Key Insights

The Automotive Modular Seating market is projected to achieve a size of 75.33 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 2.7% through 2033. This expansion is driven by increasing consumer demand for enhanced vehicle comfort, customization, and advanced features. The growing adoption of modular seating in passenger and commercial vehicles offers manufacturers greater interior design flexibility and functionality. Key trends include the integration of smart technologies (heating, cooling, massage), lightweight materials for fuel efficiency, and a rising emphasis on sustainable materials and manufacturing processes. Enhanced occupant safety and advanced seat structures also contribute to market growth.

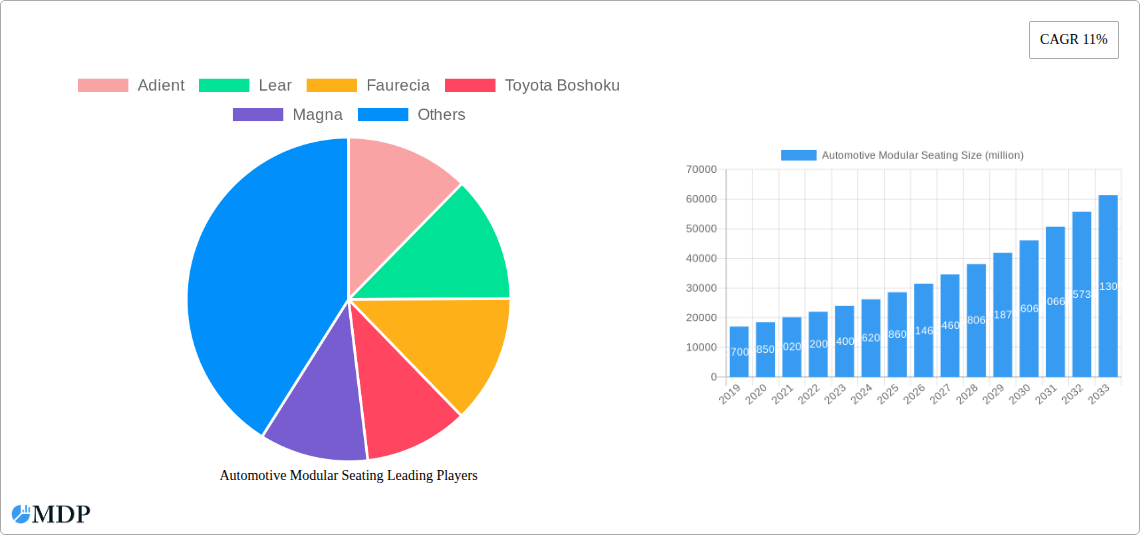

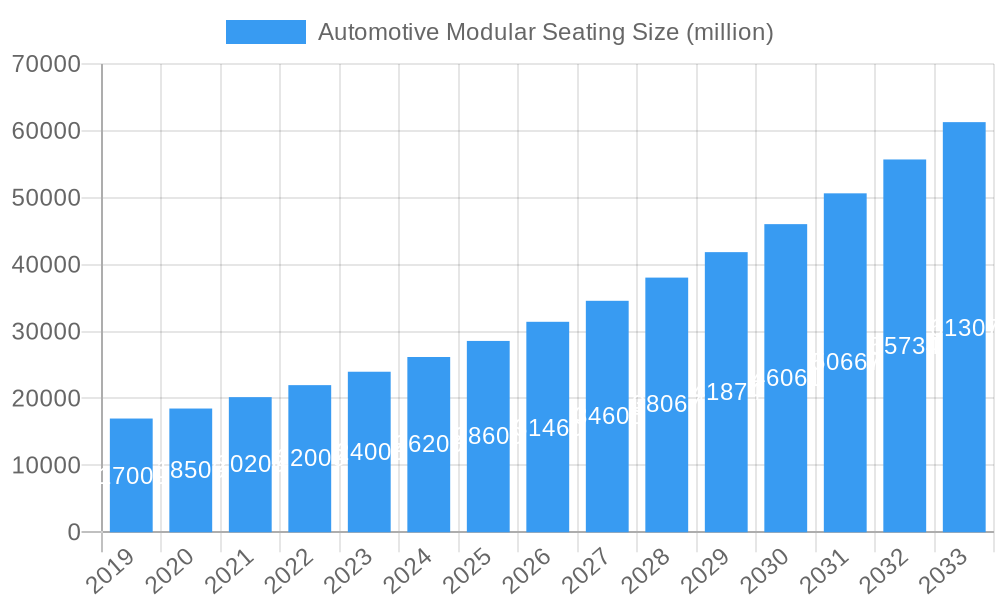

Automotive Modular Seating Market Size (In Billion)

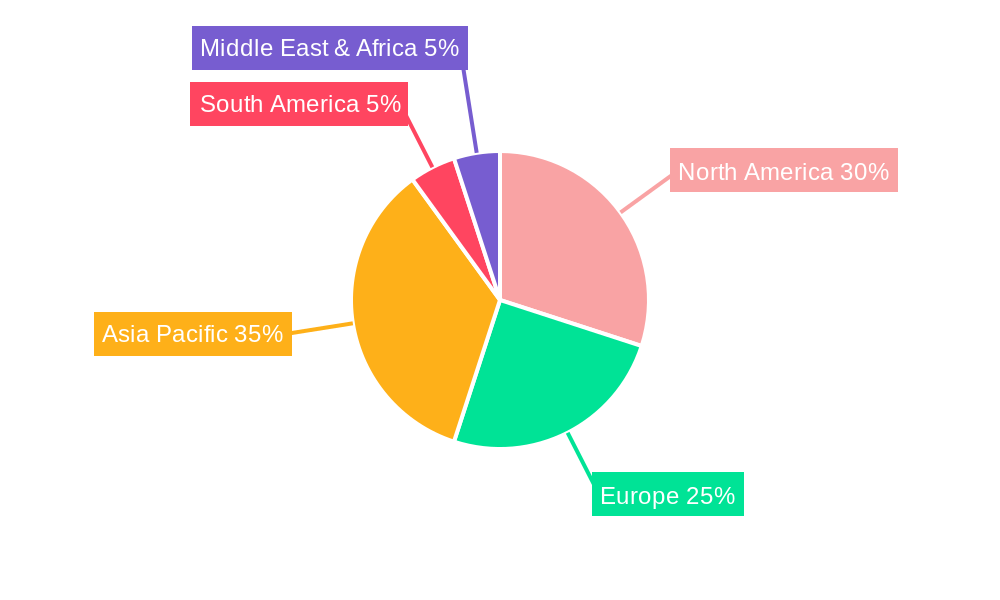

The market segmentation indicates strong demand for Passenger Cars and Fabric Seat types. North America and Asia Pacific are expected to lead market share due to robust automotive production, high vehicle penetration, and a significant presence of component manufacturers. Potential challenges include high initial investment costs for modular systems and supply chain integration complexities. However, continuous technological advancements and automotive interior innovation will propel the market forward. The rise of Advanced Driver-Assistance Systems (ADAS) and autonomous driving necessitates reconfigurable seating, further boosting demand for modular solutions.

Automotive Modular Seating Company Market Share

Automotive Modular Seating Market Analysis: Growth, Trends, and Forecasts (2019-2033)

This report provides in-depth analysis of the global Automotive Modular Seating market, covering evolving automotive interior landscapes, key drivers, trends, and future projections from 2019 to 2033. It is essential for automotive OEMs, Tier 1 suppliers, seating manufacturers, technology providers, investors, and industry analysts seeking to understand market dynamics, competitive strategies, and growth opportunities across passenger car and commercial vehicle segments, including fabric, genuine leather, and other seating types.

Key Market Data: Base Year: 2025, Forecast Period: 2025–2033, Historical Period: 2019–2024.

Leading Industry Players: Adient, Lear, Faurecia, Toyota Boshoku, Magna, TS TECH, Hyundai DYMOS, NHK Spring, Tachi-S.

Key Report Features:

This report offers crucial intelligence for navigating the dynamic Automotive Modular Seating market, expected to see substantial production volumes during the forecast period.

- Market Dynamics & Concentration: Analysis of market share, innovation, regulatory impacts, and M&A activities.

- Industry Trends & Analysis: Identification of growth drivers, technological disruptions, and consumer preferences, with projected CAGR.

- Regional & Segment Analysis: Insights into dominant regions, countries, and application/type segments, including market penetration analysis.

- Product Innovations: Overview of the latest advancements and competitive advantages in modular seating solutions.

- Growth Catalysts: Identification of technological, economic, and regulatory factors driving market expansion.

- Market Restraints: Assessment of barriers including regulatory challenges and supply chain complexities.

- Emerging Opportunities: Exploration of long-term growth avenues through technological advancements and strategic partnerships.

- Key Player Profiles: Comprehensive profiles of major industry participants.

- Industry Milestones: Tracking of significant market developments and their impact.

- Strategic Growth Outlook: Future market potential and actionable strategies.

Automotive Modular Seating Market Dynamics & Concentration

The automotive modular seating market is characterized by a moderate to high level of concentration, with a few key players dominating a significant portion of the global market share. Leading companies such as Adient, Lear, and Faurecia consistently hold substantial market positions, driven by their extensive R&D capabilities, established supply chains, and strong relationships with major automotive OEMs. Innovation remains a critical differentiator, with companies heavily investing in lightweight materials, sustainable manufacturing processes, and enhanced occupant comfort and safety features. Regulatory frameworks worldwide, particularly concerning emissions, safety standards, and recyclability, are increasingly influencing product development and material choices. The availability of effective product substitutes, while present in the form of traditional integrated seating solutions, is diminishing as the advantages of modularity—such as faster assembly times, greater customization, and simplified repair and replacement—become more apparent. End-user trends are shifting towards personalized interiors, enhanced connectivity, and sustainable materials, compelling manufacturers to adapt their offerings. Mergers and acquisitions (M&A) activity within the sector, though not at a fever pitch, plays a crucial role in consolidation and technology acquisition. Recent years have seen several strategic deals aimed at expanding geographical reach or acquiring specialized expertise, contributing to an estimated xx million in M&A deal values over the historical and forecast periods.

Automotive Modular Seating Industry Trends & Analysis

The global automotive modular seating market is poised for robust growth, driven by a confluence of factors including the accelerating adoption of electric vehicles (EVs), the increasing demand for personalized and customizable interior experiences, and the persistent push for manufacturing efficiency within the automotive industry. The shift towards EVs, in particular, presents a significant opportunity for modular seating. The unique architecture of EVs often allows for greater design freedom in interior layout, making modular seating systems that can be easily reconfigured for different battery pack sizes and passenger configurations highly desirable. Technological disruptions are at the forefront of market evolution. Advanced manufacturing techniques such as 3D printing are enabling the creation of complex, lightweight seating structures that were previously unfeasible. Furthermore, the integration of smart technologies, including sensors for occupant detection, posture adjustment, and even climate control within the seating system, is becoming a key selling point. Consumer preferences are rapidly evolving. Beyond basic comfort and aesthetics, car buyers are increasingly seeking interiors that offer flexibility, connectivity, and a premium feel. This translates to a higher demand for modular seating that can adapt to various use cases, from family travel to mobile workspaces. The competitive dynamics within the industry are intense. Established Tier 1 suppliers are continually innovating to maintain their market share, while new entrants with specialized technologies are emerging. The focus is on providing holistic interior solutions that go beyond just the seats, encompassing the entire cabin experience. The market penetration of modular seating is steadily increasing, projected to reach approximately xx% by the end of the forecast period, a testament to its growing acceptance and strategic importance in modern vehicle design. The market is expected to witness a Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period. The market size is estimated to grow from approximately $xx million in 2024 to $xx million by 2033.

Leading Markets & Segments in Automotive Modular Seating

The Passenger Car segment undeniably leads the global automotive modular seating market, accounting for over xx% of the total market value. This dominance is fueled by several key drivers. Firstly, the sheer volume of passenger car production worldwide, coupled with the increasing consumer demand for advanced features and personalized interiors in this segment, creates a massive market for modular solutions. Economic policies in major automotive manufacturing hubs, such as North America, Europe, and Asia-Pacific, often encourage innovation and the adoption of advanced manufacturing technologies, directly benefiting the modular seating sector. Infrastructure development, particularly in emerging economies, supports the expansion of automotive production, further driving demand.

Within the Passenger Car application, the Fabric Seat type currently holds the largest market share, estimated at over xx%. This is primarily due to its cost-effectiveness, durability, and wide range of customization options, making it a popular choice for mainstream passenger vehicles. However, the Genuine Leather Seat segment is witnessing significant growth, driven by the rising demand for premium interiors and the increasing affordability of high-quality leather treatments. The "Others" category, which includes sustainable and innovative materials like vegan leather and advanced textiles, is also poised for substantial expansion as environmental consciousness grows among consumers and manufacturers.

The Commercial Vehicle segment, while smaller in terms of overall market share (estimated at approximately xx%), presents a substantial growth opportunity. The increasing focus on driver comfort, ergonomics, and specialized functionalities in commercial vehicles, such as long-haul trucking and last-mile delivery vans, is driving the adoption of modular seating solutions. Factors like fuel efficiency mandates and the need for durable, easy-to-maintain interiors further bolster the demand for well-designed modular seating in this sector. Key drivers for dominance in these segments include:

- Volume Production: The sheer number of passenger cars manufactured globally.

- Consumer Demand for Customization: Desire for personalized and premium interior features.

- Technological Integration: Ease of incorporating smart features into modular designs.

- Cost-Effectiveness (Fabric Seats): Traditional preference for durable and affordable materials.

- Premium Appeal (Genuine Leather Seats): Growing demand for luxury and comfort.

- Sustainability Initiatives (Others): Increasing consumer and regulatory focus on eco-friendly materials.

- Driver Comfort & Ergonomics (Commercial Vehicles): Essential for productivity and safety in professional driving.

Automotive Modular Seating Product Developments

Product innovation in automotive modular seating is characterized by a focus on lightweight construction, enhanced comfort, and advanced functionality. Manufacturers are increasingly employing composite materials and optimized structural designs to reduce vehicle weight, contributing to improved fuel efficiency and EV range. The integration of smart features, such as integrated heating and cooling systems, multi-way power adjustments, and memory functions, is becoming standard, catering to evolving consumer expectations for a premium and personalized cabin experience. Furthermore, the development of sustainable and recycled materials for upholstery and structural components is a significant trend, aligning with global environmental initiatives. These advancements not only offer competitive advantages by meeting stringent regulatory requirements and consumer preferences but also enable OEMs to achieve faster assembly times and greater design flexibility.

Key Drivers of Automotive Modular Seating Growth

The automotive modular seating market is propelled by several interconnected growth drivers. The accelerating transition to electric vehicles (EVs) creates new opportunities for flexible and adaptable interior designs, where modular seating plays a crucial role. The increasing consumer demand for personalized and sophisticated in-car experiences, including enhanced comfort and connectivity, directly fuels the adoption of advanced modular seating solutions. Furthermore, stringent regulations focused on vehicle safety, lightweighting for emissions reduction, and the use of sustainable materials are compelling manufacturers to innovate, with modularity offering a path to meet these requirements efficiently. The pursuit of manufacturing efficiency and reduced assembly times by automotive OEMs also acts as a significant catalyst, as modular systems streamline production processes.

Challenges in the Automotive Modular Seating Market

Despite its growth potential, the automotive modular seating market faces several challenges. Navigating complex and evolving global regulatory landscapes, particularly concerning safety standards and material certifications, can be a significant hurdle. Supply chain disruptions, as witnessed in recent years, can impact the availability and cost of raw materials and components, affecting production timelines and profitability. Intense competition from established players and emerging innovators puts pressure on pricing and margins. The high initial investment required for research and development of new modular technologies and manufacturing processes can also be a barrier for smaller companies. Additionally, overcoming the inertia associated with traditional, integrated seating designs and educating the market about the long-term benefits of modularity remains an ongoing effort.

Emerging Opportunities in Automotive Modular Seating

Emerging opportunities in the automotive modular seating market are largely driven by technological advancements and evolving consumer expectations. The continued growth of the EV market will unlock further design freedom, enabling entirely new configurations and functionalities for modular seating systems, such as integrated battery thermal management solutions. The development of advanced human-machine interfaces (HMIs) and the integration of augmented reality (AR) within the cabin could lead to highly interactive and personalized seating experiences. Strategic partnerships between seating manufacturers, technology providers, and AI specialists can accelerate the development of intelligent seating solutions that proactively adapt to passenger needs. Furthermore, the increasing focus on circular economy principles presents opportunities for modular designs that facilitate easier disassembly, repair, and recycling of seating components at the end of a vehicle's life.

Leading Players in the Automotive Modular Seating Sector

- Adient

- Lear

- Faurecia

- Toyota Boshoku

- Magna

- TS TECH

- Hyundai DYMOS

- NHK Spring

- Tachi-S

Key Milestones in Automotive Modular Seating Industry

- 2019: Increased focus on sustainable materials and recycling initiatives in seating production.

- 2020: Heightened awareness and development of lightweight seating solutions for improved fuel efficiency.

- 2021: Growing integration of smart technologies within seating systems, including sensors and connectivity features.

- 2022: Significant investments in R&D for modular seating adaptable to EV architectures.

- 2023: Several strategic partnerships formed to enhance technological capabilities and market reach.

- 2024: Emergence of advanced manufacturing techniques like 3D printing for complex seating components.

Strategic Outlook for Automotive Modular Seating Market

The strategic outlook for the automotive modular seating market is exceptionally positive, driven by the ongoing automotive transformation and evolving consumer demands. The continued electrification of vehicles will be a primary growth accelerator, enabling designers to rethink interior spaces and leverage modularity for optimal functionality and passenger experience. The increasing emphasis on sustainability will further propel innovation in eco-friendly materials and manufacturing processes. Strategic opportunities lie in developing highly integrated seating systems that offer advanced features such as personalized comfort, advanced connectivity, and enhanced safety. Collaboration between OEMs, Tier 1 suppliers, and technology providers will be crucial to unlock the full potential of modular seating, leading to more intelligent, adaptable, and user-centric automotive interiors.

Automotive Modular Seating Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Vehicle

-

2. Type

- 2.1. Fabric Seat

- 2.2. Genuine Leather Seat

- 2.3. Others

Automotive Modular Seating Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Modular Seating Regional Market Share

Geographic Coverage of Automotive Modular Seating

Automotive Modular Seating REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Modular Seating Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Fabric Seat

- 5.2.2. Genuine Leather Seat

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Modular Seating Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Fabric Seat

- 6.2.2. Genuine Leather Seat

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Modular Seating Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Fabric Seat

- 7.2.2. Genuine Leather Seat

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Modular Seating Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Fabric Seat

- 8.2.2. Genuine Leather Seat

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Modular Seating Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Fabric Seat

- 9.2.2. Genuine Leather Seat

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Modular Seating Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Fabric Seat

- 10.2.2. Genuine Leather Seat

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Adient

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Lear

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Faurecia

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Toyota Boshoku

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Magna

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 TS TECH

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hyundai DYMOS

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 NHK Spring

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Tachi-S

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Adient

List of Figures

- Figure 1: Global Automotive Modular Seating Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Automotive Modular Seating Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Automotive Modular Seating Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Automotive Modular Seating Volume (K), by Application 2025 & 2033

- Figure 5: North America Automotive Modular Seating Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Automotive Modular Seating Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Automotive Modular Seating Revenue (billion), by Type 2025 & 2033

- Figure 8: North America Automotive Modular Seating Volume (K), by Type 2025 & 2033

- Figure 9: North America Automotive Modular Seating Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Automotive Modular Seating Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Automotive Modular Seating Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Automotive Modular Seating Volume (K), by Country 2025 & 2033

- Figure 13: North America Automotive Modular Seating Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Automotive Modular Seating Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Automotive Modular Seating Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Automotive Modular Seating Volume (K), by Application 2025 & 2033

- Figure 17: South America Automotive Modular Seating Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Automotive Modular Seating Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Automotive Modular Seating Revenue (billion), by Type 2025 & 2033

- Figure 20: South America Automotive Modular Seating Volume (K), by Type 2025 & 2033

- Figure 21: South America Automotive Modular Seating Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Automotive Modular Seating Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Automotive Modular Seating Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Automotive Modular Seating Volume (K), by Country 2025 & 2033

- Figure 25: South America Automotive Modular Seating Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Automotive Modular Seating Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Automotive Modular Seating Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Automotive Modular Seating Volume (K), by Application 2025 & 2033

- Figure 29: Europe Automotive Modular Seating Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Automotive Modular Seating Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Automotive Modular Seating Revenue (billion), by Type 2025 & 2033

- Figure 32: Europe Automotive Modular Seating Volume (K), by Type 2025 & 2033

- Figure 33: Europe Automotive Modular Seating Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Automotive Modular Seating Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Automotive Modular Seating Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Automotive Modular Seating Volume (K), by Country 2025 & 2033

- Figure 37: Europe Automotive Modular Seating Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Automotive Modular Seating Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Automotive Modular Seating Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Automotive Modular Seating Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Automotive Modular Seating Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Automotive Modular Seating Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Automotive Modular Seating Revenue (billion), by Type 2025 & 2033

- Figure 44: Middle East & Africa Automotive Modular Seating Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Automotive Modular Seating Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Automotive Modular Seating Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Automotive Modular Seating Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Automotive Modular Seating Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Automotive Modular Seating Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Automotive Modular Seating Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Automotive Modular Seating Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Automotive Modular Seating Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Automotive Modular Seating Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Automotive Modular Seating Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Automotive Modular Seating Revenue (billion), by Type 2025 & 2033

- Figure 56: Asia Pacific Automotive Modular Seating Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Automotive Modular Seating Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Automotive Modular Seating Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Automotive Modular Seating Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Automotive Modular Seating Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Automotive Modular Seating Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Automotive Modular Seating Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Modular Seating Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Modular Seating Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Automotive Modular Seating Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Automotive Modular Seating Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Automotive Modular Seating Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Automotive Modular Seating Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Automotive Modular Seating Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Automotive Modular Seating Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Automotive Modular Seating Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Automotive Modular Seating Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Automotive Modular Seating Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Automotive Modular Seating Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Automotive Modular Seating Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Automotive Modular Seating Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Automotive Modular Seating Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Automotive Modular Seating Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Automotive Modular Seating Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Automotive Modular Seating Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Automotive Modular Seating Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Automotive Modular Seating Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Automotive Modular Seating Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Automotive Modular Seating Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Automotive Modular Seating Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Automotive Modular Seating Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Automotive Modular Seating Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Automotive Modular Seating Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Automotive Modular Seating Revenue billion Forecast, by Type 2020 & 2033

- Table 58: Global Automotive Modular Seating Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Automotive Modular Seating Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Automotive Modular Seating Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Automotive Modular Seating Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Automotive Modular Seating Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Automotive Modular Seating Revenue billion Forecast, by Type 2020 & 2033

- Table 76: Global Automotive Modular Seating Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Automotive Modular Seating Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Automotive Modular Seating Volume K Forecast, by Country 2020 & 2033

- Table 79: China Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Automotive Modular Seating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Automotive Modular Seating Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Modular Seating?

The projected CAGR is approximately 2.7%.

2. Which companies are prominent players in the Automotive Modular Seating?

Key companies in the market include Adient, Lear, Faurecia, Toyota Boshoku, Magna, TS TECH, Hyundai DYMOS, NHK Spring, Tachi-S.

3. What are the main segments of the Automotive Modular Seating?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 75.33 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Modular Seating," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Modular Seating report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Modular Seating?

To stay informed about further developments, trends, and reports in the Automotive Modular Seating, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence