Key Insights

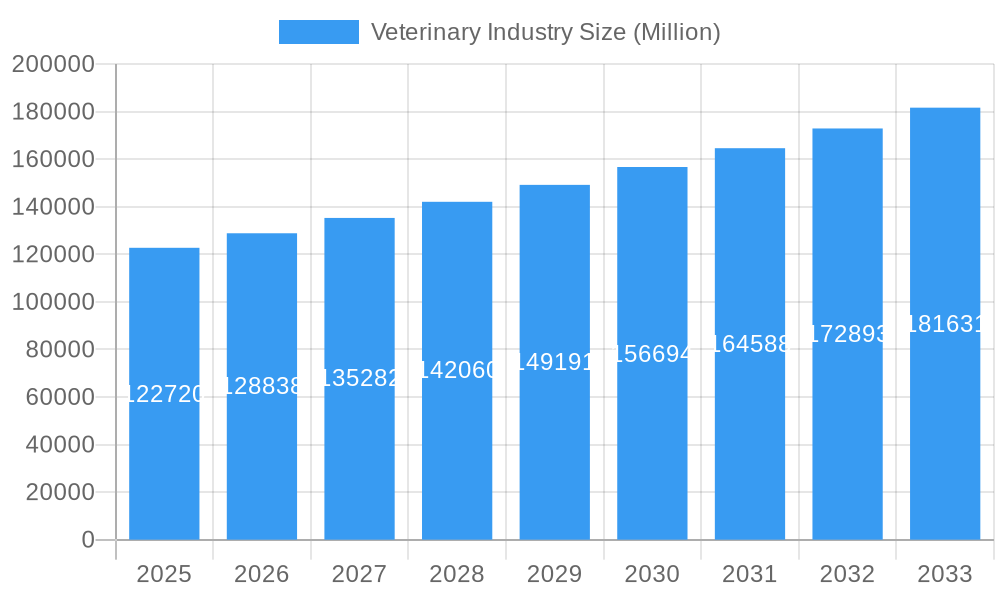

The global veterinary industry, valued at $122.72 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 4.90% from 2025 to 2033. This expansion is driven by several key factors. Increasing pet ownership globally, coupled with rising pet humanization—treating pets as family members—fuels demand for higher-quality veterinary care, including preventative services, advanced diagnostics, and specialized treatments. Technological advancements, such as telemedicine (remote veterinary consultations), sophisticated imaging technologies, and minimally invasive surgical techniques, are enhancing the quality and efficiency of veterinary services, further stimulating market growth. A growing middle class in emerging economies, particularly in Asia-Pacific, is also contributing to increased spending on animal healthcare. The market is segmented by service type (surgery, diagnostic tests and imaging, physical health monitoring, and other services) and animal type (companion animals and farm animals), with companion animals currently dominating the market share due to higher disposable income dedicated to pet care. Regulatory changes promoting animal welfare and stricter guidelines for animal health management are also influencing market dynamics. However, the industry faces challenges such as high veterinary care costs, which can act as a restraint, particularly for lower-income pet owners. Competition amongst established players and emerging veterinary startups is also intensifying.

Veterinary Industry Market Size (In Billion)

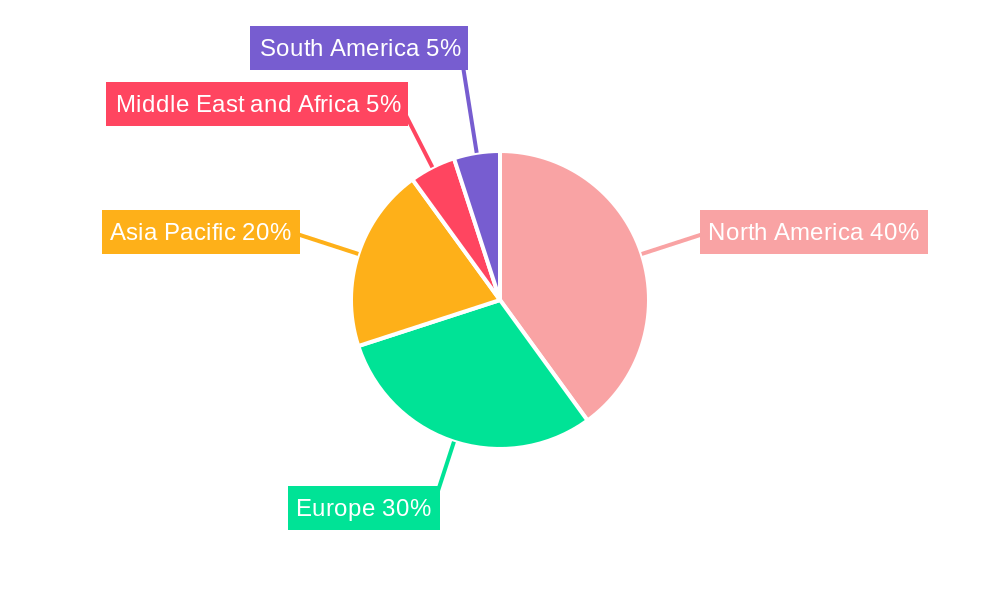

The future of the veterinary industry is bright, with continued growth expected across all segments and regions. North America and Europe currently hold the largest market shares, but rapid economic growth and increasing pet ownership in Asia-Pacific are expected to drive significant expansion in this region over the forecast period. Strategic partnerships and acquisitions are becoming increasingly common, with large corporations integrating technology and expanding their service offerings to cater to the evolving needs of pet owners and livestock farmers. Furthermore, an increasing focus on preventative care and personalized medicine for animals will further shape industry growth in the coming years. The development of innovative therapeutics and diagnostics will play a crucial role in maintaining this growth trajectory.

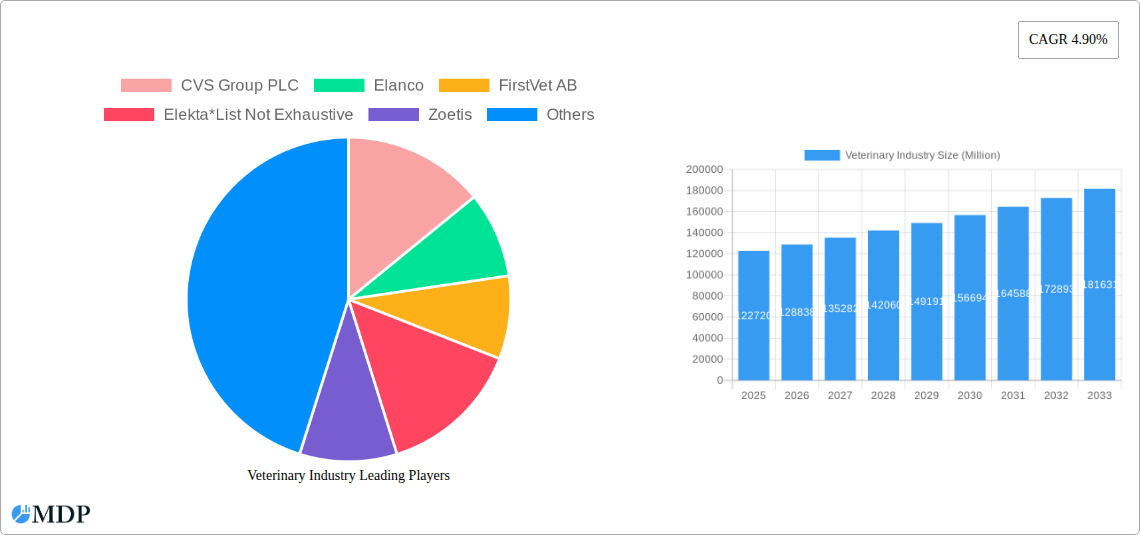

Veterinary Industry Company Market Share

Veterinary Industry Market Report: 2019-2033 Forecast

This comprehensive report provides a detailed analysis of the global veterinary industry, projecting a market value exceeding $XX Million by 2033. Uncover actionable insights into market dynamics, key players, emerging trends, and future growth opportunities. Ideal for investors, industry professionals, and strategic decision-makers seeking a competitive edge in this rapidly evolving sector. The report covers the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033.

Veterinary Industry Market Dynamics & Concentration

The global veterinary market, valued at $XX Million in 2024, exhibits a moderately consolidated structure with several multinational corporations and smaller regional players. Market share is largely influenced by company size, geographic reach, and product diversification. Key factors shaping market dynamics include:

- Innovation Drivers: Technological advancements in diagnostics, therapeutics, and surgical procedures drive significant market growth, creating demand for specialized services and advanced equipment. Examples include the introduction of minimally invasive surgical techniques and AI-powered diagnostic tools.

- Regulatory Frameworks: Government regulations concerning animal health, pharmaceutical approvals, and veterinary practice standards significantly impact market access and product development. Variations in regulations across different countries influence market entry strategies.

- Product Substitutes: While many veterinary products are specialized, the availability of alternative treatments and therapies exerts competitive pressure. Cost-effective alternatives can significantly affect market share dynamics.

- End-User Trends: Increasing pet ownership and rising awareness of animal welfare are major drivers. Owners are increasingly willing to invest in advanced treatments and premium care for their animals. Farm animal health is also a significant segment, shaped by production practices and disease prevention efforts.

- M&A Activities: Consolidation within the veterinary industry is evident through numerous mergers and acquisitions (M&As). The number of M&A deals during the historical period (2019-2024) totalled xx, indicating a significant level of industry consolidation. Large corporations are actively acquiring smaller companies to expand their market share and product portfolios. For example, the acquisition of [insert example of M&A deal if available] illustrates this trend. This activity contributes to an evolving market landscape and changes market shares.

Veterinary Industry Industry Trends & Analysis

The global veterinary market is experiencing dynamic and sustained growth, propelled by a confluence of influential factors. During the forecast period spanning from 2025 to 2033, the Compound Annual Growth Rate (CAGR) is projected to reach approximately xx%. This impressive expansion is underpinned by several key drivers:

- Market Growth Drivers: The escalating global pet ownership rates, coupled with an increased willingness among owners to invest significantly in the health and well-being of their companion animals, are primary catalysts. Furthermore, supportive government initiatives aimed at enhancing animal welfare programs and promoting disease prevention contribute to market expansion. Concurrently, continuous technological advancements are leading to the development of more sophisticated diagnostic tools and groundbreaking treatment options, thereby stimulating consistent demand across the sector.

- Technological Disruptions: The veterinary landscape is being profoundly reshaped by the integration of innovative technologies. The widespread adoption of telemedicine platforms is enhancing accessibility and convenience, while AI-powered diagnostic solutions are revolutionizing diagnostic accuracy. Advanced surgical techniques are not only improving treatment efficacy but also minimizing patient recovery times. These technological advancements collectively elevate the standard of patient care, boost market efficiency, and broaden the reach of veterinary services.

- Evolving Consumer Preferences: Modern pet owners are increasingly seeking premium and specialized veterinary care for their pets. There's a discernible shift towards proactive health management, including preventative care and early disease detection. This rising demand for higher quality, personalized services directly fuels revenue growth and encourages innovation within the veterinary industry.

- Competitive Dynamics: The veterinary market is characterized by a competitive environment featuring both established industry giants and agile emerging players. This vigorous competition serves as a powerful engine for innovation, leading to the development of novel products and services. It also contributes to cost efficiencies, making advanced veterinary care more accessible. While developed markets exhibit higher adoption rates for new technologies, the competitive landscape ensures a diverse and evolving range of offerings for consumers globally.

Leading Markets & Segments in Veterinary Industry

The companion animal segment dominates the veterinary market, primarily driven by increasing pet ownership and rising disposable incomes. Geographically, North America and Europe currently hold the largest market share, while Asia-Pacific is expected to witness significant growth in the coming years.

By Service:

- Surgery: Growing demand for specialized surgical procedures, including minimally invasive techniques, contributes to this segment's dominance.

- Diagnostic Tests and Imaging: Technological advancements, such as advanced imaging and molecular diagnostics, fuel growth in this segment.

- Physical Health Monitoring: Increased adoption of remote monitoring devices and preventative health measures drives growth.

- Other Services: This segment includes ancillary services such as grooming, boarding, and pet insurance, showing steady growth.

By Animal Type:

- Companion Animal: This segment accounts for a significant portion of the market revenue due to increased pet ownership and the willingness of owners to invest in pet healthcare.

- Farm Animal: This segment's growth is influenced by factors like livestock production levels, disease prevalence, and government regulations.

Key Drivers:

- Economic policies: Government subsidies and incentives for animal health initiatives drive market growth, particularly in developing countries.

- Infrastructure: Availability of veterinary clinics, diagnostic facilities, and skilled professionals directly influences market access and penetration.

Veterinary Industry Product Developments

Recent product innovations in the veterinary industry are strategically focused on elevating diagnostic precision, formulating more effective therapeutic solutions, and streamlining the delivery of veterinary care. Notable advancements include the development of sophisticated AI-powered diagnostic tools that can analyze medical data with remarkable accuracy, the refinement of minimally invasive surgical techniques that reduce patient trauma and recovery times, and the expansion of robust telemedicine platforms that enhance remote consultation and monitoring capabilities. These innovations collectively promise improved treatment outcomes, cost reductions for both practitioners and owners, and a significant expansion in the accessibility of high-quality veterinary services.

Key Drivers of Veterinary Industry Growth

Technological advancements, including AI-powered diagnostics and minimally invasive surgery, are driving significant growth. Rising pet ownership and increased disposable incomes are also major contributors. Government initiatives promoting animal welfare and preventative healthcare further stimulate market expansion. Examples include the Indian government’s investment in mobile veterinary clinics.

Challenges in the Veterinary Industry Market

The veterinary industry faces several significant challenges that can impact market dynamics and growth trajectories. Stringent regulatory frameworks governing drug approvals and the establishment of veterinary practice standards can present considerable hurdles for new market entrants and for companies seeking to expand their reach. Disruptions within global supply chains for veterinary products and essential services can lead to availability issues and unexpected cost increases. Moreover, the intensely competitive nature of the market, with numerous established companies and innovative startups vying for market share, exerts continuous pressure on profit margins. These combined factors can collectively act as impediments to market growth and affect overall profitability.

Emerging Opportunities in Veterinary Industry

Technological advancements, strategic partnerships, and market expansion into developing economies present significant opportunities for growth. The integration of AI and telemedicine offers opportunities for improved diagnostics and more convenient care. Strategic collaborations between veterinary clinics and pharmaceutical companies will further fuel market growth.

Leading Players in the Veterinary Industry Sector

- CVS Group PLC

- Elanco

- FirstVet AB

- Elekta

- Zoetis

- CityVet Inc

- Kremer Veterinary Services

- Ethos Veterinary Health

- Torigen Pharmaceuticals Inc

- Karyopharm Therapeutics Inc

- ELIAS Animal Health

- Greencross Limited

- Armor Animal Health (Animart)

- Mars Inc

- Idexx Laboratories

Key Milestones in Veterinary Industry Industry

- March 2022: Hacarus Inc. announced the successful launch of its innovative ECG platform in collaboration with DS Pharma Animal Health, a significant advancement in improving the detection and management of canine cardiac diseases.

- May 2022: The government of Andhra Pradesh initiated a vital program by launching 175 Mobile Ambulatory Veterinary Clinics. This initiative is designed to drastically improve the accessibility of veterinary services for animals in remote and underserved areas. The government has further outlined plans for an expansion to 340 clinics, aiming to amplify the reach and effectiveness of animal healthcare delivery across the state.

Strategic Outlook for Veterinary Industry Market

The veterinary industry is poised for continued growth, driven by technological innovation, rising pet ownership, and increased investment in animal healthcare. Strategic partnerships, expansion into underserved markets, and the development of novel therapies will be crucial for maximizing future market potential. The increasing integration of technology will transform the sector’s efficiency and accessibility.

Veterinary Industry Segmentation

-

1. Service

- 1.1. Surgery

- 1.2. Diagnostic Tests and Imaging

- 1.3. Physical Health Monitoring

- 1.4. Other Services

-

2. Animal Type

- 2.1. Companion Animal

- 2.2. Farm Animal

Veterinary Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Veterinary Industry Regional Market Share

Geographic Coverage of Veterinary Industry

Veterinary Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Surgery

- 5.1.2. Diagnostic Tests and Imaging

- 5.1.3. Physical Health Monitoring

- 5.1.4. Other Services

- 5.2. Market Analysis, Insights and Forecast - by Animal Type

- 5.2.1. Companion Animal

- 5.2.2. Farm Animal

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. Global Veterinary Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Surgery

- 6.1.2. Diagnostic Tests and Imaging

- 6.1.3. Physical Health Monitoring

- 6.1.4. Other Services

- 6.2. Market Analysis, Insights and Forecast - by Animal Type

- 6.2.1. Companion Animal

- 6.2.2. Farm Animal

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. North America Veterinary Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service

- 7.1.1. Surgery

- 7.1.2. Diagnostic Tests and Imaging

- 7.1.3. Physical Health Monitoring

- 7.1.4. Other Services

- 7.2. Market Analysis, Insights and Forecast - by Animal Type

- 7.2.1. Companion Animal

- 7.2.2. Farm Animal

- 7.1. Market Analysis, Insights and Forecast - by Service

- 8. Europe Veterinary Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service

- 8.1.1. Surgery

- 8.1.2. Diagnostic Tests and Imaging

- 8.1.3. Physical Health Monitoring

- 8.1.4. Other Services

- 8.2. Market Analysis, Insights and Forecast - by Animal Type

- 8.2.1. Companion Animal

- 8.2.2. Farm Animal

- 8.1. Market Analysis, Insights and Forecast - by Service

- 9. Asia Pacific Veterinary Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service

- 9.1.1. Surgery

- 9.1.2. Diagnostic Tests and Imaging

- 9.1.3. Physical Health Monitoring

- 9.1.4. Other Services

- 9.2. Market Analysis, Insights and Forecast - by Animal Type

- 9.2.1. Companion Animal

- 9.2.2. Farm Animal

- 9.1. Market Analysis, Insights and Forecast - by Service

- 10. Middle East and Africa Veterinary Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service

- 10.1.1. Surgery

- 10.1.2. Diagnostic Tests and Imaging

- 10.1.3. Physical Health Monitoring

- 10.1.4. Other Services

- 10.2. Market Analysis, Insights and Forecast - by Animal Type

- 10.2.1. Companion Animal

- 10.2.2. Farm Animal

- 10.1. Market Analysis, Insights and Forecast - by Service

- 11. South America Veterinary Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service

- 11.1.1. Surgery

- 11.1.2. Diagnostic Tests and Imaging

- 11.1.3. Physical Health Monitoring

- 11.1.4. Other Services

- 11.2. Market Analysis, Insights and Forecast - by Animal Type

- 11.2.1. Companion Animal

- 11.2.2. Farm Animal

- 11.1. Market Analysis, Insights and Forecast - by Service

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CVS Group PLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Elanco

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 FirstVet AB

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Elekta*List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Zoetis

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 CityVet Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Kremer Veterinary Services

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Ethos Veterinary Health

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Torigen Pharmaceuticals Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Karyopharm Therapeutics Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 ELIAS Animal Health

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Greencross Limited

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Armor Animal Health (Animart)

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Mars Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Idexx laboratories

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 CVS Group PLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Veterinary Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Veterinary Industry Revenue (Million), by Service 2025 & 2033

- Figure 3: North America Veterinary Industry Revenue Share (%), by Service 2025 & 2033

- Figure 4: North America Veterinary Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 5: North America Veterinary Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 6: North America Veterinary Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Veterinary Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Veterinary Industry Revenue (Million), by Service 2025 & 2033

- Figure 9: Europe Veterinary Industry Revenue Share (%), by Service 2025 & 2033

- Figure 10: Europe Veterinary Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 11: Europe Veterinary Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 12: Europe Veterinary Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Veterinary Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Veterinary Industry Revenue (Million), by Service 2025 & 2033

- Figure 15: Asia Pacific Veterinary Industry Revenue Share (%), by Service 2025 & 2033

- Figure 16: Asia Pacific Veterinary Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 17: Asia Pacific Veterinary Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 18: Asia Pacific Veterinary Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Veterinary Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Veterinary Industry Revenue (Million), by Service 2025 & 2033

- Figure 21: Middle East and Africa Veterinary Industry Revenue Share (%), by Service 2025 & 2033

- Figure 22: Middle East and Africa Veterinary Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 23: Middle East and Africa Veterinary Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 24: Middle East and Africa Veterinary Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Veterinary Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Veterinary Industry Revenue (Million), by Service 2025 & 2033

- Figure 27: South America Veterinary Industry Revenue Share (%), by Service 2025 & 2033

- Figure 28: South America Veterinary Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 29: South America Veterinary Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 30: South America Veterinary Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: South America Veterinary Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Veterinary Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 2: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 3: Global Veterinary Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Veterinary Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 5: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 6: Global Veterinary Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Veterinary Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 11: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 12: Global Veterinary Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Veterinary Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 20: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 21: Global Veterinary Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: China Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Australia Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Veterinary Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 29: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 30: Global Veterinary Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: GCC Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Africa Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Veterinary Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 35: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 36: Global Veterinary Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Brazil Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Argentina Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Veterinary Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Industry?

The projected CAGR is approximately 4.90%.

2. Which companies are prominent players in the Veterinary Industry?

Key companies in the market include CVS Group PLC, Elanco, FirstVet AB, Elekta*List Not Exhaustive, Zoetis, CityVet Inc, Kremer Veterinary Services, Ethos Veterinary Health, Torigen Pharmaceuticals Inc, Karyopharm Therapeutics Inc, ELIAS Animal Health, Greencross Limited, Armor Animal Health (Animart), Mars Inc, Idexx laboratories.

3. What are the main segments of the Veterinary Industry?

The market segments include Service, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 122.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Various Diseases in Animals; Rising Adoption of Animals; Growing Expenditure on Animals/Pets.

6. What are the notable trends driving market growth?

The Companion Animal Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

Shortage of Skilled Personnel; Increasing Cost of Veterinary Services.

8. Can you provide examples of recent developments in the market?

May 2022: The Chief Minister of Andhra Pradesh, Sri YS Jagan Mohan Reddy, officially launched 175 Mobile Ambulatory Veterinary Clinics (MAVCs) with an investment of Rs 278 crore. The state government planned to establish 340 Dr. YSR Sanchaara Pasu Aarogya Seva, or Mobile Ambulatory Veterinary Clinics (MAVC), in the state to improve the service delivery system and ensure that the veterinary services provided by the animal husbandry department are more easily accessible to the public.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Industry?

To stay informed about further developments, trends, and reports in the Veterinary Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence