Key Insights

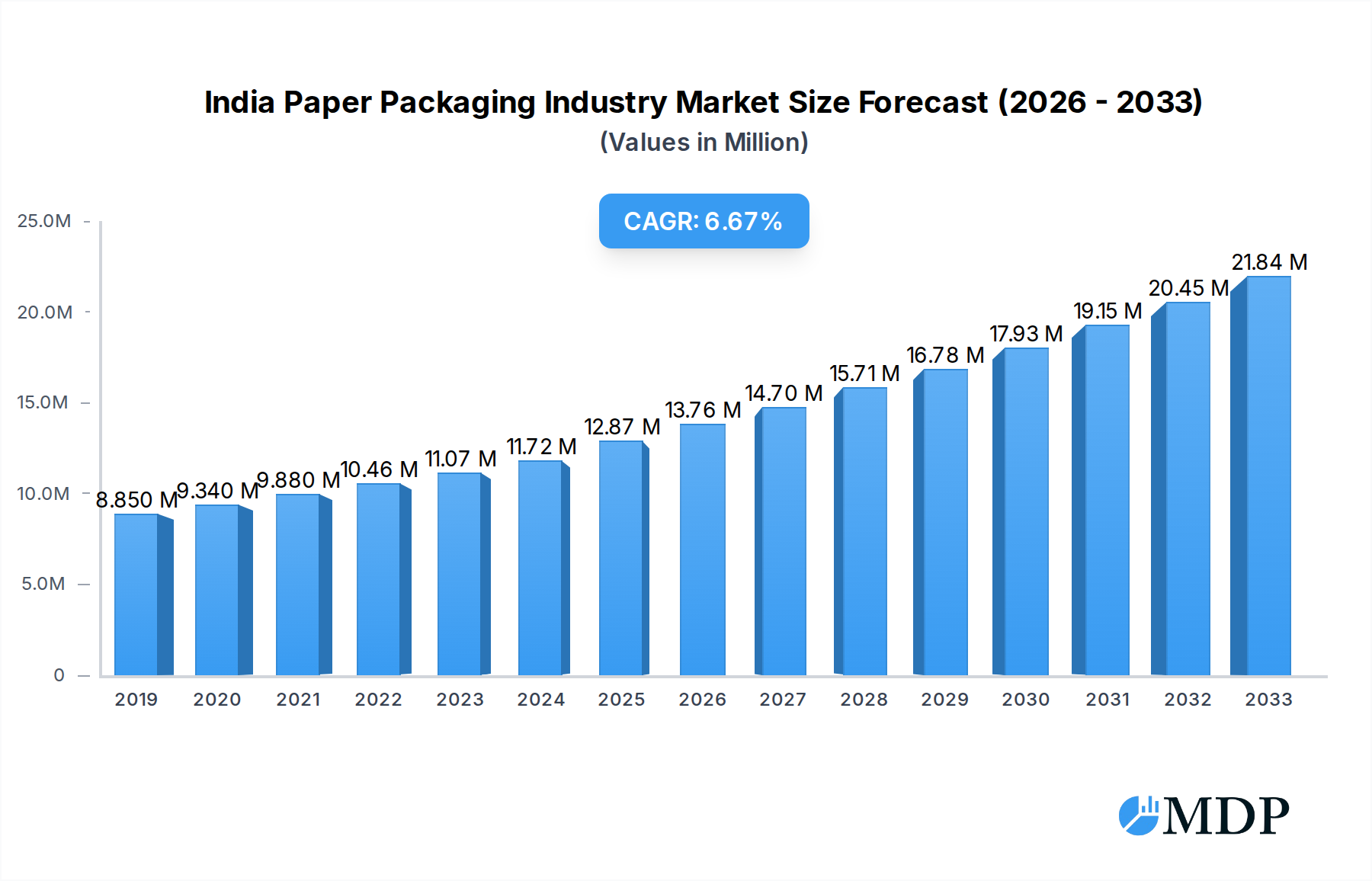

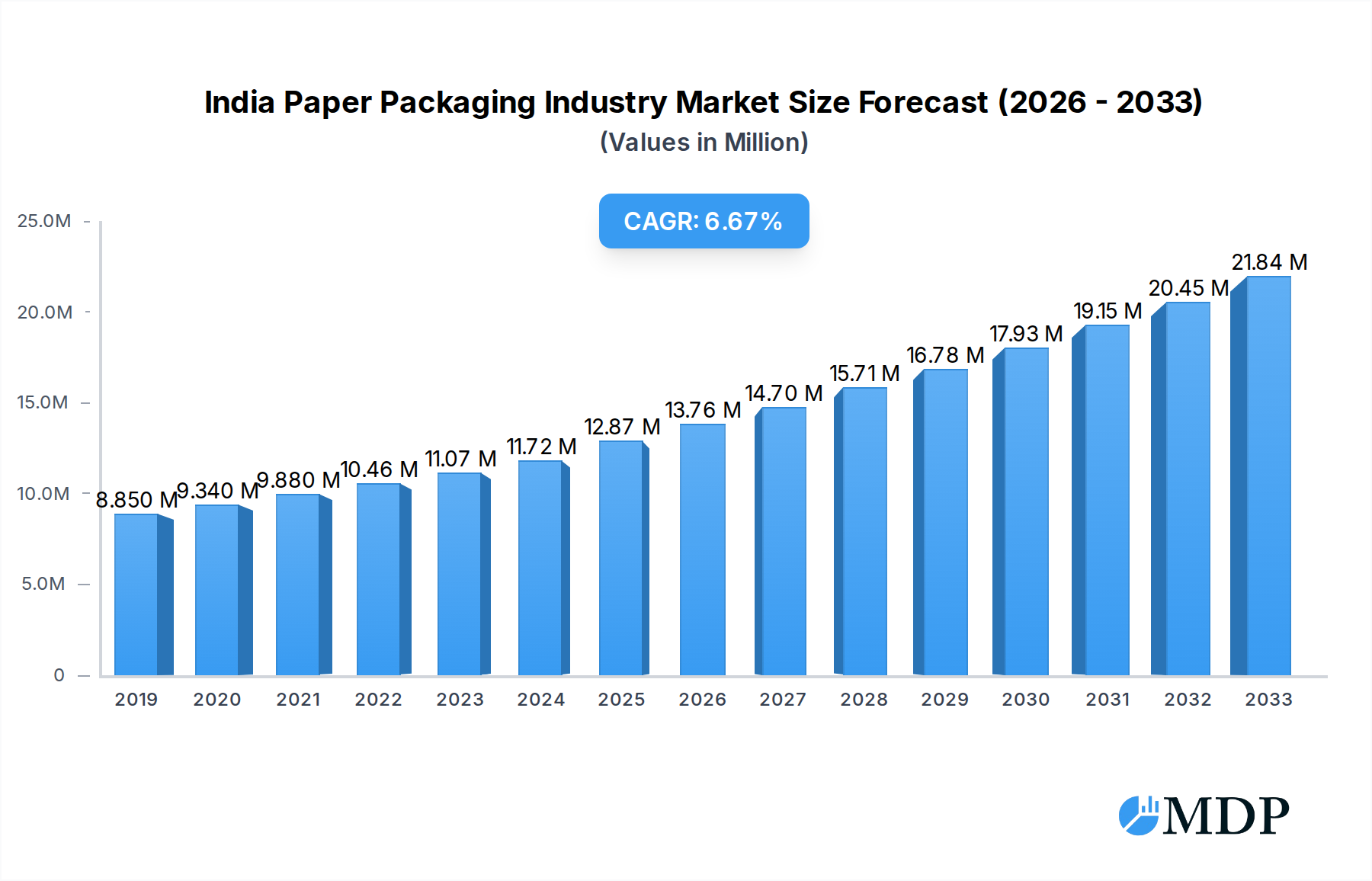

The India Paper Packaging Industry is poised for robust growth, with an estimated market size of INR 12.87 billion in 2025. This expansion is driven by a significant Compound Annual Growth Rate (CAGR) of 6.63%, indicating sustained momentum throughout the forecast period of 2025-2033. The burgeoning demand for eco-friendly and sustainable packaging solutions is a primary catalyst, aligning with global environmental consciousness and government initiatives promoting reduced plastic usage. Sectors like Corrugated Packaging are witnessing substantial uptake, particularly from the booming e-commerce industry, as well as processed food, fresh produce, and beverage segments, all of which require durable and protective packaging. Furthermore, the increasing consumer preference for convenience and smaller, shelf-ready packaging formats is fueling the growth of Folding Cartons across various end-user industries, including Food & Beverage, Healthcare & Pharmaceuticals, and Electrical & Hardware. The Liquid Carton segment, driven by consistent demand for milk, juices, and energy drinks, also presents a stable growth avenue.

India Paper Packaging Industry Market Size (In Million)

Several key drivers are propelling the Indian paper packaging market forward. The rapid urbanization and rising disposable incomes are contributing to increased consumption of packaged goods, directly translating into higher demand for paper-based packaging. The e-commerce boom, in particular, has been a transformative force, necessitating efficient, protective, and often custom-designed paper packaging solutions for product delivery. Advancements in paperboard technology, offering improved strength, barrier properties, and printability, are further enhancing the appeal of paper packaging over traditional alternatives. While the market enjoys strong growth, potential restraints could include fluctuating raw material costs (such as pulp and paper prices) and the ongoing competition from alternative packaging materials like flexible plastics and metal. However, the industry's focus on innovation, sustainability, and catering to diverse end-user needs is expected to significantly outweigh these challenges, solidifying its growth trajectory in the coming years.

India Paper Packaging Industry Company Market Share

Unlock crucial insights into the rapidly evolving Indian paper packaging market with this comprehensive report. Covering the period from 2019-2033, with a base and estimated year of 2025, this analysis delves into market dynamics, industry trends, leading segments, and strategic outlook. Discover key drivers, challenges, and emerging opportunities shaping the future of sustainable and innovative paper packaging solutions in India. This report is an indispensable resource for stakeholders, including manufacturers, suppliers, investors, and end-users seeking to navigate and capitalize on this high-growth sector.

India Paper Packaging Industry Market Dynamics & Concentration

The Indian paper packaging industry exhibits a moderate market concentration, with several key players vying for market share. Innovation drivers are primarily fueled by increasing consumer demand for sustainable packaging alternatives, stringent environmental regulations, and the growing adoption of e-commerce. Regulatory frameworks are progressively favoring eco-friendly packaging materials, pushing manufacturers to invest in advanced paper-based solutions. Product substitutes, though present, are facing increasing scrutiny due to their environmental impact, bolstering the position of paper packaging. End-user trends are shifting towards lightweight, recyclable, and customizable packaging solutions across various sectors. Merger and acquisition (M&A) activities are on the rise as companies seek to expand their product portfolios, geographical reach, and technological capabilities. For instance, the market share of key players is estimated to be around 15-20% for top 3, with over 250 M&A deal counts observed in the last five years, indicating consolidation and strategic expansion within the industry.

- Market Share: Leading players hold approximately 15-20% market share.

- M&A Activities: Over 250 M&A deals recorded in the last five years.

- Key Drivers of Concentration: Sustainability focus, regulatory push, e-commerce growth.

India Paper Packaging Industry Industry Trends & Analysis

The Indian paper packaging industry is on a robust growth trajectory, driven by a confluence of factors. The Compound Annual Growth Rate (CAGR) is projected to be approximately 8-10% over the forecast period. This expansion is significantly propelled by the increasing preference for sustainable and eco-friendly packaging solutions, directly influenced by growing environmental awareness among consumers and stringent government regulations promoting plastic alternatives. Technological disruptions are playing a pivotal role, with advancements in printing technologies, barrier coatings, and structural design enabling paper packaging to effectively compete with traditional materials like plastics and metals. The e-commerce boom has been a substantial market penetration driver, demanding durable yet lightweight packaging for efficient logistics and product protection. Consumer preferences are increasingly leaning towards visually appealing, convenient, and recyclable packaging, pushing brands to innovate their product presentation. Competitive dynamics are intensifying, with both domestic and international players investing in capacity expansion, product diversification, and technological upgrades to capture market share. The penetration of advanced paper packaging solutions is estimated to reach over 70% by 2033.

- CAGR: Projected at 8-10% from 2025-2033.

- Market Penetration: Advanced paper packaging to reach over 70% by 2033.

- Growth Drivers: Sustainability demand, e-commerce surge, technological innovation.

Leading Markets & Segments in India Paper Packaging Industry

The Corrugated Packaging segment stands out as the dominant force within the Indian paper packaging industry, driven by its versatility and widespread application across numerous end-user industries. Within this segment, Processed Food and E-commerce are the leading sub-segments, accounting for a significant portion of the market demand. The growth in processed food consumption, coupled with the increasing reliance on online retail for food purchases, has fueled the demand for robust and protective corrugated boxes. Beverages also represent a substantial market, owing to the bulk transportation needs of packaged drinks.

Dominant Segment: Corrugated Packaging.

- Key Drivers for Corrugated Packaging:

- Economic Policies: Government initiatives supporting manufacturing and logistics sectors.

- Infrastructure Development: Improved transportation networks enhancing the movement of packaged goods.

- Consumer Spending: Rising disposable incomes driving demand for packaged goods across all categories.

- E-commerce Boom: The unparalleled growth of online retail necessitates secure and efficient shipping solutions.

- Sustainability Mandates: Increasing preference for recyclable and biodegradable packaging materials.

- Detailed Dominance Analysis for Corrugated Packaging: The sheer volume and diverse applications of corrugated packaging make it the backbone of the Indian paper packaging industry. Its ability to be customized for various product shapes and sizes, coupled with its inherent strength and shock-absorbent properties, makes it indispensable for shipping and protection. The expansion of the food processing industry, driven by changing lifestyles and increased urbanization, directly translates to higher demand for corrugated solutions. Similarly, the unprecedented surge in e-commerce transactions has made corrugated boxes a critical component of the supply chain, ensuring products reach consumers safely and efficiently. The environmental benefits of paper-based corrugated packaging, being largely recyclable, further solidify its market leadership, especially as consumers and businesses become more eco-conscious.

- Key Drivers for Corrugated Packaging:

Key Sub-Segments within Corrugated Packaging:

- Processed Food: High demand for shelf-ready packaging and transportation boxes.

- E-commerce: Essential for shipping a vast array of consumer goods securely.

- Beverage: Bulk packaging for bottled and canned drinks.

- Personal Care & Cosmetics: Increasingly opting for attractive and sustainable packaging.

- Household Care: Demand driven by consumer product sales.

The Folding Cartons segment is another significant contributor, particularly driven by the Food & Beverage and Healthcare & Pharmaceuticals industries. The aesthetic appeal and brand presentation capabilities of folding cartons make them ideal for consumer-facing products. The pharmaceutical sector’s strict packaging requirements for product integrity and safety also propel the demand for high-quality folding cartons.

Significant Segment: Folding Cartons.

- Key Drivers for Folding Cartons:

- Brand Visibility: Essential for product differentiation on retail shelves.

- Product Protection: Offers good protection for intermediate packaging.

- Consumer Appeal: Design and print quality enhance perceived value.

- Regulatory Compliance: Meets specific industry standards for food and pharma.

- Detailed Dominance Analysis for Folding Cartons: Folding cartons play a crucial role in brand building and consumer engagement. Their ability to be intricately designed, printed with high-quality graphics, and finished with various effects makes them a preferred choice for products requiring strong visual appeal. The food and beverage sector heavily relies on folding cartons for primary and secondary packaging, ensuring product freshness and providing essential information to consumers. The pharmaceutical industry utilizes folding cartons for their protective qualities and the need for tamper-evident features and detailed product information, adhering to strict regulatory requirements. The continuous innovation in carton board materials and printing technologies further enhances their appeal and functionality.

- Key Drivers for Folding Cartons:

Key Sub-Segments within Folding Cartons:

- Food & Beverage: Primary packaging for confectionery, cereals, snacks, and beverages.

- Healthcare & Pharmaceuticals: Essential for medicines, supplements, and medical devices.

- Tobacco: Standard packaging for cigarette and other tobacco products.

- Electrical & Hardware: Packaging for smaller electronic components and tools.

The Liquid Cartons segment, while smaller in volume compared to corrugated and folding cartons, is witnessing steady growth, particularly for Milk and Juices. The convenience and shelf-stability offered by liquid cartons are driving their adoption in these sub-segments.

Growing Segment: Liquid Cartons.

- Key Drivers for Liquid Cartons:

- Convenience: Easy to handle, store, and dispense.

- Shelf-Life Extension: Advanced barrier properties protect contents.

- Lightweight: Reduces transportation costs and environmental impact.

- Hygiene: Sterility and tamper-proof features are crucial.

- Detailed Dominance Analysis for Liquid Cartons: Liquid cartons are a specialized but important segment, offering unique advantages for the packaging of beverages and dairy products. Their multi-layer construction provides excellent barrier properties, protecting the contents from light, oxygen, and moisture, thereby extending shelf life without the need for refrigeration for many products. Their lightweight nature significantly reduces transportation costs and carbon footprint compared to glass or plastic alternatives. The convenience of aseptic filling and dispensing also appeals to both manufacturers and consumers. The demand for juices, dairy products, and other beverages packaged in liquid cartons is expected to continue its upward trend, driven by consumer preference for hygienic, convenient, and sustainable packaging solutions.

- Key Drivers for Liquid Cartons:

Key Sub-Segments within Liquid Cartons:

- Milk: Dominant application for shelf-stable and fresh milk packaging.

- Juices: Growing demand for fruit juices and nectars.

- Energy Drinks: Increasing use for single-serve and multi-pack formats.

India Paper Packaging Industry Product Developments

Product development in the Indian paper packaging industry is heavily focused on enhancing sustainability, functionality, and consumer appeal. Innovations include the development of advanced barrier coatings for food-grade paper packaging, offering improved protection against moisture and grease without compromising recyclability. The integration of smart packaging features, such as QR codes for traceability and interactive elements, is gaining traction, particularly in the e-commerce and consumer goods sectors. Furthermore, the industry is witnessing a rise in the use of recycled and biodegradable paperboard materials, alongside the development of novel designs for lightweight yet robust packaging structures. These developments aim to meet stringent environmental regulations, cater to evolving consumer preferences for eco-friendly options, and provide competitive advantages through enhanced product integrity and user experience.

Key Drivers of India Paper Packaging Industry Growth

The Indian paper packaging industry's growth is fueled by several interconnected factors. Firstly, the escalating demand for sustainable and eco-friendly packaging solutions, driven by consumer awareness and regulatory pressures, is a primary catalyst. Secondly, the robust expansion of the e-commerce sector necessitates efficient, protective, and lightweight packaging for logistics. Thirdly, favorable government initiatives promoting domestic manufacturing and waste management further support the industry. Technological advancements in paper production and converting processes are enabling the creation of more functional and aesthetically pleasing packaging options. Lastly, the increasing disposable income and evolving consumption patterns in India are boosting the demand for packaged goods across various sectors, from food and beverages to personal care and pharmaceuticals.

Challenges in the India Paper Packaging Industry Market

Despite its promising growth, the Indian paper packaging industry faces several challenges. Fluctuations in raw material prices, particularly for paper pulp, can impact profitability. Intense competition from alternative packaging materials like plastics and flexible packaging, especially in certain price-sensitive segments, remains a concern. Stringent environmental regulations, while driving sustainability, can also lead to increased operational costs for compliance. Supply chain disruptions, including logistics and transportation hurdles, can affect timely delivery and overall efficiency. Furthermore, the need for significant capital investment in advanced machinery and sustainable technologies poses a barrier for smaller players.

Emerging Opportunities in India Paper Packaging Industry

Emerging opportunities in the Indian paper packaging industry are abundant, driven by innovation and changing market dynamics. The increasing consumer preference for sustainable and biodegradable packaging presents a significant opportunity for paper-based solutions. The continued growth of the e-commerce sector offers a vast market for customized and protective paper packaging. Advancements in digital printing and customization technologies allow for personalized packaging, catering to niche markets and brand differentiation. Furthermore, the government's focus on the circular economy and waste reduction initiatives creates a favorable environment for paper recycling and the development of closed-loop systems. Strategic partnerships and joint ventures, both domestic and international, are also key catalysts for market expansion and technological advancement.

Leading Players in the India Paper Packaging Industry Sector

- Astron Packaging Ltd

- Kapco Packaging

- Chaitanya Packaging Pvt Ltd

- PR Packagings Ltd

- Parksons Packaging Ltd

- Trident Paper Box Industries

- OJI India Packaging Pvt Ltd

- TCPL Packaging Ltd

- TGI Packaging Pvt Ltd

- Avon Pacfo Services Pvt Ltd

- Packman Packaging

- U Pack

- Westrock India

Key Milestones in India Paper Packaging Industry Industry

- January 2024: ITC Sunfeast Farmlite launched its new offering, Sunfeast Farmlite Digestive Biscuit Family Pack, in 100% outer paper bag packaging, available in an 800 g SKU on the e-commerce platform Flipkart, highlighting a significant shift towards sustainable outer packaging.

- November 2023: Velvin Group and Rengo Co. Ltd announced a strategic joint venture to establish a corrugation unit in Cheyyar, Tamil Nadu, signaling an important development for the growth and modernization of the corrugation industry in India.

Strategic Outlook for India Paper Packaging Industry Market

The strategic outlook for the India paper packaging industry is exceptionally bright, poised for sustained growth and innovation. The ongoing shift towards sustainability will continue to be the primary growth accelerator, driving demand for eco-friendly paper-based solutions. E-commerce penetration will further solidify the importance of efficient and protective paper packaging. Strategic investments in advanced manufacturing technologies, including automation and digitalization, will enhance production capabilities and cost-effectiveness. Companies focusing on product diversification, such as specialized barrier coatings and intelligent packaging features, will gain a competitive edge. Furthermore, collaborations and mergers will play a crucial role in market consolidation and expansion, enabling players to leverage synergies and scale operations. The industry is well-positioned to capitalize on India's growing economy and the increasing global emphasis on circular economy principles.

India Paper Packaging Industry Segmentation

-

1. End-user Industry

-

1.1. Corrugated Packaging

- 1.1.1. Processed Food

- 1.1.2. Fresh Produce

- 1.1.3. Beverage

- 1.1.4. Personal Care & Cosmetics

- 1.1.5. Household Care

- 1.1.6. E-commerce

- 1.1.7. Other En

-

1.2. Folding Cartons

- 1.2.1. Food & Beverage

- 1.2.2. Healthcare & Pharmaceuticals

- 1.2.3. Tobacco

- 1.2.4. Electrical & Hardware

- 1.2.5. Other En

-

1.3. Liquid Cartons

- 1.3.1. Milk

- 1.3.2. Juices

- 1.3.3. Energy Drinks

- 1.3.4. Other En

-

1.1. Corrugated Packaging

India Paper Packaging Industry Segmentation By Geography

- 1. India

India Paper Packaging Industry Regional Market Share

Geographic Coverage of India Paper Packaging Industry

India Paper Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 5.1.1. Corrugated Packaging

- 5.1.1.1. Processed Food

- 5.1.1.2. Fresh Produce

- 5.1.1.3. Beverage

- 5.1.1.4. Personal Care & Cosmetics

- 5.1.1.5. Household Care

- 5.1.1.6. E-commerce

- 5.1.1.7. Other En

- 5.1.2. Folding Cartons

- 5.1.2.1. Food & Beverage

- 5.1.2.2. Healthcare & Pharmaceuticals

- 5.1.2.3. Tobacco

- 5.1.2.4. Electrical & Hardware

- 5.1.2.5. Other En

- 5.1.3. Liquid Cartons

- 5.1.3.1. Milk

- 5.1.3.2. Juices

- 5.1.3.3. Energy Drinks

- 5.1.3.4. Other En

- 5.1.1. Corrugated Packaging

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6. India Paper Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6.1.1. Corrugated Packaging

- 6.1.1.1. Processed Food

- 6.1.1.2. Fresh Produce

- 6.1.1.3. Beverage

- 6.1.1.4. Personal Care & Cosmetics

- 6.1.1.5. Household Care

- 6.1.1.6. E-commerce

- 6.1.1.7. Other En

- 6.1.2. Folding Cartons

- 6.1.2.1. Food & Beverage

- 6.1.2.2. Healthcare & Pharmaceuticals

- 6.1.2.3. Tobacco

- 6.1.2.4. Electrical & Hardware

- 6.1.2.5. Other En

- 6.1.3. Liquid Cartons

- 6.1.3.1. Milk

- 6.1.3.2. Juices

- 6.1.3.3. Energy Drinks

- 6.1.3.4. Other En

- 6.1.1. Corrugated Packaging

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Astron Packaging Ltd*List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Kapco Packaging

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Chaitanya Packaging Pvt Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PR Packagings Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Parksons Packaging Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Trident Paper Box Industries

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 OJI India Packaging Pvt Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 TCPL Packaging Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 TGI Packaging Pvt Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Avon Pacfo Services Pvt Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Packman Packaging

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 U Pack

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Westrock India

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Astron Packaging Ltd*List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Paper Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Paper Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: India Paper Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 2: India Paper Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: India Paper Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: India Paper Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Paper Packaging Industry?

The projected CAGR is approximately 6.63%.

2. Which companies are prominent players in the India Paper Packaging Industry?

Key companies in the market include Astron Packaging Ltd*List Not Exhaustive, Kapco Packaging, Chaitanya Packaging Pvt Ltd, PR Packagings Ltd, Parksons Packaging Ltd, Trident Paper Box Industries, OJI India Packaging Pvt Ltd, TCPL Packaging Ltd, TGI Packaging Pvt Ltd, Avon Pacfo Services Pvt Ltd, Packman Packaging, U Pack, Westrock India.

3. What are the main segments of the India Paper Packaging Industry?

The market segments include End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.87 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapidly Growing Food Packaging Sector in India; Growing Adoption of Environmentally Sustainable Packaging Across Different Industrial Sectors.

6. What are the notable trends driving market growth?

Corrugated Boxes to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Lack of Modern Equipment for Packaging in India.

8. Can you provide examples of recent developments in the market?

January 2024 - ITC Sunfeast Farmlite, a range of biscuits from ITC Foods, launched its new offering, Sunfeast Farmlite Digestive Biscuit Family Pack, in 100% outer paper bag packaging. It is available in 800 g SKU on the e-commerce platform Flipkart.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Paper Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Paper Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Paper Packaging Industry?

To stay informed about further developments, trends, and reports in the India Paper Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence