Key Insights

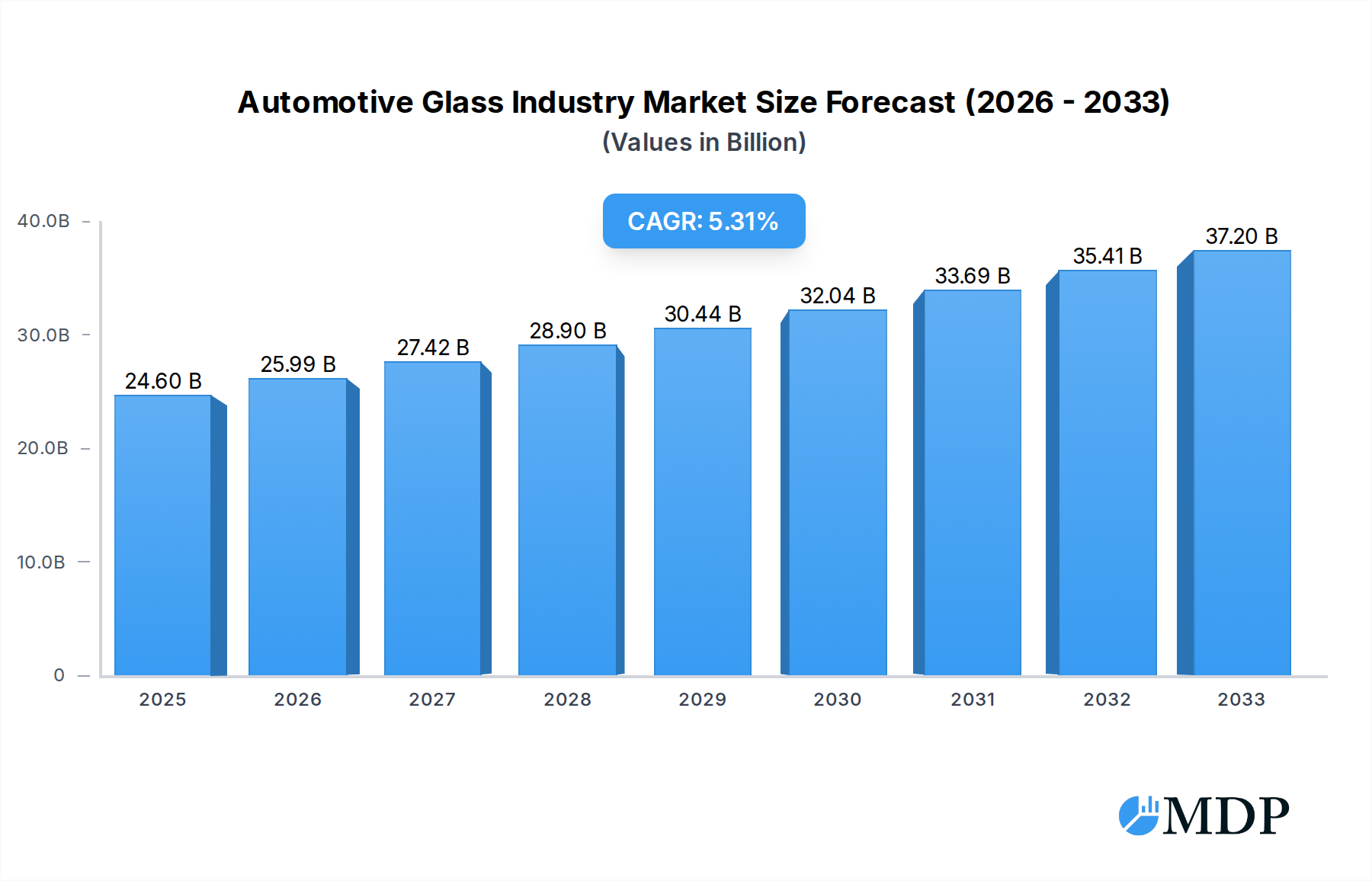

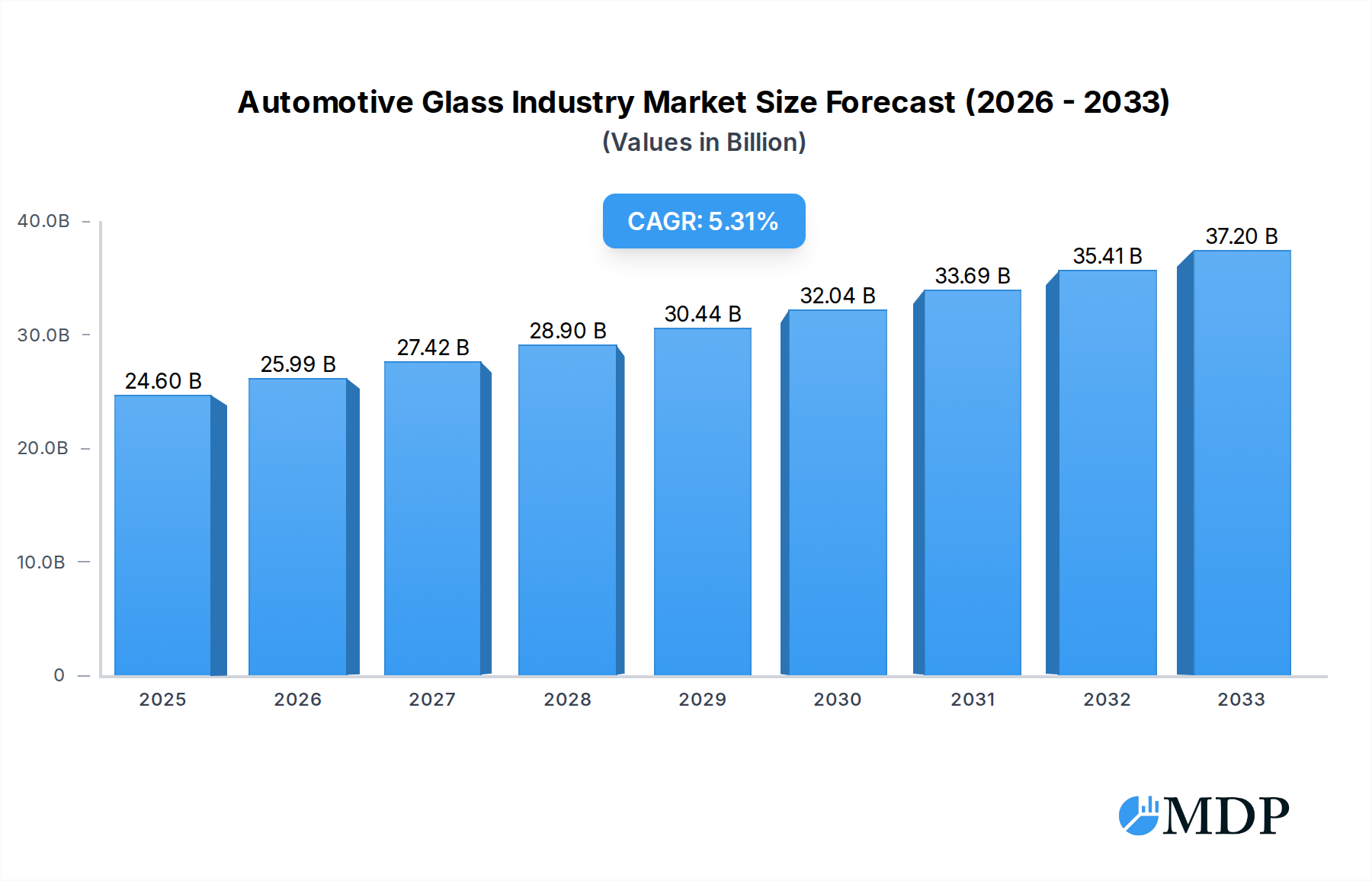

The global automotive glass market is poised for robust expansion, projected to reach a significant USD 24.6 billion in 2025. This growth is fueled by an anticipated Compound Annual Growth Rate (CAGR) of 5.63% throughout the forecast period of 2025-2033. A primary driver for this upward trajectory is the increasing global demand for vehicles, encompassing both passenger and commercial segments. Advancements in vehicle technology, such as the integration of smart glass functionalities, enhanced safety features like advanced driver-assistance systems (ADAS) requiring sophisticated sensor integration within glass, and a growing preference for premium features like panoramic sunroofs, are significantly contributing to market value. Furthermore, the burgeoning automotive industry in emerging economies, particularly in the Asia Pacific region, is creating substantial opportunities for glass manufacturers. The rising disposable incomes and expanding middle class in these regions are translating into higher vehicle sales, directly impacting the demand for automotive glass. The continuous innovation in glass manufacturing, leading to lighter, stronger, and more energy-efficient solutions, also plays a crucial role in driving market expansion.

Automotive Glass Industry Market Size (In Billion)

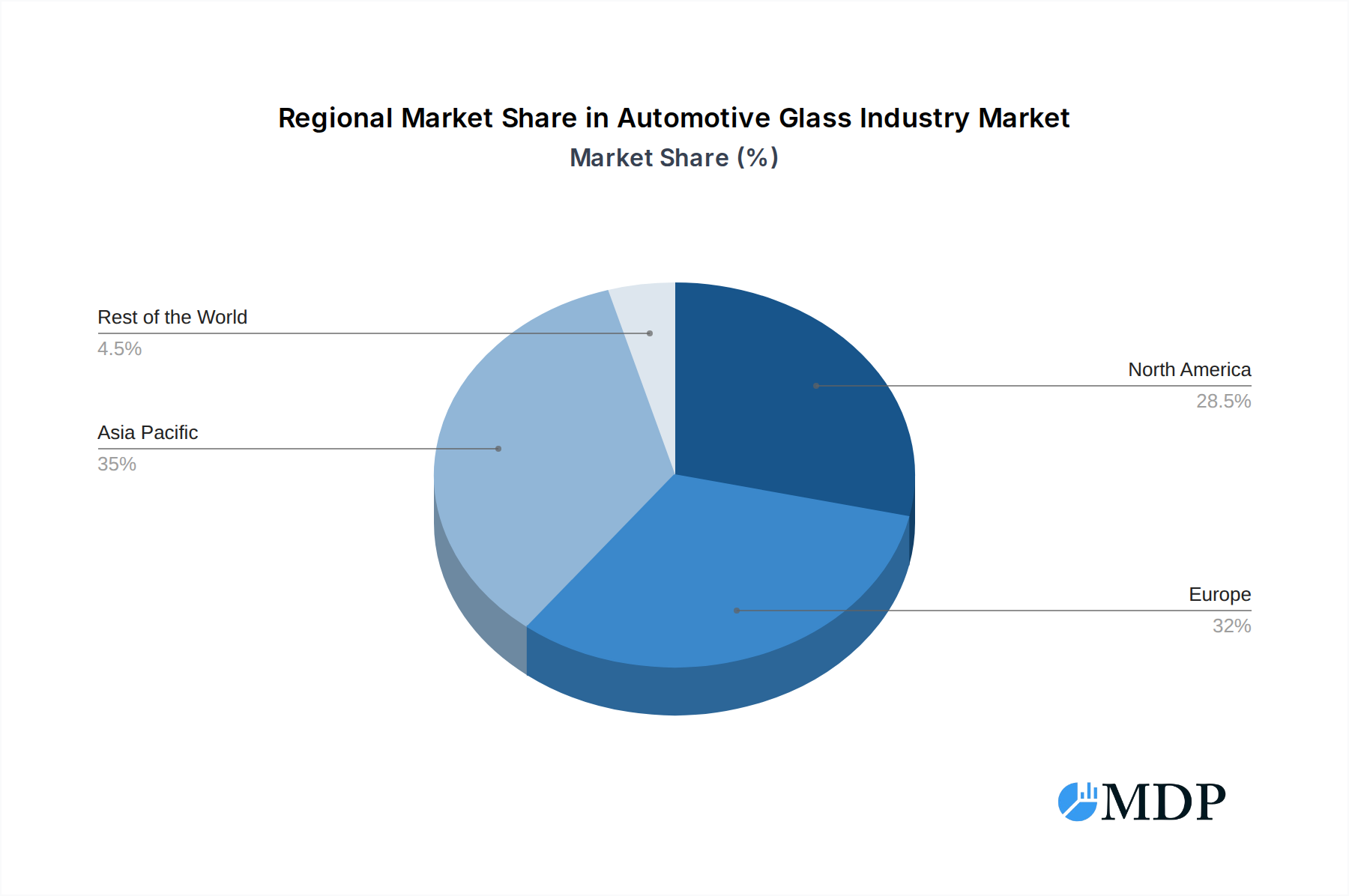

While the market exhibits strong growth, certain factors warrant attention. Stringent environmental regulations and the increasing focus on sustainable manufacturing processes necessitate investment in eco-friendly production techniques, which can represent an initial cost. Fluctuations in raw material prices, particularly for silica sand and other essential components, can also impact profit margins for manufacturers. However, the overarching trend of technological integration and the increasing complexity of automotive designs are expected to outweigh these challenges. The demand for specialized glass types, such as acoustic glass for noise reduction and heated glass for enhanced visibility in adverse weather conditions, is on the rise. The aftermarket segment, driven by repair and replacement needs, also contributes a steady stream of revenue. Geographically, the Asia Pacific region is expected to lead in terms of volume and growth, followed by North America and Europe, each presenting unique opportunities and challenges based on their respective market maturity and regulatory landscapes.

Automotive Glass Industry Company Market Share

This comprehensive report offers an in-depth analysis of the global automotive glass market, a critical and evolving sector projected to reach billions in value. Delving into intricate details from 2019 to 2033, with a base year of 2025, this report is an indispensable resource for automotive glass manufacturers, automotive OEMs, tier-1 suppliers, technology providers, and investment firms seeking to understand current dynamics, predict future trends, and capitalize on emerging opportunities within the automotive glazing industry. We meticulously examine market segmentation across regular glass and smart glass, windshields, rear-view mirrors, sunroofs, and other applications, catering to passenger vehicles and commercial vehicles.

Automotive Glass Industry Market Dynamics & Concentration

The automotive glass industry exhibits a moderately concentrated market, dominated by a handful of global players who command significant market share, estimated at over 70% collectively. Innovation is a key driver, fueled by advancements in materials science, safety regulations, and the increasing demand for smart glass technologies. Regulatory frameworks, particularly concerning vehicle safety and energy efficiency, continue to shape product development and adoption. Product substitutes, while limited in core functionality, are emerging in the form of advanced polymers and enhanced traditional glass solutions, pushing manufacturers to continually innovate. End-user trends are strongly influenced by the rise of autonomous driving, electric vehicles (EVs), and enhanced in-cabin experiences, necessitating integrated functionalities within automotive glass. Mergers and acquisitions (M&A) activities, with an estimated XX deal counts during the historical period, have been strategic, enabling companies to expand their technological capabilities, geographical reach, and product portfolios, consolidating market positions and further driving concentration.

Automotive Glass Industry Industry Trends & Analysis

The automotive glass market is experiencing robust growth, driven by escalating global vehicle production and an increasing demand for advanced automotive glazing. A significant CAGR of XX% is projected throughout the forecast period, indicating substantial market expansion. Technological disruptions are at the forefront, with the integration of smart glass solutions, including electrochromic, thermochromic, and augmented reality (AR) displays, revolutionizing the driver and passenger experience. Consumer preferences are shifting towards enhanced comfort, safety, and connectivity, with a growing emphasis on panoramic sunroofs, advanced head-up displays (HUDs) integrated into windshields, and acoustic glass for quieter cabin environments. The competitive landscape is characterized by intense rivalry among established players and the emergence of new entrants focused on niche technologies. Market penetration of advanced glass solutions is steadily increasing, particularly in premium and electric vehicle segments. The industry is witnessing a paradigm shift, moving beyond mere functional components to intelligent, interactive surfaces that contribute significantly to vehicle design, safety, and user experience. The ongoing evolution of ADAS (Advanced Driver-Assistance Systems) further necessitates sophisticated glass solutions capable of seamless sensor integration and optimal signal transmission.

Leading Markets & Segments in Automotive Glass Industry

The automotive glass industry is dominated by the windshield segment, which accounts for over XX% of the total market revenue due to its critical safety and visibility functions. Regular glass continues to hold a substantial market share, but the rapid innovation and adoption of smart glass technologies are driving significant growth in this niche, projected to achieve a XX% CAGR. Geographically, Asia Pacific is the leading region, driven by massive vehicle production in China and a burgeoning automotive market in India and Southeast Asia. Within this region, China stands out as a dominant country, contributing over XX% of the global market revenue.

- Dominant Segments:

- Type: Regular Glass (still dominant but Smart Glass gaining rapid traction)

- Application Type: Windshield (highest revenue contributor), Sunroof (growing popularity)

- Vehicle Type: Passenger Vehicles (largest market share)

- Key Drivers of Dominance:

- Economic Policies: Favorable government policies and incentives for automotive manufacturing in Asia Pacific.

- Infrastructure: Rapid development of road networks and increasing vehicle ownership in emerging economies.

- Consumer Demand: Growing middle class and rising disposable incomes leading to increased vehicle sales.

- Technological Adoption: Early and rapid adoption of advanced automotive technologies, including EVs and connected cars, in the Asia Pacific region.

Automotive Glass Industry Product Developments

Product innovation in the automotive glass sector is primarily focused on enhancing safety, comfort, and functionality. The development of ultra-durable Gorilla Glass windshields, as exemplified by Jeep's application for its Wrangler and Gladiator models, offers superior resistance to impacts and scratches. Smart glass technologies are evolving rapidly, with applications like dynamic AR windshield displays providing drivers with crucial information without distraction, and intelligent glass control systems that automatically adjust tint to optimize cabin temperature and light exposure. These advancements offer significant competitive advantages by improving vehicle aesthetics, reducing weight, and integrating advanced electronic features.

Key Drivers of Automotive Glass Industry Growth

The automotive glass industry is propelled by several key drivers. The increasing global vehicle production, especially in emerging economies, is a fundamental growth catalyst. Advancements in smart glass technology, offering enhanced safety, comfort, and connectivity features such as AR displays and intelligent tinting, are significant drivers. Stricter automotive safety regulations worldwide, mandating stronger and more robust glass components, also contribute to market expansion. Furthermore, the burgeoning electric vehicle (EV) market, which often incorporates larger glass areas and innovative designs, presents substantial growth opportunities.

Challenges in the Automotive Glass Industry Market

Despite its growth, the automotive glass market faces several challenges. Fluctuations in raw material prices, particularly for silica and other key components, can impact profitability. Stringent environmental regulations regarding manufacturing processes and emissions can increase operational costs. The high capital investment required for advanced manufacturing facilities and R&D for smart glass technologies poses a barrier to entry for smaller players. Intense competition among established manufacturers and the threat of new disruptive technologies also present ongoing challenges, potentially leading to price erosion.

Emerging Opportunities in Automotive Glass Industry

Emerging opportunities in the automotive glass industry are abundant. The rapid growth of the autonomous vehicle sector presents a significant avenue for innovation, requiring advanced sensor integration and specialized glass formulations. The increasing demand for in-cabin connectivity and personalized experiences opens doors for smart glass applications that can display information, control lighting, and enhance entertainment. The expansion of the EV market, with its unique design considerations and potential for lighter, more integrated glass solutions, offers substantial growth potential. Furthermore, strategic partnerships between glass manufacturers and technology companies are crucial for co-developing next-generation automotive glazing.

Leading Players in the Automotive Glass Industry Sector

- Asahi Glass Co

- Webasto

- Guardian Automotive

- Fuyao Group

- Benson Auto Glass

- Carlex Glass

- Saint Gobain

- Magna International

- Nippon Sheet Glass

- Xinyi Glass

Key Milestones in Automotive Glass Industry Industry

- July 2021: Jeep's Performance Parts division (JPP) introduced Gorilla Glass windshields for its Wrangler SUV and Gladiator pick-up truck models, enhancing durability with an ultra-thin inner ply and a 52% thicker outer ply.

- June 2021: Webasto supplied the sliding panorama sunroof for the new Mercedes-Benz S-Class, providing a bright interior ambiance with separately controllable roller blinds operated via gesture and voice control.

- March 2021: Audi announced that its all-electric Q4 e-tron crossover would feature a dynamic AR windshield display offering a wider field of view and more accurate animations compared to standard HUDs.

- February 2020: AGC Glass Europe collaborated with Citrine Informatics to develop new glass technology using artificial intelligence, targeting high-performance glass materials.

- January 2020: BMW introduced intelligent glass control in its iNext electric SUV at CES 2020, allowing for manual and automatic tint adjustment to manage heat and light.

Strategic Outlook for Automotive Glass Industry Market

The strategic outlook for the automotive glass industry is exceptionally positive, driven by the transformative trends in mobility. The continued push towards electrification and autonomous driving will necessitate increasingly sophisticated automotive glazing solutions, from lightweight, integrated structural glass to advanced AR-enabled windshields. Companies that invest in R&D for smart glass technologies, focus on sustainable manufacturing practices, and forge strategic alliances with EV manufacturers and tech innovators will be best positioned for long-term success. The expansion into emerging markets and the development of customized solutions for specific vehicle segments will also be critical growth accelerators.

Automotive Glass Industry Segmentation

-

1. Type

- 1.1. Regular Glass

- 1.2. Smart Glass

-

2. Application Type

- 2.1. Windshield

- 2.2. Rear View Mirrors

- 2.3. Sunroof

- 2.4. Other Application Types

-

3. Vehicle Type

- 3.1. Passenger Vehicles

- 3.2. Commercial Vehicles

Automotive Glass Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Spain

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Automotive Glass Industry Regional Market Share

Geographic Coverage of Automotive Glass Industry

Automotive Glass Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Regular Glass

- 5.1.2. Smart Glass

- 5.2. Market Analysis, Insights and Forecast - by Application Type

- 5.2.1. Windshield

- 5.2.2. Rear View Mirrors

- 5.2.3. Sunroof

- 5.2.4. Other Application Types

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Passenger Vehicles

- 5.3.2. Commercial Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Automotive Glass Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Regular Glass

- 6.1.2. Smart Glass

- 6.2. Market Analysis, Insights and Forecast - by Application Type

- 6.2.1. Windshield

- 6.2.2. Rear View Mirrors

- 6.2.3. Sunroof

- 6.2.4. Other Application Types

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.3.1. Passenger Vehicles

- 6.3.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Automotive Glass Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Regular Glass

- 7.1.2. Smart Glass

- 7.2. Market Analysis, Insights and Forecast - by Application Type

- 7.2.1. Windshield

- 7.2.2. Rear View Mirrors

- 7.2.3. Sunroof

- 7.2.4. Other Application Types

- 7.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.3.1. Passenger Vehicles

- 7.3.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Automotive Glass Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Regular Glass

- 8.1.2. Smart Glass

- 8.2. Market Analysis, Insights and Forecast - by Application Type

- 8.2.1. Windshield

- 8.2.2. Rear View Mirrors

- 8.2.3. Sunroof

- 8.2.4. Other Application Types

- 8.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.3.1. Passenger Vehicles

- 8.3.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Automotive Glass Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Regular Glass

- 9.1.2. Smart Glass

- 9.2. Market Analysis, Insights and Forecast - by Application Type

- 9.2.1. Windshield

- 9.2.2. Rear View Mirrors

- 9.2.3. Sunroof

- 9.2.4. Other Application Types

- 9.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.3.1. Passenger Vehicles

- 9.3.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of the World Automotive Glass Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Regular Glass

- 10.1.2. Smart Glass

- 10.2. Market Analysis, Insights and Forecast - by Application Type

- 10.2.1. Windshield

- 10.2.2. Rear View Mirrors

- 10.2.3. Sunroof

- 10.2.4. Other Application Types

- 10.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.3.1. Passenger Vehicles

- 10.3.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Asahi Glass Co

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Webasto

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Guardian Automotive

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Fuyao Group

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Benson Auto Glass

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Carlex Glass

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Saint Gobain

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Magna Internationa

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Nippon Sheet Glass

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Xinyi Glass

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Asahi Glass Co

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Glass Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Automotive Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Automotive Glass Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 5: North America Automotive Glass Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 6: North America Automotive Glass Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 7: North America Automotive Glass Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: North America Automotive Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Automotive Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Automotive Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: Europe Automotive Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Automotive Glass Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 13: Europe Automotive Glass Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 14: Europe Automotive Glass Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 15: Europe Automotive Glass Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 16: Europe Automotive Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Automotive Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Automotive Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 19: Asia Pacific Automotive Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Automotive Glass Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 21: Asia Pacific Automotive Glass Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 22: Asia Pacific Automotive Glass Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 23: Asia Pacific Automotive Glass Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Asia Pacific Automotive Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Automotive Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Automotive Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Rest of the World Automotive Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Rest of the World Automotive Glass Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 29: Rest of the World Automotive Glass Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 30: Rest of the World Automotive Glass Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 31: Rest of the World Automotive Glass Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 32: Rest of the World Automotive Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Rest of the World Automotive Glass Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Automotive Glass Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 3: Global Automotive Glass Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global Automotive Glass Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Automotive Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Glass Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 7: Global Automotive Glass Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 8: Global Automotive Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Automotive Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global Automotive Glass Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 14: Global Automotive Glass Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 15: Global Automotive Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: United Kingdom Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Germany Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Global Automotive Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Automotive Glass Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 23: Global Automotive Glass Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 24: Global Automotive Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: China Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: India Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Rest of Asia Pacific Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Glass Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 31: Global Automotive Glass Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 32: Global Automotive Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 33: South America Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Middle East and Africa Automotive Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Glass Industry?

The projected CAGR is approximately 5.63%.

2. Which companies are prominent players in the Automotive Glass Industry?

Key companies in the market include Asahi Glass Co, Webasto, Guardian Automotive, Fuyao Group, Benson Auto Glass, Carlex Glass, Saint Gobain, Magna Internationa, Nippon Sheet Glass, Xinyi Glass.

3. What are the main segments of the Automotive Glass Industry?

The market segments include Type, Application Type, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 24.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Fuel Economy Norms and Government Incentives.

6. What are the notable trends driving market growth?

Increasing Application of Smart Glass in Automobiles.

7. Are there any restraints impacting market growth?

Growing Demand For Battery Electric Vehicles.

8. Can you provide examples of recent developments in the market?

In July 2021, Jeep's Performance Parts division (JPP) has introduced Gorilla Glass windshields for its Wrangler SUV and Gladiator pick-up truck models. JPP's new windshield is made with Corning Gorilla Glass. Its durability is ensured by Mopar's combination of an ultra-thin Gorilla Glass inner ply with a 52 percent thicker outer ply. Both the Jeep Wrangler and Gladiator have an upright windshield, which reduces the panel's ability to deflect a strike from a rock.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Glass Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Glass Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Glass Industry?

To stay informed about further developments, trends, and reports in the Automotive Glass Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence