Key Insights

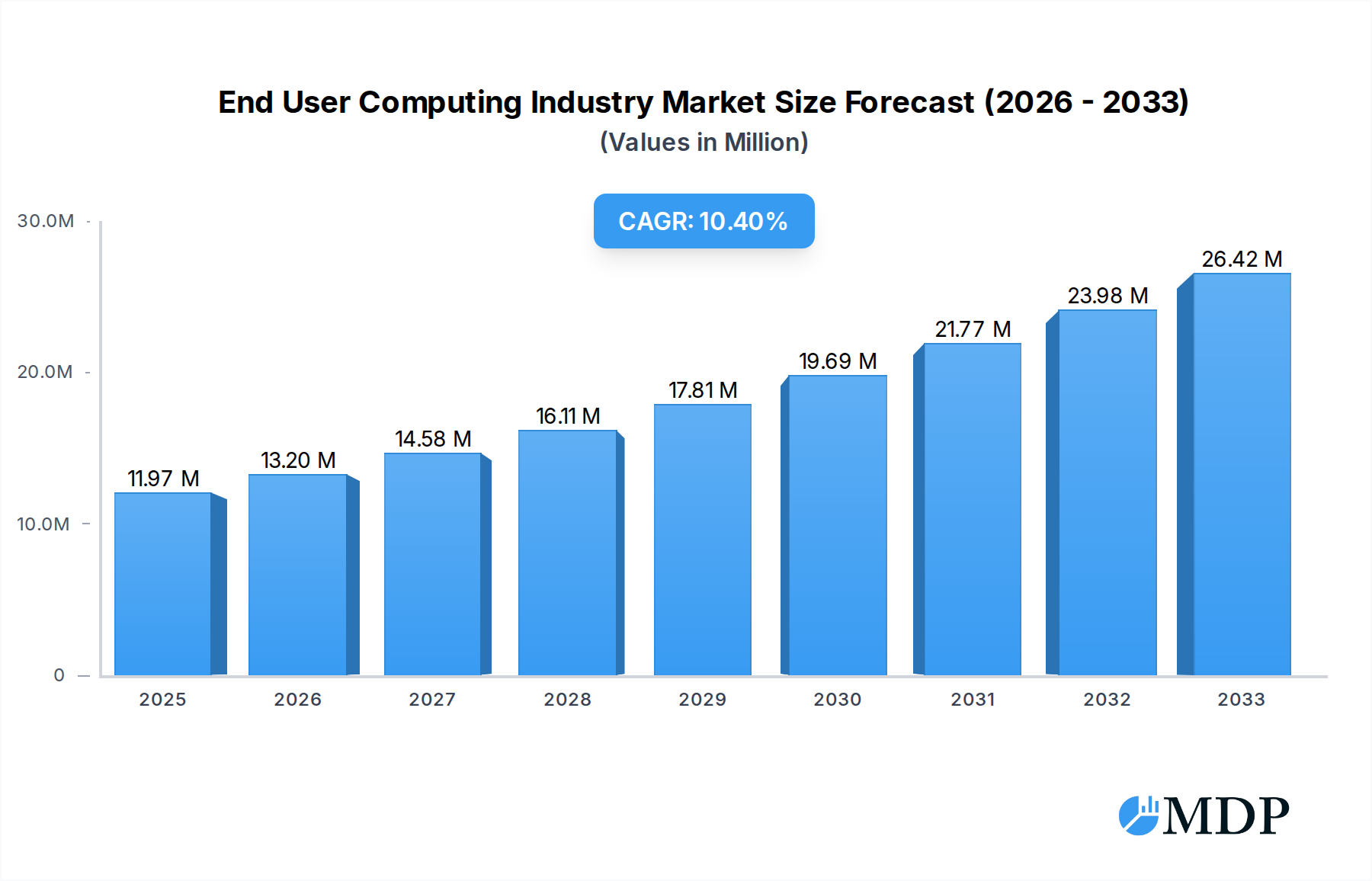

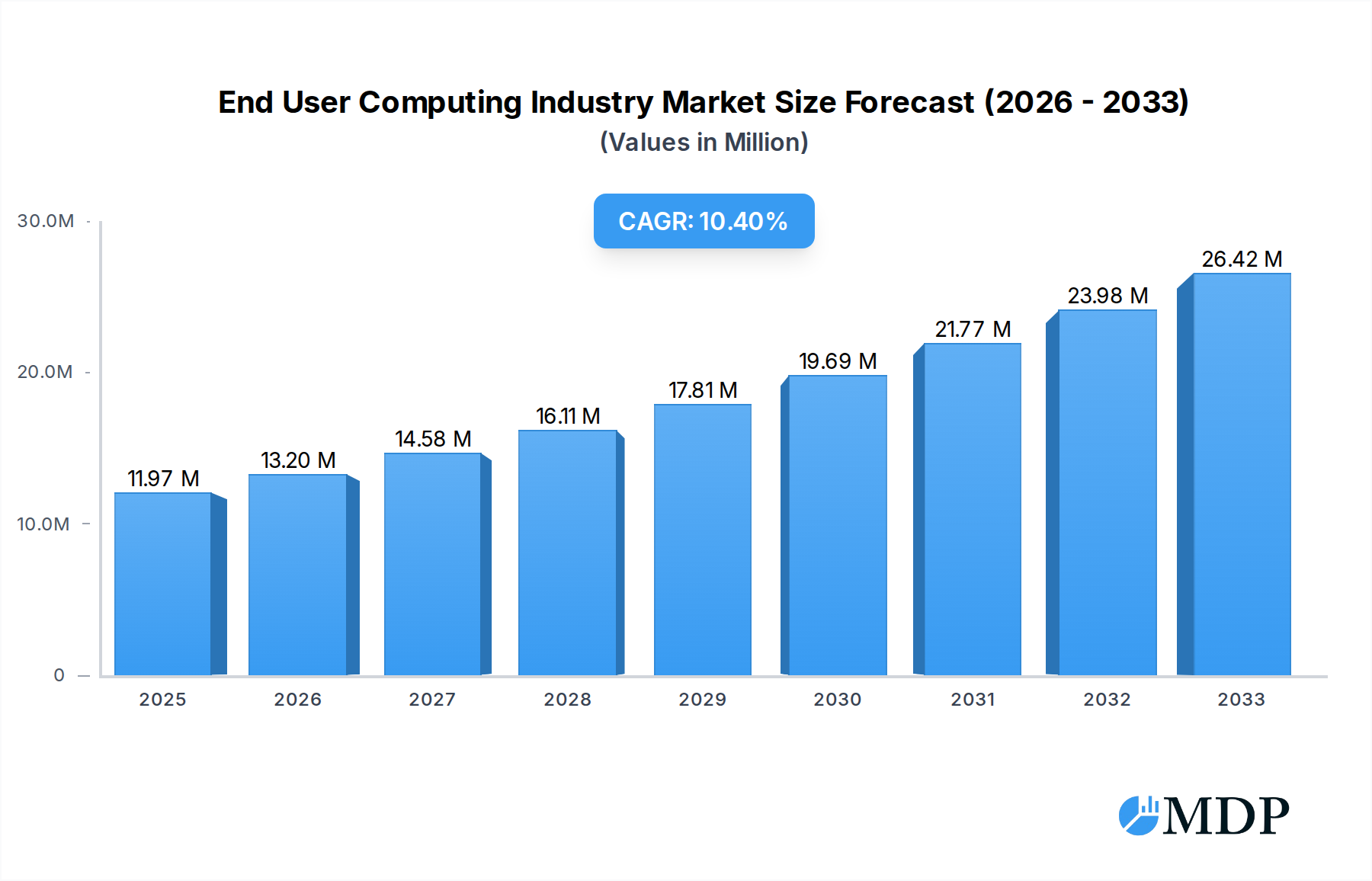

The End User Computing (EUC) industry is experiencing robust growth, projected to reach $11.97 million by 2025, with a Compound Annual Growth Rate (CAGR) exceeding 10.05% through 2033. This expansion is primarily fueled by the increasing adoption of cloud-based solutions, the growing demand for remote work capabilities, and the need for enhanced endpoint security and management. Key drivers include the digital transformation initiatives across various sectors, the proliferation of mobile devices, and the evolving regulatory landscape mandating secure data handling. The market is segmented into solutions like Virtual Desktop Infrastructure (VDI), Device Management, and others, alongside essential services that support their implementation and maintenance. Large enterprises and small to medium-sized businesses (SMEs) alike are investing in EUC to improve workforce productivity, streamline IT operations, and offer greater flexibility to their employees. The shift towards cloud deployment is particularly noteworthy, as organizations seek scalable and cost-effective infrastructure.

End User Computing Industry Market Size (In Million)

The EUC market's dynamism is further shaped by its adoption across diverse end-user industries, including IT and Telecom, BFSI, Healthcare, and Retail, each with unique requirements and growth trajectories. While the inherent flexibility and cost savings offered by cloud deployments are significant advantages, challenges such as data security concerns, integration complexities with legacy systems, and the need for specialized IT expertise can act as restraints. However, ongoing advancements in virtualization, cloud technologies, and unified endpoint management solutions are actively addressing these limitations. Major industry players are actively innovating and expanding their offerings to cater to the evolving needs of this market, focusing on delivering seamless, secure, and productive end-user experiences across all devices and locations, thereby solidifying the market's upward trajectory.

End User Computing Industry Company Market Share

Here is an SEO-optimized, engaging report description for the End User Computing Industry, designed for maximum search visibility and stakeholder attraction.

Report Title: End User Computing (EUC) Industry: Market Size, Growth Drivers, Competitive Landscape, and Future Outlook (2024-2033)

Report Description:

Dive deep into the End User Computing (EUC) industry with our comprehensive market intelligence report. Explore the dynamic landscape of virtual desktop infrastructure (VDI), device management solutions, and essential EUC services that are transforming how businesses operate. This report provides in-depth analysis of market share, CAGR, and market penetration across large enterprises and small & medium enterprises (SMEs). We meticulously examine the growth of cloud-based EUC solutions alongside traditional on-premise deployments, offering critical insights for stakeholders in IT and Telecom, Banking, Financial Services, and Insurance (BFSI), Healthcare, and Retail.

Discover key industry developments, including Fujitsu Ltd's innovative CPU/GPU optimization technology addressing the global GPU shortage, IBM and VMware's strategic hybrid cloud partnership enhancing solutions for critical workloads, and the CRISIL and Apparity LLC collaboration fortifying EUC governance in financial institutions. With a study period spanning 2019 to 2033, a base year of 2025, and a detailed forecast period from 2025 to 2033, this report is an indispensable resource for understanding the current market, identifying emerging opportunities, and navigating the challenges within the rapidly evolving EUC sector. Leverage actionable insights on market dynamics, concentration, innovation drivers, and regulatory frameworks to inform your strategic decisions.

End User Computing Industry Market Dynamics & Concentration

The End User Computing (EUC) industry is characterized by a moderate to high level of market concentration, driven by the significant investments required in research and development, robust intellectual property, and the need for extensive go-to-market strategies. Innovation drivers such as the increasing demand for remote work capabilities, the imperative for enhanced data security, and the relentless pursuit of operational efficiency are pushing companies to develop more sophisticated and integrated EUC solutions. Regulatory frameworks, particularly within the BFSI and healthcare sectors, play a pivotal role, dictating compliance standards and influencing product development. Product substitutes, while present in the form of traditional desktop environments, are increasingly being overshadowed by the agility and scalability offered by advanced EUC solutions. End-user trends overwhelmingly favor flexibility, security, and seamless access to applications and data, regardless of location or device. Merger and acquisition (M&A) activities are a significant indicator of market consolidation and strategic positioning, with an estimated xx M&A deals observed in the historical period. Leading players are continuously acquiring smaller, innovative companies to expand their service portfolios and market reach. The market share of the top five vendors is estimated to be around xx% in the base year 2025.

- Market Concentration: Moderate to High, driven by R&D investment and IP.

- Innovation Drivers: Remote work, data security, operational efficiency.

- Regulatory Frameworks: Crucial in BFSI, healthcare; influencing compliance and product design.

- Product Substitutes: Traditional desktops are losing ground to advanced EUC.

- End-User Trends: Demand for flexibility, security, and ubiquitous data access.

- M&A Activities: Active consolidation, strategic acquisitions to gain market share and capabilities. Estimated xx M&A deals in the historical period.

- Top Vendor Market Share (2025): Approximately xx%.

End User Computing Industry Industry Trends & Analysis

The End User Computing (EUC) industry is experiencing robust growth, fueled by a confluence of transformative trends. The persistent shift towards hybrid and remote work models remains a primary growth driver, compelling organizations to invest in scalable and secure solutions that enable employees to access corporate resources from any location and device. The increasing sophistication of cyber threats and the growing emphasis on data privacy regulations globally are also accelerating the adoption of EUC, particularly solutions offering centralized management and robust security features like Virtual Desktop Infrastructure (VDI) and advanced Device Management. Technological disruptions, such as the rapid advancements in cloud computing, artificial intelligence (AI), and machine learning (ML), are enabling more intelligent and automated EUC management, predictive maintenance, and personalized user experiences. These technologies are not only enhancing the functionality of existing solutions but also paving the way for entirely new use cases and services.

Consumer preferences are increasingly aligned with the consumerization of IT, demanding user experiences that are as intuitive and seamless as their personal devices. This translates to a demand for EUC solutions that are easy to deploy, manage, and use, with minimal friction for the end-user. Competitive dynamics within the EUC market are intense, with established technology giants competing alongside agile startups. Differentiation is often achieved through specialized features, superior performance, competitive pricing, and tailored support for specific industry verticals. The market penetration of advanced EUC solutions is steadily increasing, with an estimated CAGR of xx% projected for the forecast period. This growth is further bolstered by the expanding use of Services within the EUC ecosystem, encompassing managed services, consulting, and support, which are becoming integral to the overall value proposition for businesses seeking to optimize their IT infrastructure and empower their workforce. The demand for cost-effective and agile IT infrastructure also propels the adoption of cloud-based EUC, which offers scalability and reduces the upfront capital expenditure associated with on-premise solutions.

Leading Markets & Segments in End User Computing Industry

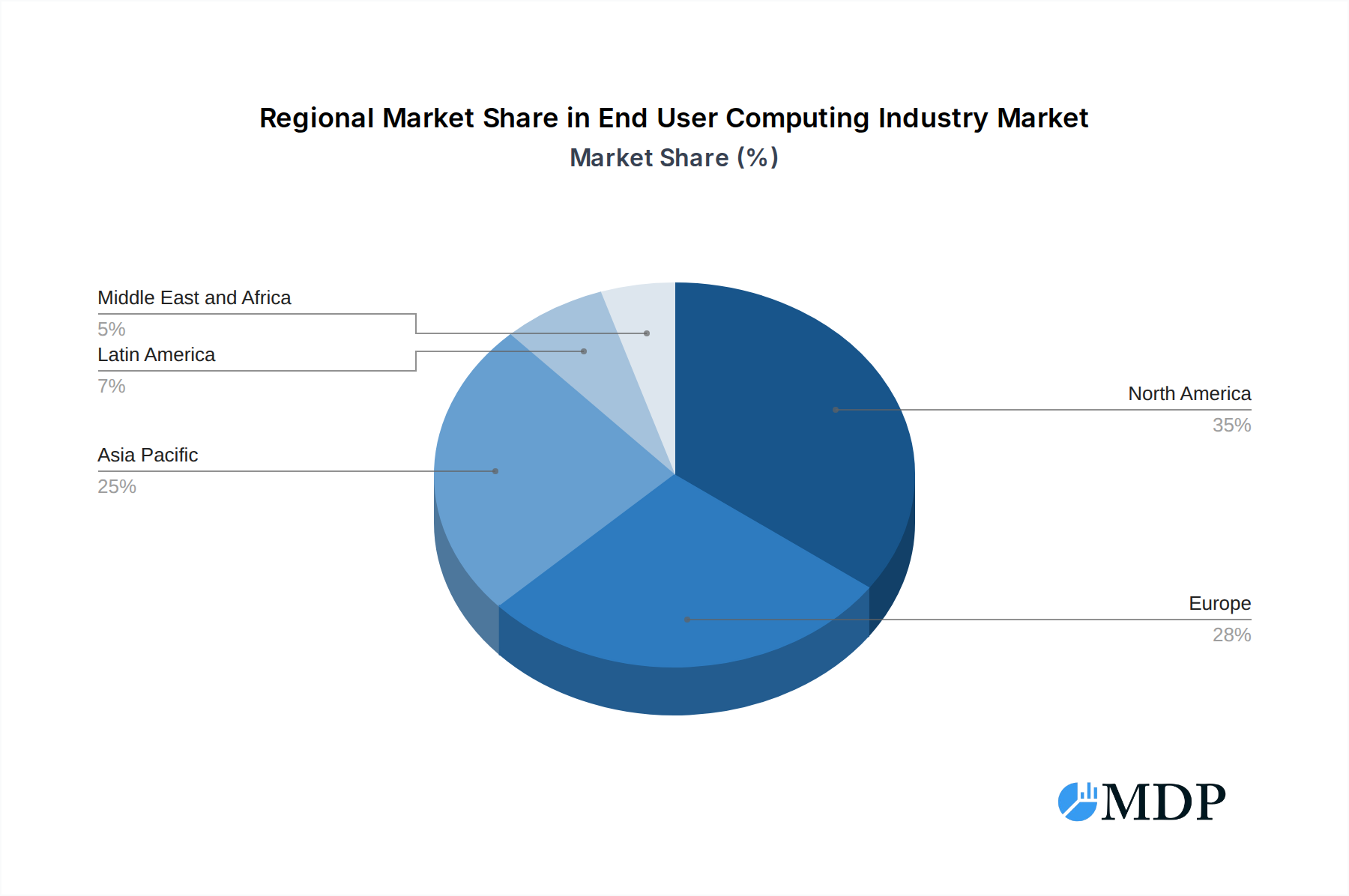

The End User Computing (EUC) industry exhibits distinct leadership across various regions and segments, driven by a combination of economic policies, digital infrastructure maturity, and specific industry demands.

Dominant Region and Country Analysis:

- North America currently leads the global EUC market, driven by its high adoption rate of advanced technologies, significant investments in cloud infrastructure, and a strong presence of large enterprises across sectors like IT, BFSI, and Healthcare.

- Europe follows closely, with countries like Germany, the UK, and France showing substantial growth due to increasing regulatory compliance requirements and a growing acceptance of remote work models post-pandemic.

- Asia Pacific is projected to be the fastest-growing region, fueled by rapid digital transformation initiatives, a burgeoning SME sector, and increasing government support for technology adoption in countries like India, China, and South Korea.

Dominant Segments:

Type: Solution:

- Virtual Desktop Infrastructure (VDI): This segment is experiencing significant expansion due to its ability to provide secure, centralized access to applications and data, crucial for remote workforces and compliance-sensitive industries. Market growth is driven by enhanced security features and improved user experience.

- Device Management: With the proliferation of diverse endpoints (laptops, tablets, smartphones), robust device management solutions are essential for IT departments to maintain control, security, and compliance across the entire device ecosystem.

- Other Solutions: This encompasses a range of specialized tools and platforms that augment core EUC capabilities, including application virtualization, data synchronization, and endpoint security solutions.

Services:

- The Services segment, including managed services, consulting, implementation, and support, is a critical component of the EUC market. Organizations are increasingly opting for specialized service providers to manage the complexity of EUC deployments and ensure optimal performance and security, thereby contributing significantly to overall market revenue.

Organization Size:

- Large Enterprises: This segment continues to be a major revenue generator due to their substantial IT budgets, complex operational requirements, and the critical need for robust security and compliance. The adoption of EUC solutions in large enterprises is driven by their global operations and diverse workforce.

- Small & Medium Enterprises (SMEs): While historically slower to adopt, SMEs are increasingly recognizing the benefits of EUC, particularly cloud-based solutions that offer scalability, cost-effectiveness, and improved IT management capabilities.

Deployment Mode:

- Cloud: Cloud-based EUC solutions are experiencing explosive growth. Their inherent scalability, flexibility, reduced upfront costs, and ease of management make them highly attractive to organizations of all sizes, especially in response to the demand for remote and hybrid work environments.

- On Premise: While cloud adoption is surging, on-premise solutions still hold a significant share, particularly for organizations with stringent data sovereignty requirements, legacy infrastructure, or a strong preference for direct control over their IT environment.

End User Industry:

- IT and Telecom: This sector is a primary adopter of EUC solutions due to its dynamic nature, remote workforce, and the constant need for secure and agile IT infrastructure.

- Banking, Financial Services, and Insurance (BFSI): The BFSI sector is a critical market for EUC due to its high security and compliance mandates. VDI and robust device management are essential for protecting sensitive customer data and meeting regulatory obligations.

- Healthcare: Similar to BFSI, the healthcare industry prioritizes security and compliance. EUC solutions enable secure access to patient records and critical applications for medical professionals, supporting both in-facility and remote healthcare delivery.

- Retail: The retail sector is leveraging EUC for flexible workforce management, secure point-of-sale systems, and improved customer service through accessible IT resources.

End User Computing Industry Product Developments

Recent product developments in the End User Computing (EUC) industry are intensely focused on enhancing performance, security, and user experience, particularly in response to the evolving work landscape. Fujitsu Ltd's November 2023 innovation in CPU/GPU resource allocation is a prime example, directly addressing the global shortage of GPUs and the increasing demand for AI and Deep Learning applications by optimizing real-time resource prioritization. This technology offers a competitive advantage by ensuring high performance even under demanding computational loads. VMware Inc. and Dell Technologies continue to refine their VDI and device management platforms, focusing on seamless integration with cloud services and enhanced security protocols. The emergence of AI-powered analytics for predictive issue resolution and automated policy enforcement is also a significant trend, promising more proactive and efficient EUC management and delivering enhanced stability and security.

Key Drivers of End User Computing Industry Growth

Several key factors are propelling the growth of the End User Computing (EUC) industry. The sustained demand for flexible and remote work arrangements, accelerated by global events, is a primary driver, necessitating secure and accessible computing environments. Technological advancements, particularly in cloud computing, AI, and automation, are enabling more powerful, scalable, and cost-effective EUC solutions. Furthermore, escalating cybersecurity threats and stringent data privacy regulations are compelling organizations to invest in robust EUC solutions that offer centralized control and enhanced data protection. The increasing need for operational efficiency and cost optimization within IT departments also fuels the adoption of managed EUC services and cloud-based platforms, reducing the burden of infrastructure management and maintenance.

- Remote & Hybrid Work Models: Enabling secure and productive work from anywhere.

- Technological Advancements: Cloud, AI, and automation enhancing capabilities and efficiency.

- Cybersecurity & Data Privacy: Driving adoption of secure, compliant EUC solutions.

- Operational Efficiency & Cost Optimization: Shifting towards managed services and cloud.

Challenges in the End User Computing Industry Market

Despite its strong growth trajectory, the End User Computing (EUC) industry faces several challenges. The complexity of integrating new EUC solutions with existing legacy IT infrastructures can be a significant hurdle, often requiring substantial technical expertise and time. Ensuring consistent security and compliance across a diverse range of devices and locations, especially with the rise of bring-your-own-device (BYOD) policies, remains a persistent concern. Furthermore, the upfront investment and ongoing operational costs associated with advanced EUC deployments can be prohibitive for some organizations, particularly SMEs, despite the long-term cost-saving potential. Intense competition and rapid technological evolution also put pressure on vendors to continuously innovate, which can be resource-intensive and challenging to keep pace with.

- Integration Complexity: Difficulty in merging with existing IT infrastructure.

- Security & Compliance: Maintaining consistency across diverse endpoints and locations.

- Cost of Implementation: High initial investment and ongoing operational expenses.

- Rapid Technological Evolution: Need for continuous innovation and adaptation.

Emerging Opportunities in End User Computing Industry

The End User Computing (EUC) industry is ripe with emerging opportunities that promise sustained long-term growth. The increasing integration of AI and machine learning within EUC platforms offers significant potential for predictive analytics, automated troubleshooting, and personalized user experiences, driving greater efficiency and user satisfaction. The burgeoning demand for specialized EUC solutions tailored to specific industry verticals, such as healthcare for remote patient monitoring or manufacturing for IoT device management, presents a lucrative avenue for market expansion. Strategic partnerships between technology providers, cloud service providers, and managed service organizations are also key catalysts, enabling the delivery of comprehensive, end-to-end EUC solutions. Furthermore, the ongoing digital transformation initiatives across emerging economies, particularly in Asia Pacific and Africa, represent substantial untapped markets for EUC adoption.

Leading Players in the End User Computing Industry Sector

- Infosys Limited

- HCL Infosystems Limited

- Nucleus Software Exports Limited

- Hitachi Systems Micro Clinic

- Vmware Inc

- Fujitsu Ltd

- Genpact

- Nutanix Inc

- NetApp Inc

- IGEL Technology

- Mindtree Limited

- Tech Mahindra Limited

- Amazon Web Service

- Citrix Systems Inc

- Dell Technologies

Key Milestones in End User Computing Industry Industry

- November 2023: Fujitsu Ltd. develops technology for real-time CPU and GPU resource allocation to optimize performance, addressing the global GPU shortage driven by AI and Deep Learning demand.

- August 2022: IBM announces a new partnership with VMware to deliver co-engineered hybrid cloud solutions for industries like healthcare and financial services, aiming to reduce costs and mitigate risks.

- February 2022: CRISIL and Apparity LLC launch a partnership to offer comprehensive EUC and model-risk propositions for financial institutions, integrating CRISIL's governance expertise with Apparity's advanced tracking solutions.

Strategic Outlook for End User Computing Industry Market

The strategic outlook for the End User Computing (EUC) industry is exceptionally positive, characterized by continuous innovation and expanding market reach. The ongoing adoption of cloud-native EUC solutions will remain a dominant growth accelerator, offering unparalleled scalability and flexibility. The deepening integration of AI and ML will further enhance automation, security, and predictive capabilities, leading to more intelligent and resilient end-user environments. Strategic partnerships and ecosystem collaborations will be crucial for vendors to deliver comprehensive, integrated solutions addressing complex enterprise needs. Furthermore, the increasing demand for specialized EUC services, from initial assessment and deployment to ongoing managed services and support, presents a significant opportunity for growth and revenue generation, solidifying the industry's role as a cornerstone of modern digital workplaces.

End User Computing Industry Segmentation

-

1. Type

-

1.1. Solution

- 1.1.1. Virtual Desktop Infrastructure

- 1.1.2. Device Management

- 1.1.3. Other So

- 1.2. Services

-

1.1. Solution

-

2. Organization Size

- 2.1. Large Enterprises

- 2.2. Small & Medium Enterprises

-

3. Deployment Mode

- 3.1. On Premise

- 3.2. Cloud

-

4. End user Industry

- 4.1. IT and Telecom

- 4.2. Banking, Financial Services, and Insurance

- 4.3. Healthcare

- 4.4. Retail

- 4.5. Other E

End User Computing Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

End User Computing Industry Regional Market Share

Geographic Coverage of End User Computing Industry

End User Computing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 10.05% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Solution

- 5.1.1.1. Virtual Desktop Infrastructure

- 5.1.1.2. Device Management

- 5.1.1.3. Other So

- 5.1.2. Services

- 5.1.1. Solution

- 5.2. Market Analysis, Insights and Forecast - by Organization Size

- 5.2.1. Large Enterprises

- 5.2.2. Small & Medium Enterprises

- 5.3. Market Analysis, Insights and Forecast - by Deployment Mode

- 5.3.1. On Premise

- 5.3.2. Cloud

- 5.4. Market Analysis, Insights and Forecast - by End user Industry

- 5.4.1. IT and Telecom

- 5.4.2. Banking, Financial Services, and Insurance

- 5.4.3. Healthcare

- 5.4.4. Retail

- 5.4.5. Other E

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global End User Computing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Solution

- 6.1.1.1. Virtual Desktop Infrastructure

- 6.1.1.2. Device Management

- 6.1.1.3. Other So

- 6.1.2. Services

- 6.1.1. Solution

- 6.2. Market Analysis, Insights and Forecast - by Organization Size

- 6.2.1. Large Enterprises

- 6.2.2. Small & Medium Enterprises

- 6.3. Market Analysis, Insights and Forecast - by Deployment Mode

- 6.3.1. On Premise

- 6.3.2. Cloud

- 6.4. Market Analysis, Insights and Forecast - by End user Industry

- 6.4.1. IT and Telecom

- 6.4.2. Banking, Financial Services, and Insurance

- 6.4.3. Healthcare

- 6.4.4. Retail

- 6.4.5. Other E

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America End User Computing Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Solution

- 7.1.1.1. Virtual Desktop Infrastructure

- 7.1.1.2. Device Management

- 7.1.1.3. Other So

- 7.1.2. Services

- 7.1.1. Solution

- 7.2. Market Analysis, Insights and Forecast - by Organization Size

- 7.2.1. Large Enterprises

- 7.2.2. Small & Medium Enterprises

- 7.3. Market Analysis, Insights and Forecast - by Deployment Mode

- 7.3.1. On Premise

- 7.3.2. Cloud

- 7.4. Market Analysis, Insights and Forecast - by End user Industry

- 7.4.1. IT and Telecom

- 7.4.2. Banking, Financial Services, and Insurance

- 7.4.3. Healthcare

- 7.4.4. Retail

- 7.4.5. Other E

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe End User Computing Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Solution

- 8.1.1.1. Virtual Desktop Infrastructure

- 8.1.1.2. Device Management

- 8.1.1.3. Other So

- 8.1.2. Services

- 8.1.1. Solution

- 8.2. Market Analysis, Insights and Forecast - by Organization Size

- 8.2.1. Large Enterprises

- 8.2.2. Small & Medium Enterprises

- 8.3. Market Analysis, Insights and Forecast - by Deployment Mode

- 8.3.1. On Premise

- 8.3.2. Cloud

- 8.4. Market Analysis, Insights and Forecast - by End user Industry

- 8.4.1. IT and Telecom

- 8.4.2. Banking, Financial Services, and Insurance

- 8.4.3. Healthcare

- 8.4.4. Retail

- 8.4.5. Other E

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific End User Computing Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Solution

- 9.1.1.1. Virtual Desktop Infrastructure

- 9.1.1.2. Device Management

- 9.1.1.3. Other So

- 9.1.2. Services

- 9.1.1. Solution

- 9.2. Market Analysis, Insights and Forecast - by Organization Size

- 9.2.1. Large Enterprises

- 9.2.2. Small & Medium Enterprises

- 9.3. Market Analysis, Insights and Forecast - by Deployment Mode

- 9.3.1. On Premise

- 9.3.2. Cloud

- 9.4. Market Analysis, Insights and Forecast - by End user Industry

- 9.4.1. IT and Telecom

- 9.4.2. Banking, Financial Services, and Insurance

- 9.4.3. Healthcare

- 9.4.4. Retail

- 9.4.5. Other E

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America End User Computing Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Solution

- 10.1.1.1. Virtual Desktop Infrastructure

- 10.1.1.2. Device Management

- 10.1.1.3. Other So

- 10.1.2. Services

- 10.1.1. Solution

- 10.2. Market Analysis, Insights and Forecast - by Organization Size

- 10.2.1. Large Enterprises

- 10.2.2. Small & Medium Enterprises

- 10.3. Market Analysis, Insights and Forecast - by Deployment Mode

- 10.3.1. On Premise

- 10.3.2. Cloud

- 10.4. Market Analysis, Insights and Forecast - by End user Industry

- 10.4.1. IT and Telecom

- 10.4.2. Banking, Financial Services, and Insurance

- 10.4.3. Healthcare

- 10.4.4. Retail

- 10.4.5. Other E

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa End User Computing Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Solution

- 11.1.1.1. Virtual Desktop Infrastructure

- 11.1.1.2. Device Management

- 11.1.1.3. Other So

- 11.1.2. Services

- 11.1.1. Solution

- 11.2. Market Analysis, Insights and Forecast - by Organization Size

- 11.2.1. Large Enterprises

- 11.2.2. Small & Medium Enterprises

- 11.3. Market Analysis, Insights and Forecast - by Deployment Mode

- 11.3.1. On Premise

- 11.3.2. Cloud

- 11.4. Market Analysis, Insights and Forecast - by End user Industry

- 11.4.1. IT and Telecom

- 11.4.2. Banking, Financial Services, and Insurance

- 11.4.3. Healthcare

- 11.4.4. Retail

- 11.4.5. Other E

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infosys Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 HCL Infosystems Limited

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Nucleus Software Exports Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hitachi Systems Micro Clinic

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Vmware Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Fujitsu Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Genpact

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Nutanix Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 NetApp Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 IGEL Technology

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Mindtree Limited

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Tech Mahindra Limited

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Amazon Web Service

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Citrix Systems Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Dell Technologies

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Infosys Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global End User Computing Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America End User Computing Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America End User Computing Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America End User Computing Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 5: North America End User Computing Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 6: North America End User Computing Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 7: North America End User Computing Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 8: North America End User Computing Industry Revenue (Million), by End user Industry 2025 & 2033

- Figure 9: North America End User Computing Industry Revenue Share (%), by End user Industry 2025 & 2033

- Figure 10: North America End User Computing Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America End User Computing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe End User Computing Industry Revenue (Million), by Type 2025 & 2033

- Figure 13: Europe End User Computing Industry Revenue Share (%), by Type 2025 & 2033

- Figure 14: Europe End User Computing Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 15: Europe End User Computing Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 16: Europe End User Computing Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 17: Europe End User Computing Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 18: Europe End User Computing Industry Revenue (Million), by End user Industry 2025 & 2033

- Figure 19: Europe End User Computing Industry Revenue Share (%), by End user Industry 2025 & 2033

- Figure 20: Europe End User Computing Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe End User Computing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific End User Computing Industry Revenue (Million), by Type 2025 & 2033

- Figure 23: Asia Pacific End User Computing Industry Revenue Share (%), by Type 2025 & 2033

- Figure 24: Asia Pacific End User Computing Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 25: Asia Pacific End User Computing Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 26: Asia Pacific End User Computing Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 27: Asia Pacific End User Computing Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 28: Asia Pacific End User Computing Industry Revenue (Million), by End user Industry 2025 & 2033

- Figure 29: Asia Pacific End User Computing Industry Revenue Share (%), by End user Industry 2025 & 2033

- Figure 30: Asia Pacific End User Computing Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific End User Computing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America End User Computing Industry Revenue (Million), by Type 2025 & 2033

- Figure 33: Latin America End User Computing Industry Revenue Share (%), by Type 2025 & 2033

- Figure 34: Latin America End User Computing Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 35: Latin America End User Computing Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 36: Latin America End User Computing Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 37: Latin America End User Computing Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 38: Latin America End User Computing Industry Revenue (Million), by End user Industry 2025 & 2033

- Figure 39: Latin America End User Computing Industry Revenue Share (%), by End user Industry 2025 & 2033

- Figure 40: Latin America End User Computing Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America End User Computing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa End User Computing Industry Revenue (Million), by Type 2025 & 2033

- Figure 43: Middle East and Africa End User Computing Industry Revenue Share (%), by Type 2025 & 2033

- Figure 44: Middle East and Africa End User Computing Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 45: Middle East and Africa End User Computing Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 46: Middle East and Africa End User Computing Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 47: Middle East and Africa End User Computing Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 48: Middle East and Africa End User Computing Industry Revenue (Million), by End user Industry 2025 & 2033

- Figure 49: Middle East and Africa End User Computing Industry Revenue Share (%), by End user Industry 2025 & 2033

- Figure 50: Middle East and Africa End User Computing Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East and Africa End User Computing Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global End User Computing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global End User Computing Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 3: Global End User Computing Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 4: Global End User Computing Industry Revenue Million Forecast, by End user Industry 2020 & 2033

- Table 5: Global End User Computing Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global End User Computing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 7: Global End User Computing Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 8: Global End User Computing Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 9: Global End User Computing Industry Revenue Million Forecast, by End user Industry 2020 & 2033

- Table 10: Global End User Computing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global End User Computing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 12: Global End User Computing Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 13: Global End User Computing Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 14: Global End User Computing Industry Revenue Million Forecast, by End user Industry 2020 & 2033

- Table 15: Global End User Computing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global End User Computing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Global End User Computing Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 18: Global End User Computing Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 19: Global End User Computing Industry Revenue Million Forecast, by End user Industry 2020 & 2033

- Table 20: Global End User Computing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global End User Computing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 22: Global End User Computing Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 23: Global End User Computing Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 24: Global End User Computing Industry Revenue Million Forecast, by End user Industry 2020 & 2033

- Table 25: Global End User Computing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global End User Computing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 27: Global End User Computing Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 28: Global End User Computing Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 29: Global End User Computing Industry Revenue Million Forecast, by End user Industry 2020 & 2033

- Table 30: Global End User Computing Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the End User Computing Industry?

The projected CAGR is approximately > 10.05%.

2. Which companies are prominent players in the End User Computing Industry?

Key companies in the market include Infosys Limited, HCL Infosystems Limited, Nucleus Software Exports Limited, Hitachi Systems Micro Clinic, Vmware Inc, Fujitsu Ltd, Genpact, Nutanix Inc, NetApp Inc, IGEL Technology, Mindtree Limited, Tech Mahindra Limited, Amazon Web Service, Citrix Systems Inc, Dell Technologies.

3. What are the main segments of the End User Computing Industry?

The market segments include Type, Organization Size, Deployment Mode, End user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.97 Million as of 2022.

5. What are some drivers contributing to market growth?

Drive to Increase the Productivity of Employees with Technology; Increasing Use of Cloud.

6. What are the notable trends driving market growth?

Increasing Use of Cloud is Expected to Drive the End User Computing Market Growth.

7. Are there any restraints impacting market growth?

Issues Associated with Transformation and Integration of Processes By Organizations.

8. Can you provide examples of recent developments in the market?

November 2023 - Fujitsu Ltd Technology for the optimization of the use of CPUs and GPUs by allocating resources on a real-time basis to prioritize processes with high performance prioritise processes with high performance, even when running programs using GPUs. For the worldwide shortage of GPUs, which has been triggered by a growing demand for intelligent Artificial Intelligence, Deep Learning, and more applications, Fujitsu developed a new technology that optimizes user computing resources.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "End User Computing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the End User Computing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the End User Computing Industry?

To stay informed about further developments, trends, and reports in the End User Computing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence