Key Insights

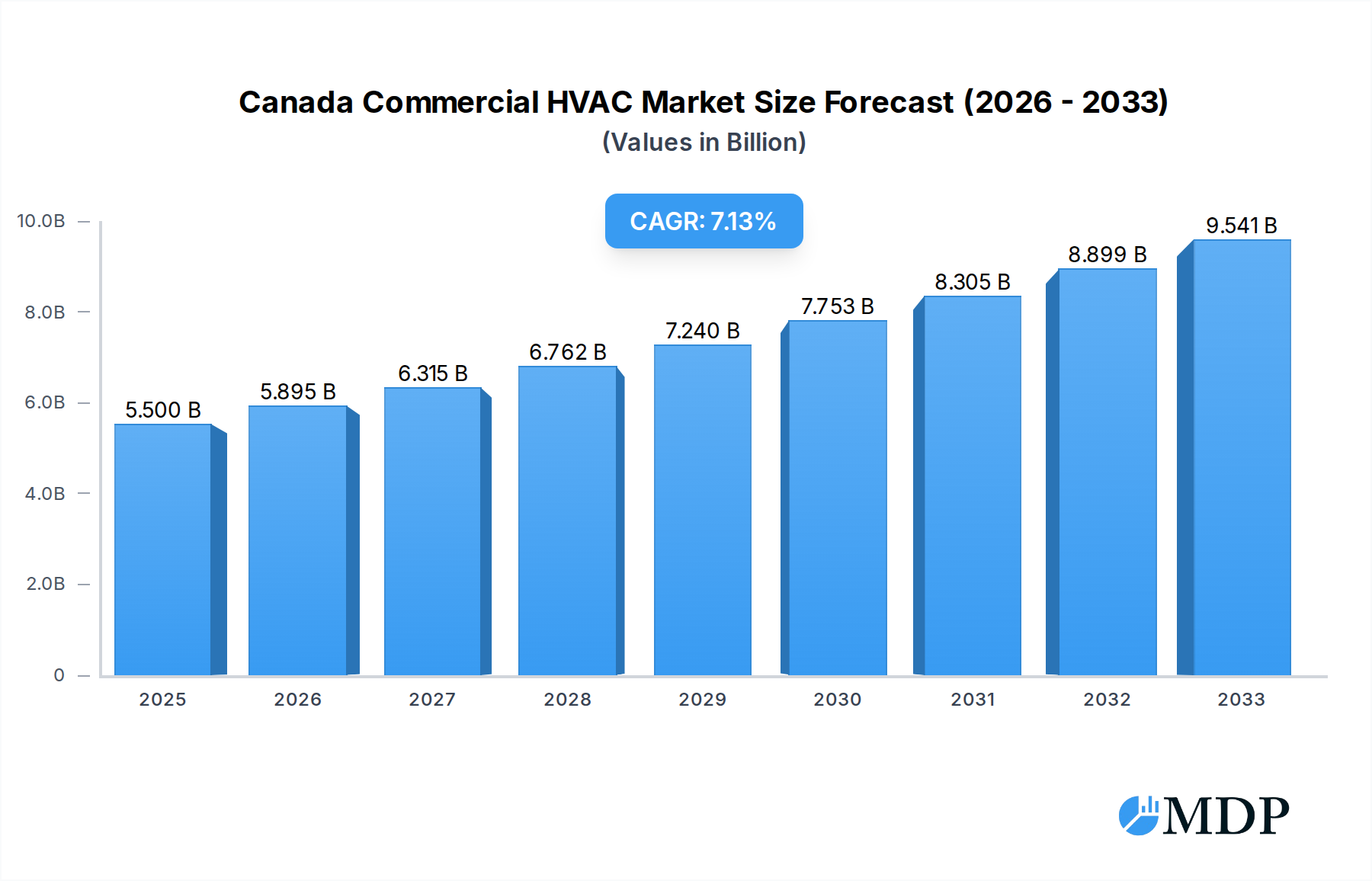

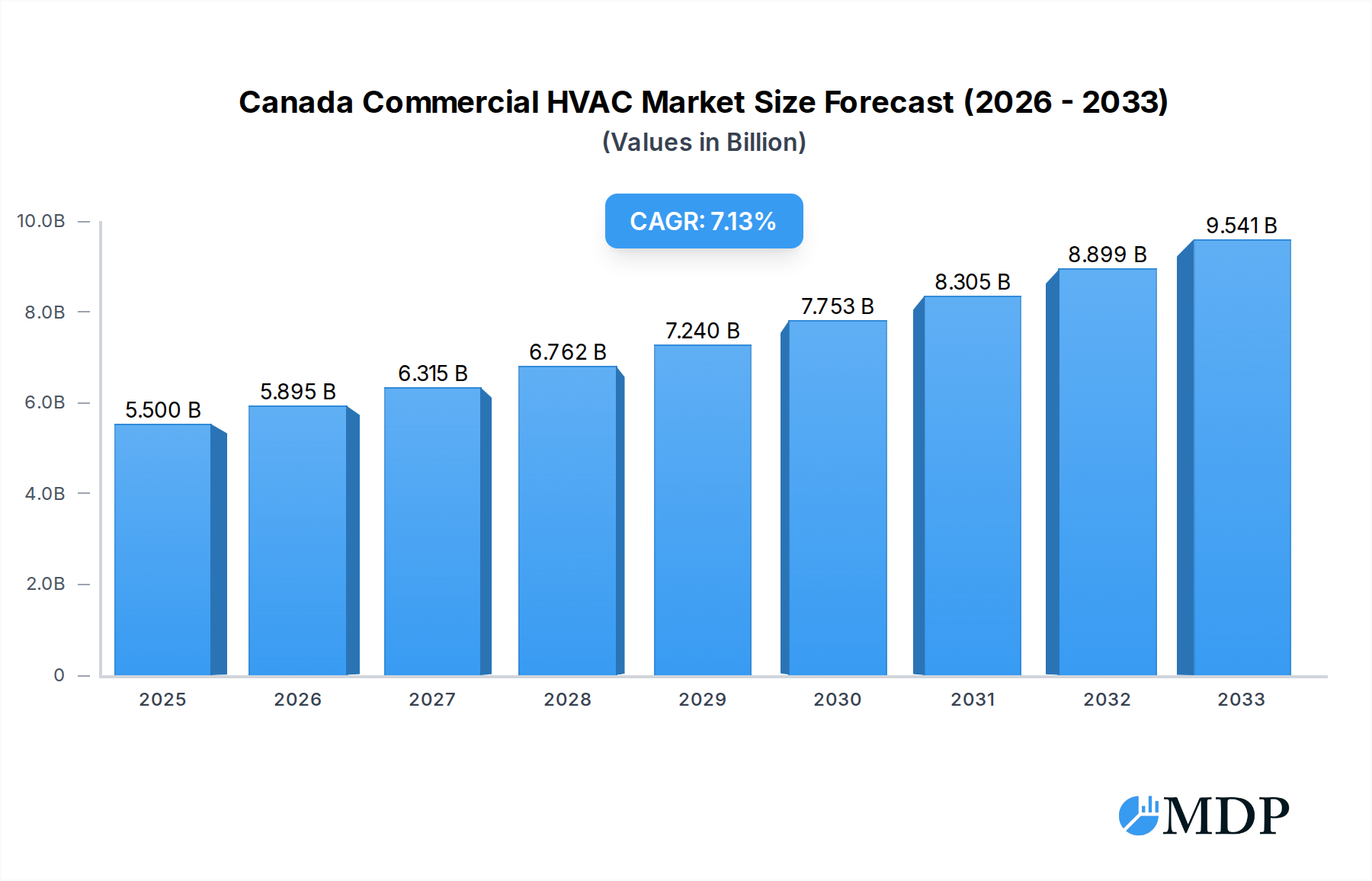

The Canadian commercial HVAC market is poised for significant expansion, driven by a growing emphasis on energy efficiency, sustainability, and occupant comfort in commercial spaces. With a projected market size of approximately USD 5,500 Million in 2025, the sector is expected to experience a healthy compound annual growth rate (CAGR) of 7.21% through the forecast period ending in 2033. This growth is fueled by increasing investments in building retrofits and new construction projects that prioritize advanced HVAC solutions. The demand for sophisticated HVAC equipment, including high-efficiency heating, ventilation, and air conditioning systems, is escalating as businesses aim to reduce operational costs and their environmental footprint. Furthermore, the burgeoning hospitality sector, along with the continuous development of commercial and public buildings, are key contributors to this upward trajectory.

Canada Commercial HVAC Market Market Size (In Billion)

The market is characterized by a robust demand for both HVAC equipment and services. HVAC services, encompassing installation, maintenance, and repair, are critical for ensuring the optimal performance and longevity of these systems, thus contributing substantially to the overall market value. Emerging trends such as the integration of smart building technologies, the Internet of Things (IoT) for remote monitoring and control, and the adoption of refrigerants with lower global warming potential are shaping the competitive landscape. While the market benefits from strong growth drivers, potential restraints include the initial high cost of advanced HVAC systems and evolving regulatory landscapes that require continuous adaptation. Leading players like Robert Bosch GmbH, Carrier Corporation, and Johnson Controls International PLC are actively innovating to meet these demands, offering a diverse range of solutions tailored to the specific needs of the Canadian market.

Canada Commercial HVAC Market Company Market Share

Canada Commercial HVAC Market: Growth, Trends, and Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the Canada Commercial HVAC market, offering strategic insights and actionable intelligence for industry stakeholders. Covering the historical period (2019-2024), base year (2025), and an extensive forecast period (2025-2033), this study meticulously examines market dynamics, key trends, leading segments, and emerging opportunities within Canada's vital commercial heating, ventilation, and air conditioning sector.

The Canadian commercial HVAC landscape is undergoing significant transformation, driven by a confluence of factors including escalating demand for energy-efficient solutions, stringent environmental regulations, and the ongoing evolution of building technologies. This report delves into the intricate details of this dynamic market, providing a granular view of its growth trajectory, competitive landscape, and future potential. Our analysis focuses on key market drivers, technological innovations, consumer preferences, and the strategic initiatives of major industry players.

Unlock critical data and expert analysis to navigate the complexities of the Canadian commercial building HVAC sector. This report is an essential resource for manufacturers, suppliers, distributors, and end-users seeking to capitalize on the burgeoning opportunities within this critical market. With a focus on HVAC equipment, HVAC services, and specific end-user industries such as hospitality, commercial buildings, and public buildings, we deliver a holistic view of the market's present state and future prospects.

This report utilizes a market research study period of 2019–2033, with a base year of 2025 and an estimated year of 2025, ensuring accurate projections and insightful analysis.

Canada Commercial HVAC Market Market Dynamics & Concentration

The Canada Commercial HVAC market exhibits a moderate to high concentration, with a few key players dominating market share. Leading companies such as Carrier Corporation, Johnson Controls International PLC, and Trane Technologies PLC hold significant sway due to their extensive product portfolios, established distribution networks, and brand recognition. Innovation is a primary driver, fueled by the increasing demand for energy-efficient and sustainable HVAC solutions. Government regulations mandating lower emissions and higher energy performance standards for commercial buildings continuously push manufacturers to develop advanced technologies. Product substitutes, while present in some niche applications, are generally less efficient or cost-effective for comprehensive HVAC solutions. End-user trends are shifting towards smart building technologies, IoT integration for remote monitoring and control, and demand for systems that offer superior indoor air quality (IAQ) and occupant comfort. Mergers and acquisitions (M&A) activities have been moderate, often focused on acquiring innovative technologies or expanding market reach. For instance, recent strategic partnerships and technology integrations are observed among the top players. The market's focus on sustainability and decarbonization presents a significant opportunity for companies that can offer green HVAC solutions and services.

Canada Commercial HVAC Market Industry Trends & Analysis

The Canada Commercial HVAC market is experiencing robust growth, projected to expand at a significant Compound Annual Growth Rate (CAGR) driven by several interconnected factors. A primary catalyst is the increasing focus on energy efficiency and sustainability across all commercial sectors. As Canada aims to meet its climate targets, stringent building codes and government incentives are encouraging the adoption of high-efficiency HVAC systems, including advanced heat pumps and variable refrigerant flow (VRF) systems. Technological disruptions are at the forefront, with the integration of the Internet of Things (IoT) and artificial intelligence (AI) revolutionizing HVAC operations. Smart thermostats, predictive maintenance software, and Building Management Systems (BMS) are becoming standard, enhancing operational efficiency, reducing energy consumption, and improving occupant comfort. Consumer preferences are increasingly aligning with these technological advancements, with building owners and facility managers prioritizing systems that offer lower operating costs, reduced carbon footprints, and enhanced indoor air quality. The growing awareness of the health impacts of poor IAQ, exacerbated by events like the COVID-19 pandemic, is further accelerating demand for sophisticated air filtration and ventilation solutions. Competitive dynamics are characterized by intense innovation, with companies investing heavily in research and development to introduce next-generation products. The market penetration of advanced HVAC technologies is steadily rising, particularly in new construction projects and major retrofits. The shift towards a service-based economy is also evident, with an increasing demand for comprehensive HVAC maintenance, repair, and upgrade services, contributing to recurring revenue streams for service providers. The commercial building sector remains the largest end-user segment, with significant investments in HVAC upgrades and new installations to meet evolving energy and comfort standards. The hospitality industry is also a key contributor, driven by the need for consistent comfort and energy management to optimize guest experiences and operational costs. The public buildings segment, including schools, hospitals, and government facilities, is experiencing a surge in demand for energy-efficient and healthy indoor environments, often bolstered by government funding for upgrades. The overall industry trend points towards greater integration, automation, and sustainability in HVAC solutions.

Leading Markets & Segments in Canada Commercial HVAC Market

The Canada Commercial HVAC market is characterized by strong performance across several key segments. Within the Type of Component, HVAC Equipment generally leads, with a substantial contribution from both Heating Equipment and Air Conditioning / Ventilation Equipment. The demand for advanced air conditioning and ventilation systems is particularly robust, driven by the need for enhanced indoor air quality (IAQ) and precise temperature control, especially in regions with fluctuating climates. Heating equipment also remains critical, with a growing preference for energy-efficient and renewable-energy-integrated solutions like high-efficiency furnaces and heat pumps. HVAC Services represent a rapidly growing segment, encompassing installation, maintenance, repair, and retrofitting services. This growth is propelled by the increasing complexity of modern HVAC systems and the rising demand for ongoing operational efficiency and longevity.

In terms of End-user Industry, Commercial Buildings represent the dominant market. This segment includes office buildings, retail spaces, manufacturing facilities, and other commercial establishments that require reliable and efficient HVAC solutions for occupant comfort, operational efficiency, and regulatory compliance. The continuous development of new commercial properties and the ongoing need to upgrade existing infrastructure to meet energy efficiency standards fuel this dominance. The Hospitality Industry is another significant segment, with hotels, restaurants, and event venues prioritizing guest comfort and experience, which directly correlates with effective HVAC performance. Energy cost management is also a critical factor for this sector, driving the adoption of smart and efficient HVAC technologies. Public Buildings, including schools, hospitals, and government offices, are also substantial contributors. These sectors often have specific IAQ requirements and long-term energy efficiency mandates, leading to significant investments in HVAC upgrades and new installations, often supported by public funding and green building initiatives. The "Others" segment, encompassing various niche applications and smaller commercial enterprises, also contributes to the overall market size, though at a smaller scale. Economic policies supporting green building certifications and energy efficiency programs significantly influence the growth of all these segments, encouraging the adoption of advanced and sustainable HVAC solutions across the Canadian commercial landscape.

Canada Commercial HVAC Market Product Developments

Product developments in the Canada Commercial HVAC market are heavily focused on enhancing energy efficiency, improving indoor air quality, and integrating smart technologies. Key innovations include the introduction of next-generation heat pumps with enhanced cold-climate performance, capable of maintaining optimal efficiency even in harsh Canadian winters. Advanced Variable Refrigerant Flow (VRF) systems are gaining traction for their zoning capabilities and energy savings. The integration of IoT sensors and AI-powered controls allows for predictive maintenance, remote diagnostics, and optimized energy consumption, offering significant competitive advantages to manufacturers and enhanced operational efficiency for end-users. Solutions designed for seamless integration with Building Management Systems (BMS) are also prominent, facilitating centralized control and data analytics.

Key Drivers of Canada Commercial HVAC Market Growth

Several key drivers are fueling the growth of the Canada Commercial HVAC market. The imperative to reduce energy consumption and carbon emissions, driven by government regulations and corporate sustainability goals, is a primary driver. The increasing demand for improved indoor air quality (IAQ) in commercial spaces, heightened by public health concerns, is another significant factor. Technological advancements in HVAC equipment, such as smart controls, IoT integration, and energy-efficient designs, are making modern systems more attractive and cost-effective. Furthermore, the ongoing development and modernization of commercial real estate, including new construction projects and retrofits of existing buildings, create sustained demand for HVAC solutions. Government incentives and rebates for adopting energy-efficient technologies also play a crucial role in stimulating market growth.

Challenges in the Canada Commercial HVAC Market Market

The Canada Commercial HVAC Market faces several challenges that can hinder its growth trajectory. Stringent building codes and regulations, while driving innovation, can also increase upfront costs for some businesses. The upfront capital investment for advanced, energy-efficient HVAC systems can be a significant barrier for smaller enterprises or those with limited budgets. Supply chain disruptions and the rising cost of raw materials and components can impact product availability and pricing. A shortage of skilled labor for installation, maintenance, and repair of sophisticated HVAC systems poses a challenge in meeting the growing demand for services. Moreover, the market faces competition from older, less efficient systems that may still be operational, creating a resistance to immediate upgrades for some building owners.

Emerging Opportunities in Canada Commercial HVAC Market

Emerging opportunities in the Canada Commercial HVAC Market are abundant, primarily driven by the accelerating shift towards sustainability and smart building technologies. The growing demand for electrification of heating systems presents a significant opportunity for heat pump manufacturers and installers. The increasing focus on indoor air quality (IAQ) is creating demand for advanced filtration, ventilation, and air purification solutions, particularly in healthcare and educational facilities. The integration of Building Information Modeling (BIM) and digital twin technologies offers opportunities for enhanced design, installation, and ongoing management of HVAC systems. Furthermore, the concept of "Cooling-as-a-Service" (CaaS) and other subscription-based models for HVAC solutions presents a recurring revenue stream opportunity for providers, making advanced technologies more accessible to a wider range of commercial clients. Strategic partnerships between HVAC manufacturers, technology providers, and energy service companies will be crucial in capitalizing on these evolving market dynamics.

Leading Players in the Canada Commercial HVAC Market Sector

- Robert Bosch GmbH

- Carrier Corporation

- Panasonic Holdings Corporation

- Johnson Controls International PLC

- Trane Technologies PLC

- Danfoss Inc

- Panasonic Corporation

- Mitsubishi Electric Hydronics & It Cooling Systems SpA

- LG Electronics Inc

- Trox GmbH

Key Milestones in Canada Commercial HVAC Market Industry

- June 2024: Carrier, a division of Carrier Global Corporation, has introduced 'Carrier Cooling-as-a-Service,' a suite of solutions designed to assist commercial clients in streamlining the management of HVAC and other thermal systems, all in the face of the contemporary energy shift. This innovative portfolio from Carrier offers an alternative to conventional heating and cooling systems, shifting from the traditional upfront payment model to a more flexible subscription-based approach.

- April 2024: Johnson Controls-Hitachi Air Conditioning has introduced its cold-climate variable-refrigerant flow (VRF) heat pump. The air365 Max with HeatForce, this top-flow VRF system, promises commercial building owners a trifecta: unmatched comfort, leading energy efficiency, and straightforward installation and maintenance. It's designed for those keen on cutting operational costs and reducing carbon footprints.

Strategic Outlook for Canada Commercial HVAC Market Market

The strategic outlook for the Canada Commercial HVAC Market is highly optimistic, driven by a sustained demand for energy-efficient and sustainable solutions. The continued push towards decarbonization will accelerate the adoption of electrification technologies, particularly advanced heat pumps for both heating and cooling. The growing emphasis on smart buildings and integrated systems presents a significant opportunity for companies that can offer IoT-enabled HVAC solutions with advanced analytics and predictive maintenance capabilities. The expansion of service-based business models, such as "Cooling-as-a-Service," will democratize access to cutting-edge HVAC technology for a broader range of commercial clients. Strategic collaborations between technology providers, manufacturers, and energy management firms will be crucial for developing holistic and innovative solutions. Furthermore, the ongoing modernization of existing commercial building stock will provide consistent demand for retrofitting and upgrade projects, ensuring a robust market for years to come.

Canada Commercial HVAC Market Segmentation

-

1. Type of Component

-

1.1. HVAC Equipment

- 1.1.1. Heating Equipment

- 1.1.2. Air Conditioning /Ventillation Equipment

- 1.2. HVAC Services

-

1.1. HVAC Equipment

-

2. End-user Industry

- 2.1. Hospitality

- 2.2. Commercial Buildings

- 2.3. Public Buildings

- 2.4. Others

Canada Commercial HVAC Market Segmentation By Geography

- 1. Canada

Canada Commercial HVAC Market Regional Market Share

Geographic Coverage of Canada Commercial HVAC Market

Canada Commercial HVAC Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Component

- 5.1.1. HVAC Equipment

- 5.1.1.1. Heating Equipment

- 5.1.1.2. Air Conditioning /Ventillation Equipment

- 5.1.2. HVAC Services

- 5.1.1. HVAC Equipment

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Hospitality

- 5.2.2. Commercial Buildings

- 5.2.3. Public Buildings

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Type of Component

- 6. Canada Commercial HVAC Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Component

- 6.1.1. HVAC Equipment

- 6.1.1.1. Heating Equipment

- 6.1.1.2. Air Conditioning /Ventillation Equipment

- 6.1.2. HVAC Services

- 6.1.1. HVAC Equipment

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Hospitality

- 6.2.2. Commercial Buildings

- 6.2.3. Public Buildings

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type of Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Robert Bosch GmbH

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Carrier Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Panasonic Holdings Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Johnson Controls International PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Trane Technologies PLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Danfoss Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Panasonic Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mitsubishi Electric Hydronics & It Cooling Systems SpA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 LG Electronics Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Trox Gmb

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Robert Bosch GmbH

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Commercial HVAC Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Commercial HVAC Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Commercial HVAC Market Revenue Million Forecast, by Type of Component 2020 & 2033

- Table 2: Canada Commercial HVAC Market Volume Billion Forecast, by Type of Component 2020 & 2033

- Table 3: Canada Commercial HVAC Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Canada Commercial HVAC Market Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 5: Canada Commercial HVAC Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Canada Commercial HVAC Market Volume Billion Forecast, by Region 2020 & 2033

- Table 7: Canada Commercial HVAC Market Revenue Million Forecast, by Type of Component 2020 & 2033

- Table 8: Canada Commercial HVAC Market Volume Billion Forecast, by Type of Component 2020 & 2033

- Table 9: Canada Commercial HVAC Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 10: Canada Commercial HVAC Market Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 11: Canada Commercial HVAC Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Canada Commercial HVAC Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Commercial HVAC Market?

The projected CAGR is approximately 7.21%.

2. Which companies are prominent players in the Canada Commercial HVAC Market?

Key companies in the market include Robert Bosch GmbH, Carrier Corporation, Panasonic Holdings Corporation, Johnson Controls International PLC, Trane Technologies PLC, Danfoss Inc, Panasonic Corporation, Mitsubishi Electric Hydronics & It Cooling Systems SpA, LG Electronics Inc, Trox Gmb.

3. What are the main segments of the Canada Commercial HVAC Market?

The market segments include Type of Component, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand For Energy-efficient Devices; Growing Commercial Construction; Supportive Government Regulations. Including Incentives for Saving Energy through Tax Credit Programs.

6. What are the notable trends driving market growth?

Commercial Buildings is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Increasing Demand For Energy-efficient Devices; Growing Commercial Construction; Supportive Government Regulations. Including Incentives for Saving Energy through Tax Credit Programs.

8. Can you provide examples of recent developments in the market?

June 2024: Carrier, a division of Carrier Global Corporation, has introduced 'Carrier Cooling-as-a-Service,' a suite of solutions designed to assist commercial clients in streamlining the management of HVAC and other thermal systems, all in the face of the contemporary energy shift. This innovative portfolio from Carrier offers an alternative to conventional heating and cooling systems, shifting from the traditional upfront payment model to a more flexible subscription-based approach.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Commercial HVAC Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Commercial HVAC Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Commercial HVAC Market?

To stay informed about further developments, trends, and reports in the Canada Commercial HVAC Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence