Key Insights

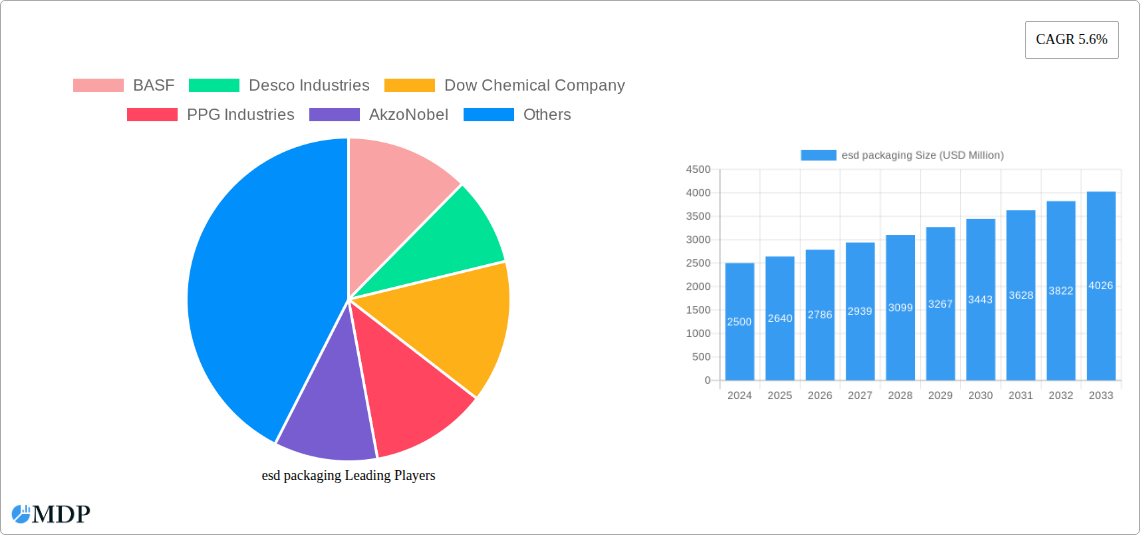

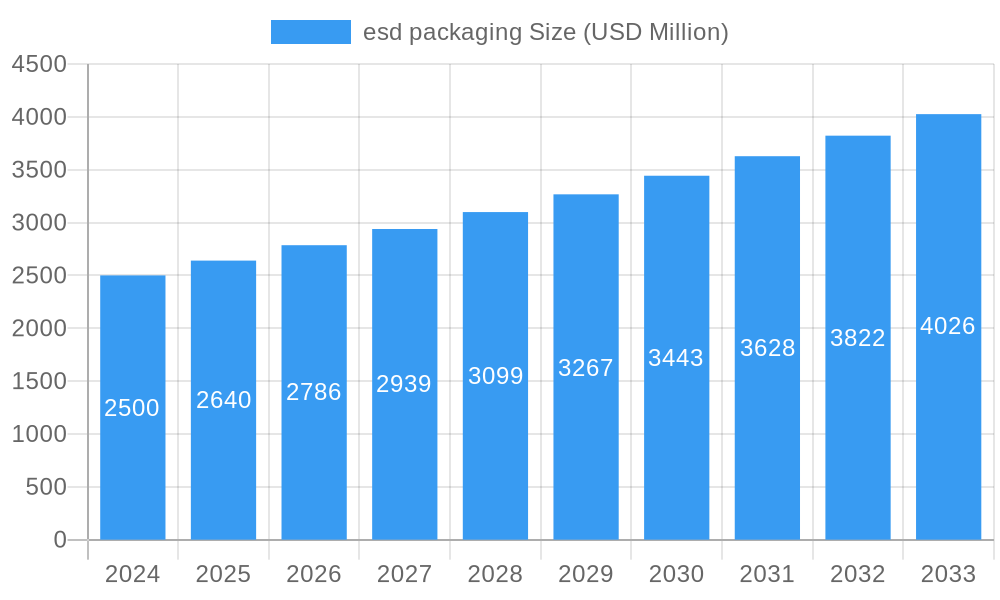

The global ESD packaging market is experiencing robust growth, currently valued at an estimated $2.5 billion in 2024. This expansion is fueled by the increasing adoption of electronic devices across various sectors and the critical need to protect sensitive components from electrostatic discharge. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.6%, indicating sustained demand and innovation within the industry. Key drivers for this surge include the escalating complexity of electronic components, stringent quality control requirements in manufacturing, and the growing awareness of the detrimental effects of ESD on product reliability and lifespan. The proliferation of the Internet of Things (IoT), advancements in 5G infrastructure, and the continuous evolution of consumer electronics are significant contributors to this upward trajectory. Furthermore, the automotive industry's increasing reliance on sophisticated electronic systems for advanced driver-assistance systems (ADAS) and in-car entertainment also presents substantial growth opportunities.

esd packaging Market Size (In Billion)

The ESD packaging market is segmented into various applications, with Communication Network Infrastructure and Consumer Electronics currently dominating, reflecting the widespread use of ESD-sensitive components in these areas. The demand is also rising significantly in Healthcare and Instrumentation, Aerospace and Defense, and Automotive sectors, where even minor electrical damage can have severe consequences. Emerging trends include the development of sustainable and eco-friendly ESD packaging solutions, as well as the integration of smart packaging features for enhanced traceability and monitoring. However, the market faces some restraints, such as the fluctuating prices of raw materials, including specialized polymers and conductive additives, which can impact manufacturing costs. Additionally, the high initial investment required for advanced ESD protection technologies can be a barrier for smaller enterprises. Despite these challenges, the overall outlook for the ESD packaging market remains exceptionally positive, driven by technological advancements and the ever-increasing ubiquity of electronics.

esd packaging Company Market Share

Here's an SEO-optimized and engaging report description for the ESD Packaging Market, ready for immediate use:

Unlocking Exponential Growth: The Comprehensive ESD Packaging Market Report (2019–2033)

This in-depth report provides a billion-dollar perspective on the dynamic ESD packaging market, a critical sector for safeguarding sensitive electronic components across numerous industries. Analyzing the period from 2019 to 2033, with a deep dive into the base year of 2025 and a robust forecast period of 2025–2033, this comprehensive study offers unparalleled insights into market dynamics, key trends, leading segments, product innovations, growth drivers, challenges, and emerging opportunities. Discover the strategic initiatives of industry giants like BASF, Desco Industries, Dow Chemical Company, PPG Industries, AkzoNobel, DaklaPack Group, Dou Yee, GWP Group, Kao-Chia Plastics, Miller Supply, Polyplus Packaging, TIP Corporation, and Uline. This report is an indispensable resource for stakeholders seeking to navigate the complex landscape of static sensitive device (SSD) packaging solutions, antistatic packaging, and electrostatic discharge (ESD) protection materials.

ESD Packaging Market Dynamics & Concentration

The ESD packaging market exhibits a moderate to high concentration, driven by a few dominant players and a growing number of specialized manufacturers. Innovation is a key driver, fueled by the increasing demand for advanced ESD shielding bags, conductive packaging, and dissipative material solutions to protect sensitive electronics in demanding applications. Regulatory frameworks, particularly those related to the safe transport and handling of electronic components, are increasingly shaping market requirements, pushing for compliance with standards like EIA-541 and ANSI/ESD S541. Product substitutes, such as traditional non-ESD packaging, are diminishing in relevance as the criticality of ESD protection becomes universally recognized. End-user trends are strongly influenced by the rapid growth of the consumer electronics market, the expansion of communication network infrastructure, and the stringent requirements of the aerospace and defense and healthcare and instrumentation sectors. Merger and acquisition (M&A) activities, while not at an extremely high pace, are strategic, focusing on acquiring innovative technologies and expanding market reach. Market share is closely watched, with key players vying for dominance in specific application segments. The number of M&A deals, though fluctuating, underscores the strategic importance of consolidation and technological acquisition in this sector, projected to reach significant billion-dollar valuations.

ESD Packaging Industry Trends & Analysis

The ESD packaging industry is poised for significant growth, driven by an escalating demand for reliable protection of sensitive electronic components. The market penetration of ESD packaging solutions is increasing year-on-year, reflecting a growing awareness of the detrimental effects of electrostatic discharge on electronic devices. Key market growth drivers include the relentless advancement and miniaturization of electronic components, necessitating more sophisticated and effective ESD packaging materials. The burgeoning internet of things (IoT), the proliferation of 5G technology, and the continuous innovation in consumer electronics are creating a perpetually expanding market for robust ESD protection. Technological disruptions, such as the development of advanced antistatic polymers, self-healing ESD films, and smart ESD packaging with integrated monitoring capabilities, are reshaping the competitive landscape. Consumer preferences are increasingly leaning towards sustainable and eco-friendly packaging options, pushing manufacturers to develop recyclable ESD packaging and bio-based alternatives. The competitive dynamics are characterized by intense innovation, strategic partnerships, and a focus on delivering tailored solutions for specific industry needs. The projected Compound Annual Growth Rate (CAGR) for the ESD packaging market signifies a substantial upward trajectory, with market penetration expected to reach new heights, creating billion-dollar opportunities for innovators and established players alike. The constant evolution of product specifications and the increasing complexity of supply chains further underscore the critical role of effective ESD packaging in ensuring product integrity and preventing costly failures.

Leading Markets & Segments in ESD Packaging

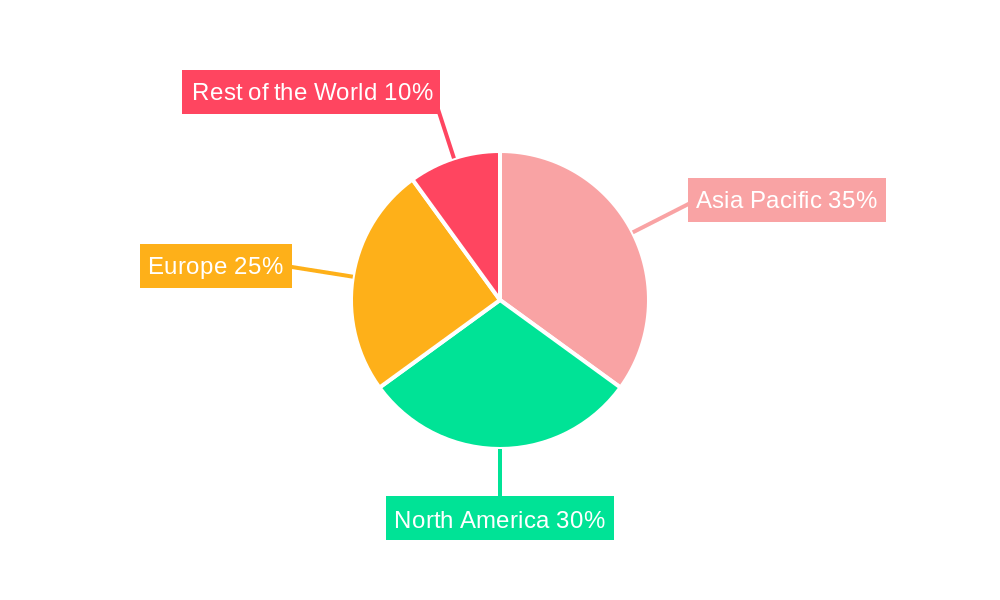

The ESD packaging market showcases distinct leadership across various regions and application segments. The Asia-Pacific region, particularly China, dominates the market due to its significant manufacturing base for consumer electronics, communication network infrastructure, and automotive electronics. Within applications, Consumer Electronics commands the largest market share, driven by the massive global demand for smartphones, laptops, tablets, and other electronic gadgets. Following closely is Communication Network Infrastructure, fueled by the ongoing global rollout of 5G networks and the expansion of data centers. The Aerospace and Defense sector, while smaller in volume, represents a high-value segment due to the stringent reliability and performance requirements for its sensitive components.

Dominant Region: Asia-Pacific

- Key Drivers: Prolific manufacturing hubs for electronics, significant investments in technological infrastructure, favorable economic policies supporting manufacturing exports.

- Detailed Dominance: The sheer volume of electronic component production and consumption in countries like China, South Korea, and Taiwan solidifies Asia-Pacific's leadership. The presence of major electronics manufacturers and their extensive supply chains creates an insatiable demand for reliable ESD protection.

Dominant Application: Consumer Electronics

- Key Drivers: High production volumes, constant product innovation, miniaturization of components, global consumer demand.

- Detailed Dominance: The rapid product cycles and the widespread use of sensitive microelectronics in consumer devices make effective ESD packaging a non-negotiable requirement. The economic policies promoting the widespread adoption of technology further amplify this segment's importance.

Dominant Type: Antistatic Latex Bag Packaging

- Key Drivers: Cost-effectiveness, widespread availability, proven ESD protection capabilities for a broad range of electronic components.

- Detailed Dominance: Antistatic Latex Bag Packaging continues to be a workhorse in the industry due to its balance of performance and affordability, making it a preferred choice for mass production in various sectors.

ESD Packaging Product Developments

Recent ESD packaging product developments are focused on enhancing protective capabilities, improving sustainability, and integrating advanced functionalities. Innovations include the introduction of multilayer films offering superior ESD shielding and moisture barrier properties, as well as the development of novel dissipative materials with improved conductivity and longer service life. Composite materials packaging is gaining traction for its strength and customizability, providing robust protection for larger and more complex electronic assemblies. Competitive advantages are being gained through lighter-weight designs, greater reusability, and the integration of smart features for real-time monitoring of environmental conditions and potential ESD events.

Key Drivers of ESD Packaging Growth

The ESD packaging market is propelled by several key growth drivers. Technologically, the increasing density and complexity of integrated circuits and the ongoing miniaturization of electronic components necessitate advanced ESD protection solutions. Economically, the rapid expansion of the global electronics industry, particularly in burgeoning markets, fuels demand. Regulatory frameworks, such as those mandating the safe transport of sensitive medical devices and critical aerospace components, also play a crucial role in driving adoption. Furthermore, the growing awareness among manufacturers of the substantial cost savings associated with preventing ESD-related product failures is a significant catalyst.

Challenges in the ESD Packaging Market

Despite robust growth prospects, the ESD packaging market faces several challenges. Regulatory hurdles can arise from differing international standards and compliance requirements, adding complexity to global supply chains. Supply chain issues, including raw material price volatility and logistics disruptions, can impact production costs and lead times. Competitive pressures from both established players and emerging manufacturers, particularly in cost-sensitive segments, necessitate continuous innovation and efficiency improvements. The perceived high cost of some advanced ESD packaging solutions can also be a barrier for smaller businesses or in less critical applications.

Emerging Opportunities in ESD Packaging

The ESD packaging market is ripe with emerging opportunities. Technological breakthroughs in material science are paving the way for next-generation ESD packaging with superior performance characteristics, such as enhanced EMI shielding and improved electrostatic dissipation. Strategic partnerships between packaging manufacturers and electronics companies are crucial for developing customized solutions tailored to evolving product needs. Market expansion into developing economies, where the adoption of advanced electronics is rapidly growing, presents significant untapped potential. The increasing focus on sustainability also opens doors for the development and adoption of eco-friendly and recyclable ESD packaging solutions.

Leading Players in the ESD Packaging Sector

- BASF

- Desco Industries

- Dow Chemical Company

- PPG Industries

- AkzoNobel

- DaklaPack Group

- Dou Yee

- GWP Group

- Kao-Chia Plastics

- Miller Supply

- Polyplus Packaging

- TIP Corporation

- Uline

Key Milestones in ESD Packaging Industry

- 2019: Increased adoption of advanced shielding bag technologies for high-frequency electronics.

- 2020: Growing demand for sustainable ESD packaging solutions amidst global environmental awareness.

- 2021: Significant growth in ESD packaging for 5G infrastructure components.

- 2022: Emergence of smart ESD packaging with integrated sensors for environmental monitoring.

- 2023: Increased M&A activity focused on acquiring innovative material science companies in the ESD sector.

- 2024: Enhanced focus on supply chain resilience and localized ESD packaging production.

- 2025 (Projected): Continued strong growth driven by AI and IoT device proliferation, demand for cost-effective and high-performance solutions.

- 2026-2033 (Forecast): Sustained upward trend with innovations in bio-based and fully recyclable ESD materials, coupled with widespread adoption of advanced ESD protection in emerging technologies.

Strategic Outlook for ESD Packaging Market

The strategic outlook for the ESD packaging market is exceptionally promising. Growth accelerators will be driven by the continuous miniaturization of electronics, the expansion of 5G and IoT networks, and the increasing stringency of regulations in sectors like healthcare and aerospace. Companies that focus on developing innovative, sustainable, and cost-effective ESD packaging solutions will be best positioned for success. Strategic opportunities lie in expanding into emerging markets, forging strong partnerships with electronics manufacturers, and investing in research and development for next-generation ESD protection materials. The market's future will be shaped by a commitment to technological advancement and a keen understanding of evolving industry demands, ensuring continued billion-dollar growth potential.

esd packaging Segmentation

-

1. Application

- 1.1. Communication Network Infrastructure

- 1.2. Consumer Electronics

- 1.3. Computer Peripherals

- 1.4. Aerospace and Defense

- 1.5. Healthcare and Instrumentation

- 1.6. Automotive

- 1.7. Other

-

2. Types

- 2.1. Antistatic Latex Bag Packaging

- 2.2. Composite Materials Packaging

- 2.3. Other

esd packaging Segmentation By Geography

- 1. CA

esd packaging Regional Market Share

Geographic Coverage of esd packaging

esd packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. esd packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Communication Network Infrastructure

- 5.1.2. Consumer Electronics

- 5.1.3. Computer Peripherals

- 5.1.4. Aerospace and Defense

- 5.1.5. Healthcare and Instrumentation

- 5.1.6. Automotive

- 5.1.7. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Antistatic Latex Bag Packaging

- 5.2.2. Composite Materials Packaging

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 BASF

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Desco Industries

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Dow Chemical Company

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 PPG Industries

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 AkzoNobel

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 DaklaPack Group

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Dou Yee

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 GWP Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Kao-Chia Plastics

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Miller Supply

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Polyplus Packaging

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 TIP Corporation

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Uline

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 BASF

List of Figures

- Figure 1: esd packaging Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: esd packaging Share (%) by Company 2025

List of Tables

- Table 1: esd packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: esd packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: esd packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: esd packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: esd packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: esd packaging Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the esd packaging?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the esd packaging?

Key companies in the market include BASF, Desco Industries, Dow Chemical Company, PPG Industries, AkzoNobel, DaklaPack Group, Dou Yee, GWP Group, Kao-Chia Plastics, Miller Supply, Polyplus Packaging, TIP Corporation, Uline.

3. What are the main segments of the esd packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "esd packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the esd packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the esd packaging?

To stay informed about further developments, trends, and reports in the esd packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence