Key Insights

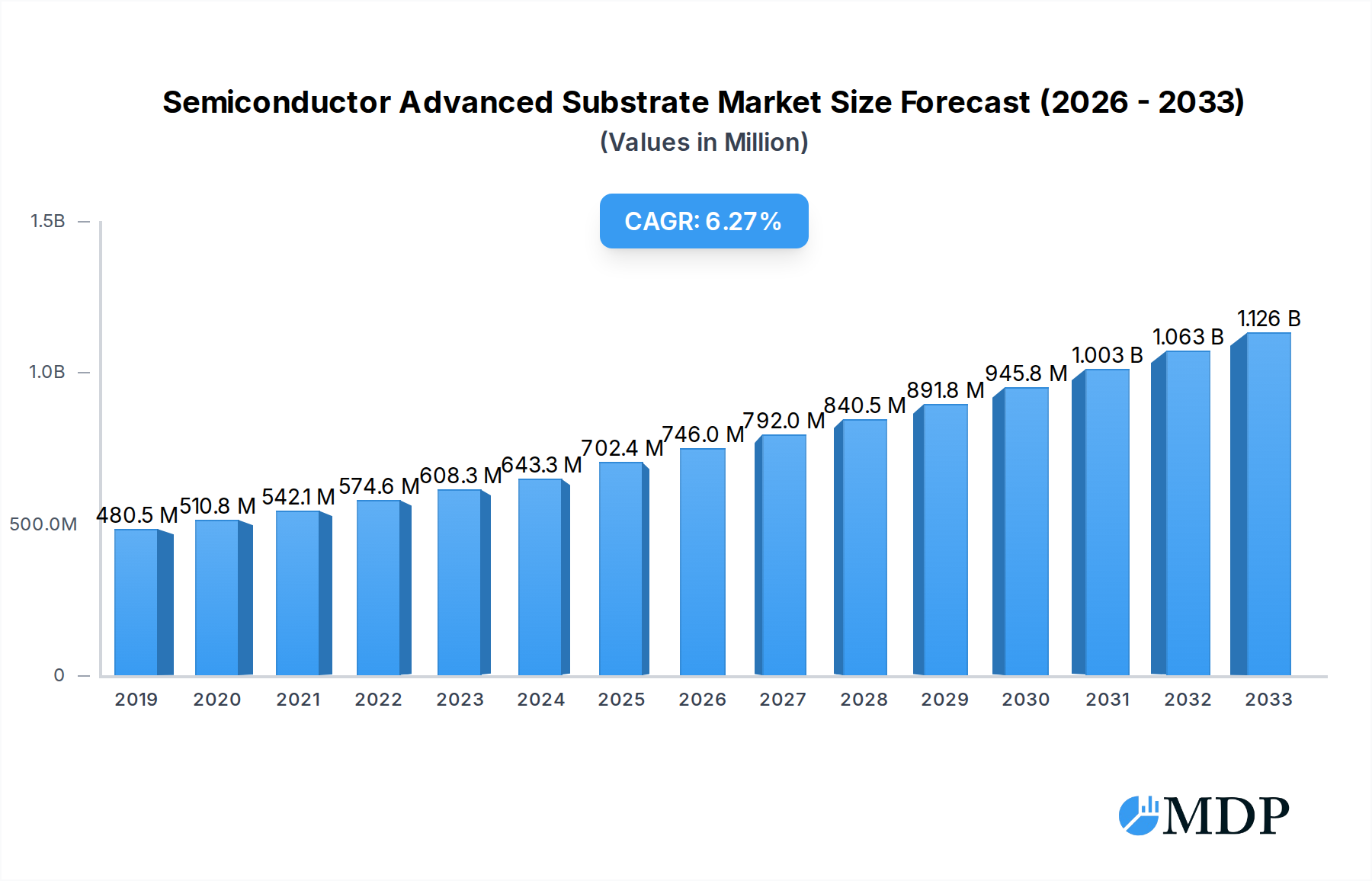

The global Semiconductor Advanced Substrate Market is poised for robust expansion, projected to reach $702.44 billion by 2025, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 6.25% from 2019 to 2033. This significant market valuation underscores the increasing demand for sophisticated semiconductor packaging solutions essential for next-generation electronic devices. Key growth drivers fueling this surge include the relentless innovation in consumer electronics, the burgeoning Internet of Things (IoT) ecosystem, and the rapid advancements in artificial intelligence (AI) and high-performance computing (HPC). As devices become smaller, more powerful, and more interconnected, the need for advanced substrates that can support higher density interconnects, improved thermal management, and enhanced signal integrity becomes paramount. This trend is further amplified by the automotive sector's growing reliance on advanced driver-assistance systems (ADAS) and the increasing electrification of vehicles, both of which necessitate sophisticated semiconductor components.

Semiconductor Advanced Substrate Market Market Size (In Million)

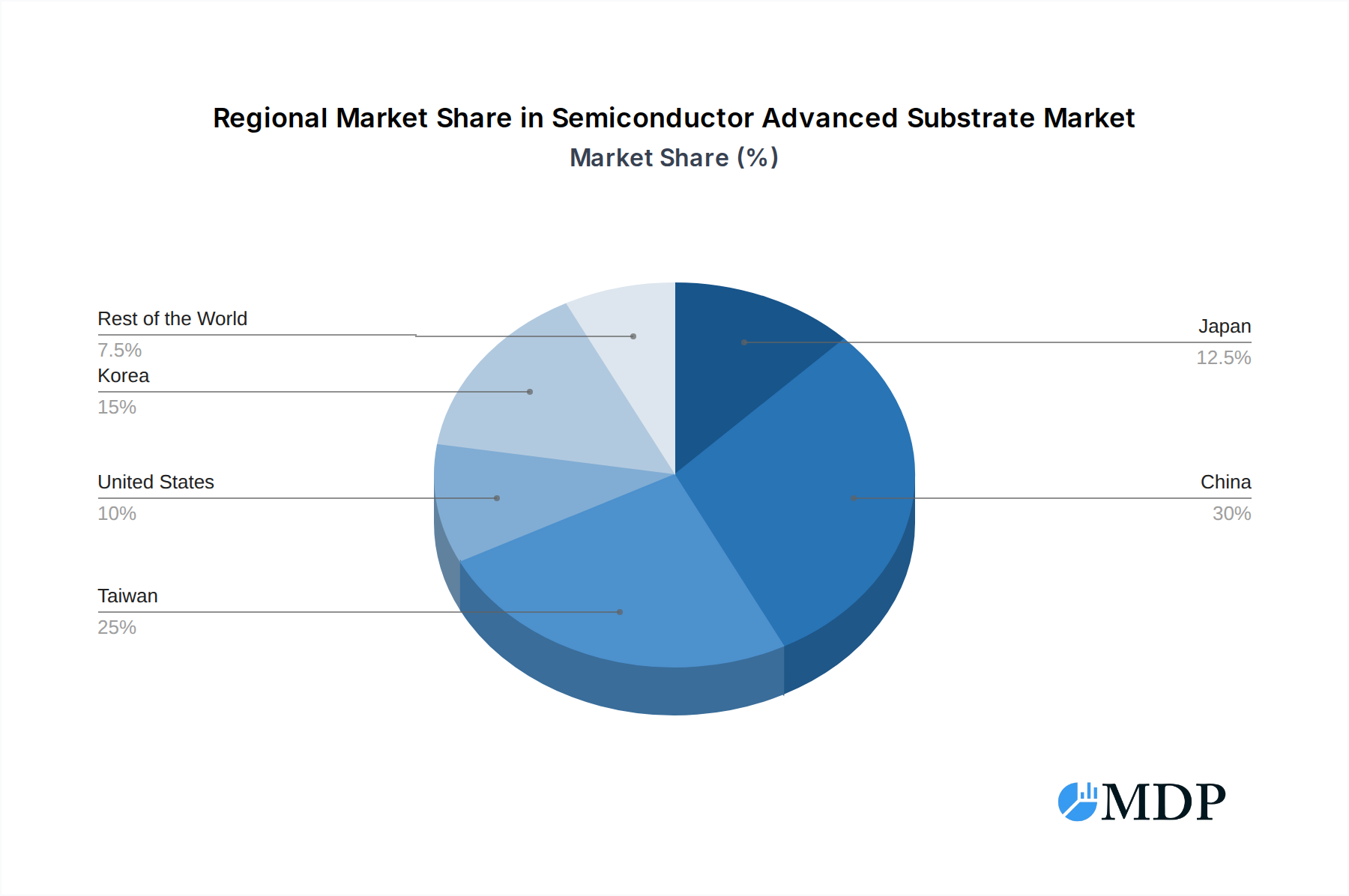

The market is segmented into several critical areas, highlighting distinct growth trajectories. The Advanced IC Substrate segment, encompassing FC BGA (Flip-Chip Ball Grid Array) and FC CSP (Flip-Chip Chip Scale Package), is a major contributor, driven by the demand for high-performance processors and memory modules in computing and mobile devices. Substrate-like PCBs (SLPs) are experiencing substantial growth, particularly for smartphone applications, where miniaturization and advanced functionalities are critical. The Embedded Die segment is also gaining traction, especially within the mobile and automotive industries, offering solutions for compact and efficient electronic designs. Geographically, Asia-Pacific, led by China and Taiwan, is expected to maintain its dominance due to the concentration of semiconductor manufacturing and assembly operations. However, regions like Japan, the United States, and Korea are also significant players, driven by their strong R&D capabilities and the presence of leading semiconductor companies. Emerging markets and increasing adoption of advanced electronics in various end-user applications worldwide will also contribute to the market's overall expansion.

Semiconductor Advanced Substrate Market Company Market Share

Semiconductor Advanced Substrate Market: Navigating the Future of Integrated Circuits - In-Depth Analysis & Forecast (2019-2033)

Uncover the dynamic landscape of the Semiconductor Advanced Substrate Market with this comprehensive, SEO-optimized report. Dive deep into the critical role of advanced substrates in powering next-generation semiconductor devices, from high-performance computing and AI to cutting-edge mobile technology. This report provides actionable insights for industry stakeholders, investors, and manufacturers seeking to capitalize on the burgeoning demand for sophisticated semiconductor packaging solutions. With a study period spanning 2019 to 2033 and a base year of 2025, our analysis leverages historical data, current trends, and robust forecasts to deliver unparalleled market intelligence.

Semiconductor Advanced Substrate Market Market Dynamics & Concentration

The global Semiconductor Advanced Substrate Market is characterized by a moderate to high concentration, driven by significant capital investment, complex manufacturing processes, and stringent quality control requirements. Key innovation drivers include the relentless pursuit of miniaturization, enhanced performance, and increased power efficiency in semiconductor devices. Regulatory frameworks, particularly concerning environmental impact and supply chain security, are increasingly shaping market entry and operational strategies. Product substitutes, such as advanced packaging technologies not relying on traditional substrates, represent an evolving competitive threat. End-user trends are overwhelmingly focused on demand for higher computing power and lower latency in applications like artificial intelligence, 5G, automotive electronics, and advanced consumer devices. Merger and acquisition (M&A) activities are sporadic but strategic, often aimed at consolidating technological expertise, expanding production capacity, or securing market share in niche segments. For instance, recent M&A activities indicate a trend towards vertical integration and strategic partnerships to gain a competitive edge. The market share distribution among the top players is a key indicator of its concentrated nature, with a few dominant companies holding a significant portion of the global market. The number of M&A deals, while not always high in volume, often involves substantial valuations, reflecting the strategic importance of advanced substrate manufacturers.

- Market Concentration: Moderate to High.

- Innovation Drivers: Miniaturization, performance enhancement, power efficiency.

- Regulatory Frameworks: Environmental regulations, supply chain security.

- Product Substitutes: Evolving advanced packaging technologies.

- End-User Trends: Demand for AI, 5G, automotive, advanced consumer devices.

- M&A Activities: Strategic consolidations and partnerships.

Semiconductor Advanced Substrate Market Industry Trends & Analysis

The Semiconductor Advanced Substrate Market is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 10.5% during the forecast period of 2025–2033. This expansion is primarily fueled by the escalating demand for sophisticated semiconductor components across a multitude of high-growth industries. Technological disruptions are at the forefront, with the increasing complexity of integrated circuits necessitating advanced substrates capable of handling higher interconnect densities, finer line widths, and more complex thermal management. The relentless miniaturization trend, driven by the need for smaller and more powerful electronic devices, directly translates to a demand for thinner, lighter, and more performant substrates. Consumer preferences are shifting towards devices with enhanced functionalities and superior performance, pushing semiconductor manufacturers to innovate at an unprecedented pace, which in turn drives the demand for advanced substrates. Competitive dynamics within the market are intense, with leading players investing heavily in research and development to maintain their technological edge and secure long-term contracts with major chip manufacturers. The increasing adoption of advanced IC substrates, particularly Flip-Chip Ball Grid Array (FC BGA) and Flip-Chip Chip Scale Package (FC CSP), is a significant market penetration driver. Furthermore, the Substrate-like PCB (SLP) segment, crucial for smartphone innovation, continues to expand its market presence. Embedded Die technologies are also gaining traction, especially in the mobile and automotive sectors, as they offer significant advantages in terms of form factor and performance. The market penetration of these advanced substrate technologies is expected to accelerate as their benefits become more widely recognized and integrated into new product designs. The overall market penetration for advanced substrates is estimated to grow from around 55% in 2024 to over 75% by 2033, indicating a substantial shift towards these superior solutions.

Leading Markets & Segments in Semiconductor Advanced Substrate Market

The Semiconductor Advanced Substrate Market is witnessing significant dominance from Asia-Pacific, with China, Taiwan, and Japan leading the charge in both production and consumption. China's vast manufacturing ecosystem and increasing investment in domestic semiconductor capabilities, coupled with supportive government policies and infrastructure development, have positioned it as a pivotal market. Taiwan, home to world-leading foundries and packaging houses, continues to be a powerhouse in advanced substrate manufacturing, particularly for high-end IC substrates. Japan, with its established technological prowess and strong presence in advanced materials science, also plays a critical role.

Within the Platform segment, Advanced IC Substrate is the dominant category, driven by the explosive growth in demand for high-performance computing, artificial intelligence, and 5G infrastructure. Specifically, FC BGA substrates are experiencing unparalleled demand due to their suitability for high-density interconnects and advanced packaging of complex processors and GPUs. The Substrate-like-PCB (SLP) segment remains crucial for the Smartphone end-user application, enabling the miniaturization and enhanced functionalities of modern mobile devices. While SLP is primarily associated with smartphones, the "Others (Tablets and Smartwatches)" sub-segment is also experiencing steady growth as these devices become more sophisticated. The Embedded Die segment is witnessing significant traction in the Mobile and Automotive sectors. In mobile, embedded die solutions allow for further space optimization and improved performance in compact devices. The automotive industry's increasing reliance on advanced driver-assistance systems (ADAS), infotainment, and electrification is creating substantial demand for embedded die technologies due to their reliability and space-saving attributes.

- Dominant Geography: Asia-Pacific (China, Taiwan, Japan).

- Key Drivers: Extensive manufacturing capabilities, government support, technological innovation, robust electronics industry ecosystem.

- Dominant Platform Segment: Advanced IC Substrate.

- Key Drivers for FC BGA: High-density interconnects, advanced processors, GPUs, AI chips.

- Key Drivers for FC CSP: Miniaturization, improved electrical performance in smaller packages.

- Dominant End-User Application (SLP): Smartphone.

- Key Drivers: Miniaturization, enhanced features, multi-functionality.

- Growth in Others (Tablets and Smartwatches): Increasing complexity and feature sets.

- Emerging Segment: Embedded Die.

- Key Drivers for Mobile: Space optimization, performance enhancement.

- Key Drivers for Automotive: ADAS, electrification, infotainment systems, reliability.

Semiconductor Advanced Substrate Market Product Developments

The Semiconductor Advanced Substrate Market is a hotbed of product innovation, driven by the demand for increasingly sophisticated semiconductor devices. Manufacturers are focusing on developing thinner, lighter, and more thermally efficient substrates with higher density interconnect capabilities. Key advancements include the widespread adoption of organic substrates for FC BGA applications, offering a balance of performance and cost-effectiveness. Substrate-like PCBs (SLPs) continue to evolve, enabling finer line and space designs crucial for next-generation smartphones. Furthermore, innovation in embedded die technologies is enhancing integration and performance for mobile and automotive applications. These developments are crucial for enabling smaller, faster, and more power-efficient electronic components across various end markets.

Key Drivers of Semiconductor Advanced Substrate Market Growth

The growth of the Semiconductor Advanced Substrate Market is propelled by several interconnected factors. Technologically, the relentless drive for higher processing power, smaller form factors, and enhanced energy efficiency in semiconductors is paramount. Economic drivers include the booming demand for advanced electronics in sectors like artificial intelligence, 5G communications, automotive electrification, and high-performance computing. Regulatory factors, such as government initiatives to bolster domestic semiconductor manufacturing and supply chain resilience, are also contributing to market expansion. The increasing complexity of ICs, requiring advanced packaging solutions, directly fuels the need for sophisticated substrates.

- Technological Advancements: Demand for higher performance, miniaturization, and power efficiency in semiconductors.

- End-Market Growth: Expansion of AI, 5G, automotive, and HPC sectors.

- Government Initiatives: Support for domestic semiconductor production and supply chain security.

- IC Complexity: Need for advanced substrates to accommodate intricate chip designs.

Challenges in the Semiconductor Advanced Substrate Market Market

Despite its strong growth trajectory, the Semiconductor Advanced Substrate Market faces several significant challenges. Regulatory hurdles, particularly concerning environmental compliance and the sourcing of raw materials, can impact production costs and timelines. Supply chain issues, exacerbated by geopolitical tensions and natural disasters, continue to pose risks to material availability and lead times. Intense competitive pressures among established players and emerging competitors necessitate continuous innovation and cost optimization. Furthermore, the high capital expenditure required for advanced substrate manufacturing creates substantial barriers to entry for new players. The cyclical nature of the semiconductor industry, with its periods of boom and bust, can also present financial challenges.

- Regulatory Hurdles: Environmental compliance and material sourcing regulations.

- Supply Chain Disruptions: Geopolitical risks, natural disasters, material availability.

- Competitive Pressures: Intense competition requiring constant innovation.

- High Capital Expenditure: Significant investment needed for advanced manufacturing.

- Industry Cyclicality: Fluctuations in semiconductor demand.

Emerging Opportunities in Semiconductor Advanced Substrate Market

The Semiconductor Advanced Substrate Market presents numerous emerging opportunities driven by ongoing technological advancements and evolving market demands. The rapid growth of artificial intelligence and machine learning applications is creating a substantial demand for high-performance IC substrates capable of handling massive data processing and complex computations. The ongoing transition to electric vehicles and the increasing adoption of autonomous driving technologies are fueling the need for specialized, high-reliability substrates in automotive electronics. Furthermore, the expansion of the Internet of Things (IoT) ecosystem, with its proliferation of connected devices, will necessitate miniaturized and cost-effective substrate solutions. Strategic partnerships between substrate manufacturers and leading semiconductor companies, as well as investments in next-generation materials and manufacturing processes, represent significant growth catalysts.

Leading Players in the Semiconductor Advanced Substrate Market Sector

- Young Poong Group

- Nippon Mektron

- Unimicron

- Korea Circuit

- AT&S

- Hannstar

- Zhen Ding Tech

- Samsung Electro-Mechanics

- IBIDEN

- Daeduck Electronics

- TTM Technologies

- Compeg

- LG Innotek

Key Milestones in Semiconductor Advanced Substrate Market Industry

- February 2023: TTM Technologies announced its exhibit at the 2023 International Electronics Circuit Exhibition (Shenzhen), showcasing cutting-edge engineering and product solutions designed to address customer challenges across diverse end markets and applications.

- November 2023: AT&S announced its provision of IC substrates for global semiconductor company AMD. These substrates are integral to AMD's high-performance, energy-efficient data center processors, powering future digital experiences, from AI to VR.

Strategic Outlook for Semiconductor Advanced Substrate Market Market

The strategic outlook for the Semiconductor Advanced Substrate Market is overwhelmingly positive, driven by the accelerating pace of technological innovation and the burgeoning demand from critical end markets. The sustained growth in artificial intelligence, 5G deployment, and the electrification of the automotive sector will continue to be major growth accelerators. Manufacturers that can invest in advanced R&D, focusing on substrate technologies that enable higher density interconnects, superior thermal management, and enhanced reliability, will be well-positioned for success. Strategic partnerships and collaborations, particularly with leading semiconductor designers and fabless companies, will be crucial for co-developing solutions that meet future industry needs. Furthermore, a focus on sustainable manufacturing practices and resilient supply chain management will be increasingly important for long-term viability and market leadership. The market is poised for significant expansion, offering substantial opportunities for companies that can adapt to evolving technological demands and market dynamics.

Semiconductor Advanced Substrate Market Segmentation

-

1. Platform

-

1.1. Advanced IC Substrate

-

1.1.1. Product Category

- 1.1.1.1. FC BGA

- 1.1.1.2. FC CSP

-

1.1.1. Product Category

-

1.2. Substrate-like-PCB (SLP)

-

1.2.1. End-User Application

- 1.2.1.1. Smartphone

- 1.2.1.2. Others (Tablets and Smartwatches)

-

1.2.1. End-User Application

-

1.3. Embedded Die

- 1.3.1. Mobile

- 1.3.2. Automotive

-

1.1. Advanced IC Substrate

-

2. Geography

- 2.1. Japan

- 2.2. China

- 2.3. Taiwan

- 2.4. United States

- 2.5. Korea

- 2.6. Rest of the World

Semiconductor Advanced Substrate Market Segmentation By Geography

- 1. Japan

- 2. China

- 3. Taiwan

- 4. United States

- 5. Korea

- 6. Rest of the World

Semiconductor Advanced Substrate Market Regional Market Share

Geographic Coverage of Semiconductor Advanced Substrate Market

Semiconductor Advanced Substrate Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Platform

- 5.1.1. Advanced IC Substrate

- 5.1.1.1. Product Category

- 5.1.1.1.1. FC BGA

- 5.1.1.1.2. FC CSP

- 5.1.1.1. Product Category

- 5.1.2. Substrate-like-PCB (SLP)

- 5.1.2.1. End-User Application

- 5.1.2.1.1. Smartphone

- 5.1.2.1.2. Others (Tablets and Smartwatches)

- 5.1.2.1. End-User Application

- 5.1.3. Embedded Die

- 5.1.3.1. Mobile

- 5.1.3.2. Automotive

- 5.1.1. Advanced IC Substrate

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. Japan

- 5.2.2. China

- 5.2.3. Taiwan

- 5.2.4. United States

- 5.2.5. Korea

- 5.2.6. Rest of the World

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Japan

- 5.3.2. China

- 5.3.3. Taiwan

- 5.3.4. United States

- 5.3.5. Korea

- 5.3.6. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Platform

- 6. Global Semiconductor Advanced Substrate Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Platform

- 6.1.1. Advanced IC Substrate

- 6.1.1.1. Product Category

- 6.1.1.1.1. FC BGA

- 6.1.1.1.2. FC CSP

- 6.1.1.1. Product Category

- 6.1.2. Substrate-like-PCB (SLP)

- 6.1.2.1. End-User Application

- 6.1.2.1.1. Smartphone

- 6.1.2.1.2. Others (Tablets and Smartwatches)

- 6.1.2.1. End-User Application

- 6.1.3. Embedded Die

- 6.1.3.1. Mobile

- 6.1.3.2. Automotive

- 6.1.1. Advanced IC Substrate

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. Japan

- 6.2.2. China

- 6.2.3. Taiwan

- 6.2.4. United States

- 6.2.5. Korea

- 6.2.6. Rest of the World

- 6.1. Market Analysis, Insights and Forecast - by Platform

- 7. Japan Semiconductor Advanced Substrate Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Platform

- 7.1.1. Advanced IC Substrate

- 7.1.1.1. Product Category

- 7.1.1.1.1. FC BGA

- 7.1.1.1.2. FC CSP

- 7.1.1.1. Product Category

- 7.1.2. Substrate-like-PCB (SLP)

- 7.1.2.1. End-User Application

- 7.1.2.1.1. Smartphone

- 7.1.2.1.2. Others (Tablets and Smartwatches)

- 7.1.2.1. End-User Application

- 7.1.3. Embedded Die

- 7.1.3.1. Mobile

- 7.1.3.2. Automotive

- 7.1.1. Advanced IC Substrate

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. Japan

- 7.2.2. China

- 7.2.3. Taiwan

- 7.2.4. United States

- 7.2.5. Korea

- 7.2.6. Rest of the World

- 7.1. Market Analysis, Insights and Forecast - by Platform

- 8. China Semiconductor Advanced Substrate Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Platform

- 8.1.1. Advanced IC Substrate

- 8.1.1.1. Product Category

- 8.1.1.1.1. FC BGA

- 8.1.1.1.2. FC CSP

- 8.1.1.1. Product Category

- 8.1.2. Substrate-like-PCB (SLP)

- 8.1.2.1. End-User Application

- 8.1.2.1.1. Smartphone

- 8.1.2.1.2. Others (Tablets and Smartwatches)

- 8.1.2.1. End-User Application

- 8.1.3. Embedded Die

- 8.1.3.1. Mobile

- 8.1.3.2. Automotive

- 8.1.1. Advanced IC Substrate

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. Japan

- 8.2.2. China

- 8.2.3. Taiwan

- 8.2.4. United States

- 8.2.5. Korea

- 8.2.6. Rest of the World

- 8.1. Market Analysis, Insights and Forecast - by Platform

- 9. Taiwan Semiconductor Advanced Substrate Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Platform

- 9.1.1. Advanced IC Substrate

- 9.1.1.1. Product Category

- 9.1.1.1.1. FC BGA

- 9.1.1.1.2. FC CSP

- 9.1.1.1. Product Category

- 9.1.2. Substrate-like-PCB (SLP)

- 9.1.2.1. End-User Application

- 9.1.2.1.1. Smartphone

- 9.1.2.1.2. Others (Tablets and Smartwatches)

- 9.1.2.1. End-User Application

- 9.1.3. Embedded Die

- 9.1.3.1. Mobile

- 9.1.3.2. Automotive

- 9.1.1. Advanced IC Substrate

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. Japan

- 9.2.2. China

- 9.2.3. Taiwan

- 9.2.4. United States

- 9.2.5. Korea

- 9.2.6. Rest of the World

- 9.1. Market Analysis, Insights and Forecast - by Platform

- 10. United States Semiconductor Advanced Substrate Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Platform

- 10.1.1. Advanced IC Substrate

- 10.1.1.1. Product Category

- 10.1.1.1.1. FC BGA

- 10.1.1.1.2. FC CSP

- 10.1.1.1. Product Category

- 10.1.2. Substrate-like-PCB (SLP)

- 10.1.2.1. End-User Application

- 10.1.2.1.1. Smartphone

- 10.1.2.1.2. Others (Tablets and Smartwatches)

- 10.1.2.1. End-User Application

- 10.1.3. Embedded Die

- 10.1.3.1. Mobile

- 10.1.3.2. Automotive

- 10.1.1. Advanced IC Substrate

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. Japan

- 10.2.2. China

- 10.2.3. Taiwan

- 10.2.4. United States

- 10.2.5. Korea

- 10.2.6. Rest of the World

- 10.1. Market Analysis, Insights and Forecast - by Platform

- 11. Korea Semiconductor Advanced Substrate Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Platform

- 11.1.1. Advanced IC Substrate

- 11.1.1.1. Product Category

- 11.1.1.1.1. FC BGA

- 11.1.1.1.2. FC CSP

- 11.1.1.1. Product Category

- 11.1.2. Substrate-like-PCB (SLP)

- 11.1.2.1. End-User Application

- 11.1.2.1.1. Smartphone

- 11.1.2.1.2. Others (Tablets and Smartwatches)

- 11.1.2.1. End-User Application

- 11.1.3. Embedded Die

- 11.1.3.1. Mobile

- 11.1.3.2. Automotive

- 11.1.1. Advanced IC Substrate

- 11.2. Market Analysis, Insights and Forecast - by Geography

- 11.2.1. Japan

- 11.2.2. China

- 11.2.3. Taiwan

- 11.2.4. United States

- 11.2.5. Korea

- 11.2.6. Rest of the World

- 11.1. Market Analysis, Insights and Forecast - by Platform

- 12. Rest of the World Semiconductor Advanced Substrate Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Platform

- 12.1.1. Advanced IC Substrate

- 12.1.1.1. Product Category

- 12.1.1.1.1. FC BGA

- 12.1.1.1.2. FC CSP

- 12.1.1.1. Product Category

- 12.1.2. Substrate-like-PCB (SLP)

- 12.1.2.1. End-User Application

- 12.1.2.1.1. Smartphone

- 12.1.2.1.2. Others (Tablets and Smartwatches)

- 12.1.2.1. End-User Application

- 12.1.3. Embedded Die

- 12.1.3.1. Mobile

- 12.1.3.2. Automotive

- 12.1.1. Advanced IC Substrate

- 12.2. Market Analysis, Insights and Forecast - by Geography

- 12.2.1. Japan

- 12.2.2. China

- 12.2.3. Taiwan

- 12.2.4. United States

- 12.2.5. Korea

- 12.2.6. Rest of the World

- 12.1. Market Analysis, Insights and Forecast - by Platform

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Young Poong Group

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Nippon Mektron

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Unimicron

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Korea Circuit

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 AT&S

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Hannstar

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Zhen Ding Tech

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Samsung Electro-Mechanics

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 IBIDEN

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Daeduck Electronics*List Not Exhaustive

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 TTM Technologies

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Compeg

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 LG Innotek

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.1 Young Poong Group

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Semiconductor Advanced Substrate Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Japan Semiconductor Advanced Substrate Market Revenue (billion), by Platform 2025 & 2033

- Figure 3: Japan Semiconductor Advanced Substrate Market Revenue Share (%), by Platform 2025 & 2033

- Figure 4: Japan Semiconductor Advanced Substrate Market Revenue (billion), by Geography 2025 & 2033

- Figure 5: Japan Semiconductor Advanced Substrate Market Revenue Share (%), by Geography 2025 & 2033

- Figure 6: Japan Semiconductor Advanced Substrate Market Revenue (billion), by Country 2025 & 2033

- Figure 7: Japan Semiconductor Advanced Substrate Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: China Semiconductor Advanced Substrate Market Revenue (billion), by Platform 2025 & 2033

- Figure 9: China Semiconductor Advanced Substrate Market Revenue Share (%), by Platform 2025 & 2033

- Figure 10: China Semiconductor Advanced Substrate Market Revenue (billion), by Geography 2025 & 2033

- Figure 11: China Semiconductor Advanced Substrate Market Revenue Share (%), by Geography 2025 & 2033

- Figure 12: China Semiconductor Advanced Substrate Market Revenue (billion), by Country 2025 & 2033

- Figure 13: China Semiconductor Advanced Substrate Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Taiwan Semiconductor Advanced Substrate Market Revenue (billion), by Platform 2025 & 2033

- Figure 15: Taiwan Semiconductor Advanced Substrate Market Revenue Share (%), by Platform 2025 & 2033

- Figure 16: Taiwan Semiconductor Advanced Substrate Market Revenue (billion), by Geography 2025 & 2033

- Figure 17: Taiwan Semiconductor Advanced Substrate Market Revenue Share (%), by Geography 2025 & 2033

- Figure 18: Taiwan Semiconductor Advanced Substrate Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Taiwan Semiconductor Advanced Substrate Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: United States Semiconductor Advanced Substrate Market Revenue (billion), by Platform 2025 & 2033

- Figure 21: United States Semiconductor Advanced Substrate Market Revenue Share (%), by Platform 2025 & 2033

- Figure 22: United States Semiconductor Advanced Substrate Market Revenue (billion), by Geography 2025 & 2033

- Figure 23: United States Semiconductor Advanced Substrate Market Revenue Share (%), by Geography 2025 & 2033

- Figure 24: United States Semiconductor Advanced Substrate Market Revenue (billion), by Country 2025 & 2033

- Figure 25: United States Semiconductor Advanced Substrate Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Korea Semiconductor Advanced Substrate Market Revenue (billion), by Platform 2025 & 2033

- Figure 27: Korea Semiconductor Advanced Substrate Market Revenue Share (%), by Platform 2025 & 2033

- Figure 28: Korea Semiconductor Advanced Substrate Market Revenue (billion), by Geography 2025 & 2033

- Figure 29: Korea Semiconductor Advanced Substrate Market Revenue Share (%), by Geography 2025 & 2033

- Figure 30: Korea Semiconductor Advanced Substrate Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Korea Semiconductor Advanced Substrate Market Revenue Share (%), by Country 2025 & 2033

- Figure 32: Rest of the World Semiconductor Advanced Substrate Market Revenue (billion), by Platform 2025 & 2033

- Figure 33: Rest of the World Semiconductor Advanced Substrate Market Revenue Share (%), by Platform 2025 & 2033

- Figure 34: Rest of the World Semiconductor Advanced Substrate Market Revenue (billion), by Geography 2025 & 2033

- Figure 35: Rest of the World Semiconductor Advanced Substrate Market Revenue Share (%), by Geography 2025 & 2033

- Figure 36: Rest of the World Semiconductor Advanced Substrate Market Revenue (billion), by Country 2025 & 2033

- Figure 37: Rest of the World Semiconductor Advanced Substrate Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 2: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 3: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 5: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 8: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 9: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 11: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 14: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 17: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 18: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 20: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 21: Global Semiconductor Advanced Substrate Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Advanced Substrate Market?

The projected CAGR is approximately 6.25%.

2. Which companies are prominent players in the Semiconductor Advanced Substrate Market?

Key companies in the market include Young Poong Group, Nippon Mektron, Unimicron, Korea Circuit, AT&S, Hannstar, Zhen Ding Tech, Samsung Electro-Mechanics, IBIDEN, Daeduck Electronics*List Not Exhaustive, TTM Technologies, Compeg, LG Innotek.

3. What are the main segments of the Semiconductor Advanced Substrate Market?

The market segments include Platform, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 702.44 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Applications of Advanced Substrates in Manufacturing IoT Equipment; Increasing Trend of Miniaturization in Semiconductor Devices.

6. What are the notable trends driving market growth?

FC BGA to Hold the Major Market Share.

7. Are there any restraints impacting market growth?

Complexity in the Manufacturing Process.

8. Can you provide examples of recent developments in the market?

February 2023 - TTM Technologies announces exhibit at the 2023 International Electronics Circuit Exhibition (Shenzhen), at Booth in the Shenzhen World Exhibition & Convention Center (Bao'an), in China, Where TTM will be hosting a series of technical seminars to present its cutting edge engineering and product solutions aimed at dealing with customer problems across different end markets and applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Advanced Substrate Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Advanced Substrate Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Advanced Substrate Market?

To stay informed about further developments, trends, and reports in the Semiconductor Advanced Substrate Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence