Key Insights

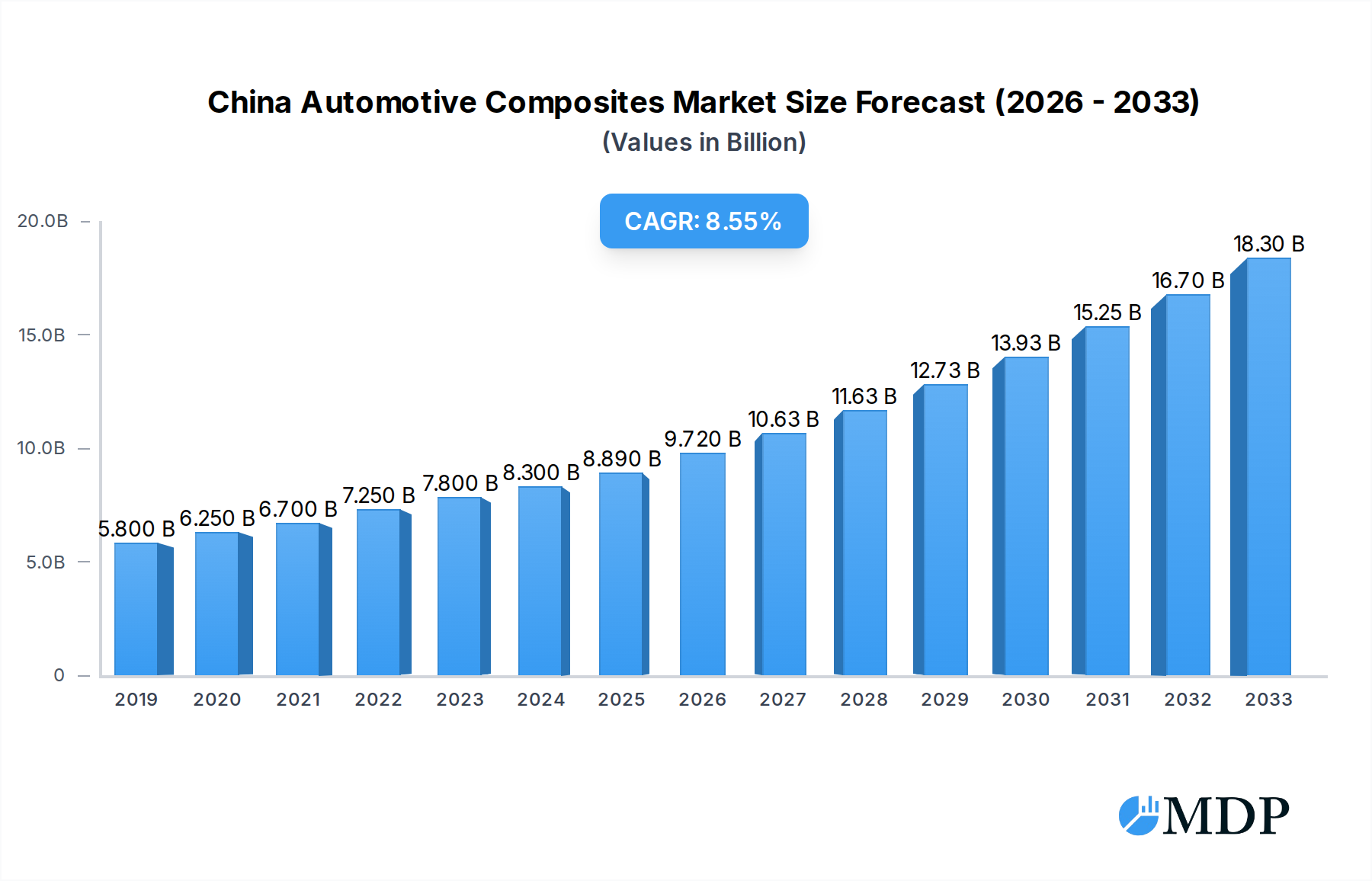

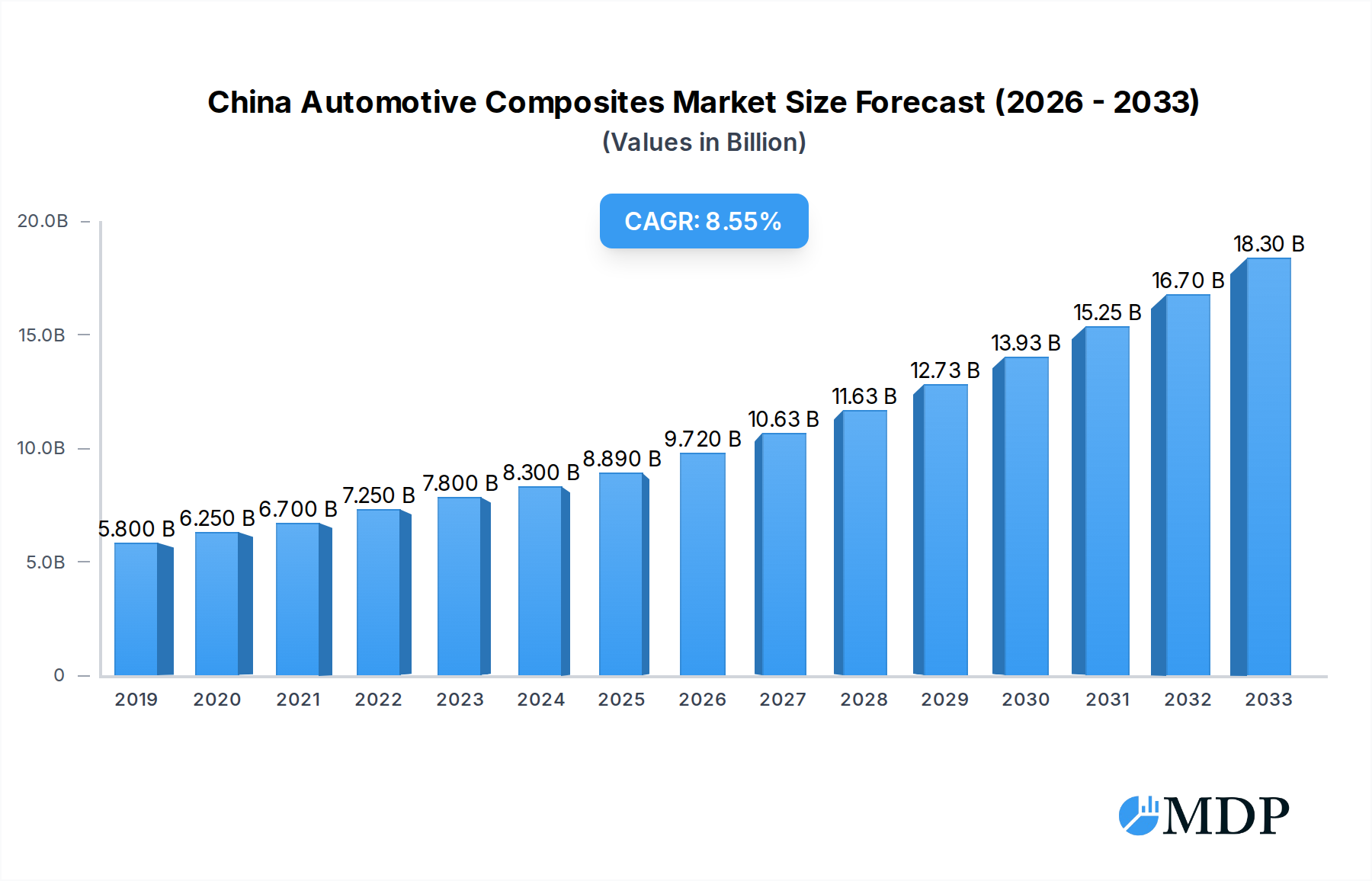

The China Automotive Composites Market is poised for substantial expansion, projected to reach a market size of 8890 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 9.50% anticipated through 2033. This robust growth is primarily propelled by the relentless pursuit of lightweighting in vehicles to enhance fuel efficiency and reduce emissions. The burgeoning demand for electric and hybrid vehicles, supported by government initiatives and increasing consumer environmental awareness, is a significant catalyst. These new energy vehicles (NEVs) heavily rely on advanced composite materials for structural components, battery enclosures, and interior parts to offset battery weight and improve overall performance. The adoption of advanced manufacturing processes like Resin Transfer Molding (RTM) and Vacuum Infusion Processing is also on the rise, enabling the production of complex and high-performance composite parts efficiently and cost-effectively.

China Automotive Composites Market Market Size (In Billion)

The market's dynamism is further shaped by evolving consumer preferences towards more sustainable and aesthetically pleasing vehicle designs, driving innovation in interior and exterior composite applications. While the market benefits from strong governmental support for NEVs and advanced manufacturing, it faces challenges such as the higher initial cost of composite materials compared to traditional metals and the need for specialized infrastructure and skilled labor for their manufacturing and repair. However, continuous advancements in material science, particularly in the development of more cost-effective and recyclable composite solutions, alongside the increasing economies of scale, are expected to mitigate these restraints. Key players like Teijin Limited, Mitsubishi Chemical Corporation, and Toray Industries Inc. are at the forefront, investing in research and development to introduce novel composite solutions tailored for the unique demands of the Chinese automotive sector. The extensive segmentation across vehicle types, propulsion systems, and material types underscores the broad applicability and evolving landscape of automotive composites in China.

China Automotive Composites Market Company Market Share

Unveiling the China Automotive Composites Market: A Comprehensive Analysis (2019–2033)

Dive deep into the rapidly evolving China Automotive Composites Market with this in-depth report. Covering the historical period (2019–2024), base year (2025), and an extensive forecast period (2025–2033), this study provides unparalleled insights into market dynamics, growth drivers, and future opportunities. Discover how advancements in lightweight materials, driven by battery electric vehicles (BEVs) and stringent emission regulations, are reshaping the automotive landscape. Explore the dominance of passenger cars, the growing adoption of thermoplastic polymers and carbon fiber, and the pivotal role of structural assembly applications. This report is essential for automotive OEMs, Tier 1 suppliers, material manufacturers, and investors seeking to capitalize on the burgeoning China automotive lightweight materials market and automotive advanced materials sector.

China Automotive Composites Market Market Dynamics & Concentration

The China automotive composites market is characterized by moderate to high concentration, with a significant presence of global giants and emerging domestic players vying for market share. Innovation drivers are primarily fueled by the automotive industry's relentless pursuit of lightweighting, enhanced fuel efficiency, and improved safety standards, particularly with the surge in electric vehicle (EV) adoption. Regulatory frameworks, including China's dual-credit policy and stricter emission standards, continue to mandate the use of advanced materials, pushing composites into mainstream applications. Product substitutes, such as advanced high-strength steels (AHSS) and aluminum alloys, present ongoing competition, though composites offer distinct advantages in weight reduction and design flexibility. End-user trends are heavily influenced by consumer demand for more sustainable and performance-driven vehicles, leading to increased acceptance of composite components. Merger and acquisition (M&A) activities are anticipated to increase as companies seek to consolidate market positions, acquire new technologies, and expand their geographical reach within the vast Chinese market. While specific M&A deal counts are still evolving, strategic partnerships and collaborations are prevalent, indicating a dynamic and competitive landscape.

- Market Concentration: Moderate to high, with key global players and growing domestic influence.

- Innovation Drivers: Lightweighting, fuel efficiency, EV adoption, safety enhancements, sustainability.

- Regulatory Frameworks: China's dual-credit policy, emission standards, government incentives for EVs.

- Product Substitutes: Advanced High-Strength Steels (AHSS), Aluminum Alloys.

- End-User Trends: Demand for sustainable, high-performance, and feature-rich vehicles.

- M&A Activities: Expected to rise, driven by consolidation and technological acquisition.

China Automotive Composites Market Industry Trends & Analysis

The China automotive composites market is experiencing robust growth, propelled by a confluence of powerful industry trends. The escalating demand for lightweight materials, driven by the imperative to enhance fuel efficiency in internal combustion engine (ICE) vehicles and significantly extend the range of battery electric vehicles (BEVs), is a primary growth engine. The rapid expansion of the EV sector in China, supported by substantial government subsidies and a burgeoning charging infrastructure, is directly translating into increased demand for composite materials in critical components such as battery enclosures, body panels, and structural elements. Technological disruptions are playing a crucial role, with advancements in resin transfer molding (RTM), injection molding, and compression molding processes enabling higher production volumes and reduced manufacturing costs. The development of novel composite materials, including advanced thermoplastic polymers and high-performance carbon fiber grades, is further expanding the application scope of composites beyond traditional uses. Consumer preferences are increasingly leaning towards vehicles that offer superior performance, reduced environmental impact, and innovative designs, all of which can be facilitated by the use of automotive composites. This evolving consumer mindset, coupled with the stringent emission regulations, is compelling automakers to invest heavily in composite technologies. The competitive dynamics within the market are intensifying, with both established international players and increasingly capable domestic manufacturers competing on price, performance, and innovation. The CAGR (Compound Annual Growth Rate) for the China automotive composites market is projected to be robust, driven by these multifaceted trends. Market penetration of composites in various vehicle segments, especially in premium and new energy vehicles, is steadily increasing, indicating a significant shift from traditional materials.

Leading Markets & Segments in China Automotive Composites Market

The China Automotive Composites Market is segmented across various vehicle types, propulsion systems, process types, material types, and applications, each exhibiting distinct growth patterns and dominance.

Vehicle Type:

- Passenger Cars represent the dominant segment, driven by the sheer volume of sales in China and the increasing adoption of lightweight composites for improved fuel economy and performance. The growing middle class and demand for aesthetically pleasing and technologically advanced vehicles further solidify this segment's leadership.

- Commercial Vehicles are also emerging as a significant growth area, particularly for lightweighting heavy-duty trucks to improve fuel efficiency and payload capacity, thereby reducing operational costs.

Propulsion:

- Battery Electric Vehicles (BEVs) are the fastest-growing propulsion segment for automotive composites. The critical need for weight reduction to maximize battery range and the integration of large battery packs necessitate the use of advanced composites in battery enclosures, structural components, and body-in-white.

- Internal Combustion Engine (ICE) vehicles continue to be a substantial market, with composites being employed for weight reduction to meet emission norms and improve fuel efficiency.

- Hybrid Electric Vehicles (HEVs) and Plug-in Hybrid Electric Vehicles (PHEVs) represent a transitional market, also benefiting from the lightweighting advantages of composites.

Process Type:

- Resin Transfer Molding (RTM) and Vacuum Infusion Processing (VIP) are gaining traction for producing complex, high-performance composite parts with precise fiber placement and excellent surface finish, crucial for structural components and demanding applications.

- Injection Molding is increasingly being adopted for thermoplastic composites, offering high-volume production capabilities and cost-effectiveness for interior and exterior components.

- Compression Molding remains a significant process, especially for thermoset composites used in larger structural parts.

Material Type:

- Carbon Fiber composites are experiencing rapid growth due to their exceptional strength-to-weight ratio, crucial for high-performance and premium EV applications, particularly in structural assembly and body panels.

- Glass Fiber composites continue to be a workhorse, offering a balance of performance and cost-effectiveness for a wide range of applications, including interior components, exterior panels, and some structural parts.

- Thermoplastic Polymers are gaining significant market share due to their recyclability, faster processing times, and ability to be welded, making them ideal for high-volume production of various automotive components.

- Thermoset Polymers remain important for applications requiring high thermal stability and mechanical strength.

Application:

- Structural Assembly is a key application area, where composites are replacing traditional metal components in chassis, body structures, and crash management systems to achieve significant weight savings and enhance vehicle safety.

- Exterior applications, including body panels, hoods, and liftgates, are witnessing increasing adoption of composites for both weight reduction and design freedom.

- Interior applications, such as dashboards, door panels, and consoles, are benefiting from composites for their aesthetic versatility and lightweight properties.

- Power train Component applications are emerging, especially in EVs, for battery housings and other components where thermal management and weight are critical.

China Automotive Composites Market Product Developments

Recent product developments are significantly shaping the China automotive composites market. In October 2023, Toray Industries, Inc. unveiled TORAYCA T1200 carbon fiber, boasting an unprecedented strength of 1,160 kilopounds per square inch (Ksi). This breakthrough material offers substantial weight reduction potential, directly contributing to reduced environmental footprints through the use of lighter carbon-fiber-reinforced plastic (CFRP) materials, making it ideal for performance-oriented vehicles and demanding structural applications. Concurrently, in October 2023, Mitsubishi Chemical Group and Honda Motor Company collaborated to develop a novel polymethyl methacrylate (acrylic resin) material specifically for automotive body parts. This innovative acrylic resin is slated for use in vehicle doors, hoods, fenders, and other body components, offering a lightweight and potentially cost-effective alternative to traditional materials, enhancing design flexibility and contributing to overall vehicle efficiency. These advancements highlight a strong industry focus on material innovation to meet the evolving demands for lightweighting, sustainability, and performance in the automotive sector.

Key Drivers of China Automotive Composites Market Growth

The China automotive composites market is propelled by several key drivers. Foremost is the stringent governmental push towards reducing vehicle emissions and improving fuel efficiency, directly incentivizing the adoption of lightweight materials like composites. The rapid expansion of the electric vehicle (EV) market in China, supported by substantial government policies and consumer interest, creates a massive demand for lightweighting solutions to enhance battery range and performance. Technological advancements in composite manufacturing processes, such as RTM and injection molding, are making these materials more cost-effective and suitable for mass production. Furthermore, the inherent advantages of composites, including their high strength-to-weight ratio, corrosion resistance, and design flexibility, are increasingly recognized and valued by automotive manufacturers.

- Stringent Emission Regulations & Fuel Efficiency Mandates: Driving the need for lightweight materials.

- Rapid Growth of the Electric Vehicle (EV) Market: Requiring significant weight reduction for battery range.

- Advancements in Composite Manufacturing Technologies: Enhancing cost-effectiveness and scalability.

- Superior Material Properties: High strength-to-weight ratio, corrosion resistance, and design flexibility.

Challenges in the China Automotive Composites Market Market

Despite its robust growth, the China automotive composites market faces several challenges. The high initial cost of raw materials, particularly carbon fiber, and the specialized manufacturing equipment required can be a significant barrier to widespread adoption, especially for cost-sensitive vehicle segments. Furthermore, the complexity and cost associated with repairing composite structures compared to traditional metal parts can deter some consumers and repair shops. Recycling and end-of-life management of composite materials present ongoing environmental and logistical challenges, requiring further development of efficient recycling technologies. Supply chain volatility for raw materials and the need for specialized workforce training also pose hurdles to seamless market expansion.

- High Material and Equipment Costs: Especially for advanced composites like carbon fiber.

- Repair and Maintenance Complexity: Compared to traditional metallic components.

- Recycling and End-of-Life Management: Requiring innovative solutions.

- Supply Chain Volatility and Skilled Workforce Shortage: Hindering large-scale adoption.

Emerging Opportunities in China Automotive Composites Market

Emerging opportunities in the China automotive composites market are substantial and diverse. The continued growth of the New Energy Vehicle (NEV) segment, including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs), will drive demand for lightweight structural components and battery enclosures. Advancements in thermoplastic composites offer significant potential for high-volume production of interior and exterior parts, enabling greater design freedom and cost efficiencies. The development of bio-based and recycled composite materials presents a significant opportunity to address sustainability concerns and meet growing consumer demand for eco-friendly vehicles. Strategic partnerships between material manufacturers, automotive OEMs, and research institutions are crucial for accelerating innovation, developing new applications, and overcoming existing manufacturing and recycling challenges. Furthermore, the growing demand for enhanced vehicle performance and safety in the competitive Chinese market will continue to spur the adoption of advanced composite solutions.

Leading Players in the China Automotive Composites Market Sector

- Teijin Limited

- Mitsubishi Chemical Corporation

- Toray Industries Inc

- Jiuding New Material Co Ltd

- BASF SE

- ALPEX Technologies GmbH

- SGL Group SE

- Hexcel Corporation

- Nippon Sheet Glass Co Ltd

Key Milestones in China Automotive Composites Market Industry

- October 2023: Toray Industries, Inc. developed TORAYCA T1200 carbon fiber, boasting the highest strength of 1,160 kilopounds per square inch (Ksi). This advancement will aid in reducing environmental footprint by using lighter carbon-fiber-reinforced plastic materials.

- October 2023: Mitsubishi Chemical Group and Honda Motor Company jointly developed polymethyl methacrylate, also called acrylic resin material for automotive body parts. The new material will be used in vehicle doors, hoods, fenders, and other automotive body parts.

Strategic Outlook for China Automotive Composites Market Market

The strategic outlook for the China automotive composites market is exceptionally positive, driven by a sustained demand for lightweighting and performance enhancements. The accelerating shift towards electric mobility will continue to be a primary growth catalyst, necessitating the widespread adoption of advanced composite materials for battery systems, lightweight chassis, and body structures. Continued innovation in material science, particularly in the development of cost-effective and sustainable composites like advanced thermoplastic and bio-based materials, will unlock new application areas and broaden market penetration. Strategic collaborations between material suppliers and automotive manufacturers will be crucial for co-developing tailor-made solutions that address specific vehicle performance and manufacturing requirements. Furthermore, government support for advanced manufacturing and sustainable technologies will play a pivotal role in shaping the market's trajectory, fostering further investment and technological advancement. The market is poised for continued expansion, driven by a strong focus on efficiency, sustainability, and cutting-edge automotive design.

China Automotive Composites Market Segmentation

-

1. Vehicle Type

- 1.1. Passenger Car

- 1.2. Commercial Vehicles

-

2. Propulsion

- 2.1. Internal Combustion Engine

- 2.2. Battery Electric Vehicles

- 2.3. Hybrid Electric Vehicles

- 2.4. Plug-in Hybrid Electric Vehicles

- 2.5. Fuel Cell Electric Vehicles

-

3. Process Type

- 3.1. Hand Layup

- 3.2. Resin Transfer Molding

- 3.3. Vacuum Infusion Processing

- 3.4. Injection Molding

- 3.5. Compression Molding

-

4. Material Type

- 4.1. Thermoset Polymer

- 4.2. Thermoplastic Polymer

- 4.3. Carbon Fiber

- 4.4. Glass Fiber

- 4.5. Others

-

5. Application

- 5.1. Structural Assembly

- 5.2. Power train Component

- 5.3. Interior

- 5.4. Exterior

- 5.5. Others

China Automotive Composites Market Segmentation By Geography

- 1. China

China Automotive Composites Market Regional Market Share

Geographic Coverage of China Automotive Composites Market

China Automotive Composites Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Propulsion

- 5.2.1. Internal Combustion Engine

- 5.2.2. Battery Electric Vehicles

- 5.2.3. Hybrid Electric Vehicles

- 5.2.4. Plug-in Hybrid Electric Vehicles

- 5.2.5. Fuel Cell Electric Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Process Type

- 5.3.1. Hand Layup

- 5.3.2. Resin Transfer Molding

- 5.3.3. Vacuum Infusion Processing

- 5.3.4. Injection Molding

- 5.3.5. Compression Molding

- 5.4. Market Analysis, Insights and Forecast - by Material Type

- 5.4.1. Thermoset Polymer

- 5.4.2. Thermoplastic Polymer

- 5.4.3. Carbon Fiber

- 5.4.4. Glass Fiber

- 5.4.5. Others

- 5.5. Market Analysis, Insights and Forecast - by Application

- 5.5.1. Structural Assembly

- 5.5.2. Power train Component

- 5.5.3. Interior

- 5.5.4. Exterior

- 5.5.5. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. China

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. China Automotive Composites Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Propulsion

- 6.2.1. Internal Combustion Engine

- 6.2.2. Battery Electric Vehicles

- 6.2.3. Hybrid Electric Vehicles

- 6.2.4. Plug-in Hybrid Electric Vehicles

- 6.2.5. Fuel Cell Electric Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Process Type

- 6.3.1. Hand Layup

- 6.3.2. Resin Transfer Molding

- 6.3.3. Vacuum Infusion Processing

- 6.3.4. Injection Molding

- 6.3.5. Compression Molding

- 6.4. Market Analysis, Insights and Forecast - by Material Type

- 6.4.1. Thermoset Polymer

- 6.4.2. Thermoplastic Polymer

- 6.4.3. Carbon Fiber

- 6.4.4. Glass Fiber

- 6.4.5. Others

- 6.5. Market Analysis, Insights and Forecast - by Application

- 6.5.1. Structural Assembly

- 6.5.2. Power train Component

- 6.5.3. Interior

- 6.5.4. Exterior

- 6.5.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Teijin Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mitsubishi Chemical Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toray Industries Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Jiuding New Material Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BASF SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 ALPEX Technologies Gmb

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 SGL Group SE

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Hexcel Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Nipposn Sheet Glass Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Teijin Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Automotive Composites Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Automotive Composites Market Share (%) by Company 2025

List of Tables

- Table 1: China Automotive Composites Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: China Automotive Composites Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 3: China Automotive Composites Market Revenue Million Forecast, by Process Type 2020 & 2033

- Table 4: China Automotive Composites Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 5: China Automotive Composites Market Revenue Million Forecast, by Application 2020 & 2033

- Table 6: China Automotive Composites Market Revenue Million Forecast, by Region 2020 & 2033

- Table 7: China Automotive Composites Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 8: China Automotive Composites Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 9: China Automotive Composites Market Revenue Million Forecast, by Process Type 2020 & 2033

- Table 10: China Automotive Composites Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 11: China Automotive Composites Market Revenue Million Forecast, by Application 2020 & 2033

- Table 12: China Automotive Composites Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Automotive Composites Market?

The projected CAGR is approximately 9.50%.

2. Which companies are prominent players in the China Automotive Composites Market?

Key companies in the market include Teijin Limited, Mitsubishi Chemical Corporation, Toray Industries Inc, Jiuding New Material Co Ltd, BASF SE, ALPEX Technologies Gmb, SGL Group SE, Hexcel Corporation, Nipposn Sheet Glass Co Ltd.

3. What are the main segments of the China Automotive Composites Market?

The market segments include Vehicle Type, Propulsion, Process Type, Material Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.89 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Lightweight Materials.

6. What are the notable trends driving market growth?

Passenger Car Hold Major Growth.

7. Are there any restraints impacting market growth?

High Expenses of Composite Processing and Manufacturing.

8. Can you provide examples of recent developments in the market?

In October 2023, Toray Industries, Inc. developed TORAYCA T1200 carbon fiber, which boasts the highest strength of 1,160 kilopounds per square inch (Ksi). This advancement will aid us in reducing our environmental footprint by using lighter carbon-fiber-reinforced plastic materials.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Automotive Composites Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Automotive Composites Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Automotive Composites Market?

To stay informed about further developments, trends, and reports in the China Automotive Composites Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence