Key Insights

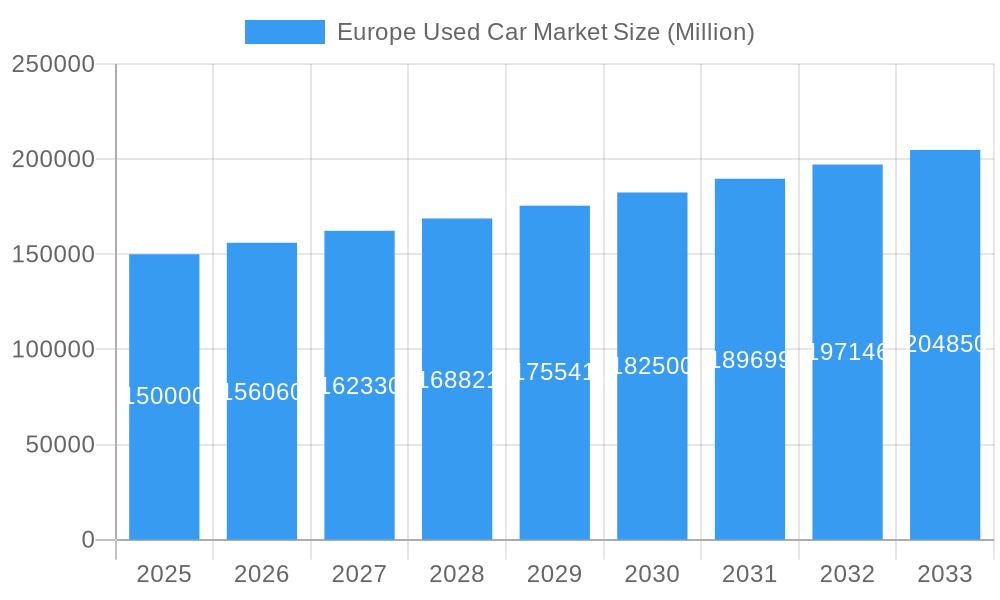

The European Used Car Market is poised for significant expansion, projected to reach 725.3 billion by 2033, with a Compound Annual Growth Rate (CAGR) of 4.6% from the base year 2024. This growth is propelled by increasing consumer demand for cost-effective mobility solutions, influenced by rising new vehicle prices and economic volatility. Enhanced market accessibility and consumer trust are further supported by evolving vehicle financing, leasing options, and a growing selection of certified pre-owned vehicles. Technological advancements and the rising popularity of electric and hybrid used cars are also redefining market segments and driving demand. The market is segmented by vehicle type (hatchback, sedan, SUV, MPV), vendor type (organized, unorganized), fuel type (gasoline, diesel, electric, others), and key geographies (Germany, UK, France, Italy, Spain, Russia, Rest of Europe), offering insights into regional trends and consumer preferences. Germany, the UK, and France are anticipated to maintain their leadership positions, while other European nations present varied growth prospects contingent on economic conditions and infrastructure development.

Europe Used Car Market Market Size (In Billion)

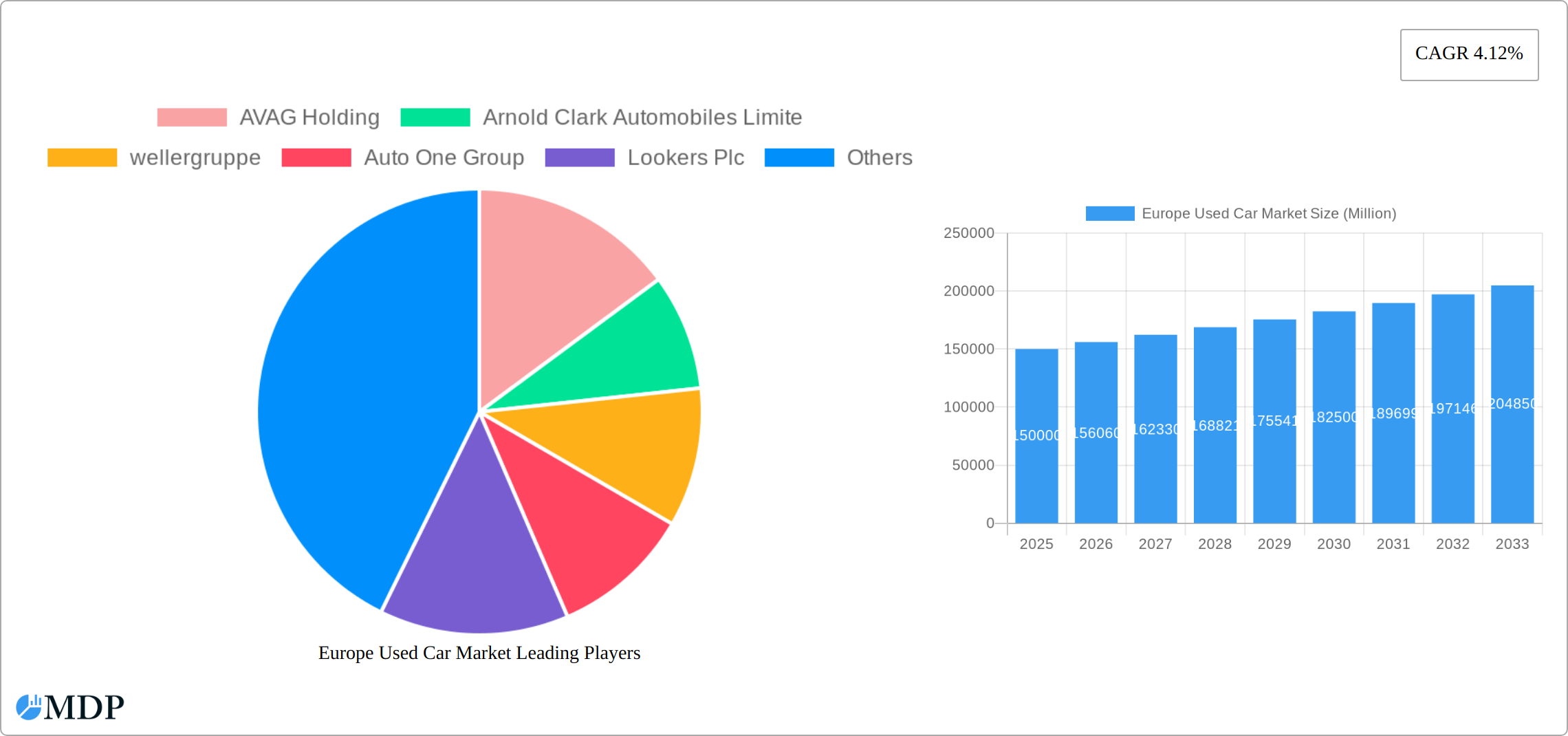

Despite a favorable outlook, potential market restraints include price volatility stemming from global supply chain disruptions and economic downturns. Stringent emission regulations and a shift towards sustainable transportation will impact older, less fuel-efficient vehicles. The expanding adoption of car-sharing and ride-hailing services may also influence overall used car demand. Nevertheless, ongoing population growth and a persistent need for affordable transportation are expected to sustain a positive growth trajectory for the European used car market. Intense competition among established vendors like AVAG Holding and Arnold Clark Automobiles, alongside emerging online marketplaces, will continue to shape market dynamics.

Europe Used Car Market Company Market Share

Europe Used Car Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Europe Used Car Market, covering market dynamics, industry trends, leading segments, key players, and future outlook. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. This report is crucial for industry stakeholders, investors, and businesses seeking to understand and capitalize on the opportunities within this dynamic market. It incorporates data and insights for crucial segments including vehicle types (Hatchback, Sedan, SUV, MPV), vendor types (Organized, Unorganized), fuel types (Gasoline, Diesel, Electric, Other), and key European countries (Germany, UK, France, Italy, Spain, Russia, Rest of Europe). The report value is xx Million.

Europe Used Car Market Market Dynamics & Concentration

The European used car market is a dynamic and evolving ecosystem, characterized by a blend of established, large-scale players and a fragmented network of independent dealerships. Market concentration is being actively reshaped by ongoing mergers and acquisitions (M&A) activity, the strategic expansion of organized dealership networks, and the disruptive influence of digital marketplaces. Our analysis delves into the impact of diverse regulatory frameworks, including increasingly stringent emission standards and evolving vehicle safety regulations, on shaping market dynamics and operational strategies.

Innovation is a significant driving force, propelled by advancements in online platforms that enhance accessibility and transparency, sophisticated vehicle inspection technologies that build consumer confidence, and flexible financing options. The burgeoning popularity of vehicle subscription services and the accelerated adoption of electric vehicles (EVs) are fundamentally altering consumer preferences and vehicle lifecycle management. While product substitutes like ride-hailing services and public transportation offer a moderate competitive challenge, particularly in densely populated urban areas, their impact is nuanced. End-user trends, such as the enduring preference for SUVs and the surging demand for pre-owned electric vehicles, are pivotal in dictating market demand and future growth trajectories.

- Market Share: The top 5 players are estimated to collectively hold approximately xx% of the market share in 2025, indicating a degree of consolidation.

- M&A Activity: An estimated xx M&A deals were recorded between 2019 and 2024. This trend of consolidation is projected to persist, further influencing the competitive landscape.

Europe Used Car Market Industry Trends & Analysis

The Europe Used Car Market is experiencing robust growth, driven by factors such as increasing disposable incomes, a preference for used vehicles due to affordability, and advancements in vehicle technology extending the lifespan of cars. The market is further influenced by evolving consumer preferences, technological disruptions (e.g., online marketplaces and digital inspection services), and intense competitive dynamics among established players and new entrants. The CAGR for the market during the forecast period (2025-2033) is estimated to be xx%. Market penetration of electric used vehicles is projected to increase to xx% by 2033.

Leading Markets & Segments in Europe Used Car Market

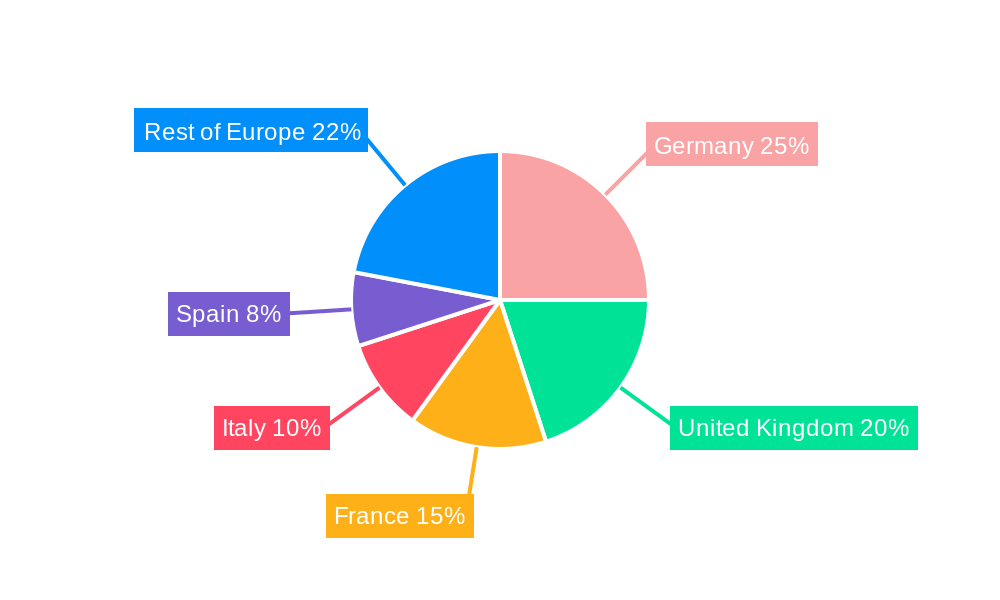

Germany, the United Kingdom, and France stand out as the leading markets within the European used car landscape. This dominance is attributable to a confluence of factors including robust economic conditions, higher disposable incomes, well-developed automotive infrastructure, and a strong presence of organized dealer networks.

Key Drivers for Leading Markets:

- Germany: Fueled by a resilient domestic economy, exceptionally high vehicle ownership rates, and a mature and sophisticated used car market infrastructure, Germany remains a powerhouse.

- United Kingdom: A large and engaged population, coupled with significant demand for pre-owned vehicles and a vibrant ecosystem of online marketplaces, underpins the UK's strong performance.

- France: Benefiting from growing consumer spending, an escalating demand for used electric vehicles, and supportive government incentives promoting greener transportation solutions, France is a key growth market.

Segment Dominance and Emerging Trends:

- Vehicle Type: SUVs and Hatchbacks currently command the largest share. However, a notable increase in MPV sales is projected, driven by evolving family structures and a preference for more spacious and versatile vehicles.

- Vendor Type: The organized sector continues to hold a significant market share, leveraging its established infrastructure, brand equity, and standardized processes. Nevertheless, the unorganized sector remains a substantial contributor to market activity.

- Fuel Type: Gasoline and diesel-powered vehicles continue to dominate the used car market. However, sales of electric vehicles are experiencing consistent and significant growth, signaling a clear shift towards electrification.

Europe Used Car Market Product Developments

The European used car market is witnessing a wave of innovation, particularly in digital platforms. These platforms are increasingly offering enhanced transparency through upfront pricing, sophisticated virtual inspection tools allowing remote vehicle assessment, and streamlined purchasing processes designed for ultimate customer convenience. Advancements in vehicle inspection technologies are also playing a crucial role, ensuring a higher standard of quality assurance for pre-owned vehicles. Furthermore, the strategic integration of data analytics is significantly improving market transparency, enabling more accurate price predictions and trend forecasting. Collectively, these developments are not only enhancing the customer experience but also acting as powerful catalysts for sustained market growth.

Key Drivers of Europe Used Car Market Growth

Several factors drive growth in this sector, including increasing affordability of used vehicles compared to new ones, supportive government policies promoting sustainable mobility (leading to higher demand for used electric cars), and expansion of online marketplaces offering convenient and transparent transactions. Technological advancements in vehicle maintenance and reconditioning extend vehicle lifespans, adding to the supply of quality used cars.

Challenges in the Europe Used Car Market Market

The European used car market navigates several significant challenges. Fluctuations in the supply of used vehicles, exacerbated by global supply chain disruptions like the ongoing chip shortages, continue to impact availability. The complexity and divergence of vehicle emission regulations across different European countries add layers of operational complexity. Intense competition among a vast array of market participants frequently puts pressure on profitability margins. Moreover, fostering and maintaining transparency and trust within the used car market remains a persistent hurdle for both businesses and consumers.

Emerging Opportunities in Europe Used Car Market

The growing demand for electric vehicles presents a significant opportunity, particularly with the increasing availability of used EVs. Strategic partnerships between traditional dealerships and fintech companies can offer better financing options. Expansion into underserved regions and leveraging advanced data analytics to improve pricing and inventory management offer substantial opportunities for growth.

Leading Players in the Europe Used Car Market Sector

- AVAG Holding

- Arnold Clark Automobiles Limited

- Weller Group

- Auto One Group

- Lookers Plc

- Auto Empire Trading GmbH

- Fahrzeug-werke LUEG AG

- Pendragon Plc

- Autorola Group Holding

- Emil Frey AG

- Penske Automotive Group

- Gottfried-Schultz

Key Milestones in Europe Used Car Market Industry

- March 2022: Toyota Motors Europe (TME) partnered with INDICATA Europe to enhance used car pricing data across 13 countries. This improves market transparency and data-driven decision-making for dealers and consumers.

- March 2022: Inchcape's withdrawal from the Russian market highlighted geopolitical risks and their impact on market stability.

- March 2022: TrueCar Inc.'s launch of TrueCar+ showcased the growing importance of online marketplaces and enhanced customer experiences in the used car sector.

Strategic Outlook for Europe Used Car Market Market

The Europe Used Car Market is poised for continued growth, fueled by evolving consumer preferences, technological advancements, and increased focus on sustainable mobility. Strategic opportunities lie in expanding online platforms, embracing data-driven decision-making, and forming strategic partnerships to enhance customer experiences and capture market share. Further consolidation through M&A activity is also expected.

Europe Used Car Market Segmentation

-

1. Vehicle Type

- 1.1. Hatchback

- 1.2. Sedan

- 1.3. Sports Utility Vehicle

- 1.4. Multi-purpose Vehicle

-

2. Vendor Type

- 2.1. Organized

- 2.2. Unorganized

-

3. Fuel Type

- 3.1. Gasoline

- 3.2. Diesel

- 3.3. Electric

- 3.4. Other Fuel Types (LPG, CNG, etc.)

Europe Used Car Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Used Car Market Regional Market Share

Geographic Coverage of Europe Used Car Market

Europe Used Car Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Sales of Forklift; Others

- 3.3. Market Restrains

- 3.3.1. Supply Chain Disruption; Others

- 3.4. Market Trends

- 3.4.1. Online Infrastructure witnessing major growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Used Car Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Hatchback

- 5.1.2. Sedan

- 5.1.3. Sports Utility Vehicle

- 5.1.4. Multi-purpose Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Vendor Type

- 5.2.1. Organized

- 5.2.2. Unorganized

- 5.3. Market Analysis, Insights and Forecast - by Fuel Type

- 5.3.1. Gasoline

- 5.3.2. Diesel

- 5.3.3. Electric

- 5.3.4. Other Fuel Types (LPG, CNG, etc.)

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 AVAG Holding

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Arnold Clark Automobiles Limite

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 wellergruppe

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Auto One Group

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Lookers Plc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Auto Empire Trading GmbH

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Fahrzeug -werke LUEG AG

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Pendragon Plc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Autorola Group Holding

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Emil Frey AG

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Penske Automotive Group

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Gottfried-schultz

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 AVAG Holding

List of Figures

- Figure 1: Europe Used Car Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Used Car Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Used Car Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: Europe Used Car Market Revenue billion Forecast, by Vendor Type 2020 & 2033

- Table 3: Europe Used Car Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 4: Europe Used Car Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Europe Used Car Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 6: Europe Used Car Market Revenue billion Forecast, by Vendor Type 2020 & 2033

- Table 7: Europe Used Car Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 8: Europe Used Car Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Germany Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: France Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Italy Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Spain Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Netherlands Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Belgium Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Sweden Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Norway Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Poland Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Denmark Europe Used Car Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Used Car Market?

The projected CAGR is approximately 4.6%.

2. Which companies are prominent players in the Europe Used Car Market?

Key companies in the market include AVAG Holding, Arnold Clark Automobiles Limite, wellergruppe, Auto One Group, Lookers Plc, Auto Empire Trading GmbH, Fahrzeug -werke LUEG AG, Pendragon Plc, Autorola Group Holding, Emil Frey AG, Penske Automotive Group, Gottfried-schultz.

3. What are the main segments of the Europe Used Car Market?

The market segments include Vehicle Type, Vendor Type, Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 725.3 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Sales of Forklift; Others.

6. What are the notable trends driving market growth?

Online Infrastructure witnessing major growth.

7. Are there any restraints impacting market growth?

Supply Chain Disruption; Others.

8. Can you provide examples of recent developments in the market?

March 2022: Toyota Motors Europe (TME) announced a major new contract with INDICATA Europe to roll out its used car pricing data to 13 countries over the next two months. INDICATA developed a bespoke reporting suite for TME that tracks all the online used Toyota and Lexus adverts from its dealer networks across Europe and presented it into an easy-to-read dashboard for each country.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Used Car Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Used Car Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Used Car Market?

To stay informed about further developments, trends, and reports in the Europe Used Car Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence