Key Insights

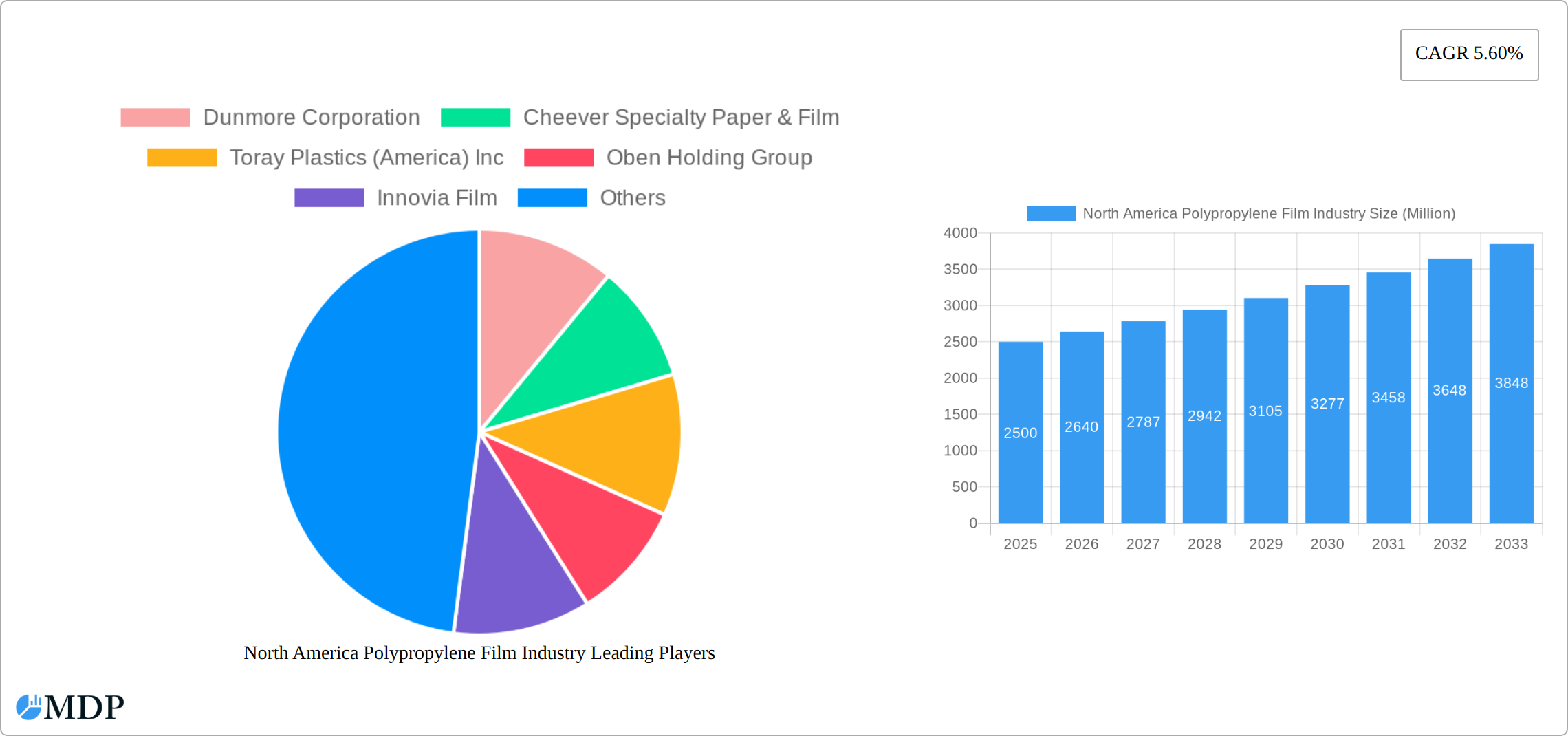

The North American polypropylene film market, valued at approximately $XX million in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 5.60% from 2025 to 2033. This expansion is fueled by several key factors. The burgeoning food and beverage industry, demanding flexible and durable packaging solutions, significantly contributes to market demand. Similarly, the pharmaceuticals and medical sectors rely heavily on polypropylene films for their barrier properties and sterility, further boosting market growth. Increasing consumer preference for convenient, ready-to-eat meals and single-serving packages also drives demand. Technological advancements in film production, leading to improved strength, clarity, and barrier properties, are also contributing factors. The United States constitutes the largest market segment within North America, followed by Canada. The presence of established players like Dunmore Corporation, Cheever Specialty Paper & Film, and Toray Plastics (America) Inc., alongside emerging companies, fosters competition and innovation, driving further market expansion.

However, the market faces certain challenges. Fluctuations in raw material prices, particularly polypropylene resin, can impact profitability. Growing environmental concerns regarding plastic waste and the increasing emphasis on sustainable packaging solutions necessitate the development and adoption of eco-friendly alternatives. These factors present opportunities for innovation within the industry, focusing on biodegradable and compostable polypropylene film options. Furthermore, regulatory changes concerning food safety and packaging standards also impact the market dynamics. Despite these restraints, the long-term outlook for the North American polypropylene film market remains positive, projecting continued growth fueled by the factors mentioned above and increasing demand from diverse end-use sectors across the region. The market's growth will likely be further fueled by the increasing adoption of advanced packaging technologies and the expansion of e-commerce, which both increase demand for flexible packaging materials.

North America Polypropylene Film Industry: Market Analysis & Forecast (2019-2033)

This comprehensive report provides an in-depth analysis of the North American polypropylene film industry, offering crucial insights for stakeholders seeking to navigate this dynamic market. The study covers the period from 2019 to 2033, with a focus on 2025 as the base and estimated year. We project a robust market expansion, revealing significant opportunities and challenges for industry players. This report leverages data-driven analysis to predict future trends and offer actionable recommendations.

North America Polypropylene Film Industry Market Dynamics & Concentration

The North American polypropylene film market is characterized by a moderately consolidated landscape, featuring prominent entities such as Dunmore Corporation, Cheever Specialty Paper & Film, Toray Plastics (America) Inc, Oben Holding Group, Innovia Film, Cosmo Films Inc, Copol International Ltd, Taghleef Industries, and Inteplast Group, all holding substantial market influence. While precise market share data remains proprietary, industry estimates for 2024 indicate that the top five players collectively command an approximate market share of 65%. The sector's innovation trajectory is heavily influenced by the increasing demand for films with superior barrier properties, a growing emphasis on sustainable alternatives like bio-based films, and the development of specialized film structures for distinct, high-value applications. Regulatory frameworks, particularly those pertaining to food safety standards and environmental sustainability, play a pivotal role in shaping market strategies. Competition from substitute materials, including polyethylene films and a diverse range of alternative packaging solutions, presents ongoing challenges. However, polypropylene's inherent versatility, combined with its cost-effectiveness, continues to solidify its strong market positioning. The industry has witnessed a moderate pace of merger and acquisition (M&A) activity over the recent past, with approximately 15-20 significant and minor transactions recorded between 2019 and 2024. A dominant end-user trend revolves around the escalating demand for sustainable and easily recyclable packaging solutions, which is directly impacting and guiding product development initiatives across the industry.

North America Polypropylene Film Industry Industry Trends & Analysis

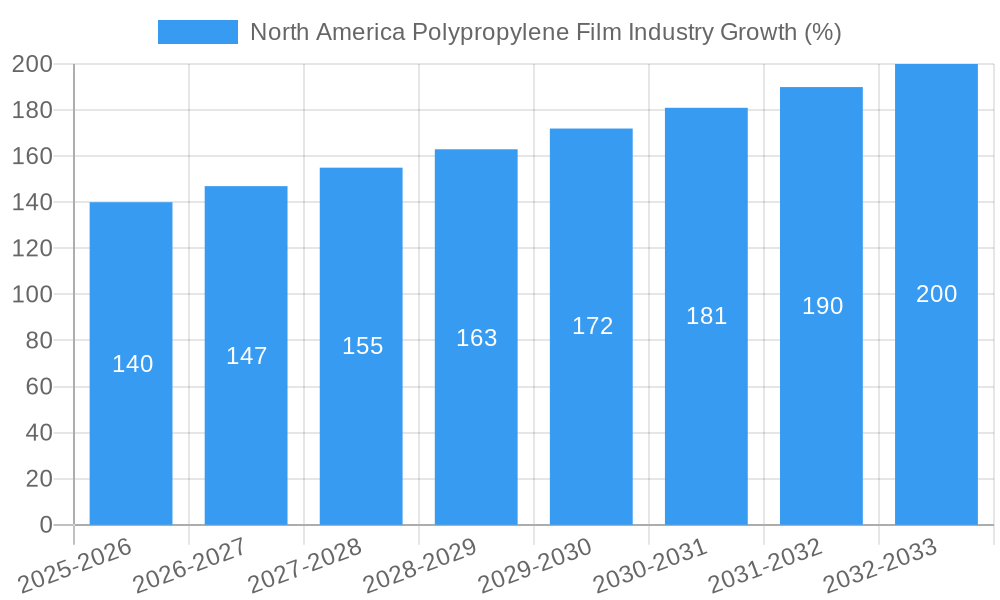

The North American polypropylene film market experienced a CAGR of approximately 4.5% during the historical period (2019-2024). This growth is primarily fueled by expanding demand across diverse end-user verticals, particularly in food packaging, driven by rising disposable incomes and changing consumer preferences. Technological advancements, such as the development of multilayer films with enhanced barrier properties and improved processing techniques, are further stimulating market expansion. The market penetration of bio-based and recyclable polypropylene films is steadily increasing, driven by growing environmental concerns and stricter regulations. Competitive dynamics are shaped by pricing strategies, product differentiation, and innovation, with larger players leveraging their scale to secure market share while smaller companies focus on niche applications and specialized products. The projected CAGR for the forecast period (2025-2033) is estimated to be around 5%, reflecting the continuous growth anticipated in key market segments.

Leading Markets & Segments in North America Polypropylene Film Industry

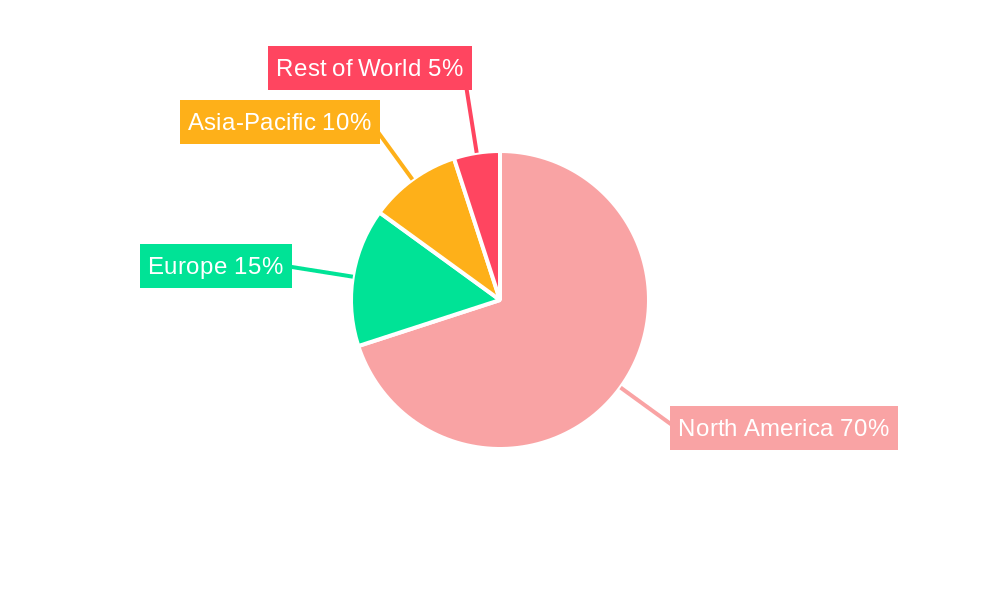

The United States stands as the preeminent market within North America for polypropylene films, capturing an estimated 85% of the total market value in 2024. This dominance is underpinned by a robust and expansive manufacturing base, sophisticated processing infrastructure, and a substantial domestic consumer demand, particularly in the packaging sector. Canada accounts for the remaining 15% of the market share. Within the diverse array of end-user verticals, the food and beverage sector emerges as the most significant segment, contributing approximately 40% to the total consumption. This strong performance is directly attributable to the widespread and indispensable use of polypropylene films in various food packaging applications.

Key Drivers for US Market Dominance:

- A highly developed and extensive domestic manufacturing capacity for polypropylene films.

- A well-established and efficient network of distribution channels and supply chains.

- Sustained high levels of consumer spending, particularly within the food and beverage sector, driving demand for packaging.

- A generally favorable and supportive regulatory environment that facilitates business operations and innovation.

Key Drivers for the Food & Beverage Segment Dominance:

- Exceptional and growing demand for flexible and adaptable packaging materials.

- The inherent and superior barrier properties of polypropylene films, crucial for product preservation and shelf life.

- A significant cost-effectiveness advantage when compared to many other specialized packaging solutions.

- Remarkable versatility, making it suitable for a wide spectrum of packaging formats, including pouches, wrappers, and labels.

North America Polypropylene Film Industry Product Developments

Recent product innovations focus on enhancing barrier properties, improving recyclability, and developing specialized film structures for specific applications. Multilayer films with enhanced oxygen and moisture barriers are gaining traction in food packaging. Bio-based and compostable polypropylene films are emerging as sustainable alternatives, catering to growing environmental concerns. These developments reflect the industry’s response to consumer preferences for sustainable and high-performance packaging solutions, creating a competitive advantage for companies investing in R&D.

Key Drivers of North America Polypropylene Film Industry Growth

Several factors are driving the growth of the North American polypropylene film industry. Firstly, the rising demand from the food and beverage sectors, coupled with the expanding industrial sector fuels substantial market growth. Secondly, advancements in film technology continue to provide better barrier properties and functionality, extending market reach. Finally, government initiatives promoting sustainable packaging solutions stimulate the adoption of eco-friendly polypropylene film alternatives.

Challenges in the North America Polypropylene Film Industry Market

The North American polypropylene film industry is navigating a landscape fraught with several significant challenges. Fluctuations in the prices of raw materials, such as propylene, can exert considerable pressure on profit margins. Concurrently, rising energy costs associated with production processes add another layer of operational expense. The market is also characterized by intense competition, both from established players and emerging entrants, often leading to price pressures. Furthermore, global supply chain disruptions, which have been amplified by geopolitical events and unforeseen circumstances, continue to impact production schedules, material availability, and timely delivery, thereby affecting overall profitability. Increasingly stringent environmental regulations, particularly those focused on promoting circular economy principles and sustainable packaging, necessitate substantial investments in research, development, and the adoption of eco-friendly film alternatives, potentially leading to increased production costs in the short to medium term. Overcoming these multifaceted challenges requires a concerted effort towards innovative solutions, strategic adaptation, and collaborative industry efforts.

Emerging Opportunities in North America Polypropylene Film Industry

The industry anticipates growth through several opportunities. Expansion into specialized niche markets, like pharmaceuticals and medical applications, offers significant potential. Strategic partnerships focused on developing sustainable and innovative materials are key. Moreover, exploring new applications in sectors such as electronics and consumer goods can significantly diversify revenue streams.

Leading Players in the North America Polypropylene Film Industry Sector

- Dunmore Corporation

- Cheever Specialty Paper & Film

- Toray Plastics (America) Inc

- Oben Holding Group

- Innovia Film

- Cosmo Films Inc

- Copol International Ltd

- Taghleef Industries

- Inteplast Group

Key Milestones in North America Polypropylene Film Industry Industry

- 2020: A notable year where several key industry players publicly announced significant investments and strategic initiatives aimed at developing and expanding their portfolio of sustainable packaging solutions, signaling a shift towards environmental responsibility.

- 2021: The industry witnessed an intensified focus on enhancing the recyclability and compostability of polypropylene films, driven by regulatory pressures and growing consumer demand for more environmentally friendly packaging options.

- 2022: A period marked by increased consolidation within the market, as several mergers and acquisitions (M&A) took place, aimed at optimizing operational efficiencies, expanding market reach, and consolidating market share among leading companies.

- 2023: The introduction of novel and advanced film structures, boasting significantly enhanced barrier properties, was a key development, catering to specialized application needs and improving product protection and shelf-life.

- 2024: This year is characterized by strategic expansions in production capacity across several key manufacturers, a proactive response to meet the escalating and sustained demand for polypropylene films driven by various end-user industries.

Strategic Outlook for North America Polypropylene Film Industry Market

The North American polypropylene film industry is poised for substantial long-term growth, driven by evolving market demands and technological advancements. Strategic investments in cutting-edge research and development (R&D), coupled with an unwavering commitment to sustainability and product innovation, will be paramount for sustained success and competitive advantage. Companies that effectively focus on developing specialized film solutions for niche applications and delivering highly customized product offerings are anticipated to gain a significant edge in the market. The future trajectory of this market will be largely shaped by the industry's ability to adeptly adapt to shifting consumer preferences, navigate increasingly stringent regulatory landscapes, and effectively manage the volatility of raw material prices. Embracing a proactive and forward-thinking approach to innovation, encompassing both technological advancements and sustainable practices, will be critical for maximizing returns and securing a robust market position in the coming years.

North America Polypropylene Film Industry Segmentation

-

1. End-User Vertical

- 1.1. Food

- 1.2. Beverage

- 1.3. Industrial

- 1.4. Pharmaceuticals & Medical

- 1.5. Other End-User Verticals

North America Polypropylene Film Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Polypropylene Film Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Cost-Effectiveness Of The Outsourcing; Access to the advanced technologies and expertise

- 3.3. Market Restrains

- 3.3.1. Monitoring issues and lack of standardization

- 3.4. Market Trends

- 3.4.1. Food Industry to Hold Major Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Polypropylene Film Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 5.1.1. Food

- 5.1.2. Beverage

- 5.1.3. Industrial

- 5.1.4. Pharmaceuticals & Medical

- 5.1.5. Other End-User Verticals

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 6. United States North America Polypropylene Film Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Polypropylene Film Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Polypropylene Film Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Polypropylene Film Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Dunmore Corporation

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Cheever Specialty Paper & Film

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Toray Plastics (America) Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Oben Holding Group

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Innovia Film

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Cosmo Films Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Copol International Ltd

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Taghleef Industries

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Inteplast Group

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.1 Dunmore Corporation

List of Figures

- Figure 1: North America Polypropylene Film Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Polypropylene Film Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Polypropylene Film Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Polypropylene Film Industry Revenue Million Forecast, by End-User Vertical 2019 & 2032

- Table 3: North America Polypropylene Film Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: North America Polypropylene Film Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: United States North America Polypropylene Film Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Canada North America Polypropylene Film Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Mexico North America Polypropylene Film Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Rest of North America North America Polypropylene Film Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: North America Polypropylene Film Industry Revenue Million Forecast, by End-User Vertical 2019 & 2032

- Table 10: North America Polypropylene Film Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: United States North America Polypropylene Film Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Canada North America Polypropylene Film Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Mexico North America Polypropylene Film Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Polypropylene Film Industry?

The projected CAGR is approximately 5.60%.

2. Which companies are prominent players in the North America Polypropylene Film Industry?

Key companies in the market include Dunmore Corporation, Cheever Specialty Paper & Film, Toray Plastics (America) Inc, Oben Holding Group, Innovia Film, Cosmo Films Inc, Copol International Ltd, Taghleef Industries, Inteplast Group.

3. What are the main segments of the North America Polypropylene Film Industry?

The market segments include End-User Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Cost-Effectiveness Of The Outsourcing; Access to the advanced technologies and expertise.

6. What are the notable trends driving market growth?

Food Industry to Hold Major Share.

7. Are there any restraints impacting market growth?

Monitoring issues and lack of standardization.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Polypropylene Film Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Polypropylene Film Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Polypropylene Film Industry?

To stay informed about further developments, trends, and reports in the North America Polypropylene Film Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence