Key Insights

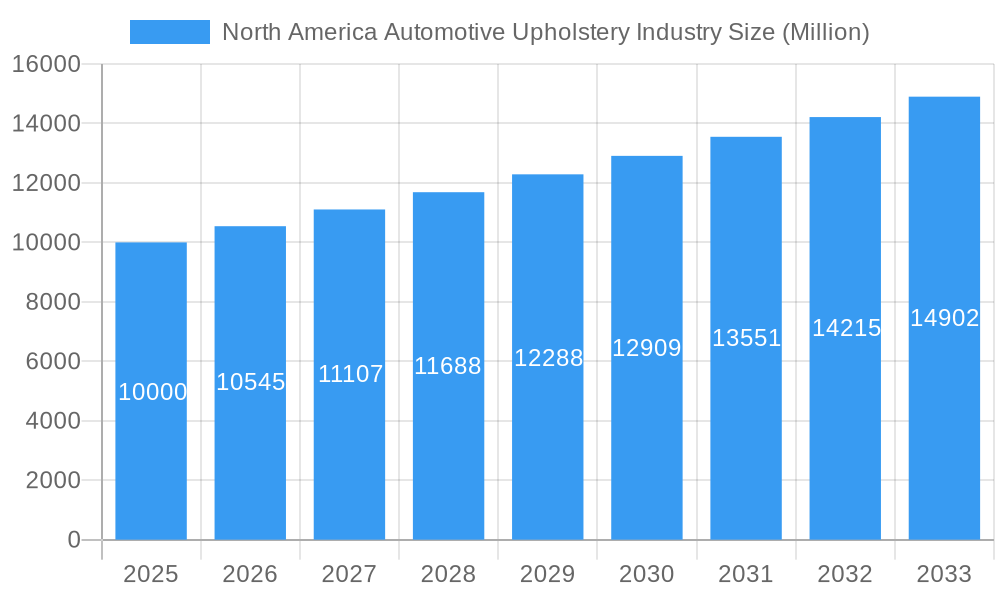

The North American automotive upholstery market, valued at approximately $22.5 billion in 2025, is projected to grow at a compound annual growth rate (CAGR) of 5.7%. Key growth drivers include the rising demand for luxury vehicles and customized interiors, favoring premium upholstery materials such as leather. Advancements in material technology, including sustainable and durable options like innovative vinyl and recycled fabrics, are also shaping industry trends. The increasing popularity of SUVs and light trucks, which inherently require more upholstery, further fuels market expansion. The aftermarket segment presents significant potential, driven by consumer interest in personalized vehicle aesthetics and the growing trend of vehicle restoration and customization. Strategic OEM partnerships are instrumental in influencing material choices and design direction.

North America Automotive Upholstery Industry Market Size (In Billion)

Market restraints include fluctuations in raw material prices, particularly for leather, which can affect profitability. Rising labor costs and stringent environmental regulations for manufacturing processes also pose ongoing challenges. Intense competition from established and emerging manufacturers offering innovative and cost-effective solutions adds to market complexity. Despite these factors, the long-term outlook is positive, supported by anticipated growth in vehicle production, an expanding middle class with increased disposable income, and continuous innovation in upholstery materials and manufacturing techniques. Segmentation analysis indicates that leather currently leads the market share, followed by vinyl, aligning with consumer preferences. While OEM sales channels remain dominant, the aftermarket channel is experiencing considerable growth due to heightened consumer demand for vehicle personalization.

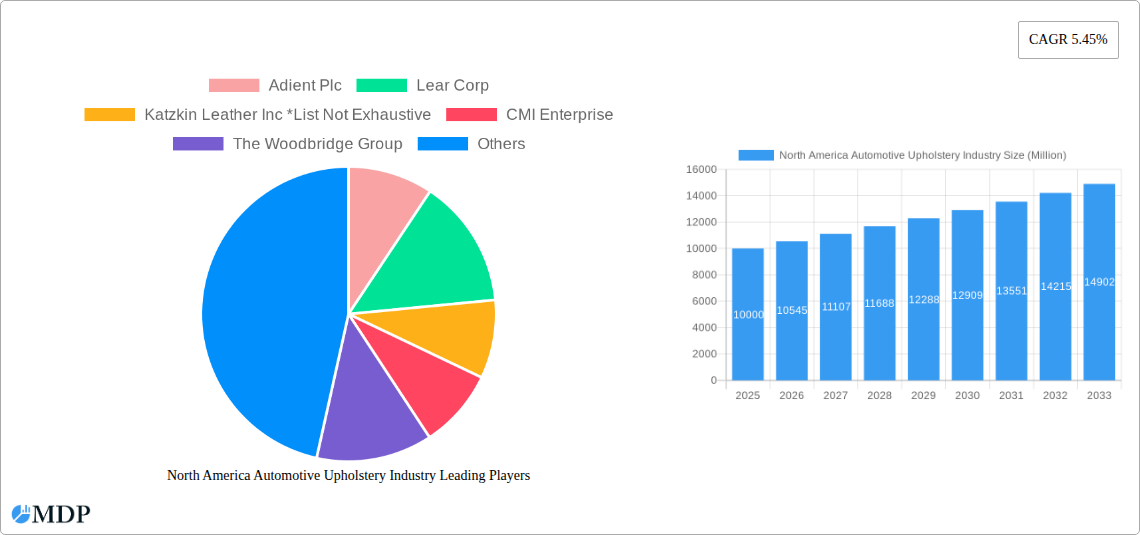

North America Automotive Upholstery Industry Company Market Share

North America Automotive Upholstery Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the North America automotive upholstery industry, covering market dynamics, trends, leading players, and future prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for industry stakeholders, investors, and strategic decision-makers. The market is projected to reach xx Million by 2033, showcasing substantial growth opportunities.

North America Automotive Upholstery Industry Market Dynamics & Concentration

The North American automotive upholstery market is characterized by a moderately concentrated landscape, with key players like Adient Plc, Lear Corp, and Faurecia SE holding significant market share. However, the presence of several smaller, specialized companies, such as Katzkin Leather Inc and CMI Enterprise, indicates a dynamic competitive environment. Market concentration is expected to remain relatively stable, with a slight increase due to potential mergers and acquisitions (M&A) activities. The industry is driven by innovation in materials (e.g., sustainable and vegan alternatives), advancements in manufacturing processes, and evolving consumer preferences towards enhanced comfort and customization. Stringent regulatory frameworks concerning emissions and material safety significantly influence industry practices. Product substitutes, such as fabric upholstery or advanced textile blends, pose a moderate competitive threat. End-user trends lean toward increased demand for luxury features, personalization, and environmentally friendly materials.

- Market Share: Adient Plc (xx%), Lear Corp (xx%), Faurecia SE (xx%), Others (xx%).

- M&A Deal Count (2019-2024): xx

- Innovation Drivers: Sustainable materials, advanced manufacturing techniques, customization options.

- Regulatory Frameworks: Safety standards, emission regulations.

- Product Substitutes: High-performance fabrics, alternative materials.

- End-User Trends: Increased demand for luxury, comfort, and sustainability.

North America Automotive Upholstery Industry Industry Trends & Analysis

The North American automotive upholstery market is experiencing robust growth, driven by several key factors. The increasing production of vehicles, especially SUVs and luxury cars, fuels demand for high-quality upholstery. Technological advancements, such as the introduction of lightweight and sustainable materials, are reshaping the industry. Consumers increasingly prioritize comfort, aesthetics, and sustainability, influencing material choices and design trends. The rise of electric vehicles (EVs) also presents both challenges and opportunities, requiring the development of specific upholstery materials that meet the unique needs of EV interiors. Competitive dynamics are marked by innovation in materials, design, and manufacturing processes, along with a focus on cost optimization and supply chain resilience. The market is anticipated to register a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), with significant market penetration of new material types and technologies.

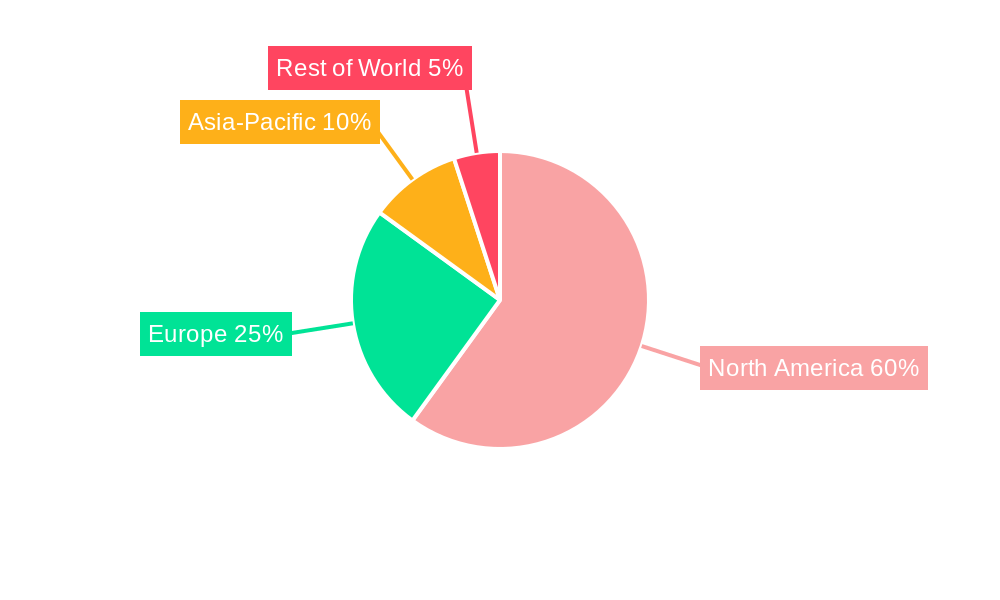

Leading Markets & Segments in North America Automotive Upholstery Industry

The automotive upholstery market in North America is largely dominated by the OEM (Original Equipment Manufacturer) sales channel. The Seats segment constitutes the most significant product category, followed by door trim and roof liners. Within material types, leather and vinyl hold the largest market shares, while the demand for "other material types," including sustainable and vegan options, is steadily increasing. The US remains the leading market, followed by Canada and Mexico. Key drivers contributing to regional dominance include robust automotive production, consumer spending habits, and existing infrastructure. The luxury vehicle segment is a particularly significant growth area, with high demand for premium materials and advanced features.

- Key Drivers (US): High automotive production, strong consumer spending, well-established infrastructure.

- Key Drivers (Canada): Growing automotive manufacturing, focus on eco-friendly materials.

- Key Drivers (Mexico): Expanding automotive exports, increasing production capacity.

Dominance Analysis: The US market’s dominance is attributed to its large automotive manufacturing sector and strong consumer demand for high-quality vehicles and premium upholstery.

North America Automotive Upholstery Industry Product Developments

Recent product innovations include the integration of sustainable materials like BIOVYN, advancements in modular seat design for enhanced durability and recyclability, and the development of vegan leather alternatives. These innovations address growing environmental concerns and cater to evolving consumer preferences. The focus on ergonomic design and enhanced comfort contributes to a superior driving experience. These advancements offer a competitive advantage by improving vehicle interiors' sustainability, comfort, and longevity.

Key Drivers of North America Automotive Upholstery Industry Growth

Several factors drive the industry's growth. Firstly, the rising production of vehicles across North America fuels demand for upholstery. Secondly, the increasing preference for luxury and customized features in automobiles creates a demand for premium materials and innovative designs. Thirdly, technological advancements in material science and manufacturing processes continue to improve the quality, comfort, and sustainability of automotive upholstery. Regulatory pressures towards eco-friendly materials also spur innovation and market growth.

Challenges in the North America Automotive Upholstery Industry Market

The automotive upholstery industry faces challenges like fluctuating raw material prices, supply chain disruptions, and intense competition. These factors can impact production costs and profitability. Furthermore, stringent environmental regulations necessitate investments in sustainable materials and technologies. These challenges necessitate strategic planning and resource allocation to maintain competitiveness and meet evolving market demands. The impact of these challenges can be measured in reduced profit margins (estimated xx% reduction in 2024) and potential production delays.

Emerging Opportunities in North America Automotive Upholstery Industry

The industry offers significant opportunities. The growing demand for sustainable and eco-friendly materials presents avenues for innovation and differentiation. Strategic partnerships with material suppliers and technology providers enhance competitiveness and access to cutting-edge technologies. Expanding into new markets and offering personalized and customizable upholstery options provides a path towards higher revenue streams and market share gains. Technological breakthroughs like advanced manufacturing techniques create avenues for higher quality and cost-effective solutions.

Leading Players in the North America Automotive Upholstery Industry Sector

- Adient Plc

- Lear Corp

- Katzkin Leather Inc

- CMI Enterprise

- The Woodbridge Group

- IMS Nonwoven

- Seiren Co Ltd

- Toyota Boshoku Corp

- Faurecia SE

Key Milestones in North America Automotive Upholstery Industry Industry

- September 2022: The BMW Group announced its intention to introduce vehicles with fully vegan interiors in 2023, showcasing a rising trend towards plant-based materials.

- November 2022: Polestar's integration of INEOS BIOVYN in its Polestar 3 SUV highlights the adoption of sustainable vinyl in the automotive upholstery industry.

- June 2023: Lexus launched the revamped 2024 GX, featuring ergonomic seat upgrades that improve driving posture and comfort, driving up sales and increasing the standards for seating.

- June 2023: Faurecia introduced a novel modular and sustainable seat design, promoting improved durability and recyclability, setting the standard for future sustainable production.

- August 2023: Bentley unveiled the Bentayga EWB Mulliner, featuring the "world's most sophisticated vehicle seating arrangement," setting a new benchmark for luxury vehicle interiors and demonstrating innovation in premium seating solutions.

Strategic Outlook for North America Automotive Upholstery Industry Market

The North America automotive upholstery market holds significant future potential, fueled by the continuous growth of the automotive sector and rising consumer demand for comfort, customization, and sustainability. Strategic opportunities include investing in sustainable material development, focusing on ergonomic designs, and capitalizing on the rising popularity of luxury and electric vehicles. The market is poised for continued growth driven by technological innovation and evolving consumer preferences. Companies that proactively address sustainability concerns and incorporate cutting-edge technologies will be best positioned for success.

North America Automotive Upholstery Industry Segmentation

-

1. Material Type

- 1.1. Leather

- 1.2. Vinyl

- 1.3. Other Material Types

-

2. Sales Channel

- 2.1. OEM

- 2.2. Aftermarket

-

3. Product

- 3.1. Dashboard

- 3.2. Seats

- 3.3. Roof Liners

- 3.4. Door Trim

North America Automotive Upholstery Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest Of North America

North America Automotive Upholstery Industry Regional Market Share

Geographic Coverage of North America Automotive Upholstery Industry

North America Automotive Upholstery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Leather

- 5.1.2. Vinyl

- 5.1.3. Other Material Types

- 5.2. Market Analysis, Insights and Forecast - by Sales Channel

- 5.2.1. OEM

- 5.2.2. Aftermarket

- 5.3. Market Analysis, Insights and Forecast - by Product

- 5.3.1. Dashboard

- 5.3.2. Seats

- 5.3.3. Roof Liners

- 5.3.4. Door Trim

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest Of North America

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Leather

- 6.1.2. Vinyl

- 6.1.3. Other Material Types

- 6.2. Market Analysis, Insights and Forecast - by Sales Channel

- 6.2.1. OEM

- 6.2.2. Aftermarket

- 6.3. Market Analysis, Insights and Forecast - by Product

- 6.3.1. Dashboard

- 6.3.2. Seats

- 6.3.3. Roof Liners

- 6.3.4. Door Trim

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. United States North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Leather

- 7.1.2. Vinyl

- 7.1.3. Other Material Types

- 7.2. Market Analysis, Insights and Forecast - by Sales Channel

- 7.2.1. OEM

- 7.2.2. Aftermarket

- 7.3. Market Analysis, Insights and Forecast - by Product

- 7.3.1. Dashboard

- 7.3.2. Seats

- 7.3.3. Roof Liners

- 7.3.4. Door Trim

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Canada North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Leather

- 8.1.2. Vinyl

- 8.1.3. Other Material Types

- 8.2. Market Analysis, Insights and Forecast - by Sales Channel

- 8.2.1. OEM

- 8.2.2. Aftermarket

- 8.3. Market Analysis, Insights and Forecast - by Product

- 8.3.1. Dashboard

- 8.3.2. Seats

- 8.3.3. Roof Liners

- 8.3.4. Door Trim

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Rest Of North America North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Leather

- 9.1.2. Vinyl

- 9.1.3. Other Material Types

- 9.2. Market Analysis, Insights and Forecast - by Sales Channel

- 9.2.1. OEM

- 9.2.2. Aftermarket

- 9.3. Market Analysis, Insights and Forecast - by Product

- 9.3.1. Dashboard

- 9.3.2. Seats

- 9.3.3. Roof Liners

- 9.3.4. Door Trim

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Adient Plc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Lear Corp

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Katzkin Leather Inc *List Not Exhaustive

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 CMI Enterprise

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 The Woodbridge Group

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 IMS Nonwoven

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Seiren Co Ltd

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Toyota Boshoku Corp

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Faurecia SE

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Adient Plc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Automotive Upholstery Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Automotive Upholstery Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 3: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 4: North America Automotive Upholstery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 7: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 8: North America Automotive Upholstery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 10: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 11: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 12: North America Automotive Upholstery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 14: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 15: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 16: North America Automotive Upholstery Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Upholstery Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the North America Automotive Upholstery Industry?

Key companies in the market include Adient Plc, Lear Corp, Katzkin Leather Inc *List Not Exhaustive, CMI Enterprise, The Woodbridge Group, IMS Nonwoven, Seiren Co Ltd, Toyota Boshoku Corp, Faurecia SE.

3. What are the main segments of the North America Automotive Upholstery Industry?

The market segments include Material Type, Sales Channel, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 22.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Passenger Car Sales Propelling Market Growth.

6. What are the notable trends driving market growth?

Increasing Demand for Aftermarket Upholstery Modifications May Drive the Market.

7. Are there any restraints impacting market growth?

Fluctuation in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

August 2023: Bentley unveiled the Bentayga Extended Wheelbase Mulliner during Monterey Car Week in California. The Bentayga EWB Mulliner flagship has greater cabin room than any similar premium competition, owing to its Airline Seats. The rear compartment, which is available in 4+1 and 4-seat configurations, comes standard with the Bentley Airline Seat specification, the world's most sophisticated vehicle seating arrangement.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Upholstery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Upholstery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Upholstery Industry?

To stay informed about further developments, trends, and reports in the North America Automotive Upholstery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence