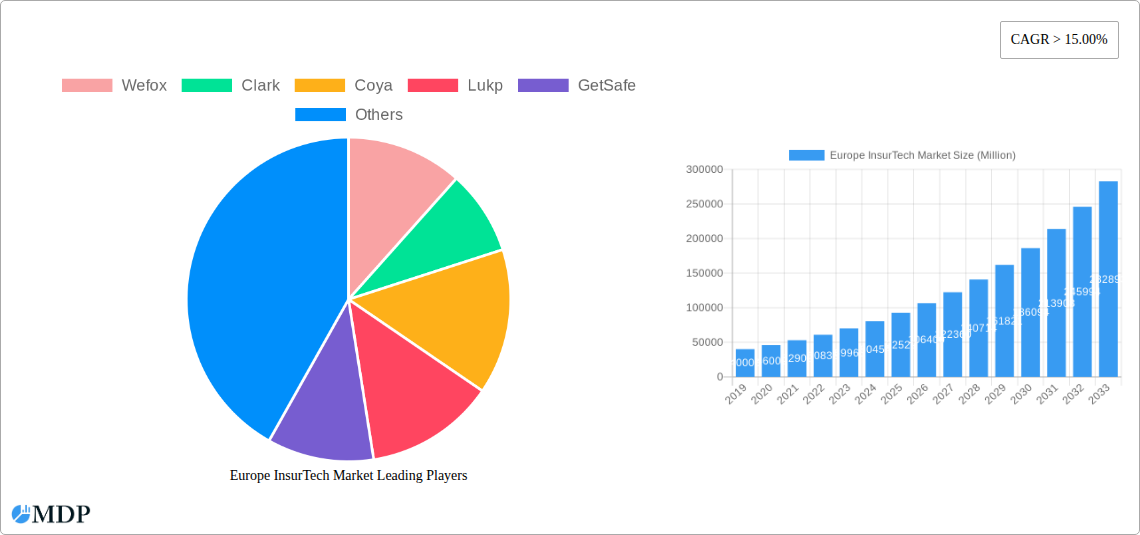

Key Insights

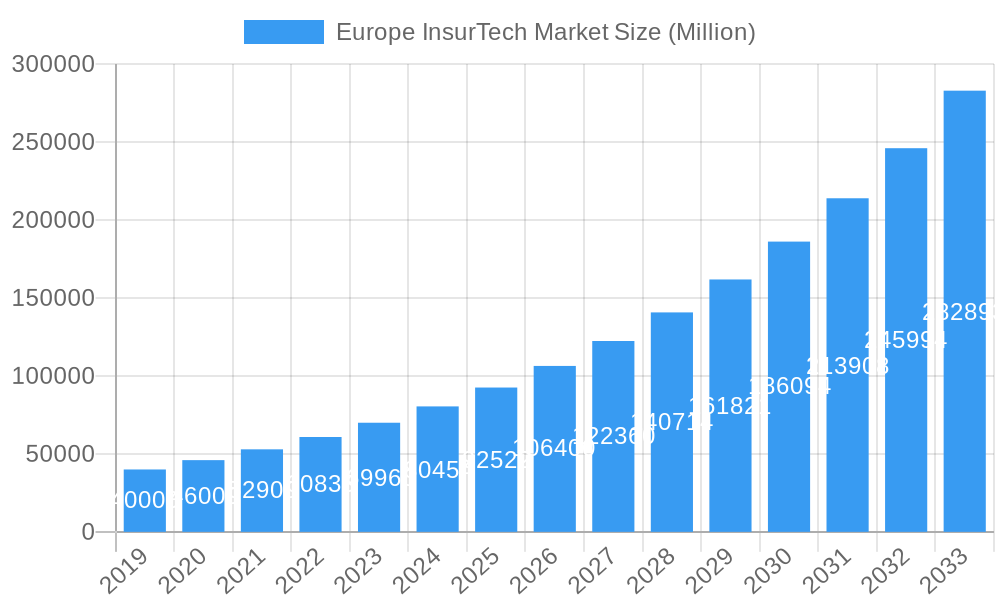

The European InsurTech market is projected for substantial expansion, driven by technological advancements and evolving consumer demands. Key growth catalysts include the widespread adoption of AI and ML for personalized risk assessment and claims processing, the proliferation of digital distribution, and a growing demand for on-demand and usage-based insurance. The integration of IoT devices for real-time data collection in underwriting and increased awareness of cyber risks are also significant drivers. The market size is estimated at 286.44 billion in 2025, with a projected CAGR of 6.09% from 2019 to 2033.

Europe InsurTech Market Market Size (In Billion)

This dynamic market emphasizes hyper-personalization through data analytics, offering tailored policies and competitive pricing. Streamlined insurance processes via intuitive digital platforms are a major focus. Emerging trends include the integration of InsurTech with digital ecosystems like smart homes and connected vehicles for embedded insurance. However, market growth is tempered by stringent regulatory frameworks, data privacy concerns, and significant investment requirements for technological upgrades and talent acquisition. The European InsurTech sector, encompassing Carriers, Enablers, and Distributors across major economies, is on an upward trajectory, prioritizing enhanced customer experience and operational efficiency.

Europe InsurTech Market Company Market Share

This comprehensive report offers definitive analysis and critical insights into the Europe InsurTech market for the period 2019 to 2033. With a base year of 2025, the research covers market dynamics, industry trends, leading markets, product developments, growth drivers, challenges, and emerging opportunities. We meticulously examine key players and pivotal milestones shaping the future of insurtech in Europe. Optimized for high search visibility with keywords like "InsurTech Europe," "Digital Insurance," "InsurTech Trends," and "InsurTech Market Size," this report provides essential intelligence for stakeholders.

Europe InsurTech Market Market Dynamics & Concentration

The Europe InsurTech market is characterized by a moderate to high concentration, with a significant number of innovative startups challenging established incumbents. Innovation drivers are primarily fueled by advancements in artificial intelligence (AI), machine learning (ML), big data analytics, and blockchain technology, enabling personalized products, streamlined claims processing, and enhanced customer experiences. Regulatory frameworks, while evolving, are increasingly supportive of digital transformation, with initiatives like Open Insurance and PSD2 fostering greater competition and data sharing. Product substitutes are emerging rapidly, ranging from peer-to-peer insurance models to embedded insurance solutions integrated into non-insurance platforms. End-user trends show a growing preference for digital-first insurance solutions, demanding transparency, convenience, and personalized coverage. Merger and acquisition (M&A) activities are on the rise as larger insurers seek to acquire innovative technologies and talent, and startups aim for scale and market penetration. For instance, the period has seen several significant funding rounds, indicating strong investor confidence. Key metrics such as market share distribution among top players and M&A deal counts are thoroughly analyzed within the report to provide a clear picture of market concentration.

Europe InsurTech Market Industry Trends & Analysis

The Europe InsurTech market is experiencing robust growth, driven by a confluence of technological advancements, evolving consumer expectations, and a conducive regulatory environment. The compound annual growth rate (CAGR) is projected to remain strong throughout the forecast period. Technological disruptions, including the widespread adoption of AI for risk assessment and fraud detection, IoT devices for proactive risk management, and blockchain for secure and transparent transactions, are fundamentally reshaping the insurance landscape. Consumer preferences are shifting towards on-demand, personalized, and usage-based insurance products, demanding seamless digital interfaces and efficient customer service. This has led to increased market penetration of insurtech solutions across various insurance lines. Competitive dynamics are intensifying, with a blend of agile startups and digitally transforming traditional insurers vying for market share. The rise of embedded insurance, where insurance is offered as an add-on to other products and services, is a significant trend, further blurring the lines between industries and expanding the reach of insurance. The analysis includes detailed metrics on market size, penetration rates for key segments, and the impact of emerging technologies on traditional insurance models.

Leading Markets & Segments in Europe InsurTech Market

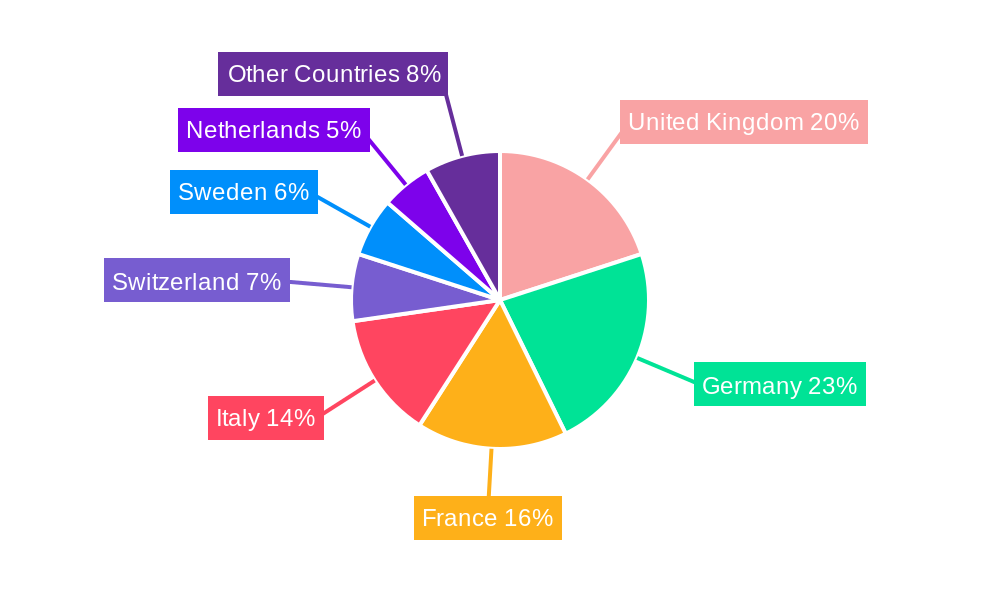

Germany and the United Kingdom stand out as the dominant geographical markets within the European InsurTech landscape, showcasing high levels of digital adoption and supportive regulatory initiatives. The United Kingdom benefits from a mature financial services sector and a proactive approach to regulatory sandboxes, fostering innovation in areas like digital underwriting and claims management. Key drivers include strong venture capital investment and a well-established ecosystem of tech startups.

Germany, with its large economy and a significant insurance penetration rate, presents a vast opportunity for insurtech solutions. The focus here is often on leveraging AI and big data for personalized product offerings and improved customer engagement. Economic policies promoting digital transformation and a strong emphasis on data privacy contribute to its leading position.

France is also a significant player, with increasing government support for digital innovation in financial services and a growing appetite for insurtech among consumers. Economic policies aimed at boosting the startup ecosystem and advancements in InsurTech infrastructure are key drivers.

Switzerland, despite its smaller market size, boasts a highly sophisticated financial sector and a strong demand for specialized, high-value insurance products, making it an attractive market for niche insurtech solutions. The focus on innovation and a stable economic environment are crucial here.

Sweden and the Netherlands are emerging as strong contenders, driven by their high digital literacy rates and open-mindedness towards new technologies. Government initiatives promoting digital financial services and a progressive regulatory approach are fueling growth.

In terms of business models, Enabler companies, providing technology and services to insurers and brokers, are experiencing substantial growth, facilitating the digital transformation of the broader industry. Distributor models, focusing on digital sales channels and customer acquisition, are also gaining traction, directly addressing evolving consumer preferences for convenience and accessibility. The Carrier model, where insurtech companies underwrite their own risks, is also present, particularly in specialized or niche insurance segments.

Europe InsurTech Market Product Developments

Product innovations in the Europe InsurTech market are characterized by a strong emphasis on customer-centricity and technological integration. This includes the development of AI-powered personalized insurance policies, on-demand coverage options tailored to specific usage scenarios, and parametric insurance solutions that trigger payouts automatically based on predefined events. The application of blockchain technology is leading to enhanced transparency and security in policy management and claims processing. Competitive advantages are being derived from seamless digital customer journeys, predictive analytics for risk mitigation, and the ability to offer highly competitive pricing through operational efficiency. Emerging trends include the integration of insurtech solutions into the Internet of Things (IoT) ecosystem for real-time monitoring and proactive risk management, as well as the development of embedded insurance products that are seamlessly integrated into other consumer purchases.

Key Drivers of Europe InsurTech Market Growth

The Europe InsurTech market's growth is propelled by several key drivers. Technological advancements, including the proliferation of AI, ML, big data analytics, and cloud computing, are enabling more efficient underwriting, personalized pricing, and streamlined claims processing. Evolving consumer expectations for digital-first, convenient, and transparent insurance solutions are a major catalyst. Furthermore, supportive regulatory frameworks, such as Open Insurance initiatives and data protection regulations, are fostering innovation and competition. The increasing adoption of IoT devices, offering opportunities for real-time risk assessment and prevention, also significantly contributes to market expansion.

Challenges in the Europe InsurTech Market Market

Despite its promising growth, the Europe InsurTech market faces several challenges. Regulatory hurdles and the complexity of navigating diverse national regulations can slow down market entry and product standardization. Cybersecurity threats and the need to protect sensitive customer data are paramount concerns, requiring significant investment in robust security infrastructure. Customer adoption and trust remain a factor, as some consumers are still hesitant to fully embrace digital insurance solutions over traditional channels. Intense competition from both established players and emerging startups also puts pressure on pricing and profitability, while issues related to data interoperability and integration with legacy systems can hinder seamless operations.

Emerging Opportunities in Europe InsurTech Market

Emerging opportunities in the Europe InsurTech market are abundant, driven by continuous innovation and evolving market needs. Technological breakthroughs in areas like generative AI and advanced predictive analytics offer new avenues for hyper-personalization and proactive risk management. Strategic partnerships between insurtech startups and traditional insurers are becoming increasingly common, allowing for the scaling of innovative solutions and access to established customer bases. The expansion of embedded insurance into new sectors, such as e-commerce, mobility, and healthcare, presents significant growth potential. Furthermore, the increasing demand for sustainability-focused insurance products and the integration of ESG (Environmental, Social, and Governance) factors into underwriting present a unique opportunity for differentiation.

Leading Players in the Europe InsurTech Market Sector

- Wefox

- Clark

- Coya

- Lukp

- GetSafe

- Simplesurance

- OMNI: US

- INZMO

- Decado

- FRISS

- Thinksurance

(List Not Exhaustive)

Key Milestones in Europe InsurTech Market Industry

- June 2021: The Berlin insurance company Wefox Group raised a record-breaking USD 650 Million in funds, leading to a USD 3 Billion valuation of the company. With this funding, the insurtech start-up's value has grown threefold since tapping investors in 2019.

- October 2021: GetSafe extended its Series B funding round. In addition to its original Series B funding of USD 30 Million, the company added another USD 63 Million in fresh capital. Overall, GetSafe raised USD 93 Million in the Series B round. The investors included an unnamed family office, Earlybird, and Abacon Capital.

Strategic Outlook for Europe InsurTech Market Market

The strategic outlook for the Europe InsurTech market is one of sustained growth and transformative change. Key growth accelerators include the continued embrace of advanced technologies like AI and blockchain, leading to more sophisticated and personalized insurance offerings. The increasing demand for embedded insurance solutions, seamlessly integrated into everyday purchases, will drive wider market penetration. Strategic partnerships between insurtech startups and traditional insurers will become even more crucial for scaling innovation and expanding market reach. Furthermore, a growing focus on sustainability and ESG principles within the insurance sector will create new product development opportunities and cater to a conscious consumer base. The market is poised for further consolidation and specialization, with a continued influx of venture capital fueling innovation and market expansion.

Europe InsurTech Market Segmentation

-

1. Business Model

- 1.1. Carrier

- 1.2. Enabler

- 1.3. Distributor

-

2. Geography

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Italy

- 2.5. Switzerland

- 2.6. Sweden

- 2.7. Netherlands

- 2.8. Other Countries

Europe InsurTech Market Segmentation By Geography

- 1. United Kingdom

- 2. Germany

- 3. France

- 4. Italy

- 5. Switzerland

- 6. Sweden

- 7. Netherlands

- 8. Other Countries

Europe InsurTech Market Regional Market Share

Geographic Coverage of Europe InsurTech Market

Europe InsurTech Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.09% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Business Model

- 5.1.1. Carrier

- 5.1.2. Enabler

- 5.1.3. Distributor

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United Kingdom

- 5.2.2. Germany

- 5.2.3. France

- 5.2.4. Italy

- 5.2.5. Switzerland

- 5.2.6. Sweden

- 5.2.7. Netherlands

- 5.2.8. Other Countries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. Germany

- 5.3.3. France

- 5.3.4. Italy

- 5.3.5. Switzerland

- 5.3.6. Sweden

- 5.3.7. Netherlands

- 5.3.8. Other Countries

- 5.1. Market Analysis, Insights and Forecast - by Business Model

- 6. Global Europe InsurTech Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Business Model

- 6.1.1. Carrier

- 6.1.2. Enabler

- 6.1.3. Distributor

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United Kingdom

- 6.2.2. Germany

- 6.2.3. France

- 6.2.4. Italy

- 6.2.5. Switzerland

- 6.2.6. Sweden

- 6.2.7. Netherlands

- 6.2.8. Other Countries

- 6.1. Market Analysis, Insights and Forecast - by Business Model

- 7. United Kingdom Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Business Model

- 7.1.1. Carrier

- 7.1.2. Enabler

- 7.1.3. Distributor

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United Kingdom

- 7.2.2. Germany

- 7.2.3. France

- 7.2.4. Italy

- 7.2.5. Switzerland

- 7.2.6. Sweden

- 7.2.7. Netherlands

- 7.2.8. Other Countries

- 7.1. Market Analysis, Insights and Forecast - by Business Model

- 8. Germany Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Business Model

- 8.1.1. Carrier

- 8.1.2. Enabler

- 8.1.3. Distributor

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United Kingdom

- 8.2.2. Germany

- 8.2.3. France

- 8.2.4. Italy

- 8.2.5. Switzerland

- 8.2.6. Sweden

- 8.2.7. Netherlands

- 8.2.8. Other Countries

- 8.1. Market Analysis, Insights and Forecast - by Business Model

- 9. France Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Business Model

- 9.1.1. Carrier

- 9.1.2. Enabler

- 9.1.3. Distributor

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. United Kingdom

- 9.2.2. Germany

- 9.2.3. France

- 9.2.4. Italy

- 9.2.5. Switzerland

- 9.2.6. Sweden

- 9.2.7. Netherlands

- 9.2.8. Other Countries

- 9.1. Market Analysis, Insights and Forecast - by Business Model

- 10. Italy Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Business Model

- 10.1.1. Carrier

- 10.1.2. Enabler

- 10.1.3. Distributor

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. United Kingdom

- 10.2.2. Germany

- 10.2.3. France

- 10.2.4. Italy

- 10.2.5. Switzerland

- 10.2.6. Sweden

- 10.2.7. Netherlands

- 10.2.8. Other Countries

- 10.1. Market Analysis, Insights and Forecast - by Business Model

- 11. Switzerland Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Business Model

- 11.1.1. Carrier

- 11.1.2. Enabler

- 11.1.3. Distributor

- 11.2. Market Analysis, Insights and Forecast - by Geography

- 11.2.1. United Kingdom

- 11.2.2. Germany

- 11.2.3. France

- 11.2.4. Italy

- 11.2.5. Switzerland

- 11.2.6. Sweden

- 11.2.7. Netherlands

- 11.2.8. Other Countries

- 11.1. Market Analysis, Insights and Forecast - by Business Model

- 12. Sweden Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Business Model

- 12.1.1. Carrier

- 12.1.2. Enabler

- 12.1.3. Distributor

- 12.2. Market Analysis, Insights and Forecast - by Geography

- 12.2.1. United Kingdom

- 12.2.2. Germany

- 12.2.3. France

- 12.2.4. Italy

- 12.2.5. Switzerland

- 12.2.6. Sweden

- 12.2.7. Netherlands

- 12.2.8. Other Countries

- 12.1. Market Analysis, Insights and Forecast - by Business Model

- 13. Netherlands Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Business Model

- 13.1.1. Carrier

- 13.1.2. Enabler

- 13.1.3. Distributor

- 13.2. Market Analysis, Insights and Forecast - by Geography

- 13.2.1. United Kingdom

- 13.2.2. Germany

- 13.2.3. France

- 13.2.4. Italy

- 13.2.5. Switzerland

- 13.2.6. Sweden

- 13.2.7. Netherlands

- 13.2.8. Other Countries

- 13.1. Market Analysis, Insights and Forecast - by Business Model

- 14. Other Countries Europe InsurTech Market Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - by Business Model

- 14.1.1. Carrier

- 14.1.2. Enabler

- 14.1.3. Distributor

- 14.2. Market Analysis, Insights and Forecast - by Geography

- 14.2.1. United Kingdom

- 14.2.2. Germany

- 14.2.3. France

- 14.2.4. Italy

- 14.2.5. Switzerland

- 14.2.6. Sweden

- 14.2.7. Netherlands

- 14.2.8. Other Countries

- 14.1. Market Analysis, Insights and Forecast - by Business Model

- 15. Competitive Analysis

- 15.1. Company Profiles

- 15.1.1 Wefox

- 15.1.1.1. Company Overview

- 15.1.1.2. Products

- 15.1.1.3. Company Financials

- 15.1.1.4. SWOT Analysis

- 15.1.2 Clark

- 15.1.2.1. Company Overview

- 15.1.2.2. Products

- 15.1.2.3. Company Financials

- 15.1.2.4. SWOT Analysis

- 15.1.3 Coya

- 15.1.3.1. Company Overview

- 15.1.3.2. Products

- 15.1.3.3. Company Financials

- 15.1.3.4. SWOT Analysis

- 15.1.4 Lukp

- 15.1.4.1. Company Overview

- 15.1.4.2. Products

- 15.1.4.3. Company Financials

- 15.1.4.4. SWOT Analysis

- 15.1.5 GetSafe

- 15.1.5.1. Company Overview

- 15.1.5.2. Products

- 15.1.5.3. Company Financials

- 15.1.5.4. SWOT Analysis

- 15.1.6 Simplesurance

- 15.1.6.1. Company Overview

- 15.1.6.2. Products

- 15.1.6.3. Company Financials

- 15.1.6.4. SWOT Analysis

- 15.1.7 OMNI

- 15.1.7.1. Company Overview

- 15.1.7.2. Products

- 15.1.7.3. Company Financials

- 15.1.7.4. SWOT Analysis

- 15.1.1 Wefox

- 15.2. Market Entropy

- 15.2.1 Company's Key Areas Served

- 15.2.2 Recent Developments

- 15.3. Company Market Share Analysis 2025

- 15.3.1 Top 5 Companies Market Share Analysis

- 15.3.2 Top 3 Companies Market Share Analysis

- 15.4. List of Potential Customers

- 16. Research Methodology

List of Figures

- Figure 1: Global Europe InsurTech Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: United Kingdom Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 3: United Kingdom Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 4: United Kingdom Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 5: United Kingdom Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 6: United Kingdom Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 7: United Kingdom Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Germany Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 9: Germany Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 10: Germany Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 11: Germany Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 12: Germany Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Germany Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: France Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 15: France Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 16: France Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 17: France Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 18: France Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 19: France Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Italy Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 21: Italy Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 22: Italy Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 23: Italy Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Italy Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Italy Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Switzerland Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 27: Switzerland Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 28: Switzerland Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 29: Switzerland Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 30: Switzerland Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Switzerland Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

- Figure 32: Sweden Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 33: Sweden Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 34: Sweden Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 35: Sweden Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 36: Sweden Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 37: Sweden Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

- Figure 38: Netherlands Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 39: Netherlands Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 40: Netherlands Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 41: Netherlands Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 42: Netherlands Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 43: Netherlands Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

- Figure 44: Other Countries Europe InsurTech Market Revenue (billion), by Business Model 2025 & 2033

- Figure 45: Other Countries Europe InsurTech Market Revenue Share (%), by Business Model 2025 & 2033

- Figure 46: Other Countries Europe InsurTech Market Revenue (billion), by Geography 2025 & 2033

- Figure 47: Other Countries Europe InsurTech Market Revenue Share (%), by Geography 2025 & 2033

- Figure 48: Other Countries Europe InsurTech Market Revenue (billion), by Country 2025 & 2033

- Figure 49: Other Countries Europe InsurTech Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 2: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 3: Global Europe InsurTech Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 5: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 8: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 9: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 11: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 14: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 17: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 18: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 20: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 21: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 23: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 24: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Global Europe InsurTech Market Revenue billion Forecast, by Business Model 2020 & 2033

- Table 26: Global Europe InsurTech Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 27: Global Europe InsurTech Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe InsurTech Market?

The projected CAGR is approximately 6.09%.

2. Which companies are prominent players in the Europe InsurTech Market?

Key companies in the market include Wefox, Clark, Coya, Lukp, GetSafe, Simplesurance, OMNI: US, INZMO, Decado, FRISS, Thinksurance**List Not Exhaustive.

3. What are the main segments of the Europe InsurTech Market?

The market segments include Business Model, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 286.44 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Investments in Insurtech Start-ups in Europe are Rising.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In October 2021, GetSafe extended its Series B funding round. In addition to its original Series B funding of USD 30 million, the company added another USD 63 million in fresh capital. Overall, GetSafe raised USD 93 million in the Series B round. The investors included an unnamed family office, Earlybird, and Abacon Capital.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe InsurTech Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe InsurTech Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe InsurTech Market?

To stay informed about further developments, trends, and reports in the Europe InsurTech Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence