Key Insights

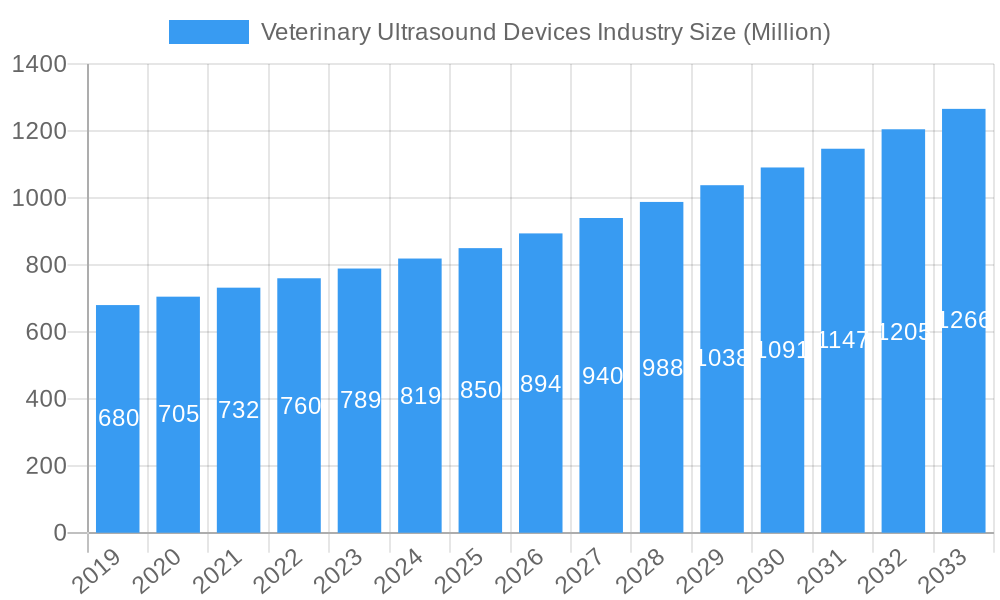

The global Veterinary Ultrasound Devices market is poised for substantial growth, projected to reach an estimated XX million by 2025 and expand at a Compound Annual Growth Rate (CAGR) of 5.60% through 2033. This robust expansion is primarily driven by the increasing adoption of advanced diagnostic imaging in animal healthcare, fueled by a growing pet population and a rising trend in pet humanization. Owners are increasingly willing to invest in comprehensive veterinary care, including sophisticated diagnostic tools like ultrasound, to ensure the health and well-being of their companion animals. Furthermore, advancements in technology, leading to more portable, user-friendly, and cost-effective ultrasound devices, are democratizing access to these critical diagnostic capabilities, especially for smaller veterinary practices and in remote areas. The expanding veterinary workforce, coupled with a greater emphasis on preventative care and early disease detection in both companion and livestock animals, further underpins this market's upward trajectory.

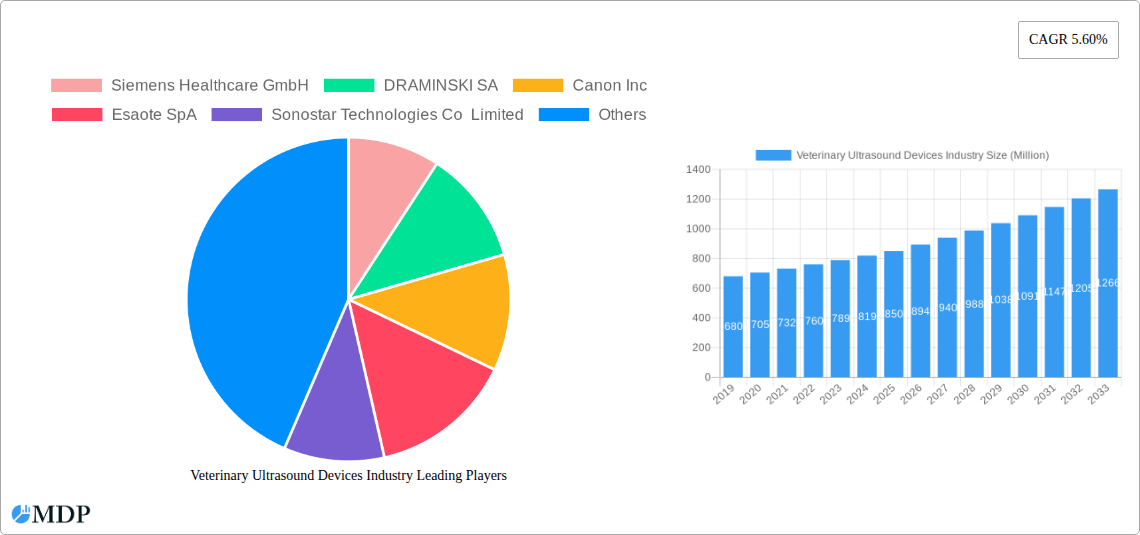

Veterinary Ultrasound Devices Industry Market Size (In Million)

The market segmentation reveals distinct opportunities within both product types and animal categories. Handheld (portable) ultrasound scanners are witnessing rapid adoption due to their convenience and affordability, making them ideal for on-the-go diagnostics and for practices with space constraints. Cart-based ultrasound scanners, offering enhanced imaging capabilities and a wider range of features, continue to be the preferred choice for specialized diagnostics and larger veterinary hospitals. In terms of animal types, the increasing demand for advanced care for small animals, driven by the booming pet industry, presents a significant growth avenue. Simultaneously, the need for efficient herd health management and early disease detection in large animals for livestock production also contributes substantially to market expansion. Leading global players such as Siemens Healthcare GmbH, Canon Inc., and Shenzhen Mindray Bio-Medical Electronics Co Ltd are actively investing in research and development to innovate and capture market share across these diverse segments and key geographical regions.

Veterinary Ultrasound Devices Industry Company Market Share

The veterinary ultrasound devices market is characterized by a moderate to high concentration, driven by a few dominant players alongside a growing number of specialized manufacturers. Key innovation drivers include the increasing demand for advanced diagnostic tools in animal healthcare, the rising pet ownership globally, and the expanding veterinary workforce seeking portable and efficient imaging solutions. Regulatory frameworks, though generally supportive of medical device advancements, can introduce complexities related to product approvals and compliance, impacting market entry and growth. Product substitutes, while limited in direct diagnostic imaging capabilities, might include X-rays or other imaging modalities, but ultrasound's real-time, non-invasive nature offers distinct advantages. End-user trends reveal a strong preference for handheld (portable) ultrasound scanners due to their versatility and affordability, particularly among mobile veterinary services and smaller clinics. There's also a significant trend towards user-friendly interfaces and AI-assisted diagnostics. Merger and acquisition (M&A) activities, though not as frequent as in broader medical device sectors, are strategically important for expanding product portfolios and market reach. For instance, recent partnerships highlight the consolidation and collaborative efforts aimed at strengthening market presence. The market share of leading companies like Siemens Healthcare GmbH and Shenzhen Mindray Bio-Medical Electronics Co Ltd is substantial, reflecting their extensive product lines and established distribution networks. The number of significant M&A deals in the past few years is estimated to be around 5-10, indicating a growing appetite for strategic alliances.

Veterinary Ultrasound Devices Industry Industry Trends & Analysis

The veterinary ultrasound devices industry is experiencing robust growth, propelled by several interconnected trends. A primary market growth driver is the escalating investment in animal welfare and advanced veterinary care, fueled by increased disposable incomes and a deepening human-animal bond, leading pet owners to seek and afford sophisticated diagnostic services. This translates into a higher demand for accurate and timely diagnoses provided by ultrasound technology. Technological disruptions are at the forefront, with the continuous development of AI-powered diagnostic support, miniaturization of components leading to more powerful handheld devices, and enhanced image resolution and penetration capabilities. These innovations are not only improving diagnostic accuracy but also making ultrasound more accessible and user-friendly for veterinary professionals. Consumer preferences are strongly leaning towards point-of-care ultrasound (POCUS) solutions, emphasizing portability, ease of use, and immediate results, which are crucial for emergency care and field diagnostics. The market penetration of veterinary ultrasound devices is steadily increasing, moving beyond specialized referral centers to general veterinary practices. The Compound Annual Growth Rate (CAGR) for the veterinary ultrasound devices market is projected to be around 7.5% to 8.5% over the forecast period. Competitive dynamics are intensifying, with established players investing heavily in R&D to maintain their edge, while new entrants are focusing on niche markets and innovative technologies. The increasing adoption of cloud-based platforms for image storage and telemedicine in veterinary diagnostics also presents a significant trend, enabling remote consultations and collaborative diagnostics. The integration of multi-modal imaging solutions and the development of specialized probes for different anatomical regions further enhance the utility and appeal of veterinary ultrasound.

Leading Markets & Segments in Veterinary Ultrasound Devices Industry

The North American region, particularly the United States, currently dominates the veterinary ultrasound devices market, driven by high per capita spending on pet healthcare, a large and well-established veterinary infrastructure, and a strong propensity for adopting advanced medical technologies. The dominance of the US is further bolstered by favorable economic policies that support healthcare innovation and infrastructure development, alongside a robust ecosystem of veterinary research institutions and professional organizations promoting advanced diagnostic imaging. Within this region, the Handheld (Portable) Ultrasound Scanner segment exhibits exceptional growth and market penetration.

- Key Drivers for Handheld Ultrasound Dominance:

- Portability and Convenience: Enables veterinarians to perform diagnostics in various settings, including farms, field calls, and examination rooms, without requiring dedicated imaging suites.

- Cost-Effectiveness: Generally more affordable than cart-based systems, making them accessible to a broader range of veterinary practices, including smaller clinics and individual practitioners.

- Ease of Use: Modern handheld devices often feature intuitive interfaces and touch-screen controls, reducing the learning curve for veterinary staff.

- Rapid Advancements: Continuous innovation in battery life, image quality, and AI integration is enhancing their diagnostic capabilities to rival larger systems.

The Small Animals segment is the leading end-user application, primarily due to the soaring popularity of companion animals like dogs and cats. The increasing focus on preventative care, early disease detection, and specialized treatments for these animals necessitates sophisticated diagnostic tools like ultrasound.

- Key Drivers for Small Animal Segment Dominance:

- High Pet Ownership Rates: Companion animals constitute the largest proportion of the veterinary patient base globally.

- Increased Lifespan of Pets: As pets live longer, they are more prone to age-related conditions requiring advanced diagnostics.

- Humanization of Pets: Owners are investing more in their pets' health, treating them as family members, and demanding high-quality veterinary care.

- Advancements in Small Animal Medicine: Specialized treatments for small animal diseases often rely heavily on precise diagnostic imaging.

While cart-based ultrasound scanners still hold a significant market share, especially in specialized referral hospitals and teaching facilities for their superior image processing capabilities and wider range of transducers, the rapid evolution and increasing sophistication of handheld devices are steadily eroding this advantage. The Large Animals segment, while important for applications in livestock management and equine sports medicine, is currently secondary to the small animal segment in terms of overall market value due to the fewer number of large animals requiring such intensive diagnostics compared to the vast population of companion animals. However, the development of robust, portable, and specialized probes for large animals continues to be an area of focus for manufacturers.

Veterinary Ultrasound Devices Industry Product Developments

Product development in the veterinary ultrasound devices industry is rapidly advancing, with a strong emphasis on portability, enhanced image quality, and user-friendly interfaces. Innovations include the integration of artificial intelligence for automated measurements, lesion detection, and diagnostic assistance, significantly improving efficiency and accuracy for veterinarians. Handheld (portable) ultrasound scanners are at the forefront of this revolution, offering veterinary professionals powerful diagnostic tools that can be easily transported and utilized in diverse clinical settings. Manufacturers are also focusing on developing specialized transducers and software packages tailored for specific animal types and diagnostic applications, such as cardiology, abdominal imaging, and reproductive health in both small and large animals. These advancements are not only improving diagnostic outcomes but also expanding the range of conditions that can be effectively managed with ultrasound, solidifying its role as an indispensable diagnostic modality in modern veterinary medicine.

Key Drivers of Veterinary Ultrasound Devices Industry Growth

The veterinary ultrasound devices industry's growth is propelled by a confluence of factors. Technologically, advancements in miniaturization, image processing, and AI integration are making devices more powerful, portable, and user-friendly. Economically, the increasing disposable income globally and the humanization of pets are driving higher spending on advanced veterinary care, creating a strong demand for sophisticated diagnostic tools. Regulatory landscapes, while requiring compliance, are generally supportive of medical device innovation aimed at improving animal health outcomes. Furthermore, the growing awareness among pet owners and livestock farmers about the benefits of early disease detection and preventative care through imaging modalities like ultrasound is a significant catalyst. The expanding veterinary workforce, particularly in emerging economies, also contributes to market expansion.

Challenges in the Veterinary Ultrasound Devices Industry Market

Despite the positive growth trajectory, the veterinary ultrasound devices market faces several challenges. High initial investment costs for advanced systems can be a barrier for smaller clinics and practitioners in developing regions. Limited availability of trained veterinary sonographers and a shortage of comprehensive training programs can hinder widespread adoption and effective utilization of the technology. Regulatory hurdles and varying approval processes across different countries can slow down market entry for new products. Intense competition among key players can lead to price pressures and impact profit margins. Supply chain disruptions, as experienced globally in recent years, can also affect the availability and cost of components, impacting production schedules and product pricing.

Emerging Opportunities in Veterinary Ultrasound Devices Industry

Emerging opportunities in the veterinary ultrasound devices industry are centered around technological innovation and market expansion strategies. The development of AI-driven diagnostic platforms holds immense potential to democratize access to expert-level diagnostics, even in remote or underserved areas. The burgeoning market for point-of-care ultrasound (POCUS), especially for handheld devices, presents a significant growth avenue, catering to the demand for immediate diagnostics in diverse settings. Strategic partnerships between device manufacturers and veterinary software providers can lead to integrated solutions that enhance workflow efficiency and data management. Furthermore, the increasing focus on specialized veterinary applications, such as advanced cardiology, oncology imaging, and reproductive health for both companion and food animals, offers lucrative niche markets for product development and commercialization. Expansion into emerging economies with rapidly growing pet populations and increasing investments in animal healthcare also represents a substantial long-term growth opportunity.

Leading Players in the Veterinary Ultrasound Devices Industry Sector

- Siemens Healthcare GmbH

- DRAMINSKI SA

- Canon Inc

- Esaote SpA

- Sonostar Technologies Co Limited

- Samsung Medison Co Ltd

- IMV Imaging

- Shenzhen Mindray Bio-Medical Electronics Co Ltd

- Fujifilm Holdings Corporation

Key Milestones in Veterinary Ultrasound Devices Industry Industry

- November 2022: Advanced Veterinary Ultrasound (AVU), a Division of Advanced Ultrasound Systems, partnered with Draminski SA to offer Draminski's portable ultrasound systems, including the Draminski Blue, iScan2, and iScan Mini, to the veterinary market, expanding AVU's product line and Draminski's market reach.

- August 2022: GM Medical partnered with Butterfly Network to distribute the iQ+ Vet, Butterfly's second-generation veterinary ultrasound device, to veterinarians in Denmark, Sweden, Norway, and Finland, aiming to provide sharper imaging and advanced diagnostic capabilities.

Strategic Outlook for Veterinary Ultrasound Devices Industry Market

The strategic outlook for the veterinary ultrasound devices industry is exceptionally promising, driven by sustained demand for advanced animal healthcare solutions. Future growth will be accelerated by continued innovation in artificial intelligence for enhanced diagnostic capabilities and user-friendliness, particularly in the handheld ultrasound segment. Strategic partnerships and collaborations between technology providers and veterinary organizations will be crucial for expanding market reach and fostering adoption. The increasing emphasis on preventative care and early disease detection in both companion and food animals presents a significant opportunity for the proliferation of ultrasound technology. Furthermore, the growing adoption of telemedicine and cloud-based solutions in veterinary diagnostics will create new avenues for remote support, data analysis, and collaborative diagnostics, further solidifying the industry's growth trajectory. The market is poised for expansion as technological advancements continue to make ultrasound more accessible and indispensable across the global veterinary landscape.

Veterinary Ultrasound Devices Industry Segmentation

-

1. Product

- 1.1. Handheld (Portable) Ultrasound Scanner

- 1.2. Cart-based Ultrasound Scanner

-

2. Animal Type

- 2.1. Small Animals

- 2.2. Large Animals

Veterinary Ultrasound Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

- 4. Middle East

-

5. GCC

- 5.1. South Africa

- 5.2. Rest of Middle East

-

6. South America

- 6.1. Brazil

- 6.2. Argentina

- 6.3. Rest of South America

Veterinary Ultrasound Devices Industry Regional Market Share

Geographic Coverage of Veterinary Ultrasound Devices Industry

Veterinary Ultrasound Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Animal Adoption and Animal Health Expenditure; Rise in Demand for Diagnosis of Animal Health Conditions and Technological Advancements

- 3.3. Market Restrains

- 3.3.1. Lack of Skilled Personnel; High Cost of the Devices

- 3.4. Market Trends

- 3.4.1. Small Animals Segment is Expected to Witness a Healthy CAGR Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Veterinary Ultrasound Devices Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Handheld (Portable) Ultrasound Scanner

- 5.1.2. Cart-based Ultrasound Scanner

- 5.2. Market Analysis, Insights and Forecast - by Animal Type

- 5.2.1. Small Animals

- 5.2.2. Large Animals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East

- 5.3.5. GCC

- 5.3.6. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Veterinary Ultrasound Devices Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Handheld (Portable) Ultrasound Scanner

- 6.1.2. Cart-based Ultrasound Scanner

- 6.2. Market Analysis, Insights and Forecast - by Animal Type

- 6.2.1. Small Animals

- 6.2.2. Large Animals

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Europe Veterinary Ultrasound Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Handheld (Portable) Ultrasound Scanner

- 7.1.2. Cart-based Ultrasound Scanner

- 7.2. Market Analysis, Insights and Forecast - by Animal Type

- 7.2.1. Small Animals

- 7.2.2. Large Animals

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Asia Pacific Veterinary Ultrasound Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Handheld (Portable) Ultrasound Scanner

- 8.1.2. Cart-based Ultrasound Scanner

- 8.2. Market Analysis, Insights and Forecast - by Animal Type

- 8.2.1. Small Animals

- 8.2.2. Large Animals

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Middle East Veterinary Ultrasound Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Handheld (Portable) Ultrasound Scanner

- 9.1.2. Cart-based Ultrasound Scanner

- 9.2. Market Analysis, Insights and Forecast - by Animal Type

- 9.2.1. Small Animals

- 9.2.2. Large Animals

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. GCC Veterinary Ultrasound Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Handheld (Portable) Ultrasound Scanner

- 10.1.2. Cart-based Ultrasound Scanner

- 10.2. Market Analysis, Insights and Forecast - by Animal Type

- 10.2.1. Small Animals

- 10.2.2. Large Animals

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. South America Veterinary Ultrasound Devices Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Handheld (Portable) Ultrasound Scanner

- 11.1.2. Cart-based Ultrasound Scanner

- 11.2. Market Analysis, Insights and Forecast - by Animal Type

- 11.2.1. Small Animals

- 11.2.2. Large Animals

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Global Market Share Analysis 2025

- 12.2. Company Profiles

- 12.2.1 Siemens Healthcare GmbH

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 DRAMINSKI SA

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Canon Inc

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Esaote SpA

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Sonostar Technologies Co Limited

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Samsung Medison Co Ltd

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 IMV Imaging

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Shenzhen Mindray Bio-Medical Electronics Co Ltd

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Fujifilm Holdings Corporation

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.1 Siemens Healthcare GmbH

List of Figures

- Figure 1: Global Veterinary Ultrasound Devices Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Veterinary Ultrasound Devices Industry Volume Breakdown (K Units, %) by Region 2025 & 2033

- Figure 3: North America Veterinary Ultrasound Devices Industry Revenue (undefined), by Product 2025 & 2033

- Figure 4: North America Veterinary Ultrasound Devices Industry Volume (K Units), by Product 2025 & 2033

- Figure 5: North America Veterinary Ultrasound Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Veterinary Ultrasound Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 7: North America Veterinary Ultrasound Devices Industry Revenue (undefined), by Animal Type 2025 & 2033

- Figure 8: North America Veterinary Ultrasound Devices Industry Volume (K Units), by Animal Type 2025 & 2033

- Figure 9: North America Veterinary Ultrasound Devices Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 10: North America Veterinary Ultrasound Devices Industry Volume Share (%), by Animal Type 2025 & 2033

- Figure 11: North America Veterinary Ultrasound Devices Industry Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Veterinary Ultrasound Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 13: North America Veterinary Ultrasound Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Veterinary Ultrasound Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Veterinary Ultrasound Devices Industry Revenue (undefined), by Product 2025 & 2033

- Figure 16: Europe Veterinary Ultrasound Devices Industry Volume (K Units), by Product 2025 & 2033

- Figure 17: Europe Veterinary Ultrasound Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 18: Europe Veterinary Ultrasound Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 19: Europe Veterinary Ultrasound Devices Industry Revenue (undefined), by Animal Type 2025 & 2033

- Figure 20: Europe Veterinary Ultrasound Devices Industry Volume (K Units), by Animal Type 2025 & 2033

- Figure 21: Europe Veterinary Ultrasound Devices Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 22: Europe Veterinary Ultrasound Devices Industry Volume Share (%), by Animal Type 2025 & 2033

- Figure 23: Europe Veterinary Ultrasound Devices Industry Revenue (undefined), by Country 2025 & 2033

- Figure 24: Europe Veterinary Ultrasound Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 25: Europe Veterinary Ultrasound Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Veterinary Ultrasound Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Veterinary Ultrasound Devices Industry Revenue (undefined), by Product 2025 & 2033

- Figure 28: Asia Pacific Veterinary Ultrasound Devices Industry Volume (K Units), by Product 2025 & 2033

- Figure 29: Asia Pacific Veterinary Ultrasound Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Asia Pacific Veterinary Ultrasound Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 31: Asia Pacific Veterinary Ultrasound Devices Industry Revenue (undefined), by Animal Type 2025 & 2033

- Figure 32: Asia Pacific Veterinary Ultrasound Devices Industry Volume (K Units), by Animal Type 2025 & 2033

- Figure 33: Asia Pacific Veterinary Ultrasound Devices Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 34: Asia Pacific Veterinary Ultrasound Devices Industry Volume Share (%), by Animal Type 2025 & 2033

- Figure 35: Asia Pacific Veterinary Ultrasound Devices Industry Revenue (undefined), by Country 2025 & 2033

- Figure 36: Asia Pacific Veterinary Ultrasound Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 37: Asia Pacific Veterinary Ultrasound Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Veterinary Ultrasound Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East Veterinary Ultrasound Devices Industry Revenue (undefined), by Product 2025 & 2033

- Figure 40: Middle East Veterinary Ultrasound Devices Industry Volume (K Units), by Product 2025 & 2033

- Figure 41: Middle East Veterinary Ultrasound Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 42: Middle East Veterinary Ultrasound Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 43: Middle East Veterinary Ultrasound Devices Industry Revenue (undefined), by Animal Type 2025 & 2033

- Figure 44: Middle East Veterinary Ultrasound Devices Industry Volume (K Units), by Animal Type 2025 & 2033

- Figure 45: Middle East Veterinary Ultrasound Devices Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 46: Middle East Veterinary Ultrasound Devices Industry Volume Share (%), by Animal Type 2025 & 2033

- Figure 47: Middle East Veterinary Ultrasound Devices Industry Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East Veterinary Ultrasound Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 49: Middle East Veterinary Ultrasound Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East Veterinary Ultrasound Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: GCC Veterinary Ultrasound Devices Industry Revenue (undefined), by Product 2025 & 2033

- Figure 52: GCC Veterinary Ultrasound Devices Industry Volume (K Units), by Product 2025 & 2033

- Figure 53: GCC Veterinary Ultrasound Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 54: GCC Veterinary Ultrasound Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 55: GCC Veterinary Ultrasound Devices Industry Revenue (undefined), by Animal Type 2025 & 2033

- Figure 56: GCC Veterinary Ultrasound Devices Industry Volume (K Units), by Animal Type 2025 & 2033

- Figure 57: GCC Veterinary Ultrasound Devices Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 58: GCC Veterinary Ultrasound Devices Industry Volume Share (%), by Animal Type 2025 & 2033

- Figure 59: GCC Veterinary Ultrasound Devices Industry Revenue (undefined), by Country 2025 & 2033

- Figure 60: GCC Veterinary Ultrasound Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 61: GCC Veterinary Ultrasound Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: GCC Veterinary Ultrasound Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 63: South America Veterinary Ultrasound Devices Industry Revenue (undefined), by Product 2025 & 2033

- Figure 64: South America Veterinary Ultrasound Devices Industry Volume (K Units), by Product 2025 & 2033

- Figure 65: South America Veterinary Ultrasound Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 66: South America Veterinary Ultrasound Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 67: South America Veterinary Ultrasound Devices Industry Revenue (undefined), by Animal Type 2025 & 2033

- Figure 68: South America Veterinary Ultrasound Devices Industry Volume (K Units), by Animal Type 2025 & 2033

- Figure 69: South America Veterinary Ultrasound Devices Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 70: South America Veterinary Ultrasound Devices Industry Volume Share (%), by Animal Type 2025 & 2033

- Figure 71: South America Veterinary Ultrasound Devices Industry Revenue (undefined), by Country 2025 & 2033

- Figure 72: South America Veterinary Ultrasound Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 73: South America Veterinary Ultrasound Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 74: South America Veterinary Ultrasound Devices Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 2: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Product 2020 & 2033

- Table 3: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Animal Type 2020 & 2033

- Table 4: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Animal Type 2020 & 2033

- Table 5: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 7: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 8: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Product 2020 & 2033

- Table 9: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Animal Type 2020 & 2033

- Table 10: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Animal Type 2020 & 2033

- Table 11: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 13: United States Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 15: Canada Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 17: Mexico Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 19: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 20: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Product 2020 & 2033

- Table 21: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Animal Type 2020 & 2033

- Table 22: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Animal Type 2020 & 2033

- Table 23: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 25: Germany Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Germany Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 29: France Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: France Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 31: Italy Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Italy Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 33: Spain Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: Spain Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 37: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 38: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Product 2020 & 2033

- Table 39: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Animal Type 2020 & 2033

- Table 40: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Animal Type 2020 & 2033

- Table 41: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 42: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 43: China Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: China Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 45: Japan Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Japan Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 47: India Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: India Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 49: Australia Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Australia Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 51: South Korea Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: South Korea Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 55: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 56: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Product 2020 & 2033

- Table 57: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Animal Type 2020 & 2033

- Table 58: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Animal Type 2020 & 2033

- Table 59: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 61: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 62: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Product 2020 & 2033

- Table 63: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Animal Type 2020 & 2033

- Table 64: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Animal Type 2020 & 2033

- Table 65: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 66: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 67: South Africa Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: South Africa Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 69: Rest of Middle East Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: Rest of Middle East Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 71: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 72: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Product 2020 & 2033

- Table 73: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Animal Type 2020 & 2033

- Table 74: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Animal Type 2020 & 2033

- Table 75: Global Veterinary Ultrasound Devices Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 76: Global Veterinary Ultrasound Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 77: Brazil Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 78: Brazil Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 79: Argentina Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: Argentina Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 81: Rest of South America Veterinary Ultrasound Devices Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: Rest of South America Veterinary Ultrasound Devices Industry Volume (K Units) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Ultrasound Devices Industry?

The projected CAGR is approximately 8.19%.

2. Which companies are prominent players in the Veterinary Ultrasound Devices Industry?

Key companies in the market include Siemens Healthcare GmbH, DRAMINSKI SA, Canon Inc, Esaote SpA, Sonostar Technologies Co Limited, Samsung Medison Co Ltd, IMV Imaging, Shenzhen Mindray Bio-Medical Electronics Co Ltd, Fujifilm Holdings Corporation.

3. What are the main segments of the Veterinary Ultrasound Devices Industry?

The market segments include Product, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increase in Animal Adoption and Animal Health Expenditure; Rise in Demand for Diagnosis of Animal Health Conditions and Technological Advancements.

6. What are the notable trends driving market growth?

Small Animals Segment is Expected to Witness a Healthy CAGR Over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Skilled Personnel; High Cost of the Devices.

8. Can you provide examples of recent developments in the market?

In November 2022, Advanced Veterinary Ultrasound (AVU), a Division of Advanced Ultrasound Systems, and Draminski SA, a manufacturer of quality point-of-care ultrasound (POCUS), partnered to provide feature-rich systems to the veterinary market. Through the agreement, AVU is authorized to market, sell, and service the line of portable ultrasound systems Draminski offers, such as the Draminski Blue, iScan2, and iScan Mini systems.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Ultrasound Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Ultrasound Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Ultrasound Devices Industry?

To stay informed about further developments, trends, and reports in the Veterinary Ultrasound Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence