Key Insights

The global dangerous goods packaging market is poised for substantial growth, projected to reach an estimated $18.5 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.8% from 2025 to 2033. This expansion is driven by the escalating global trade of hazardous materials, including chemicals, pharmaceuticals, and industrial components, which necessitate stringent safety and regulatory compliance in their transportation. The increasing emphasis on international shipping standards, such as those set by the UN Recommendations on the Transport of Dangerous Goods, IATA Dangerous Goods Regulations, and IMDG Code, directly fuels the demand for certified and reliable packaging solutions. Key market segments contributing to this growth include Explosives and Flammable Liquids, which represent a significant portion of hazardous shipments. The rising need for specialized packaging designed to prevent leaks, contamination, and environmental damage underscores the critical role of this market in ensuring safe and secure global supply chains.

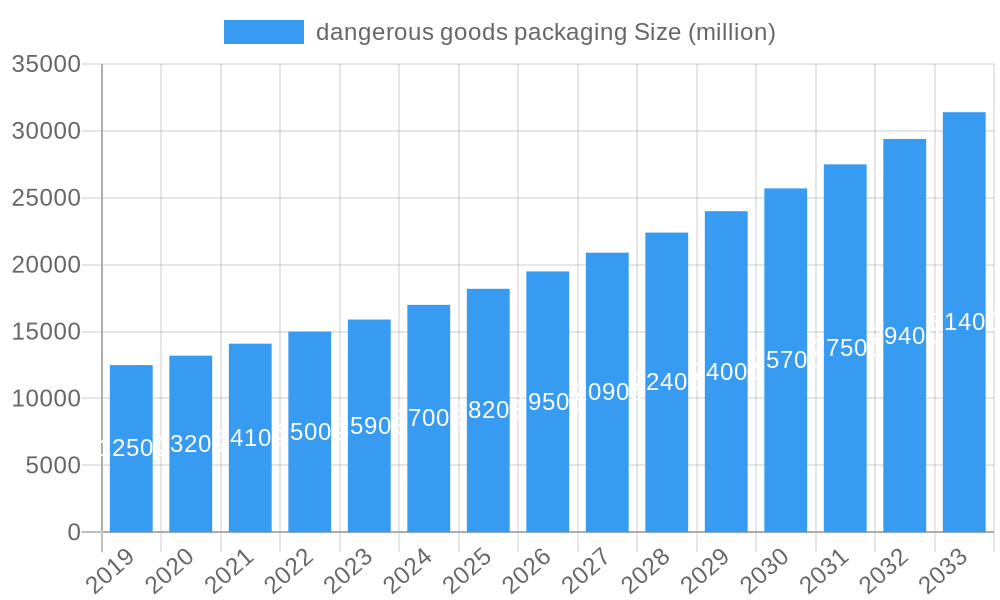

dangerous goods packaging Market Size (In Billion)

The market is characterized by a dynamic interplay of innovation and regulatory adherence. Trends such as the development of sustainable and reusable packaging solutions are gaining traction, driven by environmental concerns and corporate social responsibility initiatives. Simultaneously, advancements in material science are leading to the creation of lighter yet stronger packaging, enhancing logistical efficiency. However, the market faces certain restraints, including the high cost of specialized and certified packaging, and the complexities associated with navigating diverse international regulations, which can pose a challenge for smaller manufacturers. Despite these hurdles, the industry is witnessing significant investment in research and development, with companies like Nefab, P&M Packing, and TEN-E Packaging Services leading the charge in offering comprehensive and compliant packaging solutions. The market's segmentation by type, including High Danger, Medium Danger, and Low Danger classifications, reflects the tailored approaches required to address the unique risks associated with different categories of dangerous goods, ensuring optimal safety across the entire supply chain.

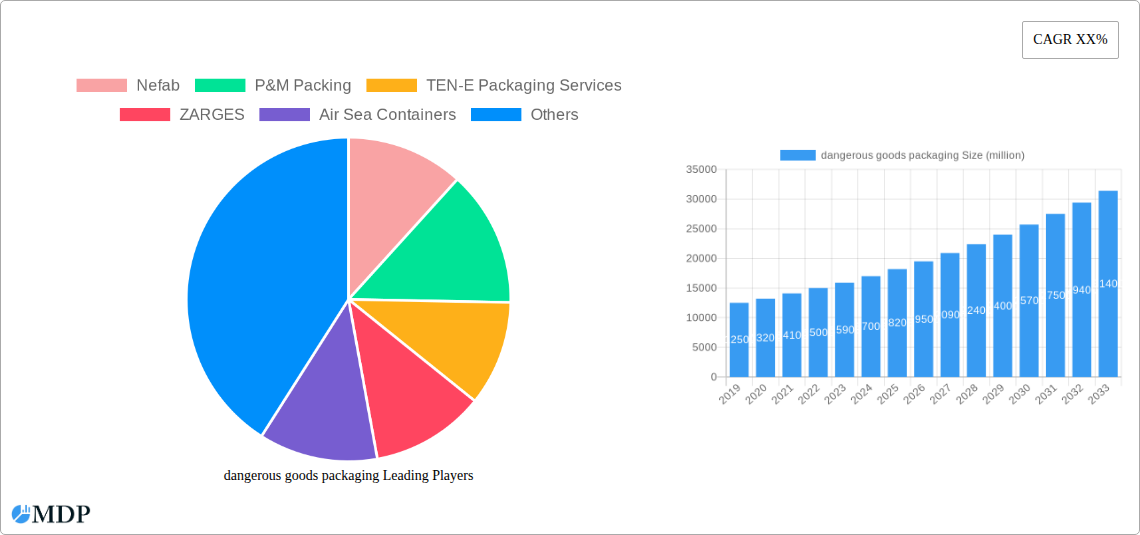

dangerous goods packaging Company Market Share

This in-depth report provides a panoramic view of the global dangerous goods packaging market, spanning from 2019 to 2033. It meticulously analyzes market dynamics, industry trends, leading segments, product innovations, growth drivers, challenges, and emerging opportunities. With a base year of 2025 and a forecast period extending to 2033, this report equips industry stakeholders with critical insights for strategic decision-making in the hazardous materials packaging sector.

dangerous goods packaging Market Dynamics & Concentration

The dangerous goods packaging market exhibits moderate concentration, with a mix of large, established players and specialized niche providers. Key innovation drivers include the relentless demand for enhanced safety, compliance with evolving international regulations (such as IATA, IMDG, and ADR), and the increasing adoption of sustainable and eco-friendly packaging solutions. Regulatory frameworks, while stringent, are also a catalyst for innovation as companies strive to meet and exceed these requirements, often leading to premium pricing for certified products. Product substitutes, while limited due to the inherent risks associated with transporting hazardous materials, primarily involve variations in material composition and design to optimize performance and cost-effectiveness. End-user trends are leaning towards lighter, more durable, and easily identifiable packaging, with a growing emphasis on supply chain visibility and traceability. Mergers and acquisitions (M&A) activities within the sector are moderately active, driven by the desire for market consolidation, expanded product portfolios, and geographical reach. For instance, a recent significant M&A deal involved a multinational packaging corporation acquiring a specialized chemical packaging solutions provider, aiming to integrate advanced material science capabilities. The market share of the top five players is estimated to be around 60 million. Over the historical period (2019-2024), approximately 15 significant M&A deals have been recorded, signaling a strategic realignment of forces within the industry.

dangerous goods packaging Industry Trends & Analysis

The dangerous goods packaging industry is projected for robust growth, driven by an escalating global trade in chemicals, pharmaceuticals, and industrial goods, many of which are classified as hazardous. The Compound Annual Growth Rate (CAGR) is anticipated to be approximately 6.5% during the forecast period (2025-2033). Technological disruptions are playing a pivotal role, with advancements in material science leading to the development of lighter yet stronger packaging, improved impact resistance, and enhanced barrier properties to contain volatile substances. The integration of smart technologies, such as RFID tags and GPS trackers, for real-time monitoring of shipments is also gaining traction, significantly improving supply chain security and accountability. Consumer preferences are increasingly shaped by a demand for packaging that not only ensures safety but also minimizes environmental impact. This has led to a surge in demand for recyclable, biodegradable, and reusable dangerous goods containers. Competitive dynamics are characterized by intense price competition, a strong emphasis on regulatory compliance, and the continuous pursuit of product differentiation through innovative design and material. Market penetration for advanced hazardous materials packaging solutions is steadily increasing, particularly in developed economies with stricter safety regulations and a higher volume of specialized cargo. For example, the penetration rate for advanced composite packaging solutions for flammable liquids has reached an estimated 45 million units. The increasing complexity of chemical formulations and the rise of specialized industrial applications are further bolstering the need for bespoke and high-performance packaging. The market is also witnessing a greater focus on lifecycle assessment of packaging, encouraging manufacturers to develop solutions that reduce waste and facilitate easier disposal or recycling.

Leading Markets & Segments in dangerous goods packaging

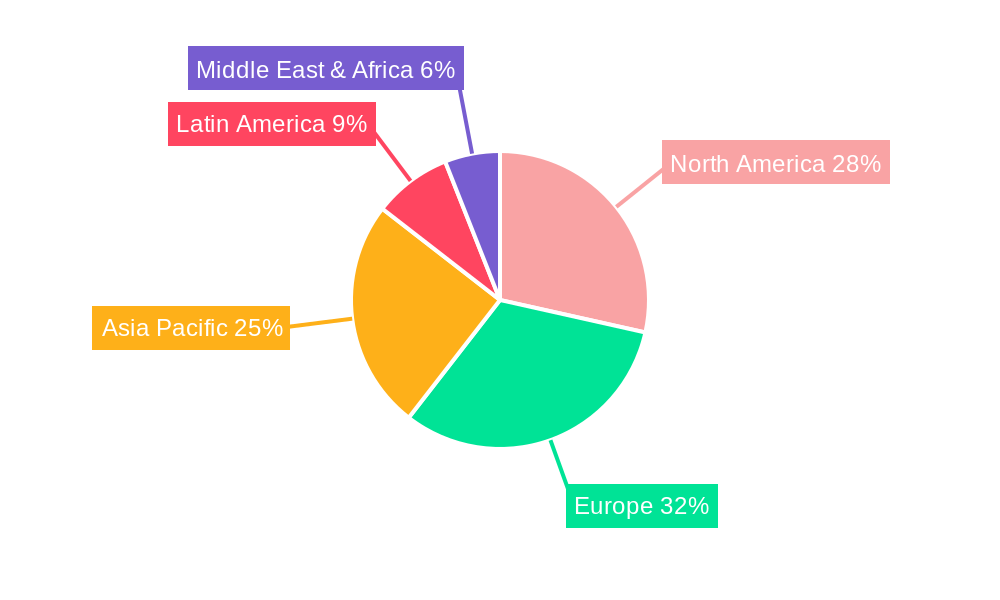

The dangerous goods packaging market is segmented by application and type, with distinct regional dominance. In terms of application, Flammable Liquids constitute the largest segment, accounting for an estimated 30% of the total market value, driven by their widespread use in industries such as petrochemicals, manufacturing, and automotive. This is closely followed by Gases and Corrosives, each representing approximately 15% of the market share. The Toxic and Infectious Substances segment, while smaller, commands a significant premium due to stringent handling and containment requirements. Within types, Medium Danger packaging represents the largest share, estimated at 55 million units, reflecting the broad spectrum of hazardous materials requiring standard compliance. High Danger packaging, though representing a smaller volume, generates substantial revenue due to its specialized design and high safety specifications, estimated at 20 million units. The Low Danger segment, comprising less hazardous materials, accounts for the remaining volume. Geographically, North America and Europe currently dominate the dangerous goods packaging market, accounting for over 60% of the global market share. Key drivers for this dominance include stringent regulatory frameworks like OSHA and REACH, a well-established industrial base, and significant investments in advanced logistics and supply chain infrastructure. Countries like the United States and Germany are at the forefront, driven by strong pharmaceutical, chemical, and aerospace industries. Asia-Pacific is emerging as a rapid growth region, fueled by expanding manufacturing capabilities, increasing chemical production, and a growing emphasis on safety standards. For instance, the economic policies in China and India, promoting domestic manufacturing of chemicals and pharmaceuticals, are directly contributing to a surge in demand for compliant dangerous goods packaging. The development of advanced transportation networks and infrastructure across these regions further supports this growth trajectory.

dangerous goods packaging Product Developments

Recent product developments in dangerous goods packaging are centered on enhancing safety, sustainability, and logistical efficiency. Innovations include the introduction of multi-layer composite drums offering superior chemical resistance and structural integrity, advanced cushioning materials to protect sensitive radioactive materials from impact, and smart packaging solutions with integrated sensors for temperature and humidity monitoring. Furthermore, there is a significant push towards the use of recycled and bio-based plastics in the manufacturing of hazardous materials packaging, aligning with global sustainability initiatives. These advancements provide a competitive advantage by offering enhanced product protection, reduced environmental footprint, and improved user experience. The market fit for these developments is strong, catering to the growing demand for safer and more responsible packaging solutions across diverse industrial applications.

Key Drivers of dangerous goods packaging Growth

The dangerous goods packaging market is propelled by several key growth drivers. Firstly, the escalating volume of global trade in chemicals, pharmaceuticals, and petrochemicals necessitates compliant and secure packaging solutions. Secondly, increasingly stringent international and national regulations for the transportation of hazardous materials mandate the use of certified and robust packaging. Thirdly, technological advancements in material science and manufacturing processes are enabling the development of lighter, stronger, and more sustainable packaging options. Finally, the growing awareness of safety and environmental risks associated with mishandled hazardous goods fuels the demand for advanced packaging solutions.

Challenges in the dangerous goods packaging Market

Despite the positive growth trajectory, the dangerous goods packaging market faces several challenges. Stringent and evolving regulatory landscapes require continuous investment in compliance and certification, which can be a significant burden, especially for smaller manufacturers. Supply chain disruptions, such as raw material shortages and logistics bottlenecks, can impact production and delivery timelines. Furthermore, intense price competition, particularly for standard packaging solutions, can squeeze profit margins. The cost associated with developing and implementing innovative, high-safety packaging can also be a barrier to widespread adoption, especially in price-sensitive markets.

Emerging Opportunities in dangerous goods packaging

Emerging opportunities in the dangerous goods packaging market are primarily driven by technological breakthroughs and strategic market expansion. The development of biodegradable and compostable hazardous materials packaging presents a significant growth avenue, catering to increasing environmental concerns. The expanding pharmaceutical industry, particularly the rise of biologics and specialized medicines, creates demand for specialized temperature-controlled and secure packaging. Furthermore, strategic partnerships between packaging manufacturers and logistics providers can lead to integrated solutions that enhance supply chain visibility and safety. The growing emphasis on e-commerce for hazardous materials also opens new avenues for direct-to-consumer packaging solutions.

Leading Players in the dangerous goods packaging Sector

- Nefab

- P&M Packing

- TEN-E Packaging Services

- ZARGES

- Air Sea Containers

- IGH Holdings

Key Milestones in dangerous goods packaging Industry

- 2019: Introduction of new UN certification standards for composite IBCs.

- 2020: Significant increase in demand for hand sanitizer packaging due to the pandemic.

- 2021: Launch of advanced tamper-evident seals for pharmaceutical dangerous goods.

- 2022: Growing adoption of sustainable packaging materials in chemical transport.

- 2023: Implementation of stricter regulations for radioactive material transport by IATA.

- 2024: Mergers and acquisitions activity increases as companies seek market consolidation.

Strategic Outlook for dangerous goods packaging Market

The strategic outlook for the dangerous goods packaging market remains highly positive, driven by continued global trade expansion and an unwavering focus on safety and sustainability. Growth accelerators include the ongoing development of innovative materials that offer enhanced protection and reduced environmental impact, such as advanced composites and biodegradable polymers. The increasing demand for specialized packaging solutions for niche hazardous materials, including pharmaceuticals and sensitive chemicals, will continue to drive market segmentation. Strategic opportunities lie in forming partnerships with logistics providers to offer end-to-end secure transport solutions and investing in smart packaging technologies for enhanced traceability. Companies that can effectively navigate regulatory complexities while championing sustainable practices are poised for significant success.

dangerous goods packaging Segmentation

-

1. Application

- 1.1. Explosives

- 1.2. Gases

- 1.3. Flammable Liquids

- 1.4. Flammable Solids

- 1.5. Oxidizing Substances and organic peroxides

- 1.6. Toxic and infectious substances

- 1.7. Radioactive materials

- 1.8. Corrosives

- 1.9. Other

-

2. Types

- 2.1. High Danger

- 2.2. Medium Danger

- 2.3. Low Danger

dangerous goods packaging Segmentation By Geography

- 1. CA

dangerous goods packaging Regional Market Share

Geographic Coverage of dangerous goods packaging

dangerous goods packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. dangerous goods packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Explosives

- 5.1.2. Gases

- 5.1.3. Flammable Liquids

- 5.1.4. Flammable Solids

- 5.1.5. Oxidizing Substances and organic peroxides

- 5.1.6. Toxic and infectious substances

- 5.1.7. Radioactive materials

- 5.1.8. Corrosives

- 5.1.9. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. High Danger

- 5.2.2. Medium Danger

- 5.2.3. Low Danger

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Nefab

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 P&M Packing

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 TEN-E Packaging Services

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 ZARGES

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Air Sea Containers

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 IGH Holdings

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.1 Nefab

List of Figures

- Figure 1: dangerous goods packaging Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: dangerous goods packaging Share (%) by Company 2025

List of Tables

- Table 1: dangerous goods packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: dangerous goods packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: dangerous goods packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: dangerous goods packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: dangerous goods packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: dangerous goods packaging Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the dangerous goods packaging?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the dangerous goods packaging?

Key companies in the market include Nefab, P&M Packing, TEN-E Packaging Services, ZARGES, Air Sea Containers, IGH Holdings.

3. What are the main segments of the dangerous goods packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "dangerous goods packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the dangerous goods packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the dangerous goods packaging?

To stay informed about further developments, trends, and reports in the dangerous goods packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence