Key Insights

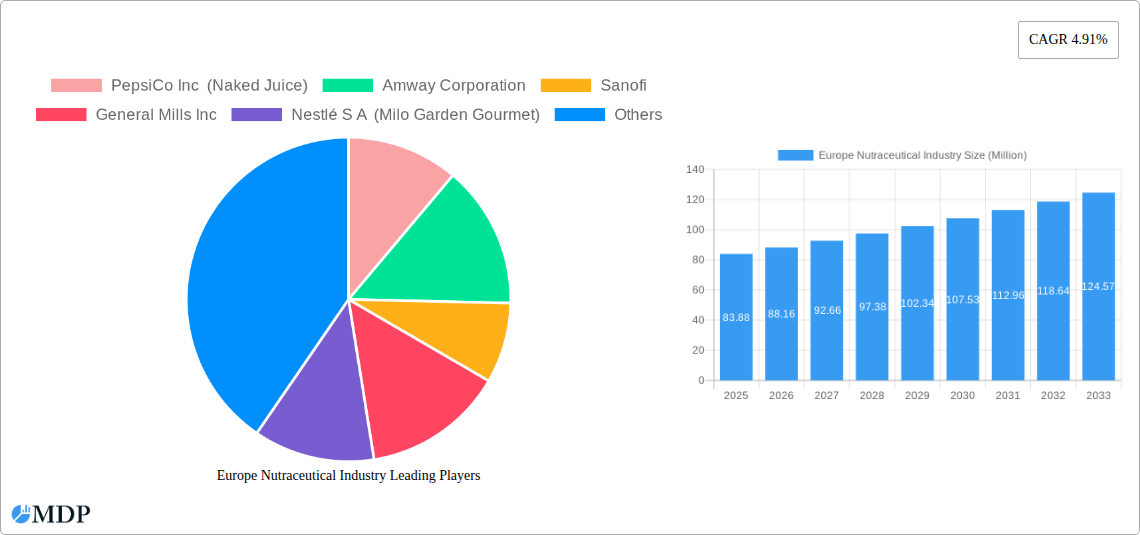

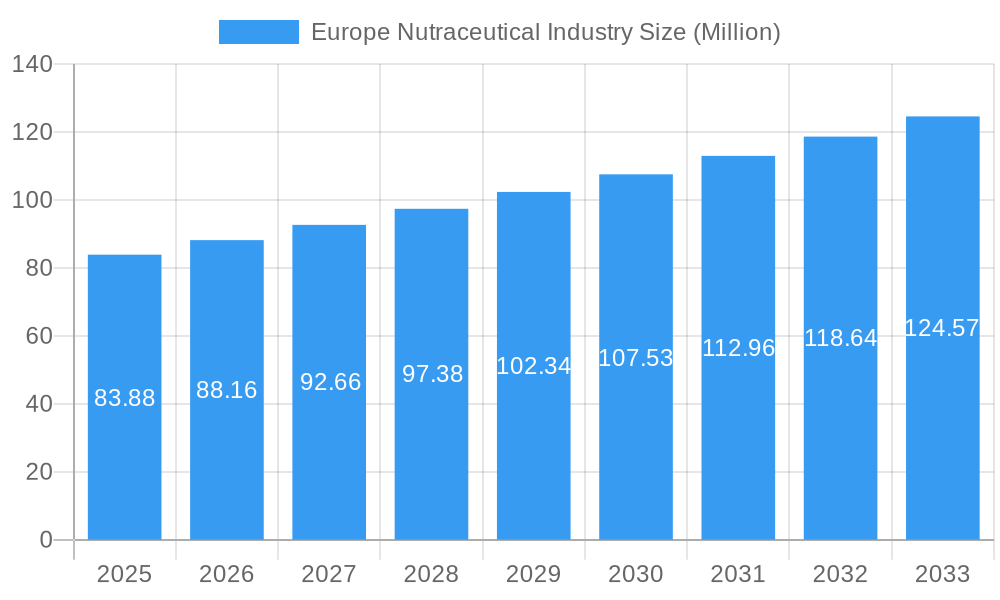

The European nutraceutical market, valued at €83.88 million in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 4.91% from 2025 to 2033. This expansion is fueled by several key drivers. A rising prevalence of chronic diseases like cardiovascular issues and diabetes is prompting consumers to proactively manage their health through dietary supplements and functional foods. Increasing health awareness, fueled by readily available online information and growing consumer interest in preventative healthcare, is significantly impacting purchasing decisions. The market is further boosted by the expanding availability of innovative products, incorporating advanced ingredients and formulations catering to specific health needs, such as improved gut health, cognitive function, and immune support. This trend is also driven by the development of more convenient delivery formats, such as powders, gummies, and functional beverages, appealing to a broader consumer base. Furthermore, a growing number of health-conscious individuals are actively seeking natural and organic options, leading to increased demand for products with clean labels and transparent sourcing. Major players like PepsiCo, Nestlé, and Amway are actively contributing to market growth through strategic product launches, acquisitions, and robust marketing strategies.

Europe Nutraceutical Industry Market Size (In Million)

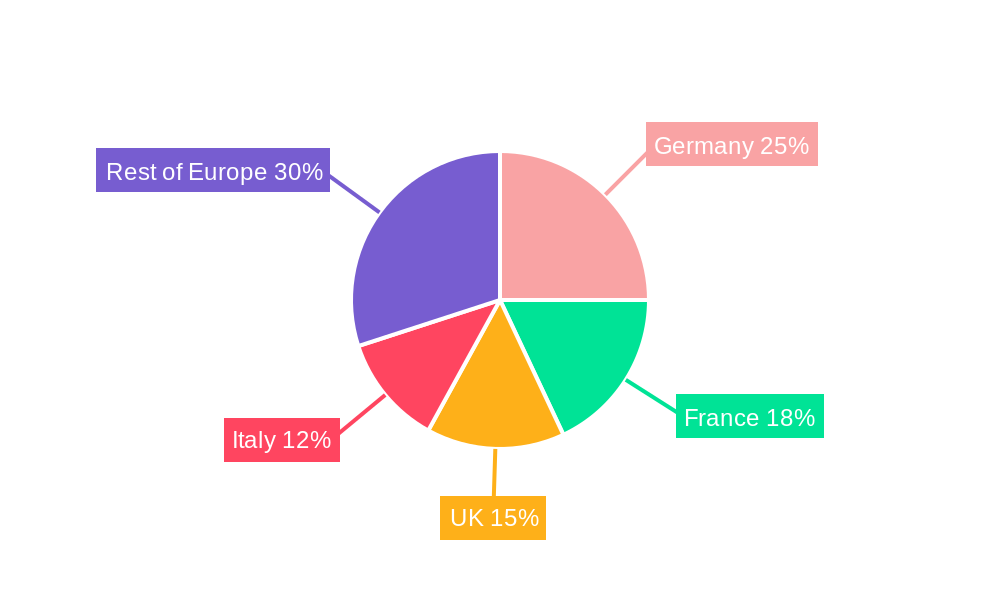

Despite this positive outlook, the market faces certain challenges. Stringent regulatory frameworks and labeling requirements across different European countries can complicate market entry and product development. Price sensitivity among consumers, particularly in economically challenging times, can impact sales of premium nutraceutical products. Furthermore, ensuring product quality and efficacy is paramount, with consumers demanding verifiable evidence of health benefits. The market segmentation is diverse, with functional foods and beverages leading the product category, and supermarkets/hypermarkets dominating the distribution channels. However, the online retail segment is experiencing significant growth as consumers increasingly shop for health products online. The projected growth across countries like Germany, France, the UK, and others within the EU reflects a burgeoning market with promising opportunities for existing and emerging players. Further diversification into specialized product segments and efficient digital marketing strategies will prove crucial in capitalizing on the market's potential.

Europe Nutraceutical Industry Company Market Share

This comprehensive report provides a detailed analysis of the Europe nutraceutical industry, covering market dynamics, trends, leading players, and future outlook. With a focus on the period 2019-2033 (base year 2025, forecast period 2025-2033), this report is an essential resource for industry stakeholders, investors, and market researchers seeking actionable insights into this dynamic sector. The report projects a market valued at xx Million by 2033, driven by significant growth factors and despite challenges.

Europe Nutraceutical Industry Market Dynamics & Concentration

This section analyzes the competitive landscape of the European nutraceutical market, encompassing market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and mergers & acquisitions (M&A) activities.

The European nutraceutical market exhibits a moderately concentrated structure, with several large multinational corporations holding significant market share. Key players like Nestlé S.A., PepsiCo Inc., and Sanofi contribute to this concentration. However, a considerable number of smaller, specialized companies also actively compete, particularly within niche segments. The market share of the top 5 players is estimated at xx%, indicating a competitive yet concentrated market.

Innovation Drivers:

- Growing consumer awareness of health and wellness.

- Technological advancements in product formulation and delivery systems.

- Increased focus on personalized nutrition solutions.

Regulatory Frameworks:

- Stringent regulations regarding labeling, claims, and safety standards.

- Varied regulatory landscapes across different European countries.

Product Substitutes:

- Competition from traditional food and beverage products.

- Emergence of alternative health and wellness solutions.

End-User Trends:

- Rising demand for convenient, functional food and beverages.

- Increasing preference for natural and organic products.

M&A Activities:

- The number of M&A deals in the sector increased significantly between 2019 and 2024, with xx deals recorded in the last five years, signifying consolidation within the industry and strategic expansion plans.

Europe Nutraceutical Industry Industry Trends & Analysis

The European nutraceutical market is witnessing robust growth, driven by several key factors. The market's CAGR from 2019 to 2024 is estimated at xx%, a projection that indicates a significant expansion. This growth is attributable to the confluence of consumer preference shifts, technological improvements, and favorable economic conditions.

Market Growth Drivers:

- Increased consumer spending on health and wellness products.

- Growing prevalence of chronic diseases and rising demand for preventative healthcare.

- Rising disposable incomes across Europe.

Technological Disruptions:

- Advancements in biotechnology leading to innovative product formulations.

- Expansion of e-commerce channels enhancing market accessibility.

Consumer Preferences:

- Strong preference for natural, organic, and plant-based ingredients.

- Growing interest in personalized nutrition.

Competitive Dynamics:

- Intense competition among established players and emerging companies.

- Focus on product innovation and differentiation.

- Strategic partnerships and alliances are becoming increasingly important. Market penetration is at xx% for leading brands in key segments.

Leading Markets & Segments in Europe Nutraceutical Industry

This section details the dominant regions, countries, and segments within the European nutraceutical industry, considering product type (Functional Food, Functional Beverage, Dietary Supplement) and distribution channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail Stores, Other Distribution Channels).

Dominant Region/Country: Western Europe, particularly Germany, France, and the UK, account for the largest share of the market due to higher consumer spending power, advanced healthcare infrastructure, and the presence of major industry players.

Dominant Segments:

- Product Type: Dietary supplements hold the largest market share, driven by a growing health-conscious population. Functional foods and beverages are also experiencing significant growth due to increasing demand for convenient and healthy options.

- Distribution Channel: Supermarkets/Hypermarkets constitute the most significant distribution channel, owing to widespread accessibility and established distribution networks. Online retail stores are rapidly gaining traction, reflecting the shift in consumer preferences toward online shopping.

Key Drivers of Segment Dominance:

- Economic Policies: Government initiatives promoting healthy lifestyles and supporting the nutraceutical industry.

- Infrastructure: Well-developed retail infrastructure and e-commerce logistics networks.

Europe Nutraceutical Industry Product Developments

Recent innovations in the European nutraceutical market encompass advanced delivery systems (e.g., liposomal encapsulation), personalized formulations based on genomics, and the incorporation of novel ingredients with demonstrable health benefits (e.g., adaptogens). These innovations target specific health concerns, and improve product efficacy and consumer acceptance. This focus on personalization and functional benefits caters directly to the evolving market needs.

Key Drivers of Europe Nutraceutical Industry Growth

Growth in the European nutraceutical industry is primarily driven by the increasing health awareness among consumers, the growing prevalence of chronic diseases, and the rise in disposable incomes. Supportive government regulations and initiatives further stimulate industry growth, encouraging innovation and investment.

Challenges in the Europe Nutraceutical Industry Market

The European nutraceutical market faces challenges, including stringent regulatory requirements impacting product approvals and launches. Supply chain complexities and fluctuations can affect ingredient sourcing and pricing. Furthermore, intense competition from established brands and new market entrants creates pressure on pricing and margins. The impact of these challenges on annual revenue growth is estimated at xx%, which is a quantifiable factor.

Emerging Opportunities in Europe Nutraceutical Industry

Significant opportunities exist in personalized nutrition, leveraging genomics and digital technologies to provide tailored solutions. Strategic collaborations between nutraceutical companies and healthcare providers are anticipated to expand market reach and improve product efficacy. Expansion into emerging markets in Eastern Europe presents further growth potential.

Leading Players in the Europe Nutraceutical Industry Sector

- PepsiCo Inc (Naked Juice)

- Amway Corporation

- Sanofi

- General Mills Inc

- Nestlé S A (Milo Garden Gourmet)

- Nutraceuticals Group

- The Coca-Cola Company (Aquarius)

- The Kraft Heinz Company

- The Kellogg's Company (Morningstar)

- Herbalife Nutrition U S

- Nature's Bounty Inc (Sundown Ester-C Solgar)

- Bioiberica

Key Milestones in Europe Nutraceutical Industry Industry

- October 2021: Nexira launched Heptura, a new hepatoprotection and detoxification ingredient.

- January 2022: DFE Pharma expanded its nutraceutical excipient offering with the Nutrofeli starch portfolio.

- April 2022: Bioiberica partnered with Apsen to develop innovative mobility products for the Brazilian market.

Strategic Outlook for Europe Nutraceutical Industry Market

The future of the European nutraceutical market appears promising, driven by the continued growth of health consciousness and rising demand for functional products. Companies focusing on innovation, personalization, and sustainable practices will be best positioned for success. Strategic partnerships and expansion into new markets will also play crucial roles in driving future growth.

Europe Nutraceutical Industry Segmentation

-

1. Product Type

- 1.1. Functional Food

- 1.2. Functional Beverage

- 1.3. Dietary Supplement

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Convenience Stores

- 2.3. Speciality Stores

- 2.4. Online Retail Stores

- 2.5. Other Distribution Channels

Europe Nutraceutical Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Nutraceutical Industry Regional Market Share

Geographic Coverage of Europe Nutraceutical Industry

Europe Nutraceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.91% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Functional Food

- 5.1.2. Functional Beverage

- 5.1.3. Dietary Supplement

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Speciality Stores

- 5.2.4. Online Retail Stores

- 5.2.5. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Europe Nutraceutical Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Functional Food

- 6.1.2. Functional Beverage

- 6.1.3. Dietary Supplement

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets/Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Speciality Stores

- 6.2.4. Online Retail Stores

- 6.2.5. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 PepsiCo Inc (Naked Juice)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Amway Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sanofi

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 General Mills Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Nestlé S A (Milo Garden Gourmet)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nutraceuticals Group*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 The Coca-Cola Company (Aquarius)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 The Kraft Heinz Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 The Kellogg's Company (Morningstar)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Herbalife Nutrition U S

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Nature's Bounty Inc (Sundown Ester-C Solgar)

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Bioiberica

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 PepsiCo Inc (Naked Juice)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Nutraceutical Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Nutraceutical Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Nutraceutical Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Europe Nutraceutical Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Europe Nutraceutical Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe Nutraceutical Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 5: Europe Nutraceutical Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Europe Nutraceutical Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: France Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Nutraceutical Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Nutraceutical Industry?

The projected CAGR is approximately 4.91%.

2. Which companies are prominent players in the Europe Nutraceutical Industry?

Key companies in the market include PepsiCo Inc (Naked Juice), Amway Corporation, Sanofi, General Mills Inc, Nestlé S A (Milo Garden Gourmet), Nutraceuticals Group*List Not Exhaustive, The Coca-Cola Company (Aquarius), The Kraft Heinz Company, The Kellogg's Company (Morningstar), Herbalife Nutrition U S, Nature's Bounty Inc (Sundown Ester-C Solgar), Bioiberica.

3. What are the main segments of the Europe Nutraceutical Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 83.88 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Consumption of Convenience Food in the Region; Increasing Demand for Gluten-free Pasta and Noodles.

6. What are the notable trends driving market growth?

Germany Dominates the Market.

7. Are there any restraints impacting market growth?

Growing Competition from Other Convenience Foods.

8. Can you provide examples of recent developments in the market?

April 2022: Bioiberica, a global life science company based in Spain, partnered with multinational health and pharmaceutical expert Apsen to develop innovative mobility products for the Brazilian market. Apsen's Motilex HA combines two of Bioiberica's leading joint health ingredients, b-2 Cool native type II collagen and Mobilee.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Nutraceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Nutraceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Nutraceutical Industry?

To stay informed about further developments, trends, and reports in the Europe Nutraceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence