Key Insights

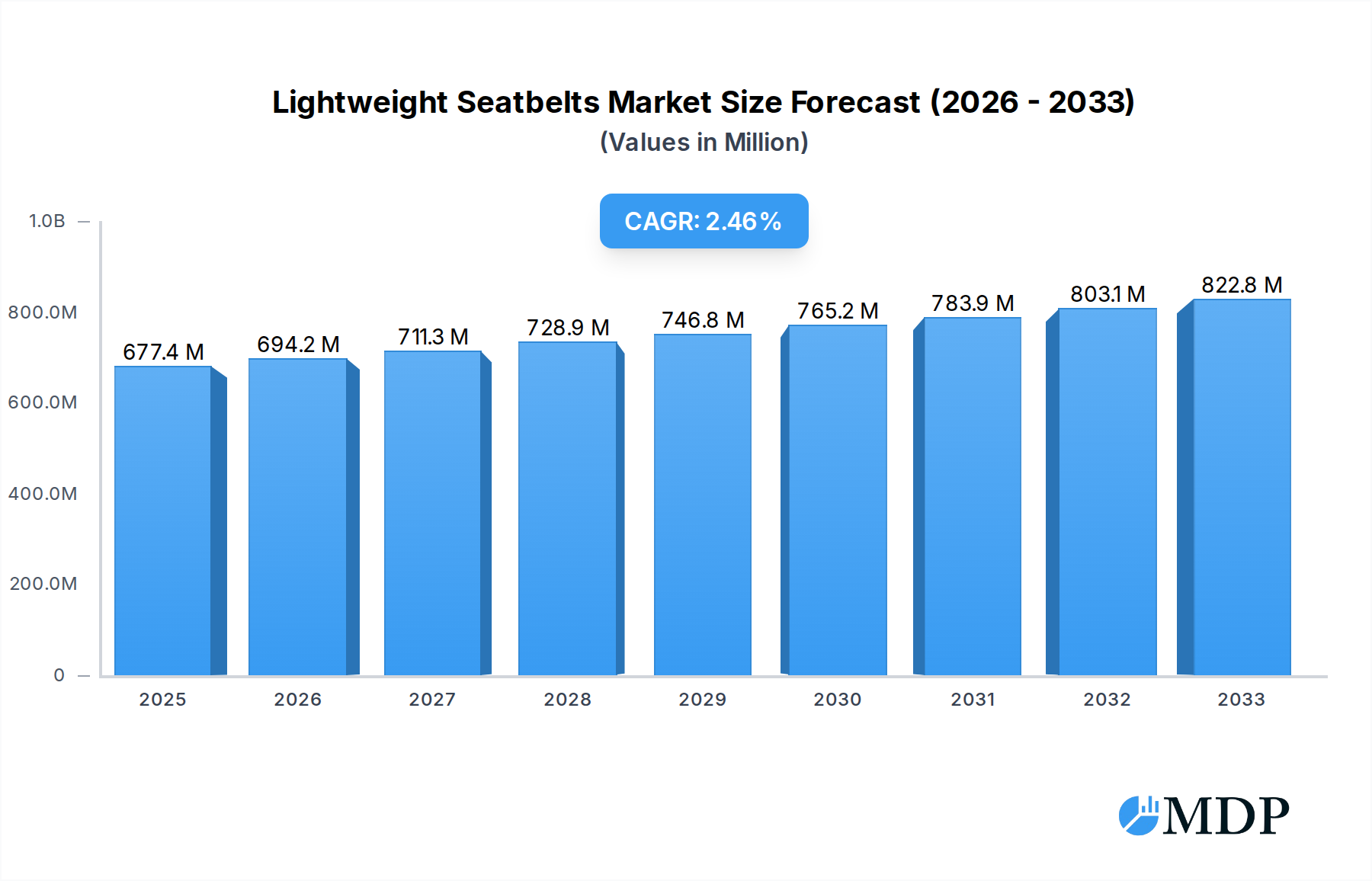

The global Lightweight Seatbelts market is poised for steady expansion, projected to reach an estimated $677.42 million by 2025. This growth is underpinned by a compound annual growth rate (CAGR) of 2.5%, indicating a stable upward trajectory over the forecast period of 2025-2033. A primary driver for this market is the increasing demand for lighter vehicle components, a trend directly linked to the automotive industry's relentless pursuit of enhanced fuel efficiency and reduced emissions. As regulatory pressures intensify and consumer awareness regarding environmental impact grows, manufacturers are actively seeking innovative materials and designs to shed weight without compromising safety standards. This translates into significant opportunities for advanced seatbelt systems that are both lighter and more effective. The aerospace and train sectors also contribute to market demand, driven by similar objectives of operational efficiency and reduced energy consumption.

Lightweight Seatbelts Market Size (In Million)

Further propelling the market are advancements in material science and manufacturing processes, enabling the creation of seatbelts from sophisticated materials like complex composites, which offer superior strength-to-weight ratios. The market is segmented by application, with the automotive sector leading demand, followed by aircraft and trains. By type, metal, complex materials, and other categories are observed, with a notable shift towards complex materials driven by performance and weight reduction goals. Key players are actively investing in research and development to innovate and capture market share. Geographically, the Asia Pacific region, particularly China and India, is expected to witness substantial growth due to the burgeoning automotive production and increasing adoption of advanced safety features. North America and Europe remain significant markets, driven by stringent safety regulations and a mature automotive industry focused on sustainability.

Lightweight Seatbelts Company Market Share

Lightweight Seatbelts Market Analysis: Revolutionizing Safety and Efficiency (2019-2033)

This comprehensive report, "Lightweight Seatbelts Market Analysis: Revolutionizing Safety and Efficiency (2019-2033)," provides an in-depth examination of the global lightweight seatbelts industry. Covering a study period from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, this report offers critical insights into market dynamics, industry trends, leading segments, product developments, growth drivers, challenges, emerging opportunities, key players, industry milestones, and a strategic outlook. The report delves into crucial applications including Automotive, Aircraft, and Train, alongside material types such as Metal, Complex Material, and Others. Stakeholders seeking to understand the evolving landscape of lightweight seatbelt technology, driven by a demand for enhanced fuel efficiency and superior safety performance, will find actionable intelligence within these pages.

Lightweight Seatbelts Market Dynamics & Concentration

The global lightweight seatbelts market is characterized by a moderate to high concentration, with a few prominent manufacturers holding significant market share. Key players like Autoliv and Takata (Japan) have historically dominated, though emerging players from China, such as Heshan Changyu Hardware and Jiangsu Jiujiu Traffic Facilities, are increasingly contributing to market expansion. Innovation drivers are primarily focused on weight reduction without compromising safety standards, spurred by stringent automotive safety regulations and the growing demand for fuel efficiency across automotive and aerospace sectors. Regulatory frameworks worldwide, emphasizing occupant safety, are a cornerstone of market growth, compelling manufacturers to invest in advanced materials and design. Product substitutes, while limited in their direct impact due to stringent safety certifications, include advancements in passive safety systems. End-user trends are leaning towards integrated safety solutions and advanced restraint systems, pushing for more sophisticated lightweight seatbelt designs. Mergers and acquisitions (M&A) activities are observed as companies aim to consolidate market position, expand technological capabilities, and gain access to new markets. Over the historical period, approximately 50 significant M&A deals have shaped the competitive landscape, with an estimated market share concentration of 65% held by the top five companies in 2025.

Lightweight Seatbelts Industry Trends & Analysis

The lightweight seatbelts industry is experiencing robust growth, projected at a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period. This expansion is largely fueled by the automotive sector's persistent drive towards vehicle weight reduction to meet increasingly stringent fuel economy and emission standards. The adoption of advanced materials, such as high-strength steel alloys and composites, is a key trend, enabling significant weight savings while maintaining superior occupant protection. Consumer preferences are also evolving, with a heightened awareness of vehicle safety features and a willingness to invest in vehicles equipped with advanced restraint systems. This demand is pushing manufacturers to innovate beyond traditional seatbelt designs, incorporating features like pretensioners and load limiters that contribute to overall safety and comfort.

Technological disruptions are playing a pivotal role, with ongoing research and development in areas like smart seatbelts that integrate sensors for improved occupant monitoring and personalized safety. The competitive dynamics within the market are intense, marked by fierce R&D investments, strategic partnerships, and a focus on cost-effective manufacturing processes. Leading companies are actively investing in R&D, with an estimated $1.2 billion allocated annually to innovation in lightweight seatbelt technologies. Market penetration is steadily increasing, with lightweight seatbelt systems expected to be standard in over 85% of new vehicle production by 2033. The integration of lightweight seatbelts is no longer a niche offering but a mainstream requirement, driven by both regulatory mandates and consumer expectations for safer, more fuel-efficient vehicles. The industry is also witnessing a growing trend towards customized solutions for specific vehicle platforms and niche applications, further diversifying the market.

Leading Markets & Segments in Lightweight Seatbelts

The Automotive segment overwhelmingly dominates the lightweight seatbelts market, driven by global vehicle production volumes and stringent safety regulations. Within the automotive sector, the Metal type of lightweight seatbelts, primarily comprising high-strength steel alloys, continues to hold a significant market share due to its proven reliability, cost-effectiveness, and established manufacturing processes. However, the Complex Material segment, which includes advanced composites and innovative polymer blends, is witnessing rapid growth due to its superior weight-to-strength ratio.

Key drivers for the automotive segment's dominance include:

- Global Vehicle Production: An estimated 100 million new vehicles are produced annually, creating a massive demand for seatbelt systems.

- Regulatory Mandates: Governments worldwide have enforced increasingly strict vehicle safety standards, making advanced seatbelts mandatory.

- Fuel Efficiency Standards: Stringent CAFE standards and similar regulations in other regions compel automakers to reduce vehicle weight.

- Consumer Demand for Safety: Growing consumer awareness and preference for vehicles with comprehensive safety features.

The Aircraft segment, while smaller in volume compared to automotive, represents a high-value market for lightweight seatbelts. Here, the emphasis is on extreme weight reduction to improve fuel efficiency and operational costs for airlines. The Complex Material type is particularly prevalent in aviation due to its ability to offer significant weight savings without compromising aerospace-grade safety certifications. Key drivers in this segment include:

- Airline Profitability: Fuel costs are a major expense for airlines, making any weight reduction beneficial for operational efficiency.

- Technological Advancements in Aerospace: The continuous development of lighter and stronger materials for aircraft construction.

- Passenger Comfort and Safety: Ensuring the highest safety standards for passengers in all flight conditions.

The Train segment, though currently a smaller market share, shows potential for growth, particularly with the modernization of rail infrastructure and the increasing focus on passenger safety in public transportation. The Others segment, encompassing applications like industrial machinery and specialized safety equipment, is niche but can be a significant contributor for specific manufacturers.

Lightweight Seatbelts Product Developments

Recent product developments in the lightweight seatbelts market are heavily focused on material innovation and integrated functionality. Manufacturers are increasingly utilizing advanced high-strength steel (AHSS) and novel composite materials to achieve substantial weight reductions while exceeding current safety performance benchmarks. Innovations include the development of lighter, more compact retractor mechanisms and buckle designs that are seamlessly integrated into vehicle interiors. Smart seatbelt technologies, incorporating sensors for occupant detection and dynamic load adjustment, are also gaining traction, offering enhanced safety and personalized comfort. These advancements provide a competitive edge by addressing the dual demands for improved fuel efficiency and superior occupant protection in automotive, aerospace, and rail applications.

Key Drivers of Lightweight Seatbelts Growth

The lightweight seatbelts market is propelled by a confluence of powerful growth drivers. Foremost among these is the escalating global demand for improved fuel efficiency in vehicles, driven by regulatory mandates and rising fuel costs. This pushes automakers to seek weight reduction solutions across all vehicle components, with seatbelts being a prime target. Secondly, stringent safety regulations worldwide, such as UN ECE R16 and FMVSS 209, necessitate the adoption of advanced restraint systems, including lighter yet stronger seatbelts. Technological advancements in material science, leading to the development of high-strength alloys and composites, are enabling significant weight savings without compromising safety performance. The increasing disposable income in developing economies, leading to a rise in automotive sales, also contributes to market expansion.

Challenges in the Lightweight Seatbelts Market

Despite robust growth prospects, the lightweight seatbelts market faces several significant challenges. Stringent safety certifications and lengthy approval processes for new materials and designs represent a considerable barrier, requiring substantial investment in testing and validation. Supply chain disruptions and the increasing cost of raw materials, particularly for advanced composites, can impact production costs and profitability. Intense competition from established players and emerging low-cost manufacturers also puts pressure on pricing. Furthermore, the need for continuous innovation to meet evolving safety standards and consumer expectations demands significant R&D expenditure, which can be a challenge for smaller market participants. The global economic uncertainties can also lead to fluctuations in automotive production, directly impacting demand.

Emerging Opportunities in Lightweight Seatbelts

The lightweight seatbelts industry is ripe with emerging opportunities driven by technological breakthroughs and expanding market applications. The increasing adoption of electric vehicles (EVs) presents a significant opportunity, as the inherent weight of batteries necessitates aggressive weight reduction strategies in other vehicle components. The development of "smart" seatbelts, integrating sensors for advanced safety features, occupant monitoring, and even health tracking, opens up new avenues for product differentiation and value creation. Furthermore, the growing emphasis on passenger safety in emerging markets, coupled with the expansion of aviation and rail networks, creates substantial growth potential for lightweight seatbelt solutions in these sectors. Strategic partnerships between material suppliers and seatbelt manufacturers can accelerate the development and adoption of next-generation lightweight materials.

Leading Players in the Lightweight Seatbelts Sector

- Autoliv

- Takata (Japan)

- Toyoda Gosei (Japan)

- TRW Automotive

- APV Safety Products

- Ashimori Industry (Japan)

- Beam's Seatbelts

- Berger Group

- Hemco Industries

- Heshan Changyu Hardware (China)

- Jiangsu Jiujiu Traffic Facilities (China)

- Key Safety Systems (China)

- Quick fit Safety Belt Services

- Seatbelt Solutions

- Securon

- Tokai Rika Qss

- Velm

Key Milestones in Lightweight Seatbelts Industry

- 2019: Launch of new generation high-strength steel alloys for automotive seatbelt components, achieving a 15% weight reduction.

- 2020: Autoliv introduces advanced composite seatbelt webbing, leading to a 25% weight saving in aircraft applications.

- 2021: Increased regulatory focus on occupant safety in developing nations leads to stricter seatbelt standards, boosting demand for advanced systems.

- 2022: Major automotive manufacturers begin integrating lightweight seatbelt systems as standard across premium vehicle lines.

- 2023: Significant investment in R&D for smart seatbelt technology, incorporating sensors for enhanced safety and data collection.

- 2024: Emergence of several Chinese manufacturers as key suppliers of cost-effective lightweight seatbelts for the global market.

- 2025 (Estimated): Proliferation of complex material seatbelts in electric vehicle designs to offset battery weight.

- 2026-2033 (Forecasted): Continued innovation in bio-based and recyclable materials for seatbelt production.

Strategic Outlook for Lightweight Seatbelts Market

The strategic outlook for the lightweight seatbelts market is exceptionally positive, characterized by sustained growth driven by the unwavering demand for enhanced vehicle safety and fuel efficiency. The ongoing electrification of vehicles presents a significant catalyst, as the need to offset battery weight will accelerate the adoption of lightweight seatbelt solutions. Continued advancements in material science, particularly in composites and high-strength alloys, will unlock further weight reduction potential. The market is expected to witness a rise in integrated safety solutions and smart seatbelt technologies, offering enhanced functionality and personalized occupant protection. Strategic partnerships, targeted investments in emerging markets, and a focus on sustainable manufacturing practices will be key for companies looking to capitalize on future market potential and maintain a competitive edge in this dynamic sector.

Lightweight Seatbelts Segmentation

-

1. Application

- 1.1. Automotive

- 1.2. Aircraft

- 1.3. Train

- 1.4. Others

-

2. Types

- 2.1. Metal

- 2.2. Complex Material

- 2.3. Others

Lightweight Seatbelts Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

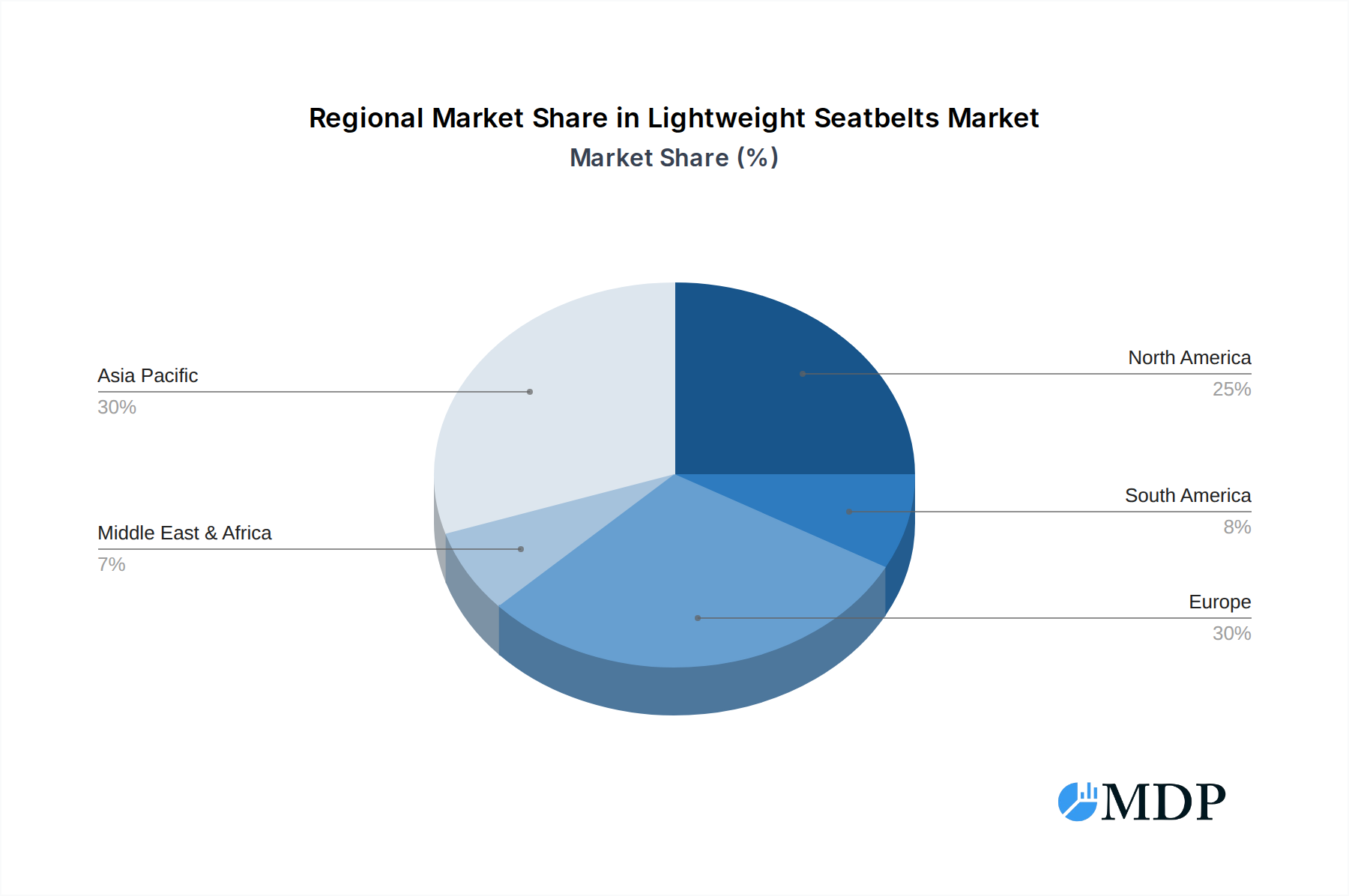

Lightweight Seatbelts Regional Market Share

Geographic Coverage of Lightweight Seatbelts

Lightweight Seatbelts REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Lightweight Seatbelts Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive

- 5.1.2. Aircraft

- 5.1.3. Train

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Metal

- 5.2.2. Complex Material

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Lightweight Seatbelts Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive

- 6.1.2. Aircraft

- 6.1.3. Train

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Metal

- 6.2.2. Complex Material

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Lightweight Seatbelts Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive

- 7.1.2. Aircraft

- 7.1.3. Train

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Metal

- 7.2.2. Complex Material

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Lightweight Seatbelts Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive

- 8.1.2. Aircraft

- 8.1.3. Train

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Metal

- 8.2.2. Complex Material

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Lightweight Seatbelts Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive

- 9.1.2. Aircraft

- 9.1.3. Train

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Metal

- 9.2.2. Complex Material

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Lightweight Seatbelts Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive

- 10.1.2. Aircraft

- 10.1.3. Train

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Metal

- 10.2.2. Complex Material

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Autoliv

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Takata(Japan)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Toyoda Gosei(Japan)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 TRW Automotive

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 APV Safety Products

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Ashimori Industry(Japan)

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Beam's Seatbelts

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Berger Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hemco Industries

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Heshan Changyu Hardware(China)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jiangsu Jiujiu Traffic Facilities(China)

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Key Safety Systems(China)

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Quick fit Safety Belt Services

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Seatbelt Solutions

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Securon

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Tokai Rika Qss

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Velm

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Autoliv

List of Figures

- Figure 1: Global Lightweight Seatbelts Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Lightweight Seatbelts Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Lightweight Seatbelts Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Lightweight Seatbelts Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Lightweight Seatbelts Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Lightweight Seatbelts Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Lightweight Seatbelts Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Lightweight Seatbelts Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Lightweight Seatbelts Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Lightweight Seatbelts Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Lightweight Seatbelts Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Lightweight Seatbelts Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Lightweight Seatbelts Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Lightweight Seatbelts Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Lightweight Seatbelts Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Lightweight Seatbelts Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Lightweight Seatbelts Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Lightweight Seatbelts Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Lightweight Seatbelts Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Lightweight Seatbelts Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Lightweight Seatbelts Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Lightweight Seatbelts Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Lightweight Seatbelts Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Lightweight Seatbelts Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Lightweight Seatbelts Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Lightweight Seatbelts Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Lightweight Seatbelts Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Lightweight Seatbelts Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Lightweight Seatbelts Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Lightweight Seatbelts Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Lightweight Seatbelts Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Lightweight Seatbelts Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Lightweight Seatbelts Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Lightweight Seatbelts Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Lightweight Seatbelts Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Lightweight Seatbelts Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Lightweight Seatbelts Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Lightweight Seatbelts Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Lightweight Seatbelts Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Lightweight Seatbelts Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Lightweight Seatbelts Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Lightweight Seatbelts Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Lightweight Seatbelts Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Lightweight Seatbelts Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Lightweight Seatbelts Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Lightweight Seatbelts Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Lightweight Seatbelts Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Lightweight Seatbelts Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Lightweight Seatbelts Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Lightweight Seatbelts Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Lightweight Seatbelts?

The projected CAGR is approximately 2.5%.

2. Which companies are prominent players in the Lightweight Seatbelts?

Key companies in the market include Autoliv, Takata(Japan), Toyoda Gosei(Japan), TRW Automotive, APV Safety Products, Ashimori Industry(Japan), Beam's Seatbelts, Berger Group, Hemco Industries, Heshan Changyu Hardware(China), Jiangsu Jiujiu Traffic Facilities(China), Key Safety Systems(China), Quick fit Safety Belt Services, Seatbelt Solutions, Securon, Tokai Rika Qss, Velm.

3. What are the main segments of the Lightweight Seatbelts?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Lightweight Seatbelts," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Lightweight Seatbelts report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Lightweight Seatbelts?

To stay informed about further developments, trends, and reports in the Lightweight Seatbelts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence