Key Insights

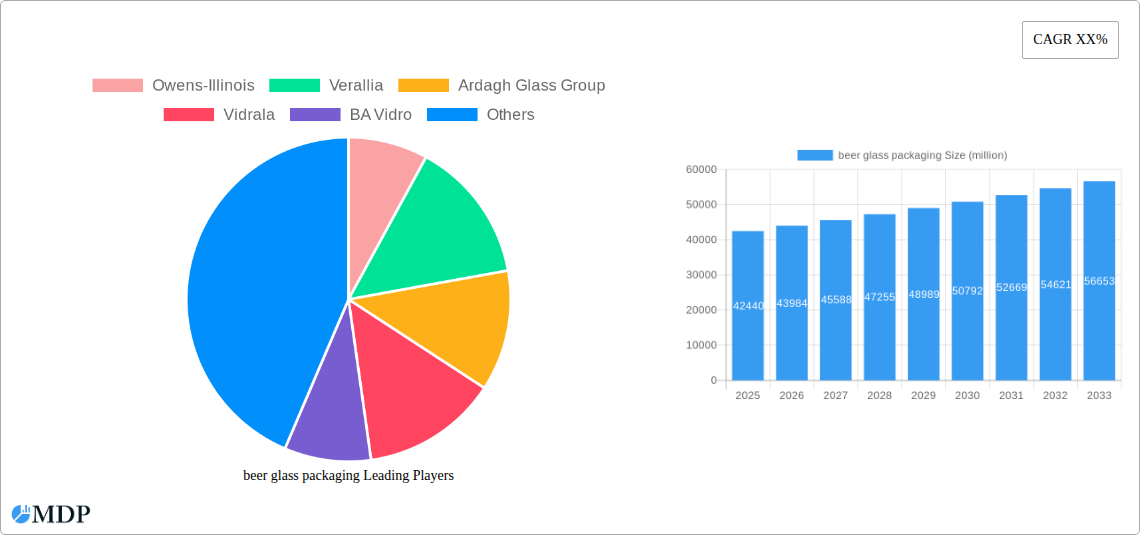

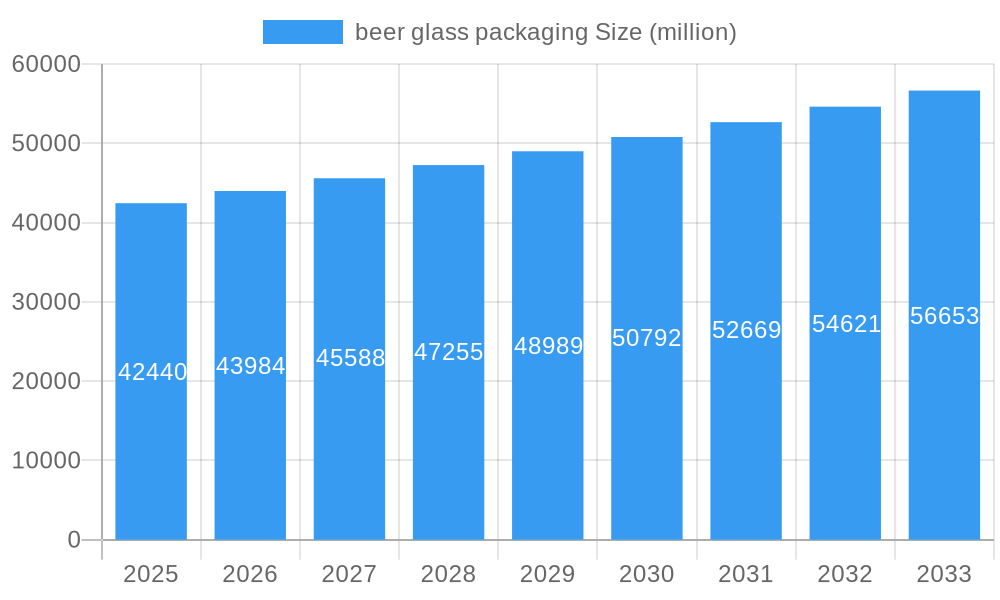

The global beer glass packaging market is poised for robust growth, projected to reach USD 42.44 billion by 2025, with an estimated Compound Annual Growth Rate (CAGR) of 3.65% during the forecast period of 2025-2033. This expansion is primarily fueled by the increasing global consumption of beer, both alcoholic and non-alcoholic variants, and a rising preference for visually appealing and sustainable packaging solutions. The demand for premium and craft beers, which often utilize distinctive glass bottle designs, is a significant driver. Furthermore, growing environmental consciousness among consumers and stricter regulations regarding plastic waste are steering the industry towards recyclable and reusable glass packaging. Key applications within this market include alcoholic beer and non-alcoholic beer, with various bottle sizes like 500ml, 650ml, and other specialized formats catering to diverse consumer preferences and product types. The market is characterized by a competitive landscape featuring prominent players such as Owens-Illinois, Verallia, and Ardagh Glass Group, who are continually innovating in terms of design, sustainability, and production efficiency to capture market share.

beer glass packaging Market Size (In Billion)

The beer glass packaging market is experiencing several influential trends and faces specific restraints that shape its trajectory. Growth is being propelled by advancements in glass manufacturing technology, leading to lighter yet more durable bottles and sophisticated design options. The increasing popularity of e-commerce for alcoholic beverages also necessitates robust and attractive glass packaging for safe and appealing delivery. However, the market is not without its challenges. Fluctuations in raw material prices, particularly for sand and soda ash, can impact production costs and profit margins. Furthermore, the transportation costs associated with glass, due to its weight and fragility, represent a significant restraint. Competition from alternative packaging materials like aluminum cans, which offer lighter weight and potentially lower transportation costs, also poses a challenge. Despite these restraints, the inherent recyclability, inertness, and perceived premium quality of glass packaging for beer are expected to sustain its market dominance and drive its continued growth.

beer glass packaging Company Market Share

Here is an SEO-optimized and engaging report description for beer glass packaging, incorporating high-traffic keywords and adhering to your specified structure and content requirements.

This in-depth report offers a critical analysis of the global beer glass packaging market, spanning the historical period of 2019–2024, the base and estimated year of 2025, and a detailed forecast from 2025 to 2033. With an estimated market size projected to reach $25.8 billion in 2025 and forecast to grow to $32.9 billion by 2033, at a compound annual growth rate (CAGR) of 3.1%, this report provides indispensable insights for stakeholders seeking to navigate this dynamic industry. We delve into market concentration, innovation drivers, regulatory landscapes, and evolving end-user trends, offering actionable intelligence for strategic decision-making. Explore cutting-edge product developments, understand key growth drivers, and identify challenges and emerging opportunities within this billion-dollar sector.

beer glass packaging Market Dynamics & Concentration

The beer glass packaging market, valued at an estimated $25.8 billion in 2025, exhibits a moderate to high concentration, with major players like Owens-Illinois, Verallia, and Ardagh Glass Group holding significant market shares. Innovation in this sector is largely driven by the demand for sustainable packaging solutions, enhanced product aesthetics, and improved durability. Regulatory frameworks, particularly those concerning environmental impact and recycling initiatives, are increasingly shaping manufacturing processes and material choices. Product substitutes, such as aluminum cans and PET bottles, present a constant competitive challenge, necessitating continuous innovation in glass packaging to maintain market appeal. End-user trends are leaning towards premiumization, with consumers seeking visually appealing and functional glass bottles that enhance the perceived value of the beer. Mergers and acquisitions (M&A) activities, with approximately 35 notable deals recorded during the historical period, indicate a strategic consolidation among leading manufacturers aiming to expand their global footprint and technological capabilities.

beer glass packaging Industry Trends & Analysis

The beer glass packaging industry is experiencing robust growth, propelled by a confluence of factors that underscore its enduring appeal and evolving capabilities. The rising global consumption of beer, particularly within emerging economies, serves as a primary market growth driver, creating sustained demand for reliable and aesthetically pleasing packaging solutions. Technological disruptions are playing a pivotal role, with advancements in glass manufacturing leading to lighter yet stronger bottles, reduced energy consumption during production, and improved design flexibility. This not only addresses cost pressures but also aligns with growing environmental consciousness among consumers. Consumer preferences are increasingly sophisticated, with a growing appreciation for the sensory experience that glass packaging offers – from the sound of a bottle opening to the visual presentation on a shelf. This preference for premiumization in beer consumption directly translates into a higher demand for high-quality, well-designed glass bottles. Competitive dynamics within the industry are characterized by a strategic focus on sustainability, cost optimization, and product differentiation. Companies are investing heavily in research and development to create innovative glass solutions that minimize environmental impact, such as increased recycled content and energy-efficient production methods. Market penetration is steadily increasing, with glass packaging retaining a dominant share in the premium beer segment and making inroads into other categories through innovative product offerings. The global beer glass packaging market is projected to witness a CAGR of 3.1% from 2025 to 2033, reflecting its resilient growth trajectory in response to evolving market demands and technological advancements.

Leading Markets & Segments in beer glass packaging

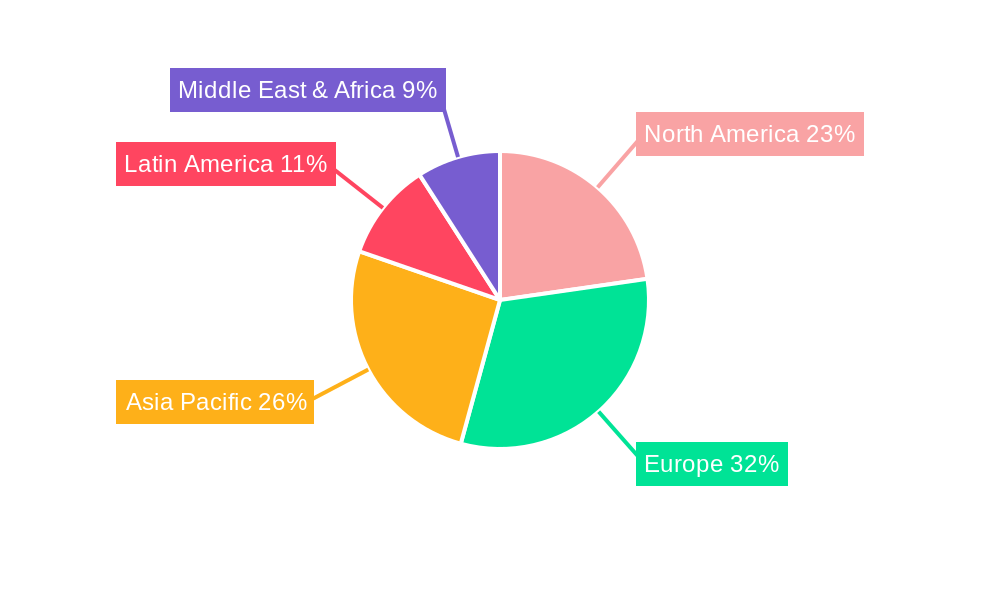

The beer glass packaging market demonstrates distinct regional leadership and segment dominance, driven by a combination of economic policies, infrastructural development, and prevailing consumer preferences. North America and Europe currently lead in terms of market value, owing to mature beer markets with a strong emphasis on premium and craft beers, which traditionally favor glass packaging. However, the Asia-Pacific region is emerging as the fastest-growing market, fueled by increasing disposable incomes, rapid urbanization, and a burgeoning middle class with a growing appetite for alcoholic beverages.

Application Dominance:

- Alcohol Beer: This segment constitutes the largest share of the beer glass packaging market, driven by the sheer volume of global beer production and consumption. The ongoing trend towards premiumization and craft beers within this category further solidifies its leadership.

- Non-alcoholic Beer: While currently a smaller segment, the non-alcoholic beer market is experiencing significant growth. As consumer health consciousness rises and the stigma surrounding non-alcoholic options diminishes, demand for specialized and attractive glass packaging in this segment is expected to surge.

Type Dominance:

- 650ml Bottles: This size is a key workhorse in many markets, offering a balance between consumption volume and shelf presence. Its versatility for various beer styles, from lagers to stouts, contributes to its widespread adoption.

- 500ml Bottles: The 500ml format is increasingly popular, particularly for single-serving consumption and in markets where portion control is a consideration. It offers a premium feel while remaining convenient.

- Other (e.g., 330ml, 750ml, growlers): This diverse category captures specialized market needs. Smaller formats cater to a growing trend of single-serving options and trial packs, while larger formats like 750ml bottles are favored for premium and limited-edition releases. Growlers and other unique vessel shapes are crucial for the craft beer segment, allowing breweries to offer unique branding and customer experiences.

The dominance of these segments is further bolstered by strategic investments in manufacturing capabilities, efficient distribution networks, and marketing initiatives that highlight the quality and sustainability of glass packaging. Economic policies supporting local manufacturing and environmental regulations favoring recyclable materials also play a crucial role in shaping market preferences and driving the adoption of glass.

beer glass packaging Product Developments

Recent product innovations in beer glass packaging are centered on sustainability, design customization, and enhanced user experience. Manufacturers are increasingly incorporating higher percentages of recycled glass, reducing the carbon footprint of their products. Lightweighting techniques are being employed to create thinner yet stronger bottles, leading to logistical efficiencies and reduced material costs without compromising on structural integrity. Furthermore, advanced decoration techniques, including digital printing and etching, are allowing breweries to create highly customized and visually striking packaging that enhances brand identity and shelf appeal. These developments provide a competitive advantage by meeting the evolving demands of both brewers and end consumers for eco-friendly, aesthetically pleasing, and functional packaging solutions.

Key Drivers of beer glass packaging Growth

The beer glass packaging market's growth is propelled by several interconnected factors. Rising global beer consumption, particularly in emerging economies, directly translates to increased demand for packaging. The premiumization trend in the beer industry, where consumers associate glass with higher quality and a superior drinking experience, is a significant accelerator. Technological advancements in glass manufacturing, leading to lighter, stronger, and more customizable bottles, address cost and aesthetic demands. Furthermore, growing consumer awareness and preference for sustainable and recyclable packaging materials strongly favor glass. Government initiatives and regulations promoting circular economy principles also act as a catalyst for the adoption of glass packaging.

Challenges in the beer glass packaging Market

Despite its robust growth, the beer glass packaging market faces several significant challenges. Intense competition from alternative packaging materials, such as aluminum cans and PET bottles, which often offer lower price points and lighter shipping weights, poses a continuous threat. Volatile raw material costs, particularly for cullet (recycled glass) and energy, can impact manufacturing profitability. Stringent environmental regulations and the need for significant investment in updated production facilities to meet these standards can be a barrier. Additionally, logistical challenges and costs associated with the weight and fragility of glass can affect supply chain efficiency and add to overall expenses.

Emerging Opportunities in beer glass packaging

The beer glass packaging market is ripe with emerging opportunities driven by innovative strategies and evolving consumer behaviors. A significant catalyst for long-term growth lies in the increasing demand for sustainable packaging solutions. Manufacturers who can further enhance the use of recycled content, reduce energy consumption in production, and implement effective take-back schemes will gain a competitive edge. Strategic partnerships between glass manufacturers and breweries can lead to co-developed packaging designs that enhance brand storytelling and consumer engagement. Furthermore, the expansion of the non-alcoholic beer segment presents a substantial opportunity for glass packaging to capture a growing market share with specialized and attractive bottle designs. The rise of the craft beer movement also continues to drive demand for unique and aesthetically appealing glass formats, encouraging customization and innovation.

Leading Players in the beer glass packaging Sector

- Owens-Illinois

- Verallia

- Ardagh Glass Group

- Vidrala

- BA Vidro

- Vetropack

- Wiegand Glass

- Zignago Vetro

- Stölzle Glas Group

- HNGIL

- Nihon Yamamura

- Allied Glass

- Bormioli Luigi

Key Milestones in beer glass packaging Industry

- 2019: Increased focus on lightweighting glass bottles to reduce transportation costs and environmental impact.

- 2020: Significant investment in advanced decoration techniques for enhanced branding and consumer appeal.

- 2021: Growing adoption of higher recycled content in glass production driven by sustainability initiatives.

- 2022: Mergers and acquisitions accelerate market consolidation and expansion of global manufacturing capabilities.

- 2023: Innovations in glass barrier properties to improve shelf life for various beer types.

- 2024: Development of smart packaging features integrated into glass bottles for enhanced traceability and consumer interaction.

Strategic Outlook for beer glass packaging Market

The strategic outlook for the beer glass packaging market remains highly positive, driven by a sustained demand for premium and sustainable products. Growth accelerators include continued innovation in lightweighting and increased recycled content, aligning with global environmental mandates and consumer preferences. The expanding non-alcoholic beer segment and the persistent appeal of glass for craft and premium beers will ensure sustained market penetration. Strategic opportunities lie in forging deeper collaborations with breweries for bespoke packaging solutions and investing in advanced manufacturing technologies that enhance efficiency and reduce environmental impact. The market is poised for continued expansion as it adapts to evolving consumer tastes and embraces a circular economy model.

beer glass packaging Segmentation

-

1. Application

- 1.1. Alcohol Beer

- 1.2. Non-alcoholic Beer

-

2. Types

- 2.1. 500ml

- 2.2. 650ml

- 2.3. Other

beer glass packaging Segmentation By Geography

- 1. CA

beer glass packaging Regional Market Share

Geographic Coverage of beer glass packaging

beer glass packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.65% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. beer glass packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Alcohol Beer

- 5.1.2. Non-alcoholic Beer

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 500ml

- 5.2.2. 650ml

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Owens-Illinois

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Verallia

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Ardagh Glass Group

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Vidrala

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 BA Vidro

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Vetropack

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Wiegand Glass

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Zignago Vetro

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Stölzle Glas Group

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 HNGIL

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Nihon Yamamura

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Allied Glass

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Bormioli Luigi

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 Owens-Illinois

List of Figures

- Figure 1: beer glass packaging Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: beer glass packaging Share (%) by Company 2025

List of Tables

- Table 1: beer glass packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: beer glass packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: beer glass packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: beer glass packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: beer glass packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: beer glass packaging Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the beer glass packaging?

The projected CAGR is approximately 3.65%.

2. Which companies are prominent players in the beer glass packaging?

Key companies in the market include Owens-Illinois, Verallia, Ardagh Glass Group, Vidrala, BA Vidro, Vetropack, Wiegand Glass, Zignago Vetro, Stölzle Glas Group, HNGIL, Nihon Yamamura, Allied Glass, Bormioli Luigi.

3. What are the main segments of the beer glass packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "beer glass packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the beer glass packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the beer glass packaging?

To stay informed about further developments, trends, and reports in the beer glass packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence