America Plastic Film Packaging Market is witnessing a sustained period of growth, driven by an expanding global population, increasing disposable incomes, and a growing preference for convenient and protected packaged goods. The market's trajectory is significantly influenced by technological disruptions, including advancements in polymer science and manufacturing processes, leading to the development of thinner, stronger, and more functional plastic films. Consumer preferences are evolving rapidly, with a heightened awareness of environmental impact spurring demand for sustainable packaging solutions, such as recycled content films and bio-based alternatives. The competitive dynamics within the market are intense, characterized by fierce price competition, a constant need for product differentiation, and strategic collaborations. The Compound Annual Growth Rate (CAGR) for the North America Plastic Film Packaging Market is estimated at XX% from 2025 to 2033, reflecting a strong and consistent expansion. Market penetration of advanced barrier films and specialty plastics is steadily increasing across various end-user industries.

Key market growth drivers include:

- Expanding Food & Beverage Industry: The relentless demand for packaged food and beverages, driven by busy lifestyles and an increasing need for extended shelf life, is a primary growth engine.

- Growth in Healthcare and Pharmaceutical Packaging: Stringent requirements for sterile, protective, and tamper-evident packaging for pharmaceuticals and medical devices continue to fuel demand for specialized plastic films.

- Rising E-commerce Penetration: The surge in online retail necessitates robust and protective packaging for product shipment, including flexible plastic films for various goods.

- Innovation in Sustainable Packaging: Growing consumer and regulatory pressure is driving the development and adoption of recycled and bio-based plastic films, presenting new market avenues.

- Technological Advancements: Innovations in film extrusion, co-extrusion, and surface treatments enable the creation of films with enhanced barrier properties, printability, and functionality.

The industry is also experiencing a shift towards greater circularity, with a strong emphasis on improving recycling infrastructure and developing easily recyclable film structures. Companies are investing heavily in R&D to create films that offer comparable performance to conventional plastics but with a significantly reduced environmental footprint. This includes the development of mono-material solutions and films designed for chemical recycling. Furthermore, the rise of smart packaging technologies, incorporating features like indicators for freshness or authentication, is opening up new frontiers in the plastic film packaging sector. The competitive landscape is dynamic, with both established giants and agile startups vying for market share. Strategic partnerships and collaborations are becoming increasingly common as companies seek to leverage complementary expertise and expand their market reach.

Leading Markets & Segments in North America Plastic Film Packaging Market

The North America Plastic Film Packaging Market is segmented by film type and end-user industry, with distinct regions and countries exhibiting varying levels of dominance.

Dominant Film Types:

- Polyethylene (Polyethy): Continues to hold a significant market share due to its versatility, cost-effectiveness, and wide range of applications, particularly in food packaging, industrial wraps, and carrier bags. Its flexibility and strength make it an ideal choice for numerous packaging needs.

- Polypropylene (Polyprop): Shows strong performance, especially in food packaging for snacks, confectionery, and baked goods, owing to its excellent clarity, stiffness, and barrier properties. Metallized BOPP films, for instance, offer superior protection against light and oxygen.

- PETG: Gaining traction in specialized applications requiring high clarity, chemical resistance, and good impact strength, such as in medical packaging and consumer goods.

Dominant End-User Industries:

- Food Packaging: This segment remains the largest consumer of plastic film packaging in North America. The demand is driven by the need for extended shelf life, product protection, convenience, and aesthetic appeal.

- Candy & Confectionery: Requires visually appealing, tamper-evident, and moisture-barrier films.

- Frozen Foods: Demands films with excellent low-temperature flexibility and barrier properties against moisture and freezer burn.

- Fresh Produce: Benefits from films that control respiration and extend shelf life.

- Dairy Products: Requires films with high barrier properties to prevent spoilage and maintain freshness.

- Dry Foods: Utilizes films with good moisture resistance to maintain product integrity.

- Meat, Poultry, And Seafood: Requires high barrier films to prevent spoilage and extend shelf life, often incorporating oxygen and moisture barriers.

- Pet Food: Growing demand for durable, resealable, and aesthetically pleasing packaging.

- Healthcare: This sector demands high-performance films with stringent safety and sterility requirements, including films for medical devices, pharmaceutical packaging, and diagnostic kits.

- Personal Care & Home Care: Characterized by the need for visually appealing, functional, and protective packaging for a wide range of products like cosmetics, toiletries, and cleaning supplies.

Geographical Dominance:

- United States: Dominates the North America plastic film packaging market due to its large consumer base, extensive manufacturing infrastructure, and significant end-user industry presence. Economic policies supporting manufacturing and infrastructure development further bolster its position.

- Canada and Mexico: While smaller in market size, these countries are crucial components of the North American supply chain, with growing domestic demand and increasing integration with the U.S. market.

North America Plastic Film Packaging Market Product Developments

Recent product developments in the North America Plastic Film Packaging Market highlight a strong emphasis on sustainability and enhanced performance. Companies are actively launching innovative films designed to meet stringent environmental regulations and evolving consumer preferences. This includes the introduction of films with higher recycled content, advanced mono-material structures for improved recyclability, and bio-based alternatives derived from renewable resources. For example, UFlex's recent launch of its 'B-UUB-M' Outstanding Barrier Metallized BOPP Film underscores the trend towards films offering superior barrier properties for a wider range of food products, including dry fruits, beverages, chips, snacks, biscuits, cookies, confectionery, and chocolate items. These innovations aim to provide competitive advantages by extending product shelf life, reducing material usage, and improving the overall sustainability profile of packaged goods, directly addressing market demands for both functionality and environmental responsibility.

Key Drivers of North America Plastic Film Packaging Market Growth

Several key factors are propelling the growth of the North America Plastic Film Packaging Market. The expanding food and beverage industry is a primary driver, with an increasing demand for packaged goods that offer convenience and extended shelf life. Advancements in polymer technology and manufacturing processes are enabling the creation of high-performance films with superior barrier properties, lightweighting capabilities, and enhanced functionality. The growing healthcare sector, with its strict packaging requirements for pharmaceuticals and medical devices, also contributes significantly to market expansion. Furthermore, the rising adoption of e-commerce necessitates robust and protective packaging solutions, often met by flexible plastic films. Finally, increasing consumer awareness regarding sustainability is driving innovation in recyclable and bio-based plastic films, creating new market opportunities and pushing the industry towards more environmentally friendly solutions.

Challenges in the North America Plastic Film Packaging Market Market

Despite its robust growth, the North America Plastic Film Packaging Market faces several significant challenges. Stringent regulatory hurdles concerning plastic waste management, single-use plastic bans, and extended producer responsibility (EPR) schemes can impact production costs and market access. Supply chain disruptions, including raw material volatility and transportation issues, can affect profitability and delivery timelines. Intense competitive pressures from both established players and emerging sustainable alternatives can lead to price erosion and necessitate continuous innovation. The perception of plastic as an environmental hazard among some consumer segments can also pose a challenge, requiring ongoing efforts to educate the public on the benefits of properly managed plastic film packaging and advancements in recycling technologies.

Emerging Opportunities in North America Plastic Film Packaging Market

The North America Plastic Film Packaging Market is ripe with emerging opportunities driven by several catalysts. The growing demand for sustainable packaging solutions, including recycled content and bio-based films, presents a significant avenue for growth as companies strive to meet environmental commitments and consumer expectations. Technological breakthroughs in advanced barrier technologies and mono-material film structures are enabling the development of high-performance, easily recyclable packaging. Strategic partnerships and collaborations, such as those aimed at improving flexible film recycling infrastructure, as exemplified by the launch of the Flexible Film Recycling Alliance (FFRA), are creating new business models and expanding market reach. Furthermore, the expansion of e-commerce continues to drive the need for efficient, protective, and lightweight packaging, offering substantial growth potential for flexible film solutions.

Leading Players in the North America Plastic Film Packaging Market Sector

- Profol Americas Inc

- TEKRA LLC (A Mativ Brand)

- Cosmo Films Inc

- Taghleef Industries Inc

- Flex Films (USA) Inc (UFlex Limited)

- Klockner Pentaplast Group

- Tara Plastics Corporation (A Part of Sigma Plastic Group)

- Berry Global Group

- Jindal Films (Jindal Films Europe S A R L)

- Winpak Ltd

- Amcor Group GmbH

- Innovia Films (CCL Industries Inc )

- SUDPACK Holding Gmb

Key Milestones in North America Plastic Film Packaging Market Industry

- May 2024: UFlex launched new offerings in the final quarter of FY 2024, introducing products specifically designed for both labels and flexible packaging. The company's packaging films division rolled out the 'B-UUB-M' Outstanding Barrier Metallized BOPP Film, catering to products like dry fruits, beverages, chips, snacks, biscuits, cookies, confectionery, and chocolate items. This launch signifies a move towards high-performance, specialized films for the food sector.

- March 2024: The Plastics Industry Association (PLASTICS) launched the Flexible Film Recycling Alliance (FFRA) to boost recycling rates, improve access, and educate the public on flexible plastic film products in the United States. This initiative highlights a concerted effort by industry stakeholders to address the challenges of recycling flexible films and bags, aiming to foster a more circular economy.

Strategic Outlook for North America Plastic Film Packaging Market Market

The strategic outlook for the North America Plastic Film Packaging Market is overwhelmingly positive, driven by a confluence of accelerating trends and proactive industry initiatives. The increasing demand for sustainable packaging solutions presents a significant growth accelerator, prompting continued investment in recycled content films, bio-based materials, and mono-material designs that enhance recyclability. Technological advancements in film extrusion and barrier technology will further enable the development of higher-performing and more functional packaging, extending shelf life and reducing food waste. Strategic partnerships and collaborations aimed at improving recycling infrastructure, such as the FFRA, are crucial for building a more circular economy and mitigating environmental concerns. The sustained growth of e-commerce will continue to fuel the demand for lightweight, protective, and efficient flexible packaging solutions. Overall, the market is poised for continued expansion by embracing innovation, sustainability, and collaborative efforts to address both consumer needs and environmental imperatives.

North America Plastic Film Packaging Market Segmentation

-

1. Type

- 1.1. Polyprop

- 1.2. Polyethy

- 1.3. Polyethy

- 1.4. Polystyrene

- 1.5. Bio-Based

- 1.6. PVC, EVOH, PETG, and Other Film Types

-

2. End-User Industry

-

2.1. Food

- 2.1.1. Candy & Confectionery

- 2.1.2. Frozen Foods

- 2.1.3. Fresh Produce

- 2.1.4. Dairy Products

- 2.1.5. Dry Foods

- 2.1.6. Meat, Poultry, And Seafood

- 2.1.7. Pet Food

- 2.1.8. Other Fo

- 2.2. Healthcare

- 2.3. Personal Care & Home Care

- 2.4. Industrial Packaging

- 2.5. Other En

-

2.1. Food

North America Plastic Film Packaging Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

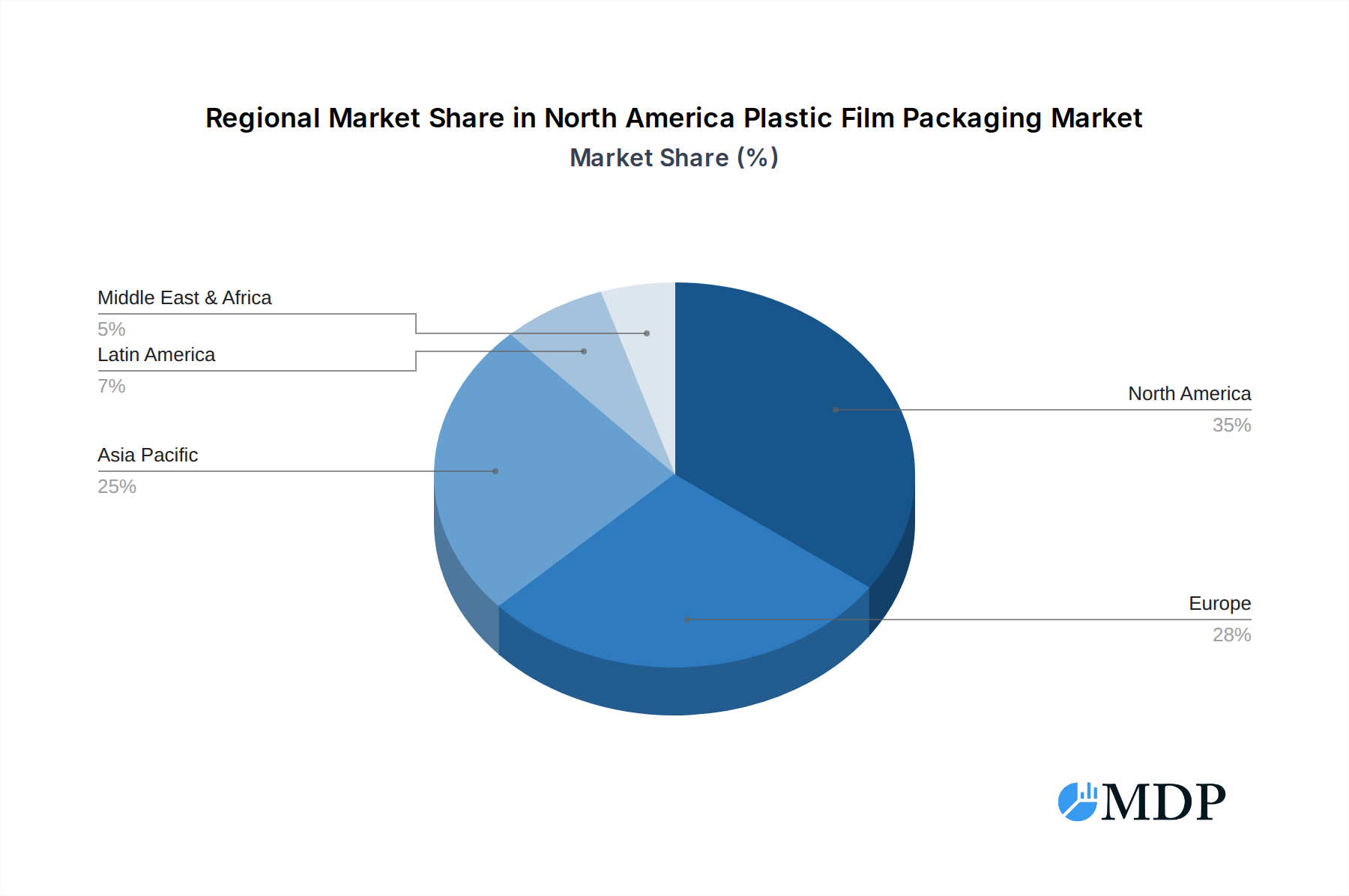

North America Plastic Film Packaging Market Regional Market Share

Geographic Coverage of North America Plastic Film Packaging Market

North America Plastic Film Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Polyprop

- 5.1.2. Polyethy

- 5.1.3. Polyethy

- 5.1.4. Polystyrene

- 5.1.5. Bio-Based

- 5.1.6. PVC, EVOH, PETG, and Other Film Types

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Food

- 5.2.1.1. Candy & Confectionery

- 5.2.1.2. Frozen Foods

- 5.2.1.3. Fresh Produce

- 5.2.1.4. Dairy Products

- 5.2.1.5. Dry Foods

- 5.2.1.6. Meat, Poultry, And Seafood

- 5.2.1.7. Pet Food

- 5.2.1.8. Other Fo

- 5.2.2. Healthcare

- 5.2.3. Personal Care & Home Care

- 5.2.4. Industrial Packaging

- 5.2.5. Other En

- 5.2.1. Food

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Plastic Film Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Polyprop

- 6.1.2. Polyethy

- 6.1.3. Polyethy

- 6.1.4. Polystyrene

- 6.1.5. Bio-Based

- 6.1.6. PVC, EVOH, PETG, and Other Film Types

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Food

- 6.2.1.1. Candy & Confectionery

- 6.2.1.2. Frozen Foods

- 6.2.1.3. Fresh Produce

- 6.2.1.4. Dairy Products

- 6.2.1.5. Dry Foods

- 6.2.1.6. Meat, Poultry, And Seafood

- 6.2.1.7. Pet Food

- 6.2.1.8. Other Fo

- 6.2.2. Healthcare

- 6.2.3. Personal Care & Home Care

- 6.2.4. Industrial Packaging

- 6.2.5. Other En

- 6.2.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Profol Americas Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 TEKRA LLC (A Mativ Brand)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Cosmo Films Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Taghleef Industries Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Flex Films (USA) Inc (UFlex Limited)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Klockner Pentaplast Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Tara Plastics Corporation (A Part of Sigma Plastic Group)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Berry Global Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Jindal Films (Jindal Films Europe S A R L)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Winpak Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Amcor Group GmbH

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Innovia Films (CCL Industries Inc )

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 SUDPACK Holding Gmb

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Profol Americas Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Plastic Film Packaging Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Plastic Film Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: North America Plastic Film Packaging Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Plastic Film Packaging Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 3: North America Plastic Film Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: North America Plastic Film Packaging Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: North America Plastic Film Packaging Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 6: North America Plastic Film Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States North America Plastic Film Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Plastic Film Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Plastic Film Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Plastic Film Packaging Market?

The projected CAGR is approximately 5.3%.

2. Which companies are prominent players in the North America Plastic Film Packaging Market?

Key companies in the market include Profol Americas Inc, TEKRA LLC (A Mativ Brand), Cosmo Films Inc, Taghleef Industries Inc, Flex Films (USA) Inc (UFlex Limited), Klockner Pentaplast Group, Tara Plastics Corporation (A Part of Sigma Plastic Group), Berry Global Group, Jindal Films (Jindal Films Europe S A R L), Winpak Ltd, Amcor Group GmbH, Innovia Films (CCL Industries Inc ), SUDPACK Holding Gmb.

3. What are the main segments of the North America Plastic Film Packaging Market?

The market segments include Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 293.92 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Convenient Packaging.

6. What are the notable trends driving market growth?

Polyethylene Film Is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Increased Demand for Convenient Packaging.

8. Can you provide examples of recent developments in the market?

May 2024: UFlex, a flexible packaging manufacturer with operations in the United States, launched its offerings in the final quarter of FY 2024. The company introduced new products specifically designed for both labels and flexible packaging. UFlex's packaging films division notably rolled out the 'B-UUB-M' Outstanding Barrier Metallized BOPP Film. This innovative film is crafted to cater to various products, including dry fruits, beverages, chips, snacks, biscuits, cookies, confectionery, and chocolate items.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Plastic Film Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Plastic Film Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Plastic Film Packaging Market?

To stay informed about further developments, trends, and reports in the North America Plastic Film Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence