Key Insights

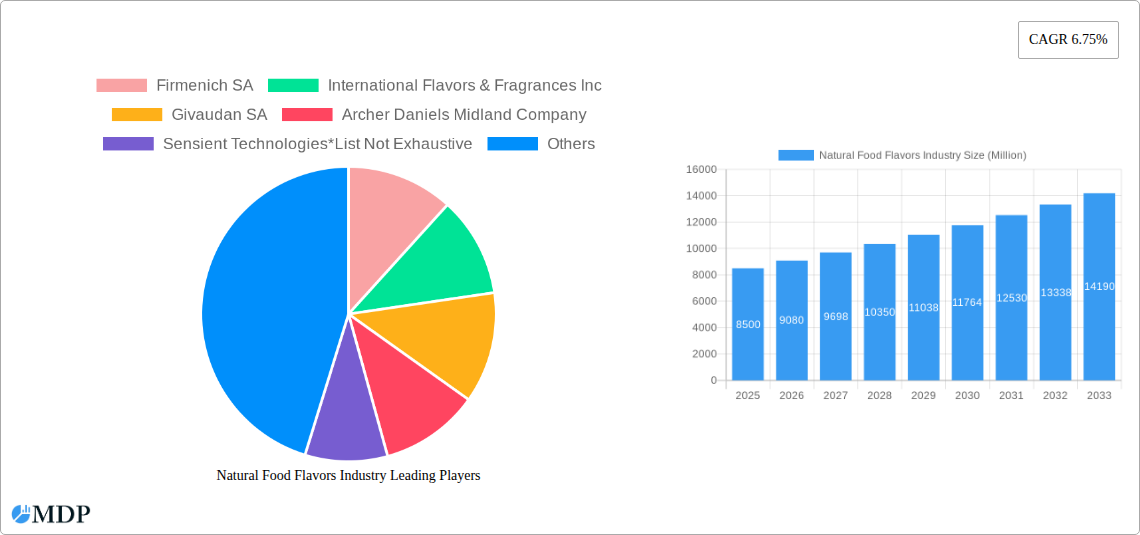

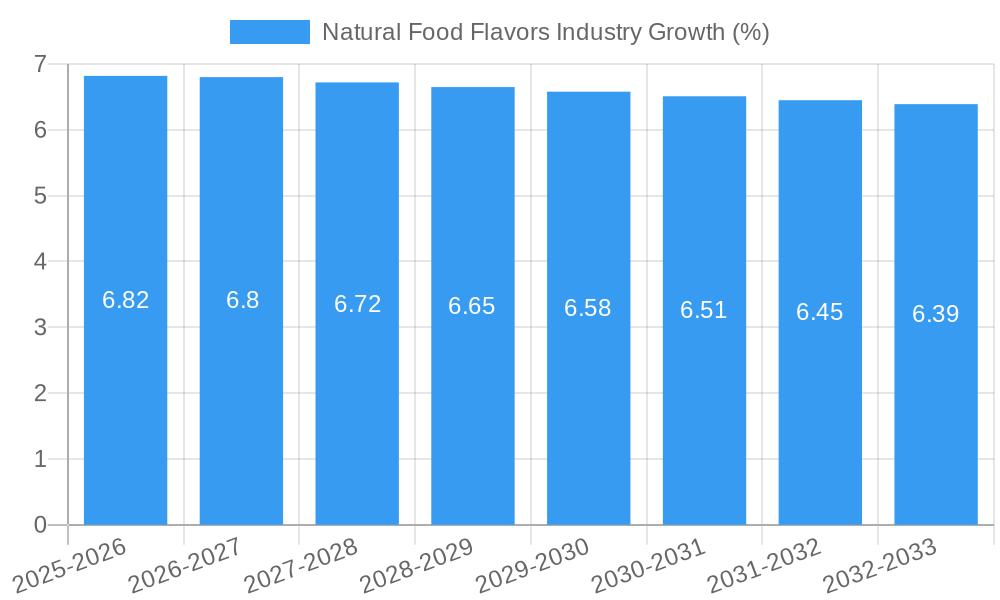

The Natural Food Flavors industry is poised for significant expansion, projected to reach a substantial market size of approximately $XX million in 2025. Driven by a burgeoning consumer demand for clean-label products and a heightened awareness of the health implications associated with artificial additives, this market is expected to witness a robust Compound Annual Growth Rate (CAGR) of 6.75% throughout the forecast period of 2025-2033. Key growth enablers include ongoing innovation in flavor extraction and encapsulation technologies, allowing for more authentic and stable natural flavor profiles. Furthermore, the increasing adoption of natural flavors across a diverse range of applications, from baked goods and confectionery to beverages and savory products, underscores its growing importance in the food and beverage sector. The industry's trajectory is further bolstered by rising disposable incomes in developing economies, leading to a greater willingness among consumers to opt for premium, natural food ingredients.

The market's dynamism is characterized by several prevailing trends. A notable trend is the surge in demand for specific flavor categories like fruit and vegetable-based natural flavors, reflecting a global shift towards healthier eating habits. Moreover, the expansion of the plant-based food sector is a significant catalyst, creating a substantial need for natural flavors that mimic traditional tastes. Despite the optimistic outlook, certain restraints warrant attention. The relatively higher cost of natural flavor production compared to synthetic alternatives can pose a challenge, particularly for price-sensitive markets. Supply chain complexities and seasonal variations in raw material availability can also impact consistent production. Nevertheless, strategic investments in research and development by leading companies like Firmenich SA, International Flavors & Fragrances Inc., and Givaudan SA are continuously addressing these challenges by optimizing sourcing and production processes, ensuring a sustained growth trajectory for the Natural Food Flavors industry.

Here's the SEO-optimized, engaging report description for the Natural Food Flavors Industry, designed for maximum visibility and stakeholder attraction:

Unlocking the Future of Taste: Natural Food Flavors Industry Market Analysis, Trends, and Forecasts (2019-2033)

This comprehensive report provides an in-depth analysis of the burgeoning Natural Food Flavors Industry, offering critical insights into market dynamics, growth trajectories, and strategic opportunities through 2033. Driven by escalating consumer demand for clean-label products and a growing preference for natural ingredients, the natural food flavors market is experiencing unprecedented expansion. This research delves into the intricate ecosystem of natural food flavorings, covering key applications, regional dominance, technological innovations, and the competitive landscape. With actionable data and expert analysis, this report is an indispensable resource for ingredient manufacturers, food and beverage companies, R&D professionals, market strategists, and investors seeking to capitalize on the evolving tastes of global consumers.

Natural Food Flavors Industry Market Dynamics & Concentration

The Natural Food Flavors Industry is characterized by a dynamic interplay of innovation, regulatory oversight, and shifting consumer preferences. Market concentration is moderately fragmented, with key players like Firmenich SA, International Flavors & Fragrances Inc, and Givaudan SA holding significant market share, estimated at over 60% collectively. However, the emergence of niche players and increased R&D investments are fostering greater competition. Innovation drivers are primarily centered on developing novel extraction techniques, enhancing flavor profiles from botanical sources, and meeting stringent clean-label demands. Regulatory frameworks, particularly concerning ingredient sourcing, labeling, and permissible usage levels, are increasingly shaping market entry and product development strategies. Product substitutes, while limited for authentic natural flavors, are primarily other natural ingredients with inherent flavoring properties or, in some cases, highly purified synthetic alternatives. End-user trends are overwhelmingly skewed towards natural, sustainable, and traceable ingredients, prompting manufacturers to invest heavily in supply chain transparency and responsible sourcing. Mergers and acquisitions (M&A) activities remain a significant feature, with an estimated xx deals in the historical period (2019-2024) valued at an aggregate of over $10 Million, signaling consolidation and strategic expansion among leading entities. The market share of natural food flavors within the broader flavorings industry is projected to reach xx% by 2033.

Natural Food Flavors Industry Industry Trends & Analysis

The Natural Food Flavors Industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033. This significant expansion is propelled by a confluence of powerful market growth drivers. The most prominent is the unyielding global consumer shift towards healthier, natural, and "free-from" food options. Consumers are increasingly scrutinizing ingredient lists, actively seeking out products free from artificial colors, flavors, and preservatives. This trend is amplified by greater awareness of the potential health implications associated with synthetic additives. Technological disruptions are also playing a pivotal role. Advancements in biotechnology, including fermentation and enzymatic processes, are enabling the cost-effective production of complex natural flavors, expanding the range of available ingredients and enhancing their consistency. Furthermore, innovative extraction technologies, such as supercritical fluid extraction and ultrasound-assisted extraction, are yielding higher yields of potent and authentic flavor compounds from diverse natural sources like fruits, vegetables, herbs, and spices.

Consumer preferences are evolving beyond just "natural" to encompass "authentic," "artisanal," and "ethically sourced" attributes. This demand for transparency and provenance is driving manufacturers to invest in traceable supply chains and support sustainable agricultural practices. The competitive dynamics within the industry are intensifying. While established giants continue to innovate and expand, a new wave of agile startups and specialized ingredient suppliers are emerging, often focusing on specific flavor profiles or unique botanical sources. This fosters a competitive environment that benefits end-users through increased choice and improved product offerings. Market penetration of natural food flavors in developed economies is already substantial, with estimates at xx%, and is rapidly growing in emerging markets as disposable incomes rise and consumer awareness increases. The perceived health benefits, coupled with enhanced taste experiences, are solidifying the market position of natural food flavors as a preferred alternative to artificial counterparts. The market size for natural food flavors is estimated to reach $XX Million in 2025, with strong projections for sustained growth throughout the forecast period.

Leading Markets & Segments in Natural Food Flavors Industry

The Beverages segment is the dominant force in the Natural Food Flavors Industry, accounting for an estimated xx% of the total market share in 2025. Within this segment, both alcoholic and non-alcoholic beverages contribute significantly to the demand for natural flavorings. The rapid growth of functional beverages, ready-to-drink (RTD) teas and coffees, and premium juices and smoothies are key drivers. Consumers are actively seeking natural flavor profiles to enhance these products, moving away from sugary, artificially flavored alternatives.

- Key Drivers for Beverage Dominance:

- Health & Wellness Trends: Increased demand for natural sweeteners and flavor enhancers in low-calorie and functional beverages.

- Clean Label Movement: Consumers prefer natural flavors in beverages to avoid artificial ingredients.

- Innovation in RTD Categories: The proliferation of ready-to-drink alcoholic and non-alcoholic beverages offers a vast canvas for natural flavor application.

- Premiumization: A growing willingness among consumers to pay more for beverages with perceived higher quality, natural ingredients.

The Bakery and Confectionery segments are also significant contributors, driven by the persistent demand for indulgent yet health-conscious treats. The rise of artisanal bakeries and the growing popularity of premium chocolates and candies utilizing natural flavorings are key indicators. The Dairy and Desserts sector is experiencing substantial growth, fueled by the demand for natural fruit flavors in yogurts, ice creams, and plant-based dairy alternatives.

The Savory and Snacks segment is witnessing remarkable expansion, with natural flavors being crucial for enhancing the taste of chips, extruded snacks, and meat alternatives. The Sauces, Soups, and Seasonings category is another robust area, as manufacturers seek to replicate authentic, home-cooked taste profiles using natural ingredients.

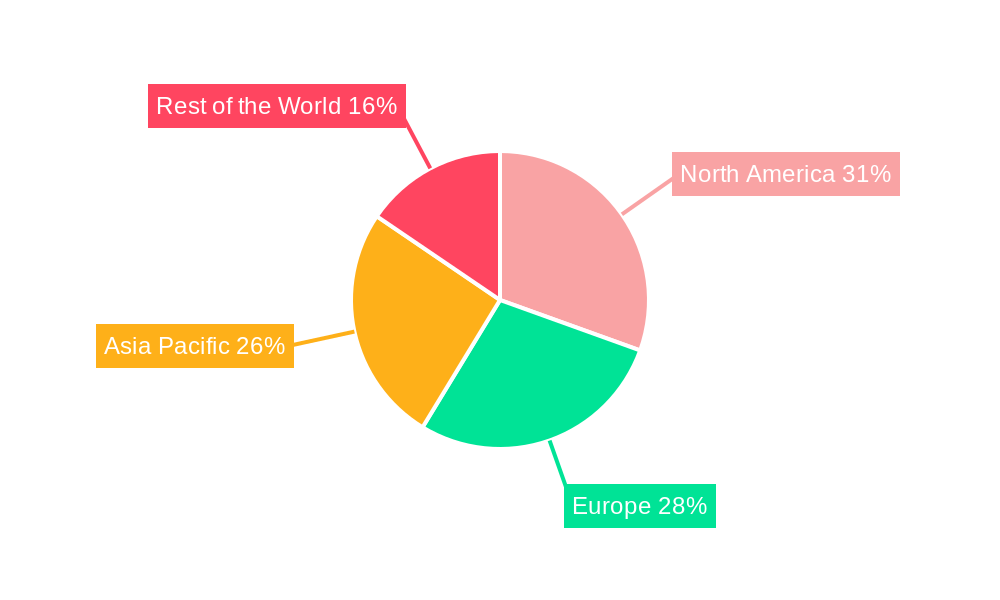

Geographically, North America and Europe currently lead the market, driven by high consumer awareness and stringent regulations favoring natural ingredients. However, the Asia-Pacific region is emerging as a high-growth market, fueled by rising disposable incomes, urbanization, and an increasing adoption of Western dietary habits alongside a growing appreciation for natural and indigenous flavors. Economic policies supporting food innovation and infrastructure development in logistics and cold chain management are crucial for market expansion across all regions.

Natural Food Flavors Industry Product Developments

Product innovations in the Natural Food Flavors Industry are increasingly focused on delivering authentic taste experiences while adhering to clean-label principles. Manufacturers are developing concentrated natural flavor extracts from a wider array of botanical sources, including exotic fruits, rare spices, and medicinal herbs, catering to the demand for unique and exotic flavor profiles. Technological advancements in encapsulation and spray-drying are improving the stability, solubility, and shelf-life of these natural flavors, making them more viable for a broader range of applications. Key competitive advantages lie in the ability to offer sustainably sourced, non-GMO, and allergen-free natural flavor solutions that resonate with health-conscious consumers. The market is witnessing a trend towards natural flavor blends that mimic complex taste profiles, providing a cost-effective and consistent solution for food and beverage manufacturers.

Key Drivers of Natural Food Flavors Industry Growth

Several key factors are propelling the growth of the Natural Food Flavors Industry. Technologically, advancements in extraction and purification methods are enabling the isolation of more potent and diverse natural flavor compounds. Economically, rising disposable incomes, particularly in emerging markets, are increasing consumer spending on premium and health-conscious food products. Regulatory frameworks, while sometimes challenging, are increasingly mandating clearer labeling and prioritizing natural ingredients, thereby creating a more favorable market environment. The growing consumer awareness regarding the health benefits and perceived safety of natural ingredients over artificial alternatives is a paramount driver. Furthermore, the sustained innovation by flavor houses in developing novel and exciting natural flavor profiles is crucial for market expansion.

Challenges in the Natural Food Flavors Industry Market

Despite the robust growth, the Natural Food Flavors Industry faces several challenges. Regulatory hurdles related to ingredient sourcing, permissible usage levels, and international harmonization of standards can complicate market entry and product development. Supply chain issues, including the seasonality of raw materials, potential crop failures due to climate change, and geopolitical instability, can lead to price volatility and availability concerns for key natural ingredients. Competitive pressures from both established players and new entrants, coupled with the high cost of R&D for novel natural flavor extraction and development, also present significant barriers. Moreover, achieving consistent flavor profiles and scalability with certain natural ingredients can be technically demanding, impacting production efficiency and overall cost-effectiveness.

Emerging Opportunities in Natural Food Flavors Industry

Emerging opportunities in the Natural Food Flavors Industry are vast and multifaceted. Technological breakthroughs in fermentation and cell-based cultivation offer promising avenues for producing complex natural flavors in a sustainable and scalable manner, independent of agricultural variables. Strategic partnerships between flavor houses, ingredient suppliers, and food manufacturers are crucial for co-creating innovative product formulations that meet evolving consumer demands. Market expansion into untapped geographical regions, particularly in developing economies where the clean-label trend is gaining traction, presents significant growth potential. Furthermore, the development of natural flavors with functional benefits, such as those offering health-promoting properties or masking undesirable off-notes in plant-based alternatives, represents a significant untapped market.

Leading Players in the Natural Food Flavors Industry Sector

- Firmenich SA

- International Flavors & Fragrances Inc

- Givaudan SA

- Archer Daniels Midland Company

- Sensient Technologies

- BASF SE

- Kerry Group PLC

- Corbion NV

Key Milestones in Natural Food Flavors Industry Industry

- 2020: Increased consumer demand for natural ingredients surges following global health events, driving R&D in clean-label solutions.

- 2021: Major flavor houses invest heavily in biotech and fermentation technologies for sustainable natural flavor production.

- 2022: Stringent new labeling regulations implemented in key markets, further boosting demand for verified natural flavors.

- 2023: Significant M&A activity as larger players acquire specialized natural ingredient startups to expand portfolios.

- 2024 (Estimated): Launch of novel natural flavor compounds derived from upcycled food waste streams by several pioneering companies.

Strategic Outlook for Natural Food Flavors Industry Market

The strategic outlook for the Natural Food Flavors Industry remains exceptionally positive, driven by the enduring consumer preference for natural, healthy, and transparent food products. Growth accelerators will stem from continued investment in sustainable sourcing and innovative extraction technologies, enabling a wider palette of authentic natural flavors. The expansion of plant-based food alternatives will continue to fuel demand for sophisticated natural flavor solutions that replicate traditional taste profiles. Manufacturers that can effectively navigate evolving regulatory landscapes, ensure supply chain resilience, and foster strong partnerships with end-users will be best positioned for long-term success and market leadership. The industry is poised for sustained innovation, leading to richer, more diverse, and healthier flavor experiences for consumers worldwide.

Natural Food Flavors Industry Segmentation

-

1. Application Type

- 1.1. Bakery

- 1.2. Confectionery

- 1.3. Dairy and Desserts

-

1.4. Beverages

- 1.4.1. Alcoholic

- 1.4.2. Non-alcoholic

- 1.5. Savory and Snacks

- 1.6. Meat and Meat Products

- 1.7. Sauces, Soups, and Seasonings

- 1.8. Other Applications

Natural Food Flavors Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Italy

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East

Natural Food Flavors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.75% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Demand for Convenient Ready-to-Eat Food Products; Growing Affinity Toward Ethnic and Organic Frozen Ready Meals

- 3.3. Market Restrains

- 3.3.1. Rising Concerns Over Food Safety and Quality

- 3.4. Market Trends

- 3.4.1. Resurgance of Natural Food Products Among Consumers

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 5.1.1. Bakery

- 5.1.2. Confectionery

- 5.1.3. Dairy and Desserts

- 5.1.4. Beverages

- 5.1.4.1. Alcoholic

- 5.1.4.2. Non-alcoholic

- 5.1.5. Savory and Snacks

- 5.1.6. Meat and Meat Products

- 5.1.7. Sauces, Soups, and Seasonings

- 5.1.8. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 6. North America Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application Type

- 6.1.1. Bakery

- 6.1.2. Confectionery

- 6.1.3. Dairy and Desserts

- 6.1.4. Beverages

- 6.1.4.1. Alcoholic

- 6.1.4.2. Non-alcoholic

- 6.1.5. Savory and Snacks

- 6.1.6. Meat and Meat Products

- 6.1.7. Sauces, Soups, and Seasonings

- 6.1.8. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Application Type

- 7. Europe Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application Type

- 7.1.1. Bakery

- 7.1.2. Confectionery

- 7.1.3. Dairy and Desserts

- 7.1.4. Beverages

- 7.1.4.1. Alcoholic

- 7.1.4.2. Non-alcoholic

- 7.1.5. Savory and Snacks

- 7.1.6. Meat and Meat Products

- 7.1.7. Sauces, Soups, and Seasonings

- 7.1.8. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Application Type

- 8. Asia Pacific Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application Type

- 8.1.1. Bakery

- 8.1.2. Confectionery

- 8.1.3. Dairy and Desserts

- 8.1.4. Beverages

- 8.1.4.1. Alcoholic

- 8.1.4.2. Non-alcoholic

- 8.1.5. Savory and Snacks

- 8.1.6. Meat and Meat Products

- 8.1.7. Sauces, Soups, and Seasonings

- 8.1.8. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Application Type

- 9. Rest of the World Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application Type

- 9.1.1. Bakery

- 9.1.2. Confectionery

- 9.1.3. Dairy and Desserts

- 9.1.4. Beverages

- 9.1.4.1. Alcoholic

- 9.1.4.2. Non-alcoholic

- 9.1.5. Savory and Snacks

- 9.1.6. Meat and Meat Products

- 9.1.7. Sauces, Soups, and Seasonings

- 9.1.8. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Application Type

- 10. North America Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 United States

- 10.1.2 Canada

- 10.1.3 Mexico

- 11. Europe Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 Germany

- 11.1.2 United Kingdom

- 11.1.3 France

- 11.1.4 Spain

- 11.1.5 Italy

- 11.1.6 Spain

- 11.1.7 Belgium

- 11.1.8 Netherland

- 11.1.9 Nordics

- 11.1.10 Rest of Europe

- 12. Asia Pacific Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 China

- 12.1.2 Japan

- 12.1.3 India

- 12.1.4 South Korea

- 12.1.5 Southeast Asia

- 12.1.6 Australia

- 12.1.7 Indonesia

- 12.1.8 Phillipes

- 12.1.9 Singapore

- 12.1.10 Thailandc

- 12.1.11 Rest of Asia Pacific

- 13. South America Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 Brazil

- 13.1.2 Argentina

- 13.1.3 Peru

- 13.1.4 Chile

- 13.1.5 Colombia

- 13.1.6 Ecuador

- 13.1.7 Venezuela

- 13.1.8 Rest of South America

- 14. Middle East & Africa Natural Food Flavors Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 UAE

- 14.1.2 South Africa

- 14.1.3 Saudi Arabia

- 14.1.4 Rest of MEA

- 15. Competitive Analysis

- 15.1. Global Market Share Analysis 2024

- 15.2. Company Profiles

- 15.2.1 Firmenich SA

- 15.2.1.1. Overview

- 15.2.1.2. Products

- 15.2.1.3. SWOT Analysis

- 15.2.1.4. Recent Developments

- 15.2.1.5. Financials (Based on Availability)

- 15.2.2 International Flavors & Fragrances Inc

- 15.2.2.1. Overview

- 15.2.2.2. Products

- 15.2.2.3. SWOT Analysis

- 15.2.2.4. Recent Developments

- 15.2.2.5. Financials (Based on Availability)

- 15.2.3 Givaudan SA

- 15.2.3.1. Overview

- 15.2.3.2. Products

- 15.2.3.3. SWOT Analysis

- 15.2.3.4. Recent Developments

- 15.2.3.5. Financials (Based on Availability)

- 15.2.4 Archer Daniels Midland Company

- 15.2.4.1. Overview

- 15.2.4.2. Products

- 15.2.4.3. SWOT Analysis

- 15.2.4.4. Recent Developments

- 15.2.4.5. Financials (Based on Availability)

- 15.2.5 Sensient Technologies*List Not Exhaustive

- 15.2.5.1. Overview

- 15.2.5.2. Products

- 15.2.5.3. SWOT Analysis

- 15.2.5.4. Recent Developments

- 15.2.5.5. Financials (Based on Availability)

- 15.2.6 BASF SE

- 15.2.6.1. Overview

- 15.2.6.2. Products

- 15.2.6.3. SWOT Analysis

- 15.2.6.4. Recent Developments

- 15.2.6.5. Financials (Based on Availability)

- 15.2.7 Kerry Group PLC

- 15.2.7.1. Overview

- 15.2.7.2. Products

- 15.2.7.3. SWOT Analysis

- 15.2.7.4. Recent Developments

- 15.2.7.5. Financials (Based on Availability)

- 15.2.8 Corbion NV

- 15.2.8.1. Overview

- 15.2.8.2. Products

- 15.2.8.3. SWOT Analysis

- 15.2.8.4. Recent Developments

- 15.2.8.5. Financials (Based on Availability)

- 15.2.1 Firmenich SA

List of Figures

- Figure 1: Global Natural Food Flavors Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: South America Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East & Africa Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East & Africa Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Natural Food Flavors Industry Revenue (Million), by Application Type 2024 & 2032

- Figure 13: North America Natural Food Flavors Industry Revenue Share (%), by Application Type 2024 & 2032

- Figure 14: North America Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: North America Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Natural Food Flavors Industry Revenue (Million), by Application Type 2024 & 2032

- Figure 17: Europe Natural Food Flavors Industry Revenue Share (%), by Application Type 2024 & 2032

- Figure 18: Europe Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: Europe Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific Natural Food Flavors Industry Revenue (Million), by Application Type 2024 & 2032

- Figure 21: Asia Pacific Natural Food Flavors Industry Revenue Share (%), by Application Type 2024 & 2032

- Figure 22: Asia Pacific Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Asia Pacific Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Rest of the World Natural Food Flavors Industry Revenue (Million), by Application Type 2024 & 2032

- Figure 25: Rest of the World Natural Food Flavors Industry Revenue Share (%), by Application Type 2024 & 2032

- Figure 26: Rest of the World Natural Food Flavors Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Rest of the World Natural Food Flavors Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Natural Food Flavors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Natural Food Flavors Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 3: Global Natural Food Flavors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: United States Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Canada Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Mexico Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Germany Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: France Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Spain Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Belgium Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Netherland Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Nordics Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Rest of Europe Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: China Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Japan Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: India Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: South Korea Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Southeast Asia Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Australia Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Indonesia Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Phillipes Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Singapore Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Thailandc Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of Asia Pacific Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: Brazil Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Argentina Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Peru Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Chile Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Colombia Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Ecuador Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Venezuela Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Rest of South America Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 41: UAE Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: South Africa Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Saudi Arabia Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Rest of MEA Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Global Natural Food Flavors Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 46: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 47: United States Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Canada Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: Mexico Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of North America Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Global Natural Food Flavors Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 52: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 53: Germany Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: United Kingdom Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: France Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: Spain Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: Italy Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: Rest of Europe Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: Global Natural Food Flavors Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 60: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 61: China Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 62: Japan Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 63: India Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 64: Australia Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Rest of Asia Pacific Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Global Natural Food Flavors Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 67: Global Natural Food Flavors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 68: South America Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 69: Middle East Natural Food Flavors Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Natural Food Flavors Industry?

The projected CAGR is approximately 6.75%.

2. Which companies are prominent players in the Natural Food Flavors Industry?

Key companies in the market include Firmenich SA, International Flavors & Fragrances Inc, Givaudan SA, Archer Daniels Midland Company, Sensient Technologies*List Not Exhaustive, BASF SE, Kerry Group PLC, Corbion NV.

3. What are the main segments of the Natural Food Flavors Industry?

The market segments include Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Demand for Convenient Ready-to-Eat Food Products; Growing Affinity Toward Ethnic and Organic Frozen Ready Meals.

6. What are the notable trends driving market growth?

Resurgance of Natural Food Products Among Consumers.

7. Are there any restraints impacting market growth?

Rising Concerns Over Food Safety and Quality.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Natural Food Flavors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Natural Food Flavors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Natural Food Flavors Industry?

To stay informed about further developments, trends, and reports in the Natural Food Flavors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence