Key Insights

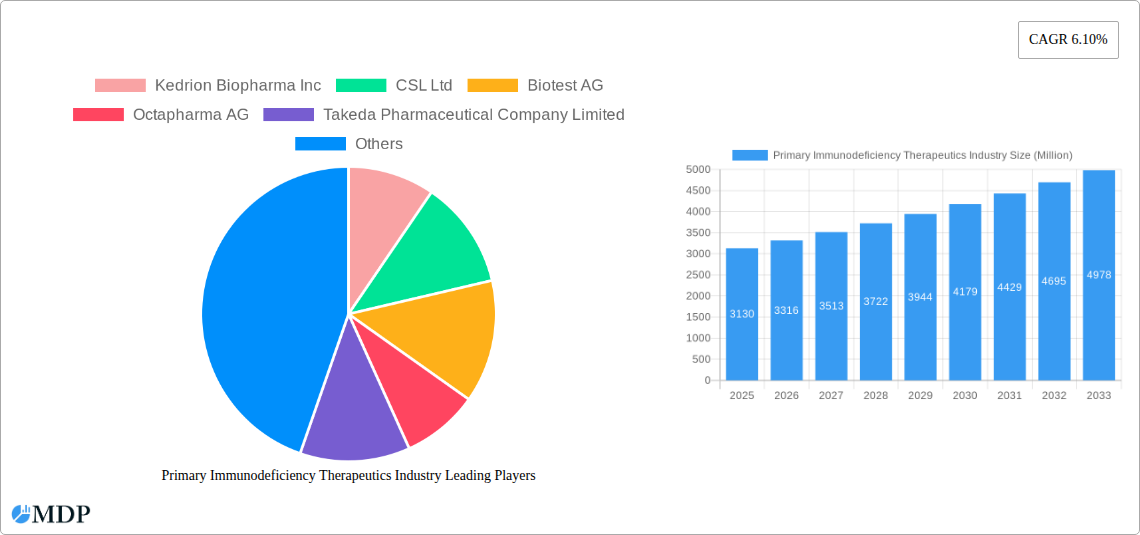

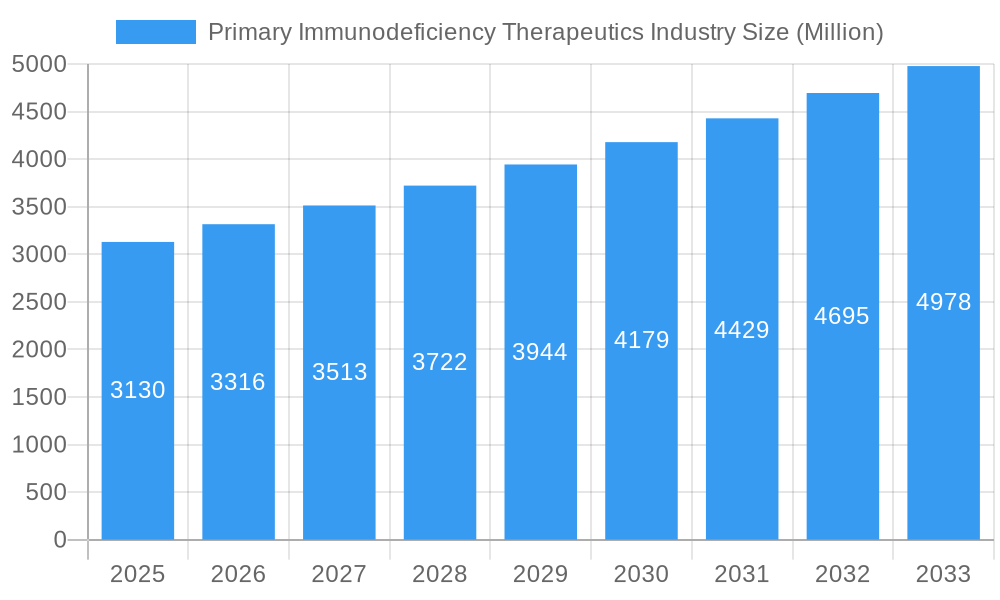

The global Primary Immunodeficiency Therapeutics Market is poised for robust growth, projected to reach approximately $3.13 billion in 2025 and expand at a significant Compound Annual Growth Rate (CAGR) of 5.7% through 2033. This expansion is fueled by increasing awareness of primary immunodeficiencies (PIDs), advancements in diagnostic capabilities leading to earlier detection, and a growing pipeline of innovative therapeutic solutions. Key drivers include the rising incidence of these rare genetic disorders, a greater understanding of the immune system, and the development of targeted therapies that offer improved patient outcomes. The market is broadly segmented by Disease Type, with Antibody Deficiency and Cellular Immunodeficiency representing significant segments due to their prevalence and the availability of established treatments. Product types such as Immunoglobulin Replacement Therapy and Stem Cell/Bone Marrow Transplantation are currently dominant, reflecting the established treatment paradigms. However, emerging therapies like Gene Therapy are expected to witness substantial growth as research progresses and regulatory approvals expand.

Primary Immunodeficiency Therapeutics Industry Market Size (In Billion)

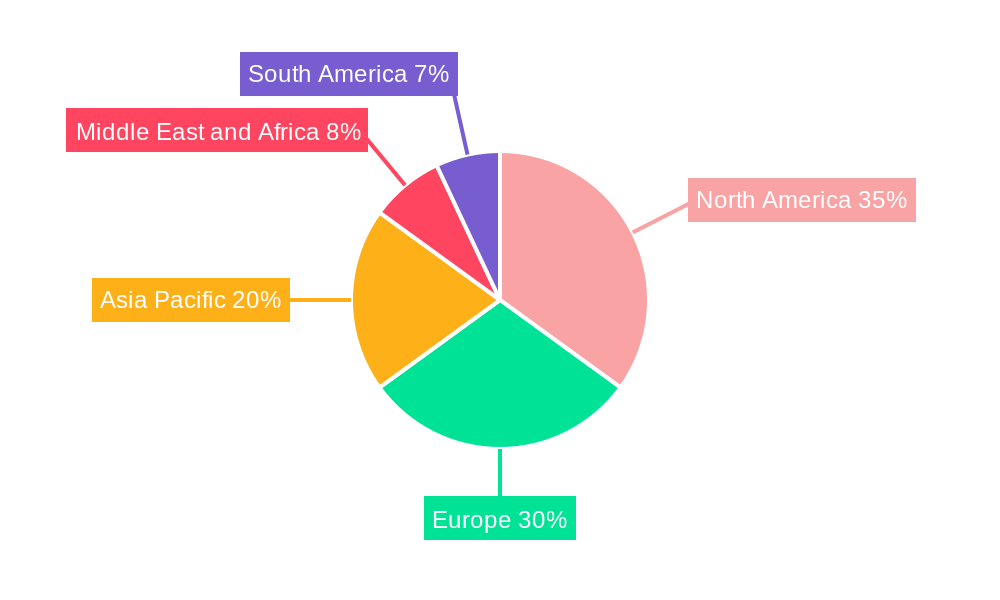

The market's trajectory is further supported by favorable reimbursement policies in key regions and increasing investments in research and development by leading pharmaceutical and biotechnology companies. North America and Europe are anticipated to remain dominant markets due to their advanced healthcare infrastructures, high diagnostic rates, and significant patient populations. However, the Asia Pacific region is expected to exhibit the fastest growth, driven by expanding healthcare access, a growing awareness of PIDs, and government initiatives to improve rare disease management. While the market is largely driven by therapeutic advancements, certain restraints such as the high cost of some treatments and the diagnostic challenges associated with rare PIDs may pose hurdles. Nevertheless, the overall outlook remains positive, with continuous innovation and increasing patient advocacy shaping a dynamic and evolving landscape for primary immunodeficiency therapeutics.

Primary Immunodeficiency Therapeutics Industry Company Market Share

Primary Immunodeficiency Therapeutics Market: Comprehensive Growth Analysis and Forecast (2019-2033)

This in-depth report provides a strategic analysis of the Primary Immunodeficiency Therapeutics market, offering granular insights into market dynamics, growth drivers, segmentation, and competitive landscape. Spanning the historical period of 2019-2024 and a forecast period of 2025-2033, with a base year of 2025, this study is an essential resource for industry stakeholders seeking to understand the future trajectory of PID therapeutics. The global Primary Immunodeficiency market is projected to witness substantial growth, driven by advancements in treatment modalities and increasing diagnosis rates. The market is valued in the billions, with significant investment in gene therapy for primary immunodeficiency and immunoglobulin replacement therapy. Key segments include antibody deficiency treatment, cellular immunodeficiency therapies, and emerging treatments for innate immune disorders.

Primary Immunodeficiency Therapeutics Industry Market Dynamics & Concentration

The Primary Immunodeficiency Therapeutics industry is characterized by a moderate to high level of market concentration, with a few key players dominating the immunoglobulin therapy market and gene therapy for PID. Innovation remains a primary driver, fueled by ongoing research into novel therapeutic targets and delivery mechanisms for rare immunodeficiency diseases. Regulatory frameworks, while stringent, are progressively adapting to accommodate advancements in PID treatment options. Product substitutes, primarily supportive care and off-label treatments, exert some pressure, but the development of targeted therapies is reducing their impact. End-user trends indicate a growing demand for personalized medicine and improved quality of life for patients. Mergers and acquisitions (M&A) activity, while not excessively high, plays a crucial role in consolidating market share and expanding R&D capabilities. For instance, recent years have seen strategic acquisitions aimed at bolstering portfolios in PID gene therapy. The market share for leading Primary Immunodeficiency drug manufacturers is closely monitored, with substantial investments in immunodeficiency disease research. M&A deal counts are expected to remain steady, focusing on acquiring innovative technologies and pipeline assets.

Primary Immunodeficiency Therapeutics Industry Industry Trends & Analysis

The Primary Immunodeficiency Therapeutics industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. This expansion is primarily fueled by a combination of increasing disease awareness, improved diagnostic capabilities, and significant advancements in treatment modalities. The market penetration of effective PID therapies is steadily rising as more patients gain access to life-changing treatments. Technological disruptions, particularly in gene therapy and cell therapy for primary immunodeficiency, are revolutionizing patient care, offering potential cures rather than just management. Consumer preferences are shifting towards less invasive and more effective treatments, creating a strong demand for novel PID drug development. Competitive dynamics are intensifying, with both established pharmaceutical giants and agile biotechnology firms vying for market leadership in immunodeficiency disorder treatment. The rising prevalence of diagnosed primary immunodeficiency diseases worldwide, coupled with the increasing availability of specialized treatments like subcutaneous immunoglobulin therapy and bone marrow transplant for immunodeficiency, are significant growth drivers. Furthermore, government initiatives and patient advocacy groups are playing a vital role in driving research and ensuring greater access to immunodeficiency treatments. The market's trajectory is also influenced by ongoing clinical trials for new PID medications and the expanding indications for existing therapies, such as the use of immunoglobulin for autoimmune conditions that may co-exist with primary immunodeficiencies.

Leading Markets & Segments in Primary Immunodeficiency Therapeutics Industry

The Antibody Deficiency segment represents the largest and most mature market within the Primary Immunodeficiency Therapeutics Industry. This dominance is attributed to its higher prevalence compared to other PID categories and the long-standing availability and efficacy of Immunoglobulin Replacement Therapy (IRT). The global market for PID treatment is heavily influenced by regions with well-established healthcare infrastructure and high disease awareness. North America and Europe currently lead in market value due to robust reimbursement policies and advanced diagnostic capabilities.

Disease Type Dominance:

- Antibody Deficiency: This segment is driven by the widespread diagnosis and established treatment protocols for conditions like Common Variable Immunodeficiency (CVID) and X-linked Agammaglobulinemia (XLA). The availability of various immunoglobulin formulations, including intravenous (IVIG) and subcutaneous (SCIG), caters to diverse patient needs and preferences, further bolstering market share. Economic policies supporting chronic disease management and extensive clinical research contribute to sustained growth.

- Cellular Immunodeficiency: While a smaller segment, it is experiencing rapid growth due to advancements in Stem Cell/Bone Marrow Transplantation and emerging gene therapy for SCID (Severe Combined Immunodeficiency). The increasing success rates and reduced risks associated with these procedures are making them more accessible. Government funding for rare disease research and infrastructure development for transplant centers are key drivers.

- Innate Immune Disorders: This is an emerging segment with significant growth potential. As understanding of these complex disorders deepens, novel therapeutic approaches, including targeted drug therapies, are being developed. The high unmet medical need and the promise of breakthrough treatments are attracting substantial investment.

- Others: This category encompasses rarer PID types, which are benefiting from increased research focus and the development of specialized treatments.

Product Type Dominance:

- Immunoglobulin Replacement Therapy: This remains the cornerstone of PID treatment, accounting for the largest market share. Its broad applicability across various antibody deficiencies and proven efficacy ensure its continued dominance. Market growth is supported by the development of more convenient and patient-friendly formulations.

- Stem Cell/Bone Marrow Transplantation: Crucial for certain severe forms of PID, this segment is experiencing growth due to improved outcomes and increased accessibility to transplant centers.

- Gene Therapy: This is the fastest-growing segment, representing a paradigm shift in PID treatment. Its potential for curative outcomes is driving significant research and development investment, promising to reshape the market in the long term.

- Antibiotic Therapy: While primarily supportive, this segment is essential for managing recurrent infections in PID patients and will continue to play a significant role.

Primary Immunodeficiency Therapeutics Industry Product Developments

Product developments in the Primary Immunodeficiency Therapeutics industry are primarily focused on enhancing efficacy, safety, and patient convenience. Innovations in immunoglobulin replacement therapy include the development of more concentrated and less viscous formulations for subcutaneous administration, reducing infusion times and improving patient compliance. Furthermore, cutting-edge gene therapy approaches for primary immunodeficiency are showing immense promise, aiming to correct the underlying genetic defects and offer potentially curative solutions for previously untreatable conditions. The development of novel small molecule therapies targeting specific immune pathways for PID management is also a key trend, offering targeted interventions for conditions like activated phosphoinositide 3-kinase delta (PI3Kδ) syndrome. These advancements are driven by a deeper understanding of immunopathology and a commitment to improving the quality of life for individuals with rare immunodeficiency disorders.

Key Drivers of Primary Immunodeficiency Therapeutics Industry Growth

Several key factors are propelling the growth of the Primary Immunodeficiency Therapeutics Industry. Firstly, significant advancements in PID diagnostics are leading to earlier and more accurate identification of patients, thereby expanding the addressable market for therapeutics. Secondly, ongoing research and development in gene therapy and novel drug discovery are yielding more effective and potentially curative treatments for various immunodeficiency diseases. Thirdly, increasing awareness among healthcare professionals and the public about primary immunodeficiency disorders is improving diagnosis rates and driving demand for specialized care. Finally, supportive government initiatives and favorable reimbursement policies for orphan drugs and advanced therapies further accelerate market expansion. The focus on unmet needs in treating severe forms of PID is also a critical growth catalyst.

Challenges in the Primary Immunodeficiency Therapeutics Industry Market

Despite its growth potential, the Primary Immunodeficiency Therapeutics Industry faces several challenges. High treatment costs associated with gene therapy and immunoglobulin replacement therapy can limit patient access, particularly in developing economies. Stringent regulatory approval processes for novel PID treatments, especially for rare diseases, can lead to extended development timelines and significant R&D expenditure. Supply chain complexities for biologics and plasma-derived therapies can also pose challenges in ensuring consistent availability for patients. Furthermore, the rarity of many primary immunodeficiency diseases can make conducting large-scale clinical trials difficult and expensive, impacting the pace of new product development. The presence of off-label use of existing medications and the need for lifelong treatment for many patients also represent ongoing hurdles.

Emerging Opportunities in Primary Immunodeficiency Therapeutics Industry

The Primary Immunodeficiency Therapeutics Industry is ripe with emerging opportunities. The rapid advancements in gene editing technologies like CRISPR-Cas9 present a transformative opportunity for developing permanent cures for genetic forms of PID. Strategic partnerships between biotechnology firms and large pharmaceutical companies are crucial for accelerating the development and commercialization of these complex therapies. Expansion into emerging markets, where diagnostic capabilities are improving and healthcare infrastructure is developing, offers significant untapped potential for PID treatment. Furthermore, the growing focus on personalized medicine and patient stratification based on genetic profiles will drive the development of highly targeted and effective therapies for specific subtypes of primary immunodeficiency diseases. The increasing exploration of non-IVIG based therapies also opens new avenues for growth.

Leading Players in the Primary Immunodeficiency Therapeutics Industry Sector

- Kedrion Biopharma Inc

- CSL Ltd

- Biotest AG

- Octapharma AG

- Takeda Pharmaceutical Company Limited

- Lupin Pharmaceuticals

- Grifols S A

- LFB group

- Baxter International Inc

- Bio Products Laboratory Limited

Key Milestones in Primary Immunodeficiency Therapeutics Industry Industry

- September 2022: Lactiga Therapeutics successfully raised USD 1.6 million in oversubscribed pre-seed financing, signaling strong investor confidence in their novel therapeutic development for primary immunodeficiency diseases.

- April 2022: Pharming Group N.V. presented positive data from their pivotal Phase II/III trial of leniolisib, a significant advancement in the treatment of activated phosphoinositide 3-kinase delta (PI3Kδ) syndrome (APDS), a specific primary immunodeficiency.

Strategic Outlook for Primary Immunodeficiency Therapeutics Industry Market

The strategic outlook for the Primary Immunodeficiency Therapeutics market is highly promising, driven by a confluence of factors aimed at improving patient outcomes and expanding treatment accessibility. Continued investment in cutting-edge gene therapy and cell therapy research will undoubtedly unlock new curative possibilities for previously untreatable forms of PID. Expansion of diagnostic networks and public health awareness campaigns will further increase the early detection rates, thereby broadening the patient base for existing and novel PID therapies. Furthermore, strategic collaborations and mergers will consolidate expertise and resources, accelerating the development and global rollout of groundbreaking treatments. The increasing focus on patient-centric care models and the development of more convenient immunoglobulin delivery systems will also play a crucial role in shaping the future market landscape, ensuring sustainable growth and improved quality of life for individuals affected by primary immunodeficiency disorders.

Primary Immunodeficiency Therapeutics Industry Segmentation

-

1. Disease Type

- 1.1. Antibody Deficiency

- 1.2. Cellular Immunodeficiency

- 1.3. Innate Immune Disorders

- 1.4. Others

-

2. Product Type

- 2.1. Immunoglobulin Replacement Therapy

- 2.2. Stem Cell/Bone Marrow Transplantation

- 2.3. Antibiotic Therapy

- 2.4. Gene Therapy

- 2.5. Others

Primary Immunodeficiency Therapeutics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Primary Immunodeficiency Therapeutics Industry Regional Market Share

Geographic Coverage of Primary Immunodeficiency Therapeutics Industry

Primary Immunodeficiency Therapeutics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 5.1.1. Antibody Deficiency

- 5.1.2. Cellular Immunodeficiency

- 5.1.3. Innate Immune Disorders

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Immunoglobulin Replacement Therapy

- 5.2.2. Stem Cell/Bone Marrow Transplantation

- 5.2.3. Antibiotic Therapy

- 5.2.4. Gene Therapy

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 6. Global Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 6.1.1. Antibody Deficiency

- 6.1.2. Cellular Immunodeficiency

- 6.1.3. Innate Immune Disorders

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Immunoglobulin Replacement Therapy

- 6.2.2. Stem Cell/Bone Marrow Transplantation

- 6.2.3. Antibiotic Therapy

- 6.2.4. Gene Therapy

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 7. North America Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 7.1.1. Antibody Deficiency

- 7.1.2. Cellular Immunodeficiency

- 7.1.3. Innate Immune Disorders

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Immunoglobulin Replacement Therapy

- 7.2.2. Stem Cell/Bone Marrow Transplantation

- 7.2.3. Antibiotic Therapy

- 7.2.4. Gene Therapy

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 8. Europe Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 8.1.1. Antibody Deficiency

- 8.1.2. Cellular Immunodeficiency

- 8.1.3. Innate Immune Disorders

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Immunoglobulin Replacement Therapy

- 8.2.2. Stem Cell/Bone Marrow Transplantation

- 8.2.3. Antibiotic Therapy

- 8.2.4. Gene Therapy

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 9. Asia Pacific Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 9.1.1. Antibody Deficiency

- 9.1.2. Cellular Immunodeficiency

- 9.1.3. Innate Immune Disorders

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Immunoglobulin Replacement Therapy

- 9.2.2. Stem Cell/Bone Marrow Transplantation

- 9.2.3. Antibiotic Therapy

- 9.2.4. Gene Therapy

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 10. Middle East and Africa Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 10.1.1. Antibody Deficiency

- 10.1.2. Cellular Immunodeficiency

- 10.1.3. Innate Immune Disorders

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Immunoglobulin Replacement Therapy

- 10.2.2. Stem Cell/Bone Marrow Transplantation

- 10.2.3. Antibiotic Therapy

- 10.2.4. Gene Therapy

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 11. South America Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Disease Type

- 11.1.1. Antibody Deficiency

- 11.1.2. Cellular Immunodeficiency

- 11.1.3. Innate Immune Disorders

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Immunoglobulin Replacement Therapy

- 11.2.2. Stem Cell/Bone Marrow Transplantation

- 11.2.3. Antibiotic Therapy

- 11.2.4. Gene Therapy

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Disease Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Kedrion Biopharma Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 CSL Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Biotest AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Octapharma AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Takeda Pharmaceutical Company Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Lupin Pharmaceuticals*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Grifols S A

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LFB group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Baxter international Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Bio Products Laboratory Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Kedrion Biopharma Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Primary Immunodeficiency Therapeutics Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 3: North America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 4: North America Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 5: North America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 9: Europe Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 10: Europe Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 11: Europe Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: Europe Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Europe Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 15: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 16: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 17: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 19: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 21: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 22: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 23: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 24: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 27: South America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 28: South America Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 29: South America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: South America Primary Immunodeficiency Therapeutics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 31: South America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 2: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 3: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 5: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 6: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 11: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 12: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Germany Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: France Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Italy Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 17: Spain Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 19: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 20: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 21: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 22: China Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Japan Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: India Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Australia Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: South Korea Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 29: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 30: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: GCC Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: South Africa Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 35: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 36: Global Primary Immunodeficiency Therapeutics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 37: Brazil Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: Argentina Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Primary Immunodeficiency Therapeutics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Primary Immunodeficiency Therapeutics Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Primary Immunodeficiency Therapeutics Industry?

Key companies in the market include Kedrion Biopharma Inc, CSL Ltd, Biotest AG, Octapharma AG, Takeda Pharmaceutical Company Limited, Lupin Pharmaceuticals*List Not Exhaustive, Grifols S A, LFB group, Baxter international Inc, Bio Products Laboratory Limited.

3. What are the main segments of the Primary Immunodeficiency Therapeutics Industry?

The market segments include Disease Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Immunodeficiency diseases; Technological Advancements in Genetic Therapy.

6. What are the notable trends driving market growth?

Gene Therapy Segment is Expected to Hold a Major Market Share in the Primary Immunodeficiency Therapeutics Market.

7. Are there any restraints impacting market growth?

High Cost of the Therapies; Side Effects Associated with the Treatment.

8. Can you provide examples of recent developments in the market?

In September 2022, Lactiga Therapeutics raised USD 1.6 million in oversubscribed pre-seed financing for developing therapeutics for patients with primary immunodeficiency diseases.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Primary Immunodeficiency Therapeutics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Primary Immunodeficiency Therapeutics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Primary Immunodeficiency Therapeutics Industry?

To stay informed about further developments, trends, and reports in the Primary Immunodeficiency Therapeutics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence