Key Insights

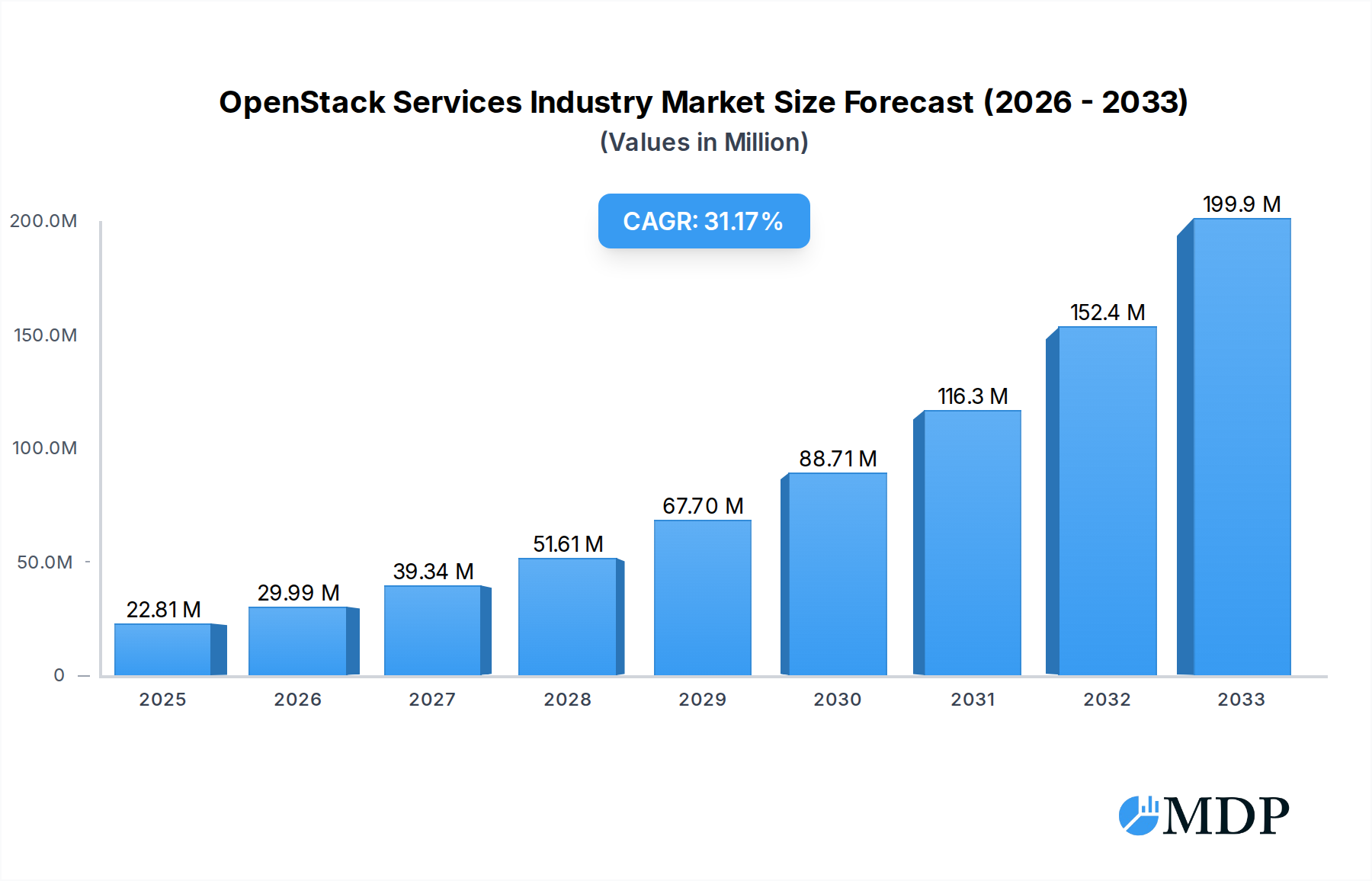

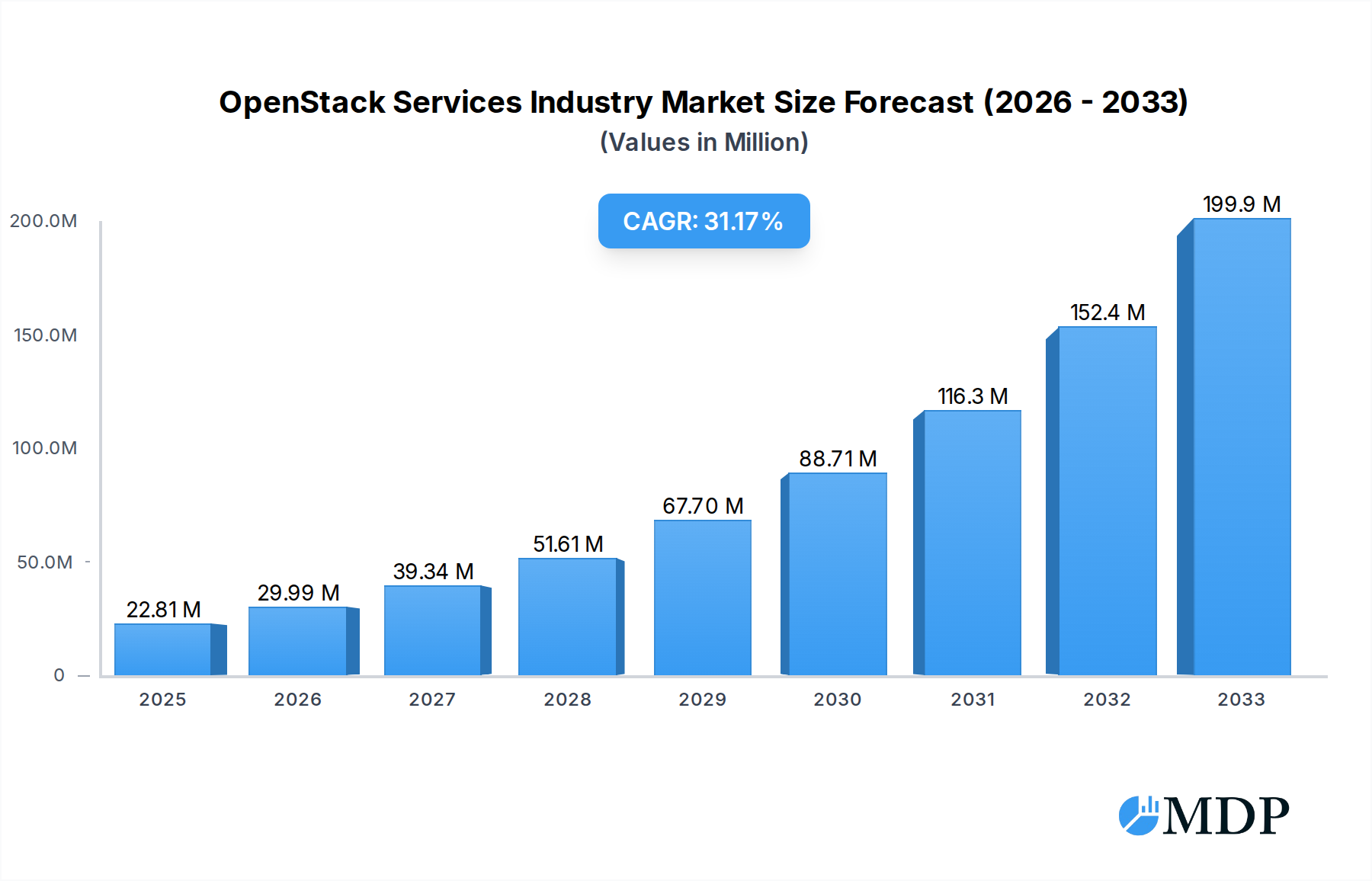

The OpenStack Services market is poised for remarkable expansion, projected to reach an impressive $22.81 million by the end of the forecast period. This significant growth is fueled by an CAGR of 32.01%, underscoring the escalating adoption of cloud computing and the increasing demand for flexible, scalable, and cost-effective private and hybrid cloud solutions. The core drivers behind this surge include the growing need for agility in IT infrastructure, enabling businesses to rapidly deploy and manage applications, and the inherent cost efficiencies offered by OpenStack solutions compared to proprietary alternatives. Furthermore, the increasing complexity of data management and the imperative for enhanced security within enterprises are pushing organizations towards robust and customizable cloud platforms like OpenStack. The market's trajectory is further bolstered by ongoing innovation in cloud-native technologies and the expanding ecosystem of OpenStack service providers, offering comprehensive support and managed services.

OpenStack Services Industry Market Size (In Million)

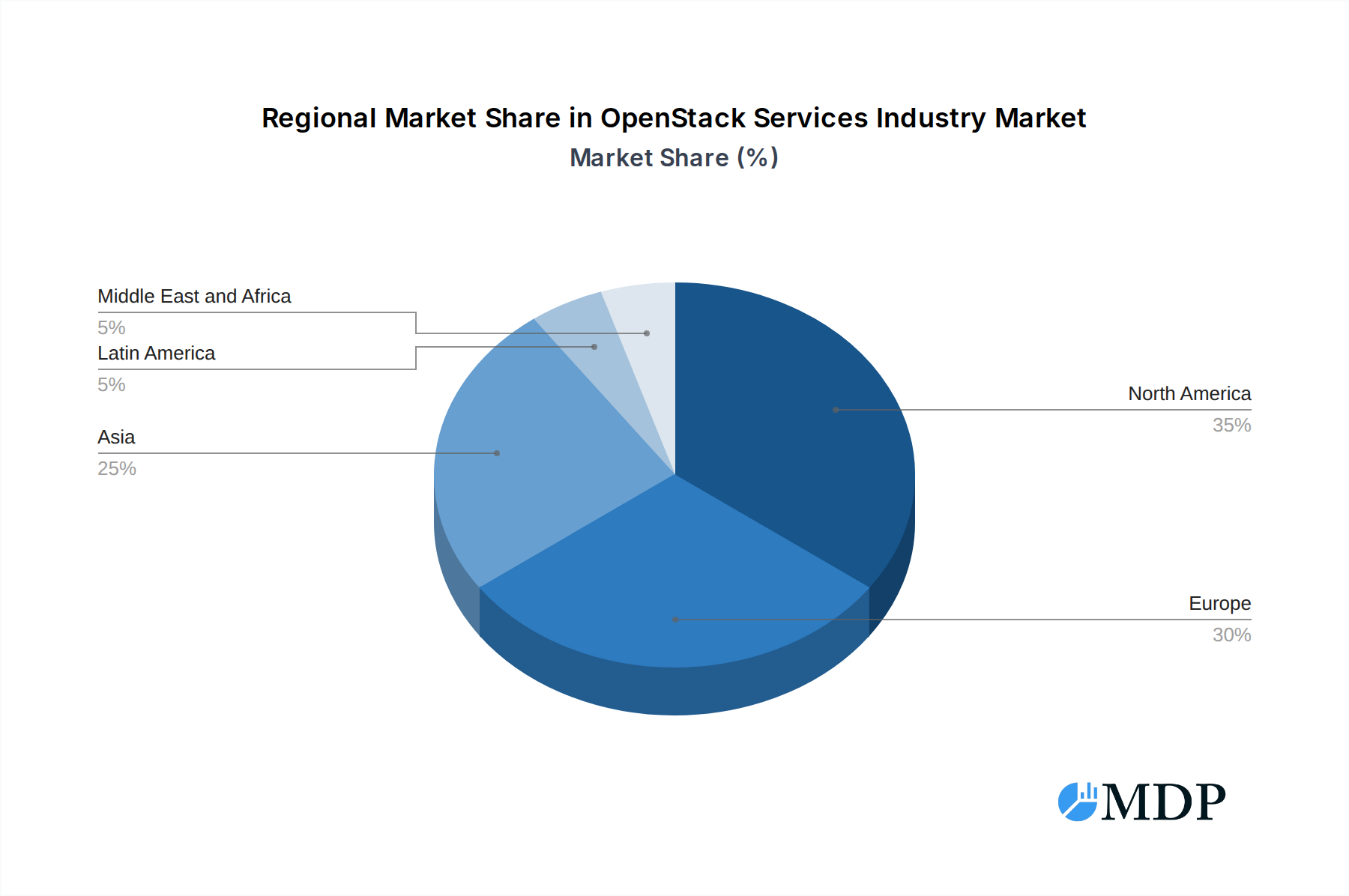

The market segmentation reveals a dynamic landscape with diverse adoption patterns across deployment models and end-user industries. The On-Cloud segment is expected to witness substantial growth, reflecting the broader shift towards cloud-native architectures. However, On-Premise deployments will continue to hold significance, particularly for organizations with stringent data sovereignty requirements or legacy system integration needs. In terms of end-user industries, Information Technology, Telecommunication, and Banking and Financial Services are leading the charge in OpenStack adoption due to their inherent reliance on scalable and secure IT infrastructure. The Academic sector is also increasingly leveraging OpenStack for research and educational purposes, while Retail/E-Commerce is capitalizing on its ability to handle fluctuating traffic and inventory demands. Geographically, while specific regional data is unavailable, North America and Europe are likely to remain dominant markets due to established IT infrastructure and early adoption trends. However, the Asia-Pacific region is anticipated to exhibit the fastest growth, driven by rapid digital transformation initiatives and increasing investments in cloud technologies. Emerging trends like edge computing integration and enhanced security features will further shape the OpenStack Services market landscape.

OpenStack Services Industry Company Market Share

**This in-depth report provides a critical analysis of the OpenStack Services Industry, offering unparalleled insights for stakeholders navigating the evolving landscape of cloud infrastructure solutions. Spanning the historical period of 2019–2024 and projecting to 2033, this study utilizes 2025 as its base and estimated year, with a robust forecast period from 2025–2033. Discover key market dynamics, emerging trends, leading segments, and the strategic imperatives driving growth in this vital sector. With a projected market size reaching *xx Million* by 2033, understanding OpenStack services is paramount for businesses seeking to optimize their IT operations, enhance scalability, and secure their digital future.**

This report is essential for IT decision-makers, cloud architects, solution providers, investors, and anyone seeking to understand the competitive intelligence, market share, and future trajectory of OpenStack services. We delve deep into the nuances of Open-Cloud, On-Premise deployments, and the specific needs of the Information Technology, Telecommunication, Banking and Financial Services, Academic, and Retail/E-Commerce sectors.

OpenStack Services Industry Market Dynamics & Concentration

The OpenStack Services Industry exhibits a moderate level of market concentration, characterized by the presence of both established technology giants and specialized service providers. Innovation drivers are primarily fueled by the increasing demand for private and hybrid cloud solutions, cost-efficiency, and the need for greater control over data sovereignty. Regulatory frameworks, particularly around data privacy and security, are increasingly influencing service offerings and deployment strategies. Product substitutes, such as proprietary cloud platforms and container orchestration services, present a competitive challenge, but OpenStack’s open-source nature and flexibility continue to attract a significant user base. End-user trends point towards a growing preference for managed OpenStack services, allowing organizations to focus on core competencies while leveraging scalable and customizable cloud infrastructure. Mergers and acquisitions (M&A) activities, while not as frenzied as in some other tech sectors, are strategic, aimed at consolidating market presence, expanding service portfolios, and acquiring specialized expertise. The market share distribution sees key players like Mirantis Inc. and Canonical Ltd. holding significant positions, alongside contributions from hardware vendors and system integrators. M&A deal counts are influenced by the need to integrate OpenStack capabilities with broader cloud management and automation tools.

- Market Concentration: Moderate, with a blend of large enterprises and niche players.

- Innovation Drivers: Cost-efficiency, data sovereignty, private/hybrid cloud demand, open-source flexibility.

- Regulatory Influence: Growing impact of data privacy and security compliance.

- Competitive Landscape: OpenStack competes with proprietary clouds and containerization technologies.

- End-User Trends: Increasing adoption of managed OpenStack services.

- M&A Activity: Strategic, focused on portfolio expansion and expertise acquisition.

- Estimated Market Share Snapshot (2025): Key players collectively holding over 70% of the managed services market.

- Estimated M&A Deal Volume (2025): 5-10 strategic acquisitions focused on technology integration.

OpenStack Services Industry Industry Trends & Analysis

The OpenStack Services Industry is experiencing robust growth, driven by a confluence of technological advancements and evolving business needs. The market's projected Compound Annual Growth Rate (CAGR) is estimated at xx%, indicating a sustained upward trajectory. This expansion is fueled by the increasing adoption of hybrid and multi-cloud strategies, where OpenStack serves as a crucial enabler for private cloud environments that can seamlessly integrate with public cloud services. Technological disruptions, such as the maturation of containerization technologies (e.g., Kubernetes) and advancements in AI/ML capabilities for cloud management, are reshaping the OpenStack ecosystem. While container orchestration is not a direct substitute, OpenStack's ability to provide underlying infrastructure for these platforms is becoming increasingly significant. Consumer preferences are shifting towards more user-friendly, automated, and managed OpenStack solutions, reducing the operational burden on IT teams. This has led to a surge in demand for comprehensive service offerings that encompass deployment, management, security, and support. Competitive dynamics are intensifying, with providers differentiating themselves through specialized industry solutions, enhanced security features, and superior support services. Market penetration for OpenStack services is steadily increasing across various industry verticals, with organizations recognizing its value proposition for agility, scalability, and cost optimization. The ongoing development of OpenStack's core components and the vibrant community support continue to foster innovation and adoption.

Leading Markets & Segments in OpenStack Services Industry

The OpenStack Services Industry demonstrates significant regional and sectoral dominance, with distinct segments driving market growth. The On-Cloud deployment model is emerging as the leading segment, driven by its inherent scalability, flexibility, and the ability to offer services with greater agility. This trend is particularly pronounced in regions with well-developed digital infrastructure and a strong emphasis on cloud adoption.

- Dominant Region: North America currently leads the market, propelled by a mature IT ecosystem, significant investments in cloud technologies, and a high concentration of enterprises across various sectors. Asia Pacific is projected to exhibit the fastest growth rate due to rapid digitalization and increasing cloud adoption in emerging economies.

- Leading Deployment Model:

- On-Cloud: This segment benefits from the growing demand for flexible, scalable, and readily accessible cloud infrastructure. Key drivers include the need for rapid deployment of applications, cost-effectiveness through pay-as-you-go models, and the ability to scale resources up or down based on demand.

- On-Premise: While On-Cloud is growing faster, the On-Premise segment remains crucial, particularly for organizations with stringent data sovereignty requirements, legacy application dependencies, or specific security mandates. Economic policies that favor local data storage and strict regulatory compliance in sectors like Banking and Financial Services are key drivers for this segment.

- Dominant End-User Industries:

- Information Technology (IT): This sector consistently leads in OpenStack adoption, utilizing it for private cloud infrastructure, development and testing environments, and to support their own service offerings. The need for agility, cost control, and the ability to manage complex IT landscapes are paramount.

- Telecommunication: With the advent of 5G and the increasing demand for edge computing, telecommunications companies are leveraging OpenStack for network function virtualization (NFV) and software-defined networking (SDN), enabling them to build more agile and programmable networks. Infrastructure investments and the drive for operational efficiency are significant growth catalysts.

- Banking and Financial Services (BFS): This industry is increasingly adopting OpenStack for its ability to provide secure, compliant, and cost-effective private cloud solutions. The stringent regulatory environment and the need for robust data security and disaster recovery capabilities make OpenStack an attractive option for modernizing their IT infrastructure. Compliance with financial regulations and the demand for digital transformation are key drivers.

- Academic: Educational institutions are utilizing OpenStack to build research clouds, facilitate data-intensive research projects, and provide scalable computing resources to students and faculty. Government grants and the need for cutting-edge research infrastructure contribute to growth.

- Retail/E-Commerce: This sector leverages OpenStack for scalable e-commerce platforms, inventory management systems, and data analytics to personalize customer experiences. The need to handle peak loads, manage large datasets, and provide seamless online shopping experiences drives adoption.

OpenStack Services Industry Product Developments

Recent product developments in the OpenStack Services Industry are focused on enhancing automation, security, and interoperability. Innovations are increasingly integrating OpenStack with container orchestration platforms, simplifying hybrid cloud deployments and offering greater application portability. Advanced features for multi-tenancy, self-service portals, and AI-driven operational insights are becoming standard, aiming to reduce management overhead and improve resource utilization. Competitive advantages are being built around specialized solutions for telecommunications (NFV/SDN), high-performance computing, and compliance-heavy industries, alongside robust partner ecosystems that offer extended functionality and support. The overarching trend is towards making OpenStack more accessible, intelligent, and seamlessly integrated with the broader cloud-native landscape, addressing evolving market demands for flexibility and efficiency.

Key Drivers of OpenStack Services Industry Growth

The OpenStack Services Industry is experiencing significant growth propelled by several key factors. The escalating demand for cost-effective private and hybrid cloud solutions remains a primary driver, as businesses seek to gain more control over their infrastructure while optimizing IT spend. The inherent flexibility and open-source nature of OpenStack allow for deep customization, catering to specific organizational needs and preventing vendor lock-in, a crucial factor for many enterprises. Furthermore, the burgeoning digital transformation initiatives across industries, from telecommunications modernizing their networks to financial services digitizing their offerings, necessitate scalable and agile infrastructure that OpenStack services provide. The increasing need for data sovereignty and compliance with stringent regulations also fuels adoption, particularly in sectors like BFS and government.

- Cost Optimization: OpenStack offers a compelling alternative to proprietary cloud solutions, reducing operational expenses and capital expenditure.

- Hybrid and Multi-Cloud Enablement: It acts as a foundational technology for building and managing hybrid and multi-cloud environments, offering seamless integration.

- Digital Transformation: The broad adoption of digital technologies requires scalable and flexible infrastructure, which OpenStack services readily provide.

- Data Sovereignty and Compliance: Organizations with strict data locality and regulatory requirements find OpenStack's control and customization capabilities essential.

- Vendor Lock-in Avoidance: The open-source nature provides freedom from vendor dependency, allowing greater strategic flexibility.

Challenges in the OpenStack Services Industry Market

Despite its strong growth trajectory, the OpenStack Services Industry faces several challenges that can impede its widespread adoption and market penetration. The complexity of managing and deploying OpenStack can be a significant barrier for organizations lacking specialized expertise, leading to a reliance on managed service providers, which can increase costs. Security concerns, while continuously addressed by the community, remain a point of apprehension for some enterprises, especially in highly regulated industries. Competition from mature public cloud providers, offering vast economies of scale and extensive feature sets, presents a formidable challenge. Additionally, the fragmented nature of the OpenStack ecosystem, with numerous projects and components, can sometimes lead to integration complexities and a steeper learning curve. Supply chain issues, particularly for hardware components in on-premise deployments, can also impact timely service delivery.

- Management Complexity: The technical expertise required for deployment and ongoing management can be a barrier.

- Security Perceptions: Persistent concerns, despite continuous improvements, regarding the security posture of open-source cloud platforms.

- Public Cloud Competition: Dominance and extensive offerings from major public cloud providers.

- Ecosystem Fragmentation: The vast array of projects can lead to integration challenges and a steep learning curve.

- Talent Shortage: A limited pool of skilled OpenStack professionals can impact service delivery and support.

Emerging Opportunities in OpenStack Services Industry

The OpenStack Services Industry is ripe with emerging opportunities, driven by technological innovation and evolving market demands. The increasing convergence of OpenStack with containerization technologies like Kubernetes presents a significant opportunity for providers to offer unified platforms for managing both virtual machines and containers, simplifying hybrid and multi-cloud operations. The growing adoption of edge computing in industries such as telecommunications and manufacturing creates a demand for localized, scalable, and resilient cloud infrastructure, where OpenStack can play a pivotal role. Furthermore, the development of AI and machine learning capabilities for automating cloud management, optimizing resource allocation, and enhancing security presents a lucrative area for service innovation. Strategic partnerships between OpenStack service providers, hardware vendors, and software developers are crucial for creating comprehensive, end-to-end solutions that address complex enterprise needs and unlock new market segments.

Leading Players in the OpenStack Services Industry Sector

The OpenStack Services Industry is shaped by a diverse group of leading players, each contributing unique strengths and solutions. These companies are instrumental in driving innovation, providing robust support, and expanding the reach of OpenStack technologies across various enterprise segments.

- Mirantis Inc

- Canonical Ltd

- NetApp Inc

- Cisco Systems Inc

- Rackspace US Inc

- Hewlett Packard Enterprise Development LP

- Red Hat Inc

- Dell Inc

- Huawei Technologies Co Ltd

- VMware Inc

- VEXXHOST Inc

Key Milestones in OpenStack Services Industry Industry

The OpenStack Services Industry has been marked by significant developments that have shaped its trajectory and continue to influence its evolution. These milestones highlight strategic partnerships, technological advancements, and product innovations.

- October 2023: UNICC is Partnered with Canonical, the publisher of Ubuntu and provider of open-source security, support and services, to build and deliver the secure private cloud environment for the UN system, offering advanced security and data sovereignty for the UN’s most sensitive data and software applications. This partnership underscores the growing trust in open-source solutions for critical government infrastructure and data protection.

- September 2022: New telecom operator-focused capabilities were introduced with the release of Red Hat's most recent version of its venerable OpenStack platform, tightening the connection between it and the company's cloud-native OpenShift platform. This development signifies a strategic push to empower telecommunications companies with enhanced capabilities for network virtualization and cloud-native deployments.

- June 2022: VEXXHOST Inc. announced the launch of Atmosphere, a new tool that can deploy a fully integrated OpenStack environment. Furthermore, the company has made the technology open source so that it benefits all of the users of the cloud-based infrastructure-as-a-service platform. This initiative democratizes OpenStack deployment and fosters wider community adoption and innovation.

Strategic Outlook for OpenStack Services Industry Market

The strategic outlook for the OpenStack Services Industry is highly positive, driven by ongoing digital transformation and the increasing demand for flexible, cost-effective, and secure cloud infrastructures. Growth accelerators will stem from the continued evolution of hybrid and multi-cloud strategies, where OpenStack serves as a critical enabler for private cloud environments. The industry will witness a greater emphasis on managed services, automation, and AI-driven operations, simplifying deployment and management for end-users. Opportunities will expand in niche markets such as edge computing and specialized industry solutions for telecommunications and financial services. Strategic partnerships and the integration of OpenStack with emerging technologies like Kubernetes and serverless computing will further solidify its position. By focusing on innovation in security, performance, and user experience, providers can capitalize on the sustained demand for robust and adaptable cloud infrastructure solutions, ensuring continued market expansion and value creation for stakeholders.

OpenStack Services Industry Segmentation

-

1. Deployment Model

- 1.1. On-Cloud

- 1.2. On-Premise

-

2. End-user Industry

- 2.1. Information Technology

- 2.2. Telecommunication

- 2.3. Banking and Financial Services

- 2.4. Academic

- 2.5. Retail/E-Commerce

OpenStack Services Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Latin America

- 5. Middle East and Africa

OpenStack Services Industry Regional Market Share

Geographic Coverage of OpenStack Services Industry

OpenStack Services Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 32.01% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment Model

- 5.1.1. On-Cloud

- 5.1.2. On-Premise

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Information Technology

- 5.2.2. Telecommunication

- 5.2.3. Banking and Financial Services

- 5.2.4. Academic

- 5.2.5. Retail/E-Commerce

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment Model

- 6. Global OpenStack Services Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment Model

- 6.1.1. On-Cloud

- 6.1.2. On-Premise

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Information Technology

- 6.2.2. Telecommunication

- 6.2.3. Banking and Financial Services

- 6.2.4. Academic

- 6.2.5. Retail/E-Commerce

- 6.1. Market Analysis, Insights and Forecast - by Deployment Model

- 7. North America OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment Model

- 7.1.1. On-Cloud

- 7.1.2. On-Premise

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Information Technology

- 7.2.2. Telecommunication

- 7.2.3. Banking and Financial Services

- 7.2.4. Academic

- 7.2.5. Retail/E-Commerce

- 7.1. Market Analysis, Insights and Forecast - by Deployment Model

- 8. Europe OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment Model

- 8.1.1. On-Cloud

- 8.1.2. On-Premise

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Information Technology

- 8.2.2. Telecommunication

- 8.2.3. Banking and Financial Services

- 8.2.4. Academic

- 8.2.5. Retail/E-Commerce

- 8.1. Market Analysis, Insights and Forecast - by Deployment Model

- 9. Asia OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment Model

- 9.1.1. On-Cloud

- 9.1.2. On-Premise

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Information Technology

- 9.2.2. Telecommunication

- 9.2.3. Banking and Financial Services

- 9.2.4. Academic

- 9.2.5. Retail/E-Commerce

- 9.1. Market Analysis, Insights and Forecast - by Deployment Model

- 10. Latin America OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment Model

- 10.1.1. On-Cloud

- 10.1.2. On-Premise

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Information Technology

- 10.2.2. Telecommunication

- 10.2.3. Banking and Financial Services

- 10.2.4. Academic

- 10.2.5. Retail/E-Commerce

- 10.1. Market Analysis, Insights and Forecast - by Deployment Model

- 11. Middle East and Africa OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Deployment Model

- 11.1.1. On-Cloud

- 11.1.2. On-Premise

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Information Technology

- 11.2.2. Telecommunication

- 11.2.3. Banking and Financial Services

- 11.2.4. Academic

- 11.2.5. Retail/E-Commerce

- 11.1. Market Analysis, Insights and Forecast - by Deployment Model

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Mirantis Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Canonical Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 NetApp Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cisco Systems Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Rackspace US Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hewlett Packard Enterprise Development LP

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Red Hat Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Dell Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Huawei Technologies Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 VMware Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Mirantis Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global OpenStack Services Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 3: North America OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 4: North America OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 5: North America OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 9: Europe OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 10: Europe OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 11: Europe OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 15: Asia OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 16: Asia OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 17: Asia OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 21: Latin America OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 22: Latin America OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Latin America OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Latin America OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 27: Middle East and Africa OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 28: Middle East and Africa OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 2: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global OpenStack Services Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 5: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 8: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 9: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 11: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 12: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 14: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 15: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 17: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 18: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the OpenStack Services Industry?

The projected CAGR is approximately 32.01%.

2. Which companies are prominent players in the OpenStack Services Industry?

Key companies in the market include Mirantis Inc, Canonical Ltd, NetApp Inc, Cisco Systems Inc, Rackspace US Inc, Hewlett Packard Enterprise Development LP, Red Hat Inc, Dell Inc, Huawei Technologies Co Ltd, VMware Inc.

3. What are the main segments of the OpenStack Services Industry?

The market segments include Deployment Model, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 22.81 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Organizations to Improve Their Business Agility and Efficiency; OpenStack Being Open Source Provides the Flexibility for Customized Solution; Increasing use of OpenStack Services in Telecommunication Sector.

6. What are the notable trends driving market growth?

Increasing use of OpenStack Services in Telecommunication Sector is Driving the Market.

7. Are there any restraints impacting market growth?

Lack of Robustness that Enterprises Desire for Their Data Centers. Including IT Management Features. Such as Availability and Security.

8. Can you provide examples of recent developments in the market?

October 2023 - UNICC is Partnered with Canonical, the publisher of Ubuntu and provider of open-source security, support and services, to build and deliver the secure private cloud environment for the UN system, offering advanced security and data sovereignty for the UN’s most sensitive data and software applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "OpenStack Services Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the OpenStack Services Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the OpenStack Services Industry?

To stay informed about further developments, trends, and reports in the OpenStack Services Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence