Key Insights

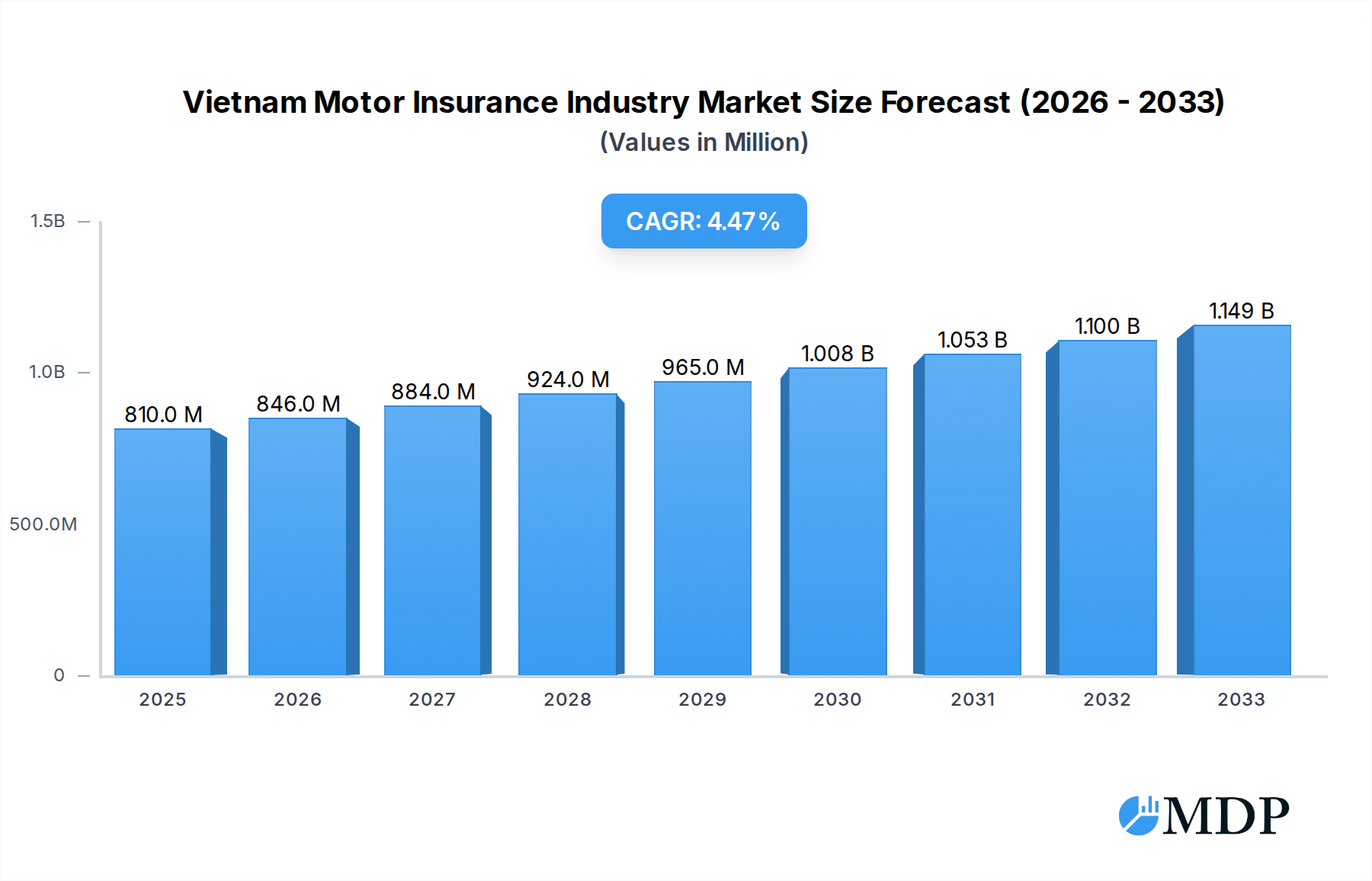

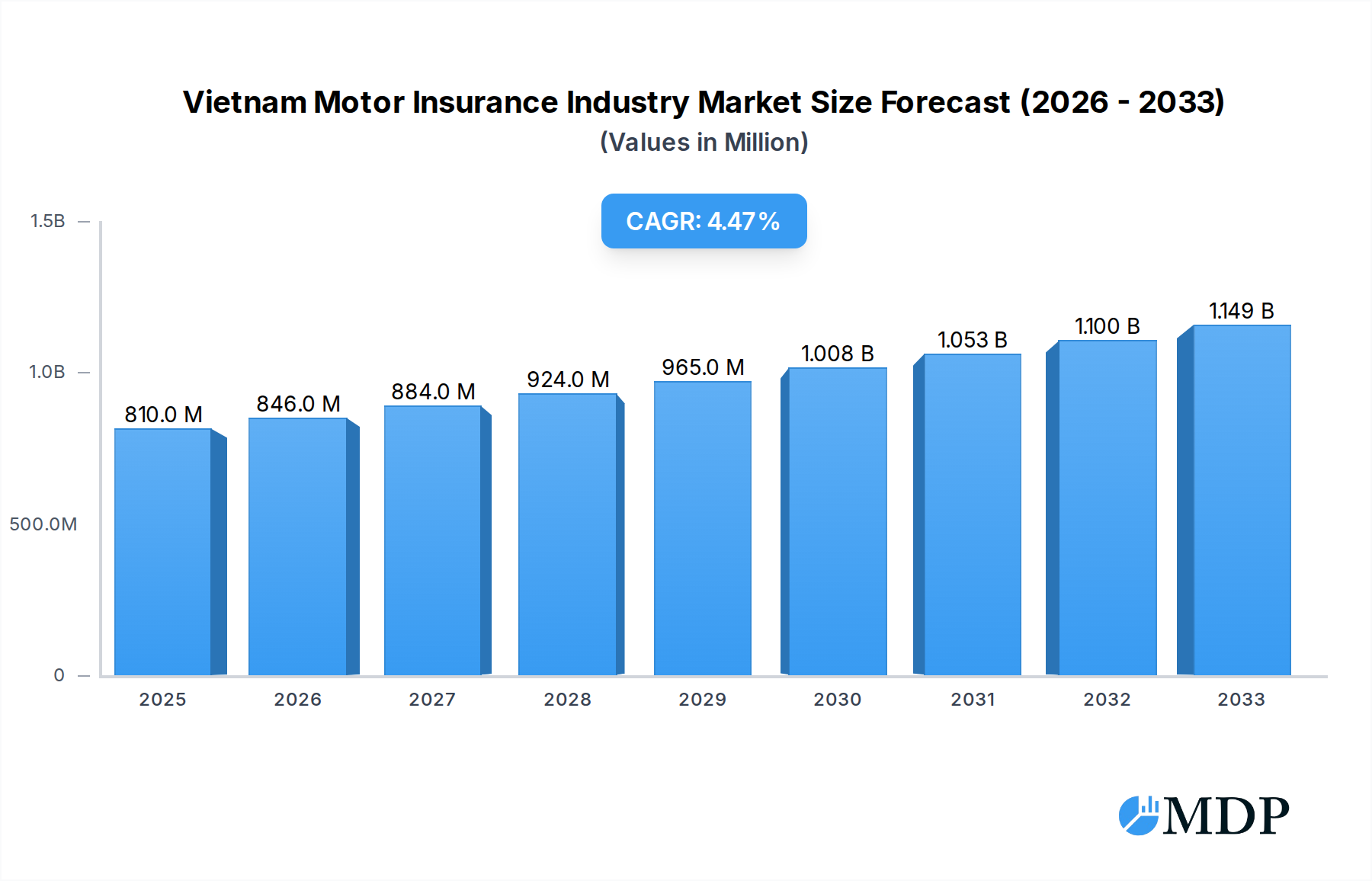

The Vietnam Motor Insurance Industry is poised for robust expansion, with an estimated market size of $810 million in 2025. This growth is driven by a projected Compound Annual Growth Rate (CAGR) of 4.50% over the forecast period of 2025-2033, indicating a steadily increasing demand for motor insurance solutions in the country. The industry is broadly segmented by policy type, encompassing both Compulsory Third-Party Liability (CTPL) insurance, which is mandated by law, and Comprehensive Insurance, offering broader coverage for vehicles. This segmentation caters to a diverse range of customer needs, from basic legal compliance to enhanced protection.

Vietnam Motor Insurance Industry Market Size (In Million)

Further driving this market's evolution is the segmentation by vehicle type, with Passenger Vehicles and Commercial Vehicles representing key segments. The increasing number of vehicles on Vietnamese roads, coupled with growing awareness of the financial implications of accidents, fuels the demand for insurance across both categories. Distribution channels are also diversifying, with Agents, Brokers, Banks, and Online platforms playing crucial roles in reaching consumers. The digital transformation trend is particularly evident in the growing adoption of online channels, offering convenience and accessibility. However, potential restraints such as increasing competition among insurers and evolving regulatory frameworks could influence the market's trajectory. Key players like Bao Viet Holdings, PetroVietnam Insurance (PVI), and Bao Minh Insurance Corporation are actively shaping the competitive landscape.

Vietnam Motor Insurance Industry Company Market Share

Gain a comprehensive understanding of the dynamic Vietnam Motor Insurance Industry with this in-depth report. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this analysis provides critical insights into market concentration, emerging trends, leading segments, and future growth opportunities. Uncover the strategies of key players, navigate regulatory landscapes, and capitalize on innovation drivers for significant market penetration. This report is essential for insurers, reinsurers, brokers, automotive manufacturers, and financial institutions seeking to strategize and thrive in Vietnam's rapidly evolving automotive insurance sector.

Vietnam Motor Insurance Industry Market Dynamics & Concentration

The Vietnam Motor Insurance Industry is characterized by a moderate level of market concentration, with a few dominant players like Bao Viet Holdings and PetroVietnam Insurance (PVI) holding significant market share. Innovation drivers are primarily centered around digital transformation and enhanced customer experience, pushing companies to develop user-friendly online platforms and personalized policy offerings. The regulatory framework, though evolving, plays a crucial role in shaping market access and product development, particularly concerning mandatory third-party liability insurance. Product substitutes, while limited in the core insurance offerings, are emerging in the form of embedded insurance solutions integrated with vehicle purchases and after-sales services. End-user trends highlight a growing demand for comprehensive coverage and value-added services, driven by increasing vehicle ownership and a greater awareness of financial protection. Mergers and acquisitions (M&A) activities are anticipated to increase as larger, established insurers seek to consolidate their market position and acquire innovative technologies or niche customer bases. M&A deal counts are projected to see a gradual rise, with an estimated xx deals within the forecast period. The market share distribution indicates that leading companies hold approximately 60-70% of the total market.

Vietnam Motor Insurance Industry Industry Trends & Analysis

The Vietnam Motor Insurance Industry is poised for robust growth, fueled by a confluence of macroeconomic factors and evolving consumer behavior. The Compound Annual Growth Rate (CAGR) is projected to be a healthy xx% over the forecast period (2025–2033), driven by increasing vehicle ownership across passenger and commercial segments. Rising disposable incomes and a growing middle class are directly translating into higher demand for both compulsory third-party liability (CTPL) and comprehensive insurance policies. Technological disruptions are revolutionizing the industry, with a significant shift towards online distribution channels and the adoption of InsurTech solutions. This includes the use of telematics for usage-based insurance (UBI) and AI-powered claims processing, enhancing efficiency and customer satisfaction. Consumer preferences are increasingly leaning towards personalized insurance products, with a demand for flexible policy terms, add-on benefits, and seamless digital interactions. The competitive dynamics are intensifying, with both domestic and international players vying for market share. Established insurers are investing heavily in digital infrastructure and innovative product development to stay ahead, while new entrants are focusing on niche markets and disruptive technologies. Market penetration for motor insurance is expected to rise from an estimated xx% in the base year 2025 to xx% by 2033, reflecting the growing maturity of the market. The expansion of the road network and increased urbanization also contribute to a higher volume of vehicles, thus boosting the demand for motor insurance. Furthermore, government initiatives promoting financial literacy and insurance awareness are playing a vital role in encouraging greater adoption of motor insurance products. The impact of natural disasters and road safety concerns is also subtly driving the demand for comprehensive coverage, providing a sense of security to vehicle owners.

Leading Markets & Segments in Vietnam Motor Insurance Industry

Compulsory Third-Party Liability Insurance (CTPL): This segment continues to be a foundational pillar of the Vietnam Motor Insurance Industry, mandated by law. Its dominance is driven by the unwavering regulatory requirement for all vehicle owners to possess this coverage. Key drivers for its continued strength include consistent enforcement of traffic laws and the growing number of registered vehicles, both passenger and commercial. The economic policies encouraging vehicle ownership and the development of transportation infrastructure further bolster its position. While mandatory, CTPL is often bundled with other insurance offerings, contributing to the overall revenue stream.

Comprehensive Insurance: This segment is experiencing substantial growth, fueled by rising consumer affluence and a greater emphasis on protecting valuable assets. The key drivers for its expansion are the increasing average vehicle values, particularly for passenger vehicles, and a growing awareness of the financial implications of accidents, theft, and damage beyond third-party liability. Enhanced road infrastructure leading to increased vehicle usage, alongside the competitive push for innovative add-on features and bundled services, are also significant contributors.

Passenger Vehicles: This segment holds the largest market share within the vehicle types, propelled by strong economic growth, urbanization, and a burgeoning middle class. The increasing affordability of passenger cars, coupled with lifestyle aspirations, drives consistent demand for new and used vehicles, consequently boosting the need for associated motor insurance. Factors like expanded financing options for vehicle purchases and the development of better road networks further underpin the dominance of this segment.

Commercial Vehicles: While smaller than passenger vehicles, the commercial vehicle segment is a significant contributor, driven by the expansion of logistics, e-commerce, and the service industry. The growth of businesses requiring transportation of goods and services necessitates a robust fleet of commercial vehicles, thereby creating a consistent demand for specialized commercial motor insurance. Government support for trade and industry, alongside investments in infrastructure supporting commerce, are key drivers for this segment's sustained importance.

Distribution Channels:

- Agents: Historically a dominant channel, agents continue to play a crucial role, especially in less urbanized areas, providing personalized advice and facilitating complex claims. Their strength lies in building trust and offering tailored solutions.

- Brokers: The increasing complexity of insurance needs, particularly for commercial fleets and specialized vehicles, is leading to a growing reliance on insurance brokers who offer expertise in risk assessment and policy negotiation.

- Banks: Bancassurance partnerships are gaining traction, leveraging existing customer relationships to offer motor insurance as a value-added product during vehicle financing. This channel benefits from high trust and direct access to potential customers.

- Online: This channel is experiencing the most rapid growth. Digital platforms offer convenience, competitive pricing, and a seamless purchasing experience, appealing to younger, tech-savvy consumers. The ongoing digital transformation of the insurance sector is directly fueling the expansion of online distribution.

- Other Distribution Channels: This category includes direct sales by insurers and partnerships with automotive dealerships, both of which are crucial for reaching specific customer segments and facilitating point-of-sale insurance purchases.

Vietnam Motor Insurance Industry Product Developments

Product innovation in the Vietnam Motor Insurance Industry is increasingly driven by technological advancements and a focus on customer-centric solutions. Key developments include the introduction of usage-based insurance (UBI) leveraging telematics to offer personalized premiums based on driving behavior, and the integration of AI for faster and more efficient claims processing. Insurers are also expanding their offerings beyond traditional coverage, introducing value-added services such as roadside assistance, concierge services, and partnerships with repair networks to enhance customer experience and competitive advantage. The trend towards bundled policies, combining motor insurance with personal accident or travel insurance, is also gaining momentum, catering to the diverse needs of modern consumers and strengthening market fit.

Key Drivers of Vietnam Motor Insurance Industry Growth

The Vietnam Motor Insurance Industry's growth is propelled by several key factors. Economic Expansion leads to increased disposable incomes and a higher rate of vehicle ownership, directly boosting demand for motor insurance. Technological Advancements, particularly in InsurTech, are enabling more efficient operations, personalized products, and improved customer experiences, driving adoption. Favorable Regulatory Environment, such as Vietnam's participation in the ASEAN Compulsory Motor Insurance Scheme (ACMI), ensures a foundational market for third-party liability coverage. Furthermore, Growing Consumer Awareness regarding the importance of financial protection against unforeseen events and accidents plays a crucial role in increasing insurance penetration rates.

Challenges in the Vietnam Motor Insurance Industry Market

The Vietnam Motor Insurance Industry faces several significant challenges. Intense Competition from both domestic and international players can lead to price wars and pressure on profit margins, estimated to impact profitability by xx%. Regulatory Hurdles and evolving compliance requirements can increase operational costs and complexity. Fraudulent Claims remain a persistent issue, impacting the industry's financial stability and potentially leading to increased premiums for honest policyholders, with an estimated xx% of claims being fraudulent. Infrastructure Deficiencies, in some regions, can lead to higher accident rates, further straining insurer resources. Finally, Customer Education on the benefits of comprehensive insurance beyond mandatory coverage is an ongoing challenge, hindering market penetration for value-added products.

Emerging Opportunities in Vietnam Motor Insurance Industry

Emerging opportunities in the Vietnam Motor Insurance Industry are abundant, driven by innovation and evolving market demands. The widespread adoption of InsurTech solutions, such as AI for underwriting and claims, and telematics for UBI, presents a significant avenue for improved efficiency and personalized offerings. The growing demand for electric vehicles (EVs) creates a niche market for specialized EV insurance products and services. Strategic partnerships with automotive manufacturers, dealerships, and financial institutions can unlock new distribution channels and customer segments. Furthermore, the increasing urbanization and rising middle class are fueling a demand for premium and comprehensive insurance policies, offering substantial growth potential for insurers focusing on value-added services and superior customer experiences.

Leading Players in the Vietnam Motor Insurance Industry Sector

- Bao Viet Holdings

- PetroVietnam Insurance (PVI)

- Bao Minh Insurance Corporation

- Liberty Insurance Vietnam

- Petrolimex Joint Stock Insurance Company (Pjico)

- AAA Assurance Corporation

- BIDV Insurance Corporation

- Fubon Insurance Company

- Phu Hung Assurance Corporation

- Samsung Vina Insurance Company

Key Milestones in Vietnam Motor Insurance Industry Industry

- December 2023: Cathay Insurance Vietnam launched an all-inclusive "Dual Finance" initiative with SAWAD, enabling customers to seamlessly secure mandatory insurance coverage while accessing financial assistance. Cathay also announced plans to roll out a personal injury insurance scheme, complementing its existing financial support and automobile insurance offerings.

- November 2023: Vietnam officially joined the Association of Southeast Asian Nations (ASEAN) Compulsory Motor Insurance Scheme (ACMI), mandating third-party motor liability insurance for all motor vehicles transiting within or en route to any ASEAN member state.

Strategic Outlook for Vietnam Motor Insurance Industry Market

The strategic outlook for the Vietnam Motor Insurance Industry is highly promising, characterized by sustained growth and evolving market dynamics. Key growth accelerators include the continued digital transformation of the insurance value chain, from customer acquisition to claims settlement, offering opportunities for enhanced efficiency and customer engagement. The increasing adoption of InsurTech, including AI, telematics, and blockchain, will be pivotal in developing personalized products and optimizing operational costs. Strategic partnerships with automotive ecosystem players, such as manufacturers and ride-sharing platforms, will unlock new revenue streams and customer bases. Furthermore, the growing demand for specialized insurance products, like those for electric vehicles and shared mobility services, presents significant untapped market potential for agile and innovative insurers to capitalize on.

Vietnam Motor Insurance Industry Segmentation

-

1. Policy Type

- 1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 1.2. Comprehensive Insurance

-

2. Vehicle Type

- 2.1. Passenger Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Agents

- 3.2. Brokers

- 3.3. Banks

- 3.4. Online

- 3.5. Other Distribution Channels

Vietnam Motor Insurance Industry Segmentation By Geography

- 1. Vietnam

Vietnam Motor Insurance Industry Regional Market Share

Geographic Coverage of Vietnam Motor Insurance Industry

Vietnam Motor Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Policy Type

- 5.1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 5.1.2. Comprehensive Insurance

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Agents

- 5.3.2. Brokers

- 5.3.3. Banks

- 5.3.4. Online

- 5.3.5. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Vietnam

- 5.1. Market Analysis, Insights and Forecast - by Policy Type

- 6. Vietnam Motor Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Policy Type

- 6.1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 6.1.2. Comprehensive Insurance

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Vehicles

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Agents

- 6.3.2. Brokers

- 6.3.3. Banks

- 6.3.4. Online

- 6.3.5. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Policy Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bao Viet Holdings

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 PetroVietnam Insurance (PVI)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Bao Minh Insurance Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Liberty Insurance Vietnam

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Petrolimex Joint Stock Insurance Company (Pjico)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 AAA Assurance Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BIDV Insurance Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Fubon Insurance Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Phu Hung Assurance Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Samsung Vina Insurance Company**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Bao Viet Holdings

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Vietnam Motor Insurance Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Vietnam Motor Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: Vietnam Motor Insurance Industry Revenue Million Forecast, by Policy Type 2020 & 2033

- Table 2: Vietnam Motor Insurance Industry Volume Billion Forecast, by Policy Type 2020 & 2033

- Table 3: Vietnam Motor Insurance Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 4: Vietnam Motor Insurance Industry Volume Billion Forecast, by Vehicle Type 2020 & 2033

- Table 5: Vietnam Motor Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Vietnam Motor Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 7: Vietnam Motor Insurance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Vietnam Motor Insurance Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Vietnam Motor Insurance Industry Revenue Million Forecast, by Policy Type 2020 & 2033

- Table 10: Vietnam Motor Insurance Industry Volume Billion Forecast, by Policy Type 2020 & 2033

- Table 11: Vietnam Motor Insurance Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 12: Vietnam Motor Insurance Industry Volume Billion Forecast, by Vehicle Type 2020 & 2033

- Table 13: Vietnam Motor Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 14: Vietnam Motor Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Vietnam Motor Insurance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Vietnam Motor Insurance Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vietnam Motor Insurance Industry?

The projected CAGR is approximately 4.50%.

2. Which companies are prominent players in the Vietnam Motor Insurance Industry?

Key companies in the market include Bao Viet Holdings, PetroVietnam Insurance (PVI), Bao Minh Insurance Corporation, Liberty Insurance Vietnam, Petrolimex Joint Stock Insurance Company (Pjico), AAA Assurance Corporation, BIDV Insurance Corporation, Fubon Insurance Company, Phu Hung Assurance Corporation, Samsung Vina Insurance Company**List Not Exhaustive.

3. What are the main segments of the Vietnam Motor Insurance Industry?

The market segments include Policy Type, Vehicle Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.81 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government.

6. What are the notable trends driving market growth?

Surge in Vehicle Ownership Generating Major Demand in the Market.

7. Are there any restraints impacting market growth?

Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government.

8. Can you provide examples of recent developments in the market?

December 2023: Cathay Insurance Vietnam joined hands with SAWAD to unveil an all-inclusive "Dual Finance" initiative. This program empowers customers to seek financial assistance while securing mandatory insurance coverage seamlessly. To cater to its clientele's diverse needs, Cathay has set to roll out a personal injury insurance scheme in December, complementing its existing financial support and automobile insurance offerings.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vietnam Motor Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vietnam Motor Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vietnam Motor Insurance Industry?

To stay informed about further developments, trends, and reports in the Vietnam Motor Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence