Key Insights

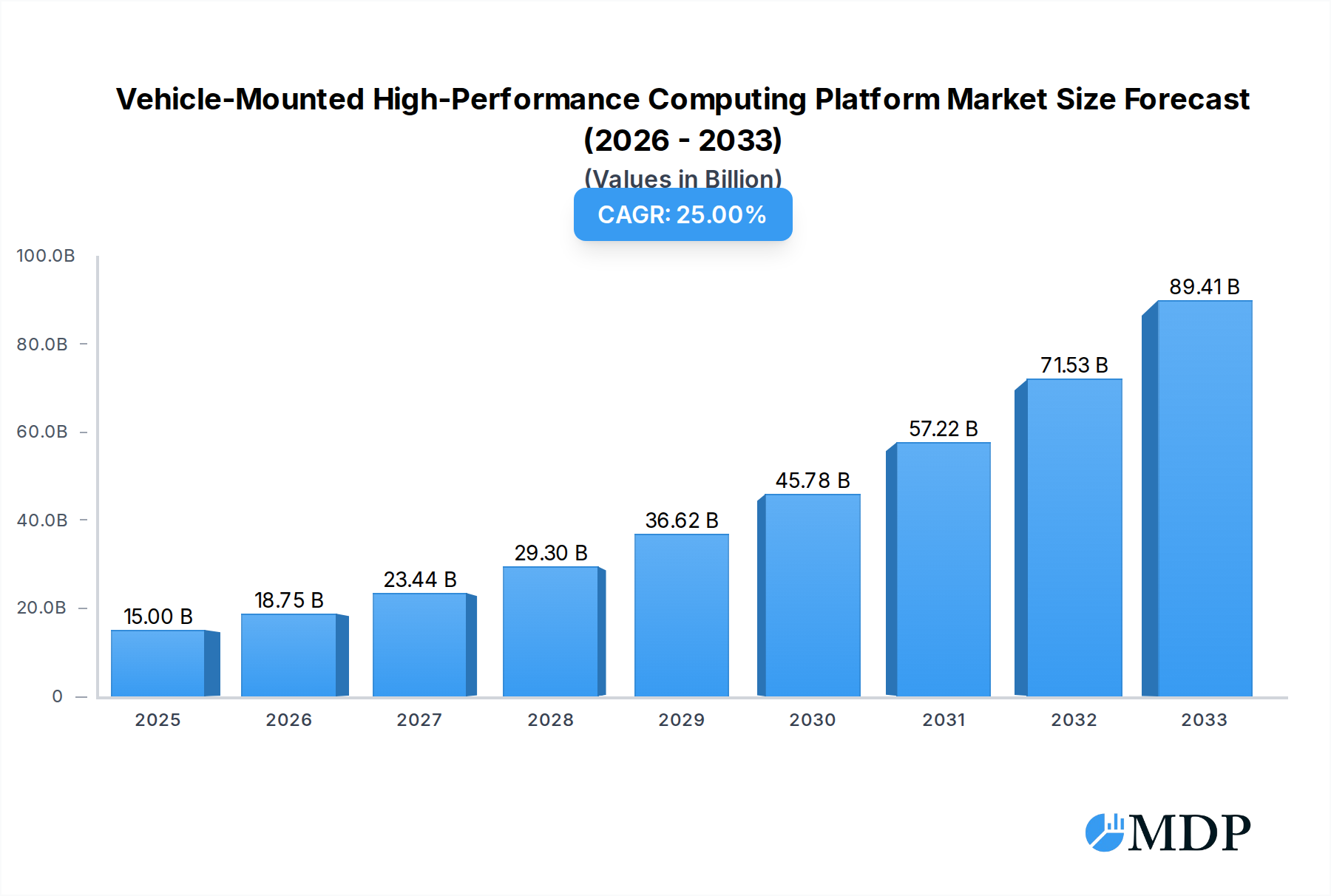

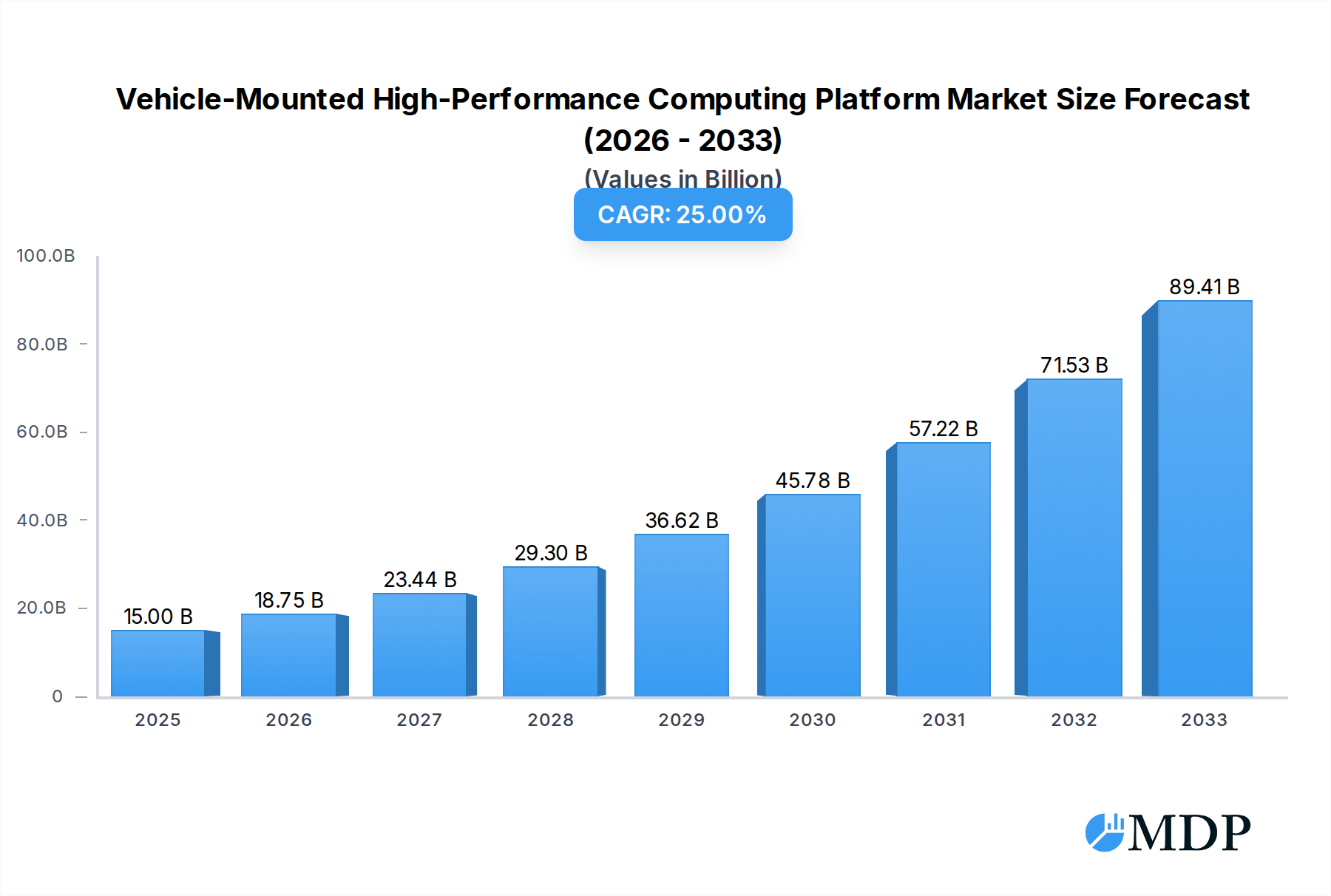

The global Vehicle-Mounted High-Performance Computing Platform market is poised for robust expansion, driven by the accelerating adoption of advanced driver-assistance systems (ADAS) and the nascent stages of autonomous driving. With a projected market size of $15 billion in 2025, the sector is expected to witness a remarkable CAGR of 25% throughout the forecast period of 2025-2033. This significant growth trajectory is primarily fueled by the increasing demand for sophisticated in-vehicle computing solutions capable of processing vast amounts of sensor data in real-time. Key applications are bifurcated between commercial and passenger vehicles, with hardware and software segmentation highlighting the integrated nature of these platforms. Leading technology giants and automotive suppliers like NVIDIA, Qualcomm, Mobileye, and Bosch are heavily investing in R&D, pushing the boundaries of processing power and artificial intelligence integration within vehicles. The trend towards software-defined vehicles, where computing capabilities are central to functionality and updates, further amplifies the market’s potential.

Vehicle-Mounted High-Performance Computing Platform Market Size (In Billion)

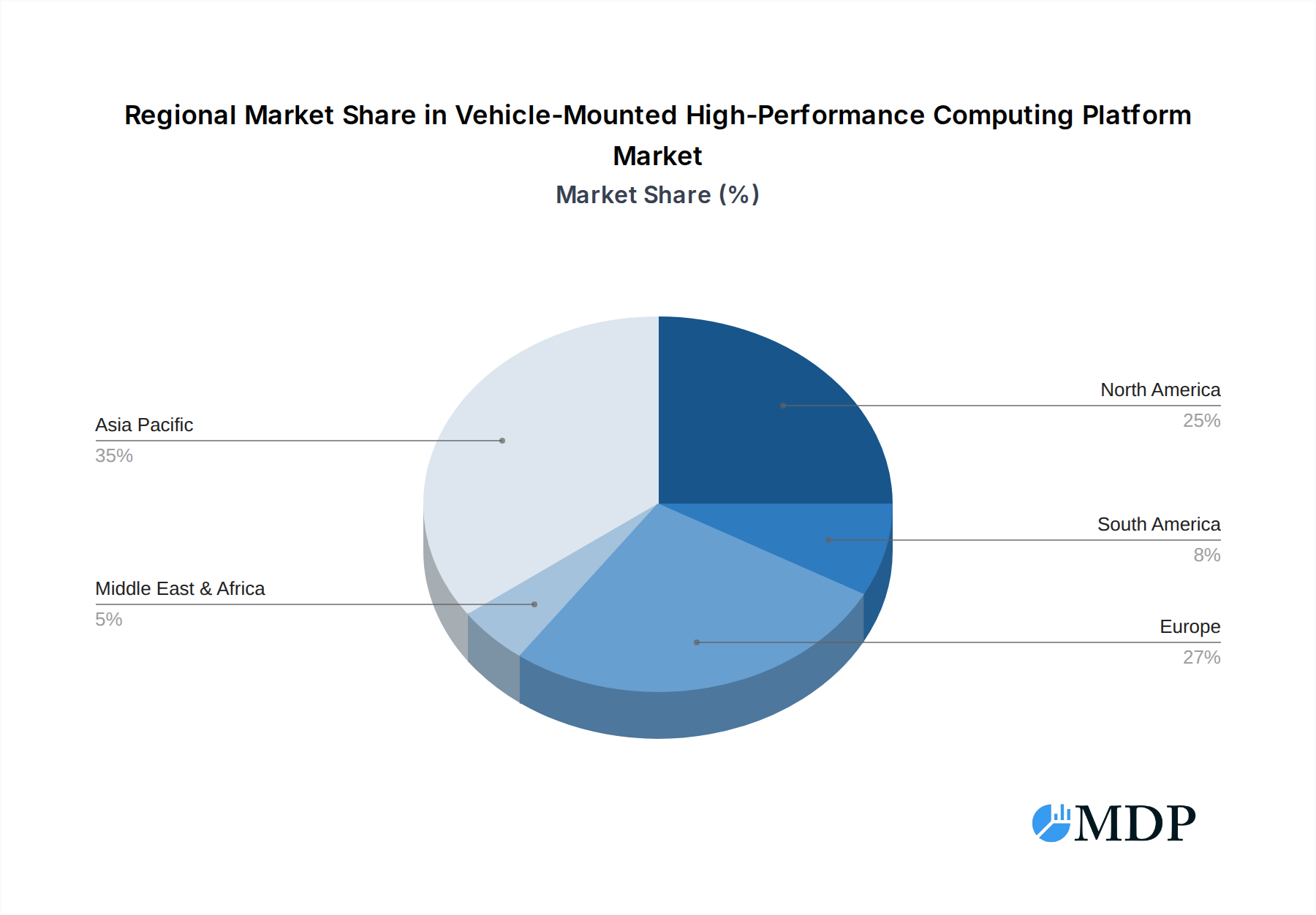

The market's dynamism is also shaped by significant trends such as the proliferation of 5G connectivity enabling vehicle-to-everything (V2X) communication, and the growing imperative for enhanced safety and convenience features. However, challenges such as the high cost of development and deployment, stringent regulatory hurdles, and cybersecurity concerns present potential restraints. Geographically, Asia Pacific, led by China and Japan, is expected to be a major growth engine due to its strong automotive manufacturing base and rapid technological adoption. North America and Europe are also critical markets, driven by advanced technological infrastructure and consumer demand for premium automotive features. The competitive landscape is characterized by intense innovation and strategic collaborations, with companies constantly striving to offer more powerful, efficient, and cost-effective computing solutions to meet the evolving needs of the automotive industry.

Vehicle-Mounted High-Performance Computing Platform Company Market Share

Vehicle-Mounted High-Performance Computing Platform Market: A Comprehensive Analysis (2019–2033)

Dive deep into the transformative landscape of Vehicle-Mounted High-Performance Computing (HPC) Platforms with this in-depth report. Spanning the study period of 2019–2033, with a base and estimated year of 2025, this report offers unparalleled insights into market dynamics, technological advancements, and strategic imperatives. Explore the critical role of HPC in the evolution of automotive technology, from advanced driver-assistance systems (ADAS) to fully autonomous driving and connected car services. This report is an essential resource for stakeholders seeking to navigate and capitalize on this rapidly expanding market.

Vehicle-Mounted High-Performance Computing Platform Market Dynamics & Concentration

The Vehicle-Mounted High-Performance Computing Platform market is characterized by a dynamic and evolving concentration, driven by intense innovation and strategic collaborations. Key players like NVIDIA, Qualcomm, Mobileye, Huawei, and Intel are at the forefront, investing billions in research and development to push the boundaries of in-vehicle processing power. The market's innovation drivers stem from the insatiable demand for advanced features such as AI-driven perception, real-time decision-making, and seamless connectivity. Regulatory frameworks, particularly those concerning safety standards for autonomous driving, are shaping platform development and market entry. Product substitutes, while nascent, are emerging, including centralized cloud-based computing architectures, though the latency and security benefits of on-board HPC remain significant. End-user trends, primarily driven by consumer desire for enhanced safety, convenience, and in-car infotainment, fuel the adoption of sophisticated HPC solutions. Mergers and acquisitions (M&A) activities, estimated to be in the hundreds over the historical period and projected to grow in the forecast period, are consolidating the market and fostering strategic synergies. For instance, the acquisition of Xilinx by AMD, though impacting the broader semiconductor landscape, signifies the strategic importance of specialized processing units for automotive applications. The market share of leading vendors is highly competitive, with continuous shifts based on technological breakthroughs and strategic partnerships, forming a complex web of alliances involving companies like Continental, Renesas, ZF, NXP, Baidu, Bosch, Aptiv, and Samsung. ThunderSoft, Desaysv, KOTEI, Neusoft, Navinfo, Jingwei HiRain, and Horizon are also actively contributing to this ecosystem through their specialized hardware and software solutions.

Vehicle-Mounted High-Performance Computing Platform Industry Trends & Analysis

The Vehicle-Mounted High-Performance Computing Platform industry is experiencing an unprecedented surge, driven by a confluence of technological advancements and evolving automotive needs. The projected Compound Annual Growth Rate (CAGR) is a robust xx%, signifying substantial expansion throughout the forecast period (2025–2033). This growth is intrinsically linked to the increasing complexity of automotive software and the burgeoning demand for sophisticated artificial intelligence (AI) capabilities within vehicles. The shift towards electric vehicles (EVs) and autonomous driving technologies are primary market growth drivers, necessitating powerful, energy-efficient computing solutions capable of processing vast amounts of sensor data in real-time. Technological disruptions, such as the advancement of AI accelerators, neural processing units (NPUs), and specialized automotive-grade System-on-Chips (SoCs), are fundamentally reshaping platform architectures. Companies like NVIDIA with their DRIVE platform, Qualcomm with their Snapdragon Ride, and Mobileye with their EyeQ chips are leading this technological revolution, offering integrated hardware and software solutions that accelerate development and deployment. Consumer preferences are increasingly leaning towards vehicles equipped with advanced safety features, enhanced infotainment systems, and personalized digital experiences, all of which are powered by high-performance computing. The market penetration of these advanced HPC solutions is projected to witness significant acceleration, moving from a modest percentage in the historical period (2019–2024) to a substantial portion of new vehicle production by 2033. Competitive dynamics are intensifying, with a battle for technological supremacy and market dominance. Strategic partnerships between semiconductor manufacturers, automotive OEMs, and software providers are becoming crucial. For instance, collaborations between chip giants like Intel and Xilinx with automotive Tier-1 suppliers like Bosch and Continental are creating integrated solutions that address the stringent requirements of the automotive industry. The increasing focus on data security and functional safety standards, such as ISO 26262, is also a significant factor shaping product development and market adoption. Furthermore, the evolution of 5G connectivity is enabling more sophisticated cloud-hybrid computing strategies, complementing on-board HPC capabilities for enhanced data processing and over-the-air (OTA) updates. The automotive industry's move towards software-defined vehicles is a paradigm shift, where computing power becomes a central differentiator, driving continued investment and innovation in vehicle-mounted HPC platforms.

Leading Markets & Segments in Vehicle-Mounted High-Performance Computing Platform

The global market for Vehicle-Mounted High-Performance Computing Platforms is experiencing robust growth, with certain regions and segments demonstrating particularly strong dominance. Asia-Pacific, spearheaded by China, is emerging as the leading market, fueled by the nation's aggressive push towards intelligent transportation systems, substantial investments in automotive R&D, and a burgeoning domestic automotive industry with companies like Huawei, Horizon, ThunderSoft, Desaysv, KOTEI, Neusoft, Navinfo, and Jingwei HiRain playing pivotal roles. Economic policies in countries like China, which prioritize the development of autonomous driving and connected vehicle technologies, are creating a fertile ground for HPC adoption. Furthermore, significant government incentives and the establishment of dedicated industrial parks for AI and automotive innovation are accelerating market penetration.

Within the application segment, Passenger Vehicles currently hold the largest market share and are projected to continue their dominance due to the sheer volume of production and the rapid integration of advanced driver-assistance systems (ADAS) and in-car entertainment systems. The demand for enhanced safety features, personalized digital experiences, and the increasing prevalence of premium and luxury vehicles equipped with sophisticated computing power are key drivers. However, the Commercial Vehicle segment is rapidly gaining traction and is expected to witness the highest growth rate. The adoption of autonomous trucking, advanced fleet management solutions, and the need for sophisticated diagnostic and telematics systems in logistics are propelling the demand for powerful HPC platforms in this sector.

In terms of types, the Hardware segment, encompassing advanced processors, GPUs, NPUs, and specialized automotive SoCs from industry giants like NVIDIA, Qualcomm, Intel, Xilinx, Renesas, and NXP, forms the foundational backbone of vehicle-mounted HPC. This segment is characterized by continuous innovation in terms of processing power, power efficiency, and functional safety certifications. The Software segment, including operating systems, middleware, AI algorithms, and development tools, is equally critical and is witnessing substantial growth. Companies like Baidu, with its Apollo platform, and Aptiv are at the forefront of developing comprehensive software stacks that enable the full potential of HPC hardware. The symbiotic relationship between hardware and software is crucial, with advancements in one driving progress in the other. For instance, the development of new AI models requires increasingly powerful hardware, while the availability of specialized hardware enables the deployment of more complex and performant software solutions. The strategic importance of these segments is further underscored by the active participation of Tier-1 suppliers such as Continental and Bosch, who integrate both hardware and software into their comprehensive automotive solutions.

Vehicle-Mounted High-Performance Computing Platform Product Developments

Product developments in Vehicle-Mounted High-Performance Computing Platforms are characterized by a relentless pursuit of increased processing power, enhanced energy efficiency, and robust safety features. Innovations focus on heterogeneous computing architectures, integrating CPUs, GPUs, and specialized AI accelerators like NPUs and TPUs to optimize performance for diverse automotive workloads, from sensor fusion to deep learning inference. Companies are developing automotive-grade SoCs that offer high performance within strict thermal and power envelopes. The integration of advanced memory technologies and high-speed interconnects further bolsters data throughput. Competitive advantages are derived from superior AI inference capabilities, advanced safety functionalities adhering to ISO 26262 standards, and scalable architectures that can support a range of applications from L2 ADAS to L4/L5 autonomous driving.

Key Drivers of Vehicle-Mounted High-Performance Computing Platform Growth

The growth of the Vehicle-Mounted High-Performance Computing Platform market is propelled by several critical factors. The relentless advancement of autonomous driving technology, demanding immense computational power for real-time decision-making and sensor data processing, is a primary catalyst. The increasing sophistication of in-car infotainment systems, connectivity features, and the emergence of the software-defined vehicle concept further escalate the need for powerful onboard computing. Government regulations and safety mandates pushing for advanced ADAS features and, eventually, higher levels of autonomy also play a crucial role. Economic factors, including rising consumer disposable income and the growing demand for premium vehicle features, indirectly contribute to the adoption of these advanced computing platforms.

Challenges in the Vehicle-Mounted High-Performance Computing Platform Market

Despite its promising trajectory, the Vehicle-Mounted High-Performance Computing Platform market faces significant challenges. Regulatory hurdles related to the safety validation and certification of complex AI systems for automotive applications remain a substantial barrier. Supply chain complexities and potential shortages of specialized semiconductors, as experienced in recent years, can disrupt production and drive up costs. Furthermore, the intense competitive pressure and the high cost of R&D for developing cutting-edge HPC solutions necessitate substantial investment and strategic foresight. The cybersecurity of these powerful computing platforms against evolving threats is another critical concern requiring continuous attention and robust solutions.

Emerging Opportunities in Vehicle-Mounted High-Performance Computing Platform

The Vehicle-Mounted High-Performance Computing Platform market is ripe with emerging opportunities. The expansion of 5G connectivity and edge computing will enable more sophisticated cloud-hybrid computing models, enhancing the capabilities of on-board HPC systems. Strategic partnerships between semiconductor manufacturers, AI software developers, and automotive OEMs are creating synergistic ecosystems that accelerate innovation and market adoption. The growing demand for personalized in-car experiences, advanced telematics, and over-the-air (OTA) updates presents further avenues for growth. The development of specialized HPC solutions for emerging mobility services, such as robotaxis and autonomous delivery vehicles, also represents a significant untapped market potential.

Leading Players in the Vehicle-Mounted High-Performance Computing Platform Sector

- NVIDIA

- Qualcomm

- Mobileye

- Huawei

- Horizon

- ThunderSoft

- Desaysv

- KOTEI

- Neusoft

- Navinfo

- Jingwei HiRain

- Continental

- Renesas

- ZF

- NXP

- Baidu

- Bosch

- Intel

- Xilinx

- Aptiv

- Samsung

Key Milestones in Vehicle-Mounted High-Performance Computing Platform Industry

- 2019: NVIDIA launches the DRIVE AGX Xavier, a powerful AI compute platform for autonomous vehicles.

- 2020: Qualcomm introduces its Snapdragon Ride platform, targeting autonomous driving and ADAS.

- 2021: Mobileye announces its EyeQ Ultra system-on-chip, designed for fully autonomous driving.

- 2022: Huawei showcases its Ascend AI processor series for automotive applications.

- 2022: Continental and Intel announce a strategic partnership for autonomous driving solutions.

- 2023: Renesas acquires Mobileye's former competitor, Syntiant, to bolster its AI capabilities.

- 2023: Baidu's Apollo platform continues to expand its ecosystem and adoption.

- 2024: Industry-wide discussions intensify regarding the integration of Level 4/5 autonomous driving hardware.

Strategic Outlook for Vehicle-Mounted High-Performance Computing Platform Market

The strategic outlook for the Vehicle-Mounted High-Performance Computing Platform market is exceptionally bright, driven by the accelerating pace of automotive innovation and the transformative potential of intelligent vehicles. Growth accelerators include the continued push towards autonomous driving, the proliferation of connected car services, and the increasing demand for sophisticated in-cabin digital experiences. Strategic opportunities lie in forging deeper collaborations between hardware and software providers to create fully integrated, end-to-end solutions. Furthermore, a focus on developing scalable and future-proof architectures that can adapt to evolving technological landscapes and regulatory requirements will be crucial for long-term success. The market is poised for substantial expansion, offering significant value creation for companies that can effectively navigate its complexities.

Vehicle-Mounted High-Performance Computing Platform Segmentation

-

1. Application

- 1.1. Commercial Vehicle

- 1.2. Passenger Vehicle

-

2. Types

- 2.1. Hardware

- 2.2. Software

Vehicle-Mounted High-Performance Computing Platform Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Vehicle-Mounted High-Performance Computing Platform Regional Market Share

Geographic Coverage of Vehicle-Mounted High-Performance Computing Platform

Vehicle-Mounted High-Performance Computing Platform REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Vehicle-Mounted High-Performance Computing Platform Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicle

- 5.1.2. Passenger Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Hardware

- 5.2.2. Software

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Vehicle-Mounted High-Performance Computing Platform Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicle

- 6.1.2. Passenger Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Hardware

- 6.2.2. Software

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Vehicle-Mounted High-Performance Computing Platform Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicle

- 7.1.2. Passenger Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Hardware

- 7.2.2. Software

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Vehicle-Mounted High-Performance Computing Platform Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicle

- 8.1.2. Passenger Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Hardware

- 8.2.2. Software

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicle

- 9.1.2. Passenger Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Hardware

- 9.2.2. Software

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Vehicle-Mounted High-Performance Computing Platform Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicle

- 10.1.2. Passenger Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Hardware

- 10.2.2. Software

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 NVIDIA

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Qualcomm

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Mobileye

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Huawei

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Horizon

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ThunderSoft

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Desaysv

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 KOTEI

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Neusoft

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Navinfo

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jingwei HiRain

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Continental

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Renesas

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 ZF

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 NXP

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Baidu

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Bosch

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Intel

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Xilinx

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Aptiv

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Samsung

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 NVIDIA

List of Figures

- Figure 1: Global Vehicle-Mounted High-Performance Computing Platform Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Vehicle-Mounted High-Performance Computing Platform Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Vehicle-Mounted High-Performance Computing Platform Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Vehicle-Mounted High-Performance Computing Platform Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Vehicle-Mounted High-Performance Computing Platform Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vehicle-Mounted High-Performance Computing Platform?

The projected CAGR is approximately 25%.

2. Which companies are prominent players in the Vehicle-Mounted High-Performance Computing Platform?

Key companies in the market include NVIDIA, Qualcomm, Mobileye, Huawei, Horizon, ThunderSoft, Desaysv, KOTEI, Neusoft, Navinfo, Jingwei HiRain, Continental, Renesas, ZF, NXP, Baidu, Bosch, Intel, Xilinx, Aptiv, Samsung.

3. What are the main segments of the Vehicle-Mounted High-Performance Computing Platform?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vehicle-Mounted High-Performance Computing Platform," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vehicle-Mounted High-Performance Computing Platform report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vehicle-Mounted High-Performance Computing Platform?

To stay informed about further developments, trends, and reports in the Vehicle-Mounted High-Performance Computing Platform, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence