Key Insights

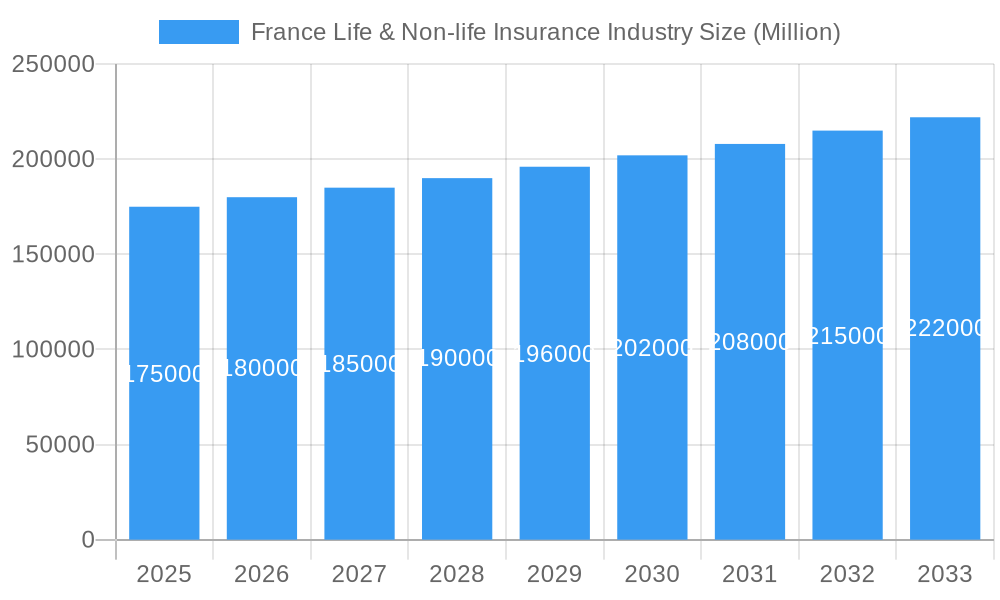

The French life and non-life insurance market is projected for significant expansion, with an estimated market size of 291.04 billion by 2025, and is anticipated to grow at a Compound Annual Growth Rate (CAGR) of 34.51% from 2025 to 2033. Key growth drivers include an aging demographic demanding enhanced retirement and long-term care solutions, increasing consumer understanding of insurance benefits, and supportive government regulations mandating financial security. Digital advancements, such as personalized risk assessment and innovative online insurance platforms, are further accelerating market development. However, the market faces challenges from prevailing low interest rates affecting insurer investment yields and intensified competition from both established insurers and agile fintech disruptors. The market is segmented into life insurance (encompassing endowment, term, and retirement products) and non-life insurance (including property, casualty, and health), with potential for specialized segments like agricultural insurance.

France Life & Non-life Insurance Industry Market Size (In Billion)

Leading market participants such as Société Générale, Crédit Agricole, Covea, AXA, Allianz, La Banque Postale, MACIF, Crédit Mutuel, MAIF, ACM, Caisse d'Épargne, and Groupama are actively engaged in strategic initiatives including mergers and acquisitions, product portfolio expansion, and digital transformation to secure market leadership and customer loyalty. While regional market penetration and risk variations across France are expected, specific data remains limited. The forecast period (2025-2033) indicates sustained market growth, influenced by the aforementioned drivers, economic conditions, and regulatory shifts. Long-term success will depend on continuous adaptation to emerging trends, meeting the evolving demands of a digitally-empowered consumer base, and maintaining robust financial health within a competitive landscape.

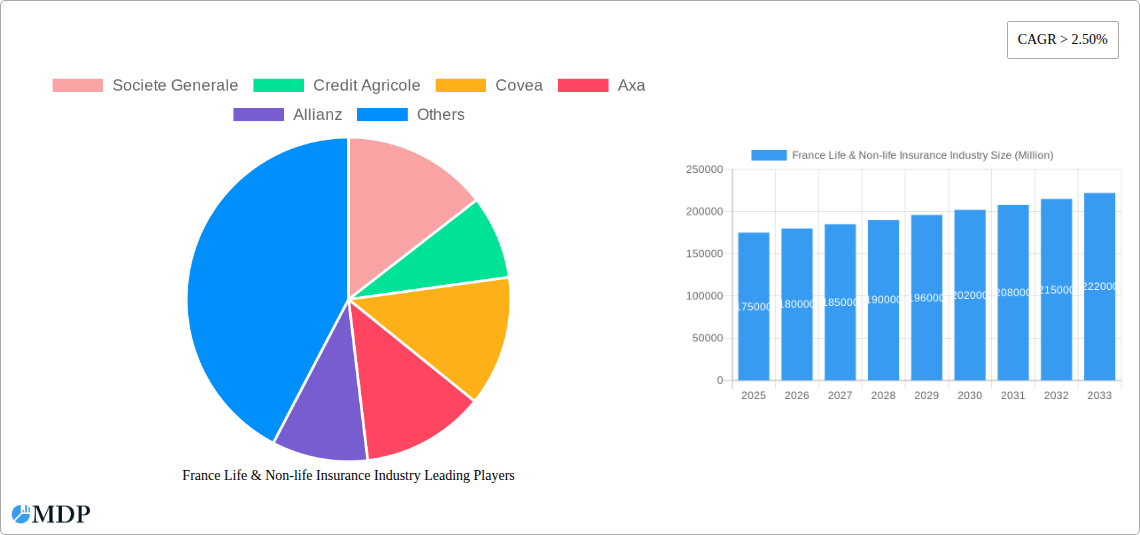

France Life & Non-life Insurance Industry Company Market Share

France Life & Non-life Insurance Industry: 2019-2033 Market Report

This comprehensive report provides an in-depth analysis of the French life & non-life insurance industry, offering invaluable insights for investors, insurers, and industry stakeholders. With a detailed study period spanning 2019-2033 (Base Year: 2025, Forecast Period: 2025-2033), this report unveils market dynamics, growth drivers, challenges, and emerging opportunities. Projected market value data is included for improved strategic planning and decision-making.

France Life & Non-life Insurance Industry Market Dynamics & Concentration

The French life & non-life insurance market, valued at €XX Million in 2024, exhibits a moderately concentrated landscape. Key players like AXA, Allianz, and Societe Generale hold significant market share, but a considerable number of smaller insurers also contribute to the market's diversity. Market concentration is influenced by several factors:

- Regulatory Framework: Stringent regulations imposed by the Autorité de Contrôle Prudentiel et de Résolution (ACPR) shape market dynamics and influence M&A activity.

- Innovation Drivers: Digitalization, including Insurtech advancements, is driving innovation in product offerings and service delivery.

- Product Substitutes: The rise of alternative risk management tools presents a challenge to traditional insurance models.

- End-User Trends: Shifting consumer preferences towards digital interaction and personalized insurance solutions are reshaping the industry's approach.

- M&A Activities: While the number of M&A deals fluctuated in the historical period (2019-2024), with approximately XX deals annually, a moderate increase is anticipated during the forecast period due to market consolidation and expansion strategies. The average deal size is estimated at €XX Million.

France Life & Non-life Insurance Industry Industry Trends & Analysis

The French life & non-life insurance market is expected to witness a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This growth is primarily fueled by:

- Increasing Insurance Penetration: Growing awareness of risk management and the expanding middle class are contributing to higher insurance penetration rates. Market penetration is projected to reach XX% by 2033.

- Technological Disruptions: Insurtech solutions are streamlining operations, enhancing customer experience, and fostering product innovation.

- Evolving Consumer Preferences: Demand for personalized, digital, and readily accessible insurance products is on the rise, demanding dynamic adaptation from insurers.

- Competitive Dynamics: Intense competition necessitates continuous innovation, cost optimization, and strategic partnerships to maintain market position.

Leading Markets & Segments in France Life & Non-life Insurance Industry

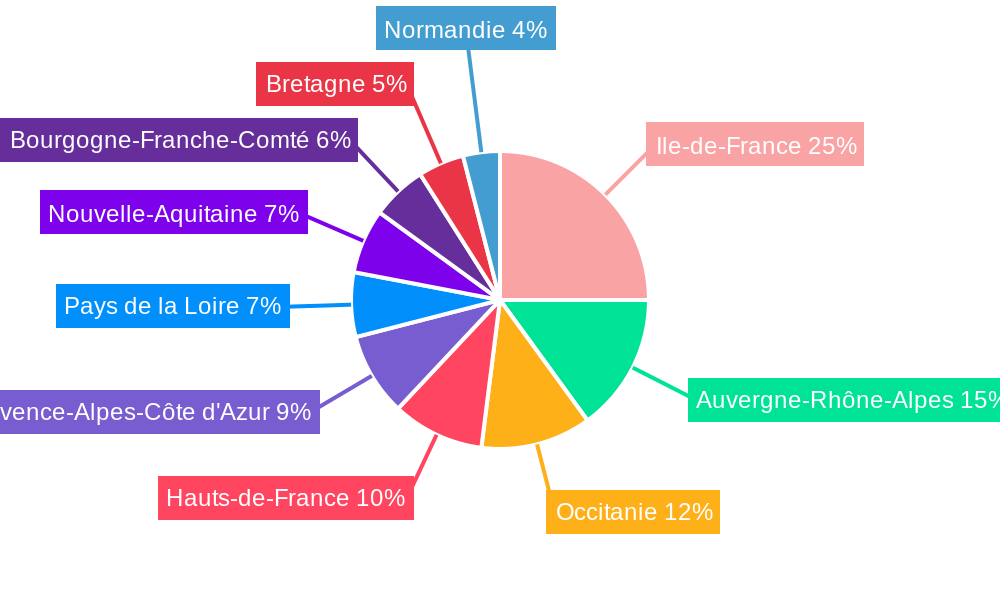

The Île-de-France region remains the dominant market segment in France's life and non-life insurance sector, contributing approximately XX% to the overall market value in 2024. This dominance is driven by:

- High Population Density: The region's substantial population concentration creates a large pool of potential customers.

- Economic Hub: Paris as an economic powerhouse boosts demand for various insurance products across sectors.

- Developed Infrastructure: Robust infrastructure facilitates efficient operations and distribution networks.

Further analysis reveals that the non-life segment holds a larger market share, primarily driven by the increasing demand for motor, health, and property insurance products. The life insurance segment is expected to experience slower, yet consistent growth, driven by increasing demand for retirement and savings plans.

France Life & Non-life Insurance Industry Product Developments

Recent product innovations include the integration of telematics in motor insurance, personalized health insurance packages, and the introduction of parametric insurance solutions. These innovations, driven by technological advancements, enhance customer experience and address specific market needs, improving risk assessment and pricing models. The market is also witnessing a trend towards digital-first insurance products, leveraging mobile apps and online platforms for streamlined policy management and claims processing.

Key Drivers of France Life & Non-life Insurance Industry Growth

Several factors contribute to the industry's projected growth:

- Favorable Economic Conditions: Steady economic growth in France contributes to increased disposable incomes and insurance spending.

- Government Regulations: Regulatory support for insurance innovation and market development stimulates industry growth.

- Technological Advancements: Digitalization streamlines processes and enhances customer experience, furthering market expansion.

Challenges in the France Life & Non-life Insurance Industry Market

The industry faces several headwinds:

- Intense Competition: A large number of players creates intense competition, pressuring profit margins and requiring continuous innovation.

- Regulatory Scrutiny: Strict regulatory compliance demands significant resources and careful navigation of evolving regulations.

- Economic Slowdown: Potential economic downturns could impact consumer spending and insurance demand, potentially reducing market growth by XX% in the most pessimistic scenarios.

Emerging Opportunities in France Life & Non-life Insurance Industry

Strategic partnerships, expansion into niche markets (e.g., cyber insurance), and the adoption of innovative technologies present significant opportunities. Developing personalized insurance solutions tailored to individual customer needs using AI and data analytics promises significant growth potential.

Leading Players in the France Life & Non-life Insurance Industry Sector

- Societe Generale

- Credit Agricole

- Covea

- Axa

- Allianz

- La banque postale

- MACIF

- Credit mutuel

- MAIF

- ACM

- Caisse D'Epargne

- Groupama (List Not Exhaustive)

Key Milestones in France Life & Non-life Insurance Industry Industry

- December 6, 2021: Allianz Partners and Uber partnered to offer insurance to independent drivers and couriers. This expands the reach of insurance to the gig economy.

- June 15, 2022: Berkshire Hathaway Specialty Insurance launched a Directors and Officers Liability policy, strengthening its multinational program offerings in France.

Strategic Outlook for France Life & Non-life Insurance Industry Market

The French life & non-life insurance market presents significant growth potential driven by technological innovation, evolving consumer preferences, and strategic partnerships. Companies that adapt to digitalization, prioritize customer experience, and embrace data-driven decision-making will be best positioned to thrive in this dynamic market. The focus on personalized products and expanded coverage into emerging sectors like cyber security and the gig economy will be pivotal for sustained market success.

France Life & Non-life Insurance Industry Segmentation

-

1. Insurance type

-

1.1. Life Insurance

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non-Life Insurance

- 1.2.1. Home

- 1.2.2. Motor

- 1.2.3. Health

- 1.2.4. Rest of Non-Life Insurance

-

1.1. Life Insurance

-

2. Channel of Distribution

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Online

- 2.5. Other distribution channels

France Life & Non-life Insurance Industry Segmentation By Geography

- 1. France

France Life & Non-life Insurance Industry Regional Market Share

Geographic Coverage of France Life & Non-life Insurance Industry

France Life & Non-life Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 34.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 5.1.1. Life Insurance

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non-Life Insurance

- 5.1.2.1. Home

- 5.1.2.2. Motor

- 5.1.2.3. Health

- 5.1.2.4. Rest of Non-Life Insurance

- 5.1.1. Life Insurance

- 5.2. Market Analysis, Insights and Forecast - by Channel of Distribution

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Online

- 5.2.5. Other distribution channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. France

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 6. France Life & Non-life Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance type

- 6.1.1. Life Insurance

- 6.1.1.1. Individual

- 6.1.1.2. Group

- 6.1.2. Non-Life Insurance

- 6.1.2.1. Home

- 6.1.2.2. Motor

- 6.1.2.3. Health

- 6.1.2.4. Rest of Non-Life Insurance

- 6.1.1. Life Insurance

- 6.2. Market Analysis, Insights and Forecast - by Channel of Distribution

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Banks

- 6.2.4. Online

- 6.2.5. Other distribution channels

- 6.1. Market Analysis, Insights and Forecast - by Insurance type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Societe Generale

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Credit Agricole

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Covea

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Axa

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Allianz

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 La banque postale

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 MACIF

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Credit mutuel

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 MAIF

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 ACM

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Caisse D'Epargne

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Groupama**List Not Exhaustive

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Societe Generale

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: France Life & Non-life Insurance Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: France Life & Non-life Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: France Life & Non-life Insurance Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 2: France Life & Non-life Insurance Industry Revenue billion Forecast, by Channel of Distribution 2020 & 2033

- Table 3: France Life & Non-life Insurance Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: France Life & Non-life Insurance Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 5: France Life & Non-life Insurance Industry Revenue billion Forecast, by Channel of Distribution 2020 & 2033

- Table 6: France Life & Non-life Insurance Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Life & Non-life Insurance Industry?

The projected CAGR is approximately 34.51%.

2. Which companies are prominent players in the France Life & Non-life Insurance Industry?

Key companies in the market include Societe Generale, Credit Agricole, Covea, Axa, Allianz, La banque postale, MACIF, Credit mutuel, MAIF, ACM, Caisse D'Epargne, Groupama**List Not Exhaustive.

3. What are the main segments of the France Life & Non-life Insurance Industry?

The market segments include Insurance type, Channel of Distribution.

4. Can you provide details about the market size?

The market size is estimated to be USD 291.04 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Significant Growth Contributed by the Non-Life Insurance Sector.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

On June 15, 2022, Berkshire Hathaway Specialty Insurance launched a Directors and Officers Liability policy insurance in France to serve local and multinational companies. This new coverage enhances BHSI's ability to provide multinational programs and services to companies with exposure in France and throughout the company's global network, which spans 170 countries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Life & Non-life Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Life & Non-life Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Life & Non-life Insurance Industry?

To stay informed about further developments, trends, and reports in the France Life & Non-life Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence