Key Insights

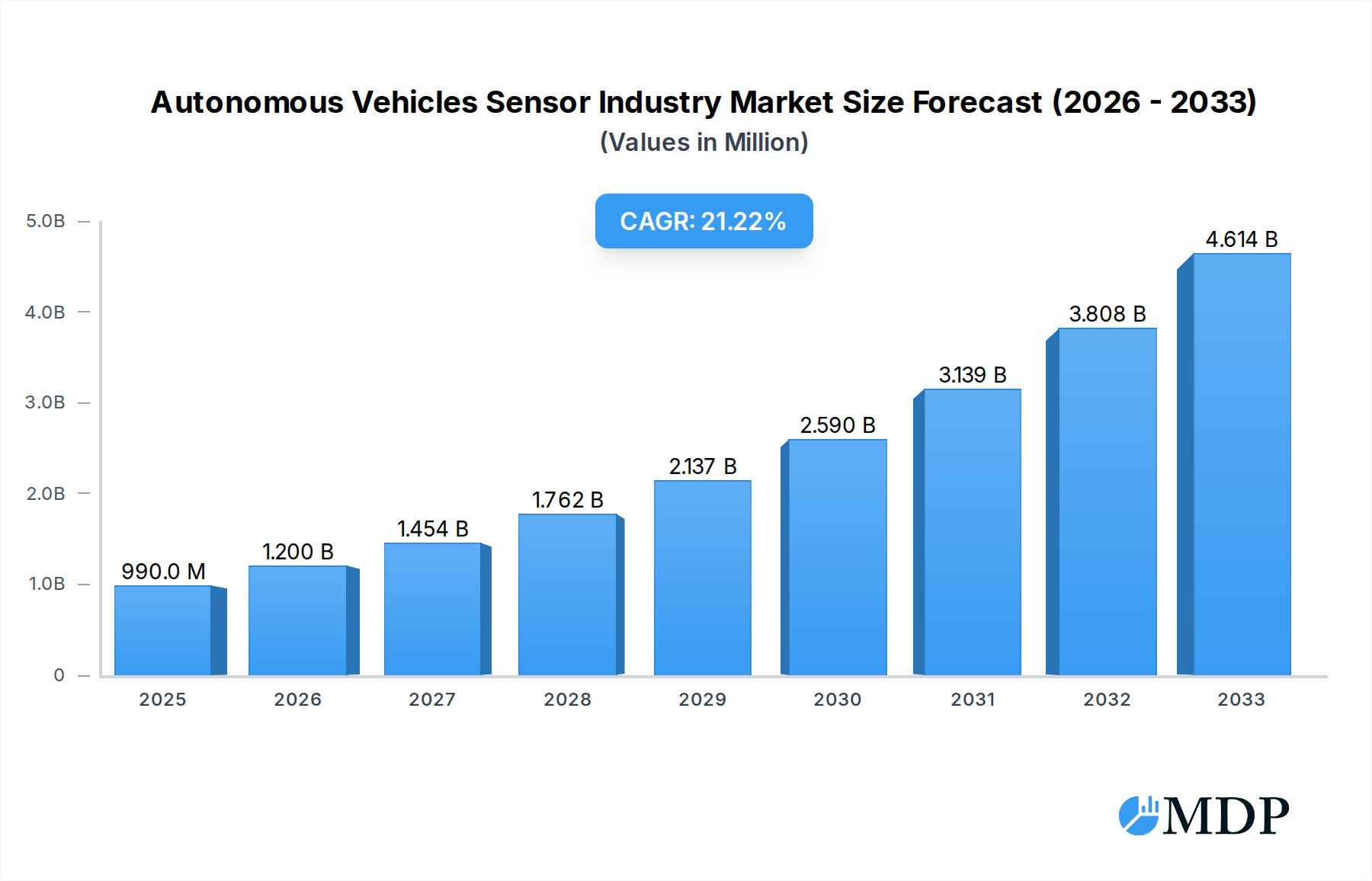

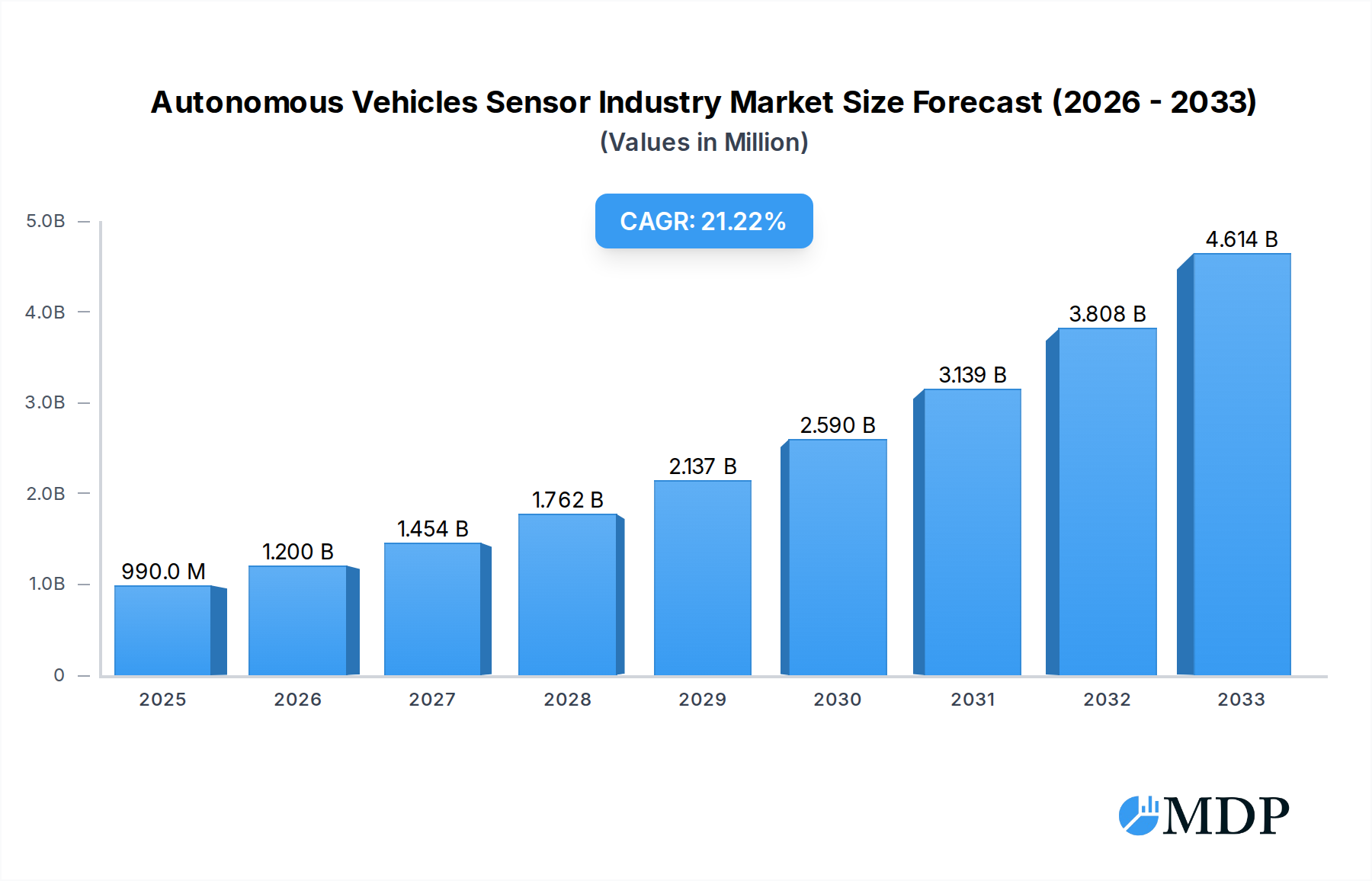

The Autonomous Vehicles Sensor Industry is poised for explosive growth, driven by an increasing demand for advanced safety features and the accelerating adoption of self-driving technology across all vehicle types. With a current estimated market size of $990 million in 2025, the industry is projected to experience a remarkable 21.16% CAGR from 2025 to 2033. This robust expansion is primarily fueled by significant investments in research and development by leading automotive and technology companies, coupled with supportive government initiatives aimed at enhancing road safety and efficiency. The continuous evolution of sensor technologies, including LiDAR, radar, cameras, and ultrasonic sensors, is critical to enabling higher levels of vehicle autonomy, from advanced driver-assistance systems (ADAS) to fully autonomous driving capabilities. This technological advancement is not only enhancing vehicle performance but also addressing the growing consumer desire for safer and more convenient transportation solutions.

Autonomous Vehicles Sensor Industry Market Size (In Million)

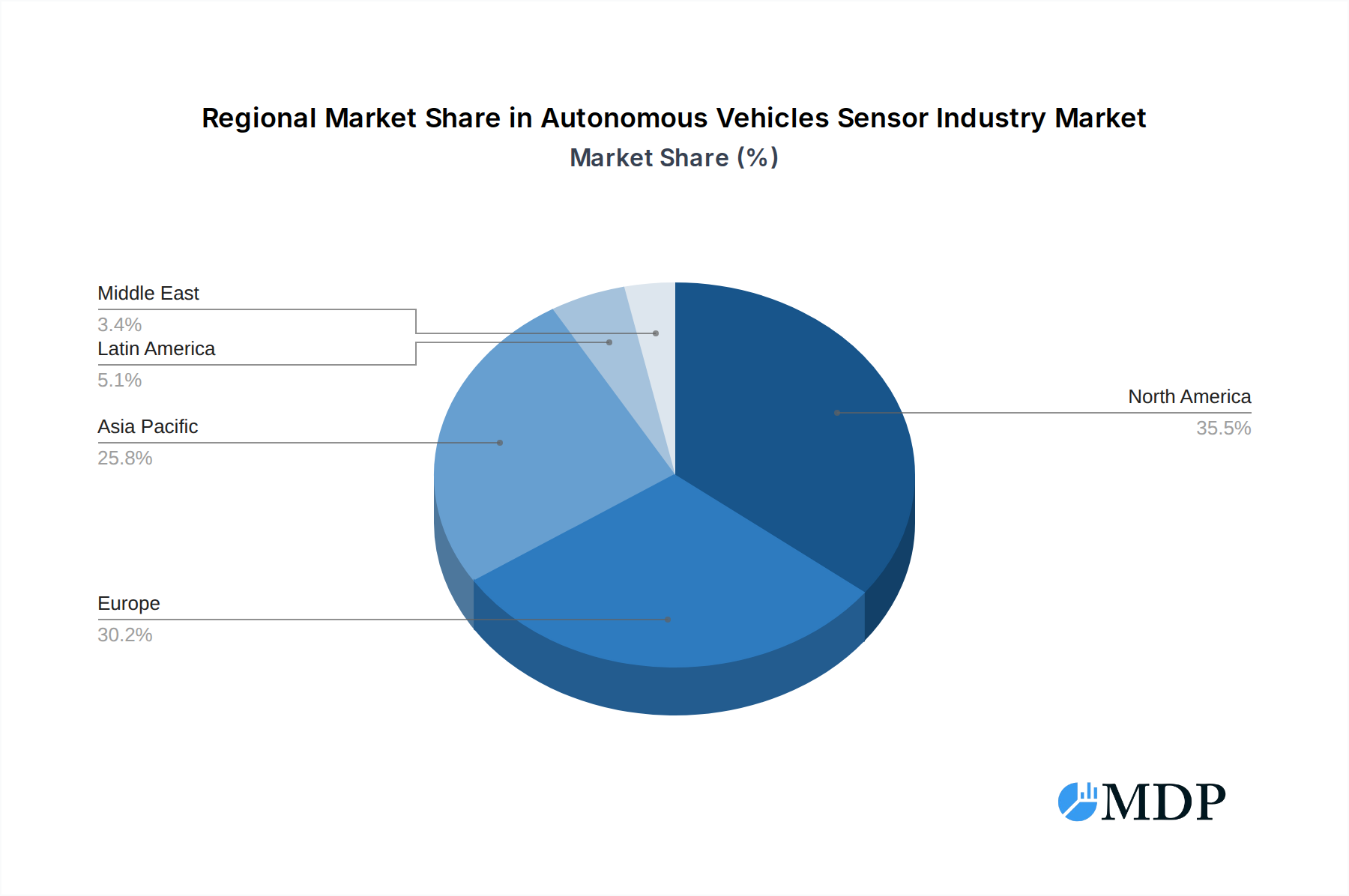

The market is broadly segmented by vehicle types, encompassing Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), and Other Autonomous Vehicles, each presenting unique opportunities and challenges. While passenger cars are leading the charge in sensor integration, the commercial vehicle sector is rapidly catching up, recognizing the potential for improved logistics and operational efficiency. Key industry players such as Infineon Technologies AG, Microchip Technology Inc., NXP Semiconductor, and Robert Bosch GmbH are at the forefront of innovation, developing sophisticated sensor solutions. Geographically, North America and Europe are currently leading the market, driven by stringent safety regulations and early adoption rates. However, the Asia Pacific region is expected to witness the fastest growth in the coming years, owing to its burgeoning automotive industry and increasing disposable incomes. Despite the promising outlook, challenges such as high sensor costs, regulatory hurdles in certain regions, and the need for robust cybersecurity measures may temper the pace of adoption in specific segments.

Autonomous Vehicles Sensor Industry Company Market Share

Dive deep into the rapidly evolving autonomous vehicles sensor market with this comprehensive report. Explore market dynamics, technological advancements, and growth opportunities shaping the future of self-driving technology. This report provides critical insights for automotive sensor manufacturers, ADAS (Advanced Driver-Assistance Systems) solution providers, AI chip developers, and vehicle OEMs. With a market size projected to reach billions, understand the trajectory of lidar sensors, radar sensors, camera sensors, and ultrasonic sensors in passenger cars, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs).

Autonomous Vehicles Sensor Industry Market Dynamics & Concentration

The autonomous vehicles sensor market is characterized by a dynamic landscape with significant concentration among leading technology providers. Innovation in areas like sensor fusion, AI perception algorithms, and edge computing are key drivers. Regulatory frameworks, though still evolving, are increasingly focused on safety and performance standards, influencing product development and market entry. While direct product substitutes for advanced sensing capabilities are limited, incremental improvements and integration of existing technologies pose a competitive threat. End-user trends, particularly the growing demand for enhanced safety features and the commercialization of autonomous fleets, are propelling market growth. Mergers and acquisitions (M&A) are a significant feature, with major players consolidating to gain market share and access new technologies. The number of M&A deals in the past five years is estimated to be in the dozens, with transaction values in the billions, signaling intense strategic activity. Market share is highly fragmented but dominated by a few key players in specific sensor categories.

Autonomous Vehicles Sensor Industry Industry Trends & Analysis

The autonomous vehicles sensor industry is witnessing unprecedented growth, driven by a confluence of technological breakthroughs and a burgeoning demand for advanced mobility solutions. The global autonomous vehicle sensor market is projected to experience a compound annual growth rate (CAGR) of over 20% from 2025 to 2033, indicating substantial expansion. This surge is fueled by the relentless pace of innovation in lidar technology, the increasing sophistication of automotive radar, and the growing adoption of high-resolution vision sensors and ultrasonic sensors for robust environmental perception. Market penetration of advanced sensing systems in new vehicle models is rapidly increasing, moving beyond luxury segments into mass-market applications. Key growth drivers include the push for enhanced vehicle safety, the development of Level 3 and Level 4 autonomous driving capabilities, and the commercial viability of robotaxi services and autonomous trucking. Technological disruptions, such as the miniaturization of lidar sensors, the integration of AI into sensor processing units, and advancements in sensor fusion algorithms, are fundamentally reshaping the competitive landscape. Consumer preferences are also evolving, with a greater emphasis on safety and convenience offered by autonomous features. This evolving demand, coupled with fierce competition among established automotive suppliers and emerging technology companies, is creating a vibrant and competitive market environment.

Leading Markets & Segments in Autonomous Vehicles Sensor Industry

The autonomous vehicles sensor industry is experiencing significant dominance from the Passenger Cars segment, which is expected to represent over 70% of the total market value by 2033. This segment's growth is underpinned by increasing consumer adoption of ADAS features and the gradual rollout of higher levels of autonomous driving in personal vehicles. Economically, developed regions like North America and Europe are leading in adoption due to strong consumer purchasing power and supportive regulatory frameworks. Infrastructure development, including advancements in smart city initiatives and 5G connectivity, further bolsters the deployment of autonomous technologies.

- Passenger Cars: This segment is the largest contributor, driven by the demand for safety features like automatic emergency braking, lane keeping assist, and the increasing integration of adaptive cruise control. The falling cost and improved performance of sensors are making these features more accessible.

- Light Commercial Vehicles (LCV): The LCV segment is exhibiting strong growth, propelled by the expansion of e-commerce and last-mile delivery services. Autonomous delivery vans and logistics vehicles are increasingly relying on sophisticated sensor suites for efficient and safe operations.

- Heavy Commercial Vehicles (HCV): Autonomous trucking is a significant growth frontier for the HCV segment. The potential for reduced operational costs, improved fuel efficiency, and enhanced safety on long-haul routes is driving substantial investment and development in this area.

- Other Autonomous Vehicles: This category includes autonomous shuttles, specialty vehicles, and emerging mobility solutions, which, while currently smaller in market share, represent a significant area for future innovation and market expansion.

Asia-Pacific, particularly China, is emerging as a critical market, fueled by government initiatives supporting the development of autonomous driving technologies and a rapidly growing automotive industry.

Autonomous Vehicles Sensor Industry Product Developments

Product development in the autonomous vehicles sensor industry is characterized by a relentless pursuit of higher accuracy, miniaturization, and cost-effectiveness. Innovations focus on advanced lidar technology offering improved range and resolution, sophisticated radar systems with enhanced object detection capabilities in adverse weather, and AI-powered camera systems capable of superior scene understanding and semantic segmentation. The integration of these disparate sensor modalities through advanced sensor fusion algorithms is a key competitive advantage, enabling robust perception and decision-making for autonomous systems.

Key Drivers of Autonomous Vehicles Sensor Industry Growth

The autonomous vehicles sensor industry is experiencing robust growth driven by several pivotal factors. Technological advancements in artificial intelligence and machine learning are enabling more sophisticated sensor processing and interpretation. Supportive government regulations and safety standards are accelerating the adoption of autonomous driving features. Furthermore, increasing consumer demand for enhanced vehicle safety and convenience, coupled with the commercial viability of autonomous mobility services like robotaxis and autonomous trucking, are significant economic catalysts. Investment in R&D by leading automotive and technology companies further fuels innovation and market expansion.

Challenges in the Autonomous Vehicles Sensor Industry Market

Despite significant growth, the autonomous vehicles sensor market faces several formidable challenges. Regulatory hurdles, particularly the lack of standardized global regulations for autonomous vehicle deployment, create uncertainty. High development and integration costs for advanced sensor systems remain a barrier to mass adoption. Supply chain disruptions and the global semiconductor shortage continue to impact production and pricing. Furthermore, public perception and trust in autonomous technology, alongside cybersecurity concerns, pose significant challenges that need to be addressed for widespread market acceptance. The complexity of sensor calibration and validation also contributes to development timelines.

Emerging Opportunities in Autonomous Vehicles Sensor Industry

Emerging opportunities in the autonomous vehicles sensor industry are abundant, driven by continuous technological breakthroughs and strategic market expansion. The development of more affordable and robust solid-state lidar sensors presents a significant opportunity for broader deployment. Advancements in AI-powered sensor fusion and perception algorithms are unlocking new levels of autonomy and enabling complex driving scenarios. Strategic partnerships between sensor manufacturers, AI chip providers, and automotive OEMs are crucial for co-development and faster market penetration. The growing demand for autonomous solutions in commercial fleets, logistics, and public transportation also represents a substantial growth catalyst.

Leading Players in the Autonomous Vehicles Sensor Industry Sector

- Infineon Technologies AG

- Microchip Technology Inc

- CEVA Inc

- Aimotive kft

- BASELABS GmbH

- NXP Semiconductor

- STMicroelectronics NV

- Kionix Inc (Rohm Co Ltd)

- Robert Bosch GmbH

- TDK Corporation

Key Milestones in Autonomous Vehicles Sensor Industry Industry

- January 2022: Ambarella Inc. launched the CV3 AI domain controller family during CES, offering up to 500 eTOPS of AI processing performance for multi-sensor perception and AV path planning.

- January 2022: Qualcomm launched the Snapdragon Ride Vision System, an open and scalable platform for automated driving, supporting customization and integration of various automotive technologies.

Strategic Outlook for Autonomous Vehicles Sensor Industry Market

The strategic outlook for the autonomous vehicles sensor industry is highly optimistic, driven by ongoing technological advancements and expanding market applications. Future growth will be accelerated by the continued miniaturization and cost reduction of sensor technologies, enabling wider adoption across all vehicle segments. The increasing sophistication of AI and machine learning for sensor fusion will unlock higher levels of autonomous driving capabilities. Strategic alliances and collaborations will play a crucial role in accelerating development and bringing new solutions to market. The growing deployment of autonomous vehicles in commercial sectors, such as logistics and ride-sharing, will be a significant growth accelerator, driving demand for reliable and high-performance sensor systems.

Autonomous Vehicles Sensor Industry Segmentation

-

1. Types of Vehicle

- 1.1. Passenger Cars

- 1.2. Light Commercial Vehicle (LCV)

- 1.3. Heavy Commercial Vehicle (HCV)

- 1.4. Other Autonomous Vehicles

Autonomous Vehicles Sensor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Autonomous Vehicles Sensor Industry Regional Market Share

Geographic Coverage of Autonomous Vehicles Sensor Industry

Autonomous Vehicles Sensor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 5.1.1. Passenger Cars

- 5.1.2. Light Commercial Vehicle (LCV)

- 5.1.3. Heavy Commercial Vehicle (HCV)

- 5.1.4. Other Autonomous Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 6. Global Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 6.1.1. Passenger Cars

- 6.1.2. Light Commercial Vehicle (LCV)

- 6.1.3. Heavy Commercial Vehicle (HCV)

- 6.1.4. Other Autonomous Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 7. North America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 7.1.1. Passenger Cars

- 7.1.2. Light Commercial Vehicle (LCV)

- 7.1.3. Heavy Commercial Vehicle (HCV)

- 7.1.4. Other Autonomous Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 8. Europe Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 8.1.1. Passenger Cars

- 8.1.2. Light Commercial Vehicle (LCV)

- 8.1.3. Heavy Commercial Vehicle (HCV)

- 8.1.4. Other Autonomous Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 9. Asia Pacific Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 9.1.1. Passenger Cars

- 9.1.2. Light Commercial Vehicle (LCV)

- 9.1.3. Heavy Commercial Vehicle (HCV)

- 9.1.4. Other Autonomous Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 10. Latin America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 10.1.1. Passenger Cars

- 10.1.2. Light Commercial Vehicle (LCV)

- 10.1.3. Heavy Commercial Vehicle (HCV)

- 10.1.4. Other Autonomous Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 11. Middle East Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 11.1.1. Passenger Cars

- 11.1.2. Light Commercial Vehicle (LCV)

- 11.1.3. Heavy Commercial Vehicle (HCV)

- 11.1.4. Other Autonomous Vehicles

- 11.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infineon Technologies AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Microchip Technology Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 CEVA Inc *List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Aimotive kft

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BASELABS GmbH

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NXP Semiconductor

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 STMicroelectronics NV

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Kionix Inc (Rohm Co Ltd)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Robert Bosch GmbH

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 TDK Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Infineon Technologies AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Autonomous Vehicles Sensor Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 3: North America Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 4: North America Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 7: Europe Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 8: Europe Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 11: Asia Pacific Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 12: Asia Pacific Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 15: Latin America Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 16: Latin America Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Latin America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 19: Middle East Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 20: Middle East Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 2: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 4: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 6: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 8: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 10: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 12: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autonomous Vehicles Sensor Industry?

The projected CAGR is approximately 11.9%.

2. Which companies are prominent players in the Autonomous Vehicles Sensor Industry?

Key companies in the market include Infineon Technologies AG, Microchip Technology Inc, CEVA Inc *List Not Exhaustive, Aimotive kft, BASELABS GmbH, NXP Semiconductor, STMicroelectronics NV, Kionix Inc (Rohm Co Ltd), Robert Bosch GmbH, TDK Corporation.

3. What are the main segments of the Autonomous Vehicles Sensor Industry?

The market segments include Types of Vehicle.

4. Can you provide details about the market size?

The market size is estimated to be USD 39.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Autonomous Vehicles; Efficient Real Time Data Processing and Data Sharing Capabilities to Drive the Demand.

6. What are the notable trends driving market growth?

Passenger Cars to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Lack of Standardization in Sensor Fusion Technology.

8. Can you provide examples of recent developments in the market?

January 2022 - Ambarella Inc., an AI vision silicon company, launched the CV3 AI domain controller family during CES. This power-efficient and fully scalable CVflow family of SoCs provides the automotive industry's highest AI processing performance at up to 500 eTOPS. Furthermore, the product family enables centralized, single-chip processing for multi-sensor perception-including radar, high-resolution vision, ultrasonic, and lidar- and AV path planning and deep fusion for multiple sensor modalities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autonomous Vehicles Sensor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autonomous Vehicles Sensor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autonomous Vehicles Sensor Industry?

To stay informed about further developments, trends, and reports in the Autonomous Vehicles Sensor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence