Key Insights

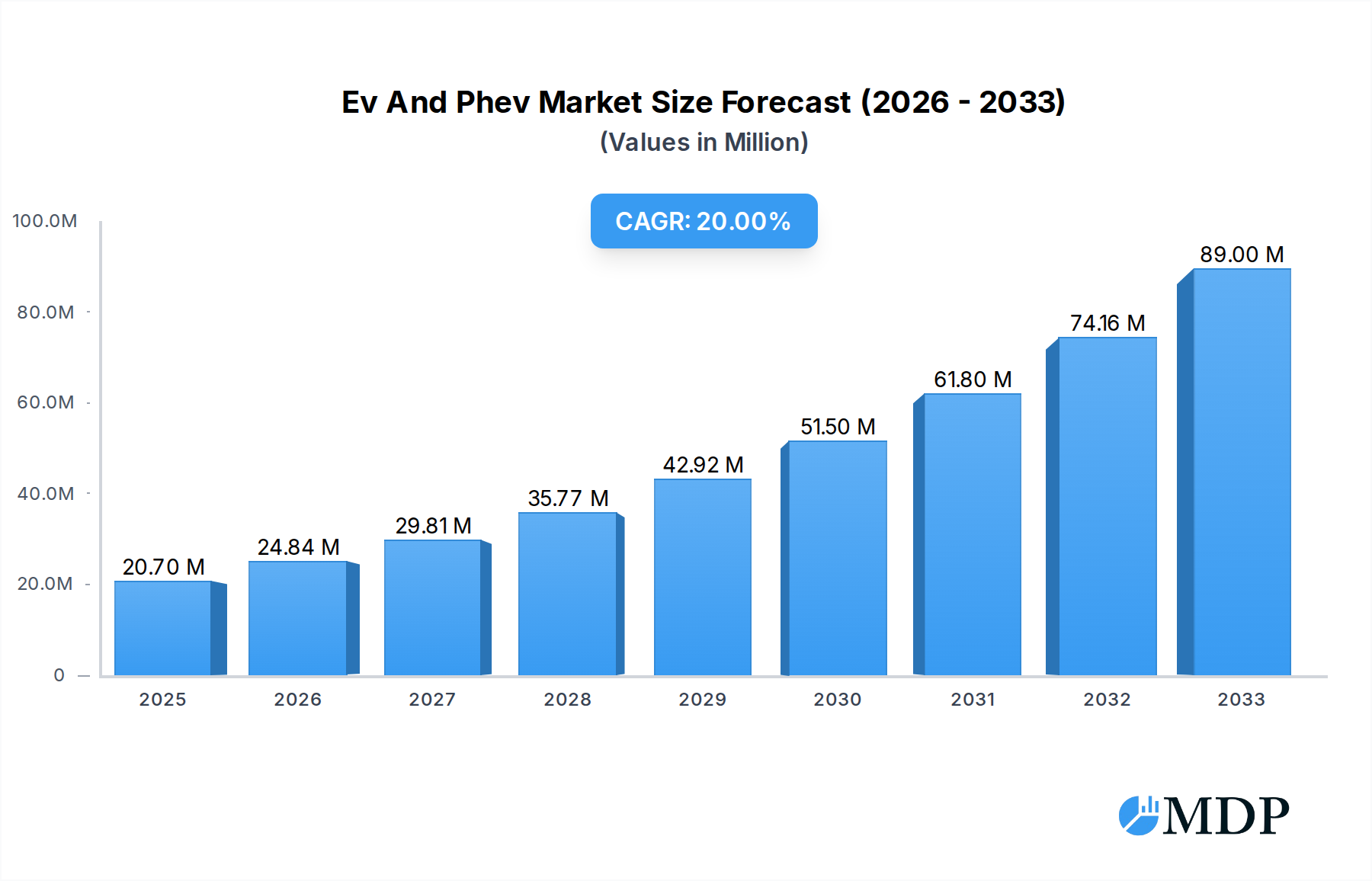

The global market for Electric Vehicles (EVs) and Plug-in Hybrid Electric Vehicles (PHEVs) is poised for substantial expansion, demonstrating robust growth trajectories across diverse automotive sectors. With an estimated market size of $20.7 million in 2025, this segment is projected to witness an impressive Compound Annual Growth Rate (CAGR) of 20% through 2033. This surge is primarily fueled by an increasing global awareness and commitment towards sustainability, coupled with stringent government regulations aimed at reducing tailpipe emissions and promoting greener transportation solutions. Advancements in battery technology, leading to improved range and faster charging times, are further democratizing EV adoption. The growing charging infrastructure, both public and private, is alleviating range anxiety among consumers. Furthermore, the expanding portfolio of EV and PHEV models offered by major automotive manufacturers, encompassing a wider range of vehicle types from commercial fleets to passenger cars, caters to a broader consumer base and specific industrial needs. The escalating fuel prices also contribute significantly, making the lower running costs of electric powertrains increasingly attractive to both individual buyers and fleet operators.

Ev And Phev Market Size (In Million)

The dynamism of the EV and PHEV market is further shaped by evolving consumer preferences and technological innovations. While the initial adoption might have been concentrated in developed regions, emerging economies are rapidly catching up, driven by supportive government incentives and a burgeoning middle class keen on adopting advanced technologies. The competitive landscape is intense, with established automotive giants like Toyota, Volkswagen, and Ford actively investing in and launching new electric models, alongside dedicated EV players such as Tesla and BYD. This competition is driving down prices and enhancing the overall value proposition for consumers. However, challenges such as the initial high purchase cost of some EV models, the availability of charging infrastructure in certain remote areas, and the sourcing of raw materials for battery production present ongoing considerations. Nevertheless, the overwhelming trend indicates a definitive shift towards electric mobility, with EVs and PHEVs set to redefine the future of personal and commercial transportation.

Ev And Phev Company Market Share

Dive deep into the rapidly evolving electric vehicle (EV) and plug-in hybrid electric vehicle (PHEV) market with this comprehensive, SEO-optimized report. Covering the period from 2019 to 2033, this analysis provides crucial insights for stakeholders in the automotive industry, government bodies, and investors. Our study zeroes in on key companies such as Volvo, Volkswagen, Toyota, Tesla, BMW, Porsche, Nissan, Mitsubishi, Kia, Hyundai, Honda, Ford, Fiat, Chevrolet, Audi, and BYD, examining their strategies and market positioning across Commercial Vehicle and Passenger Vehicle applications, and EV and PHEV types.

EV And Phev Market Dynamics & Concentration

The global EV and PHEV market is experiencing dynamic shifts, marked by increasing concentration in certain segments and intense competition among leading automotive manufacturers. Innovation drivers such as advancements in battery technology, charging infrastructure development, and government incentives are fueling rapid adoption. Regulatory frameworks, including emission standards and EV mandates, are further shaping market dynamics, pushing companies towards sustainable mobility solutions. The threat of product substitutes, while present in the form of highly efficient internal combustion engine (ICE) vehicles and emerging hydrogen fuel cell technologies, is diminishing as EV and PHEV technology matures and infrastructure expands. End-user trends reveal a growing consumer preference for environmentally friendly, technologically advanced, and cost-effective transportation options. Mergers and acquisitions (M&A) activities are also on the rise, with an estimated xx M&A deal count in the historical period, as companies seek to consolidate their market share, acquire new technologies, and expand their global footprint. Key players like Tesla and BYD have significantly influenced market concentration, with Tesla leading in battery-electric vehicle (BEV) market share, estimated at over 20% globally in the Passenger Vehicle segment. The overall market concentration, however, remains moderately fragmented, with a significant portion of the market share distributed amongst established automotive giants and emerging EV manufacturers.

EV And Phev Industry Trends & Analysis

The EV and PHEV industry is on an unprecedented growth trajectory, driven by a confluence of technological advancements, shifting consumer preferences, and supportive governmental policies. The Compound Annual Growth Rate (CAGR) for the global EV and PHEV market is projected to be approximately 15% over the forecast period (2025–2033), signaling robust expansion. Market penetration, which stood at around 8% globally in the base year 2025, is expected to surge significantly by 2033, driven by increasing model availability, falling battery costs, and expanding charging infrastructure. Technological disruptions, particularly in battery technology – including solid-state batteries and improved energy density – are leading to longer ranges and faster charging times, addressing key consumer concerns. Advancements in electric powertrains, autonomous driving features integrated into EVs, and smart connectivity are further enhancing the appeal of electric mobility. Consumer preferences are increasingly tilting towards sustainability, lower running costs, and the perceived technological superiority of EVs and PHEVs. This is evident in the rising demand for electric passenger vehicles, which currently dominate the market, but a significant growth is also anticipated in the commercial vehicle segment as fleets transition to cleaner alternatives. Competitive dynamics are intensifying, with traditional automakers like Volkswagen, Toyota, and Ford aggressively investing in their EV lineups to compete with established players like Tesla and emerging Chinese manufacturers such as BYD. The strategic focus is on offering diverse models across various price points and vehicle types, catering to a broader spectrum of consumers. The industry is also witnessing a significant shift towards electrification of the entire automotive value chain, from battery production and raw material sourcing to vehicle manufacturing and after-sales services.

Leading Markets & Segments in EV And Phev

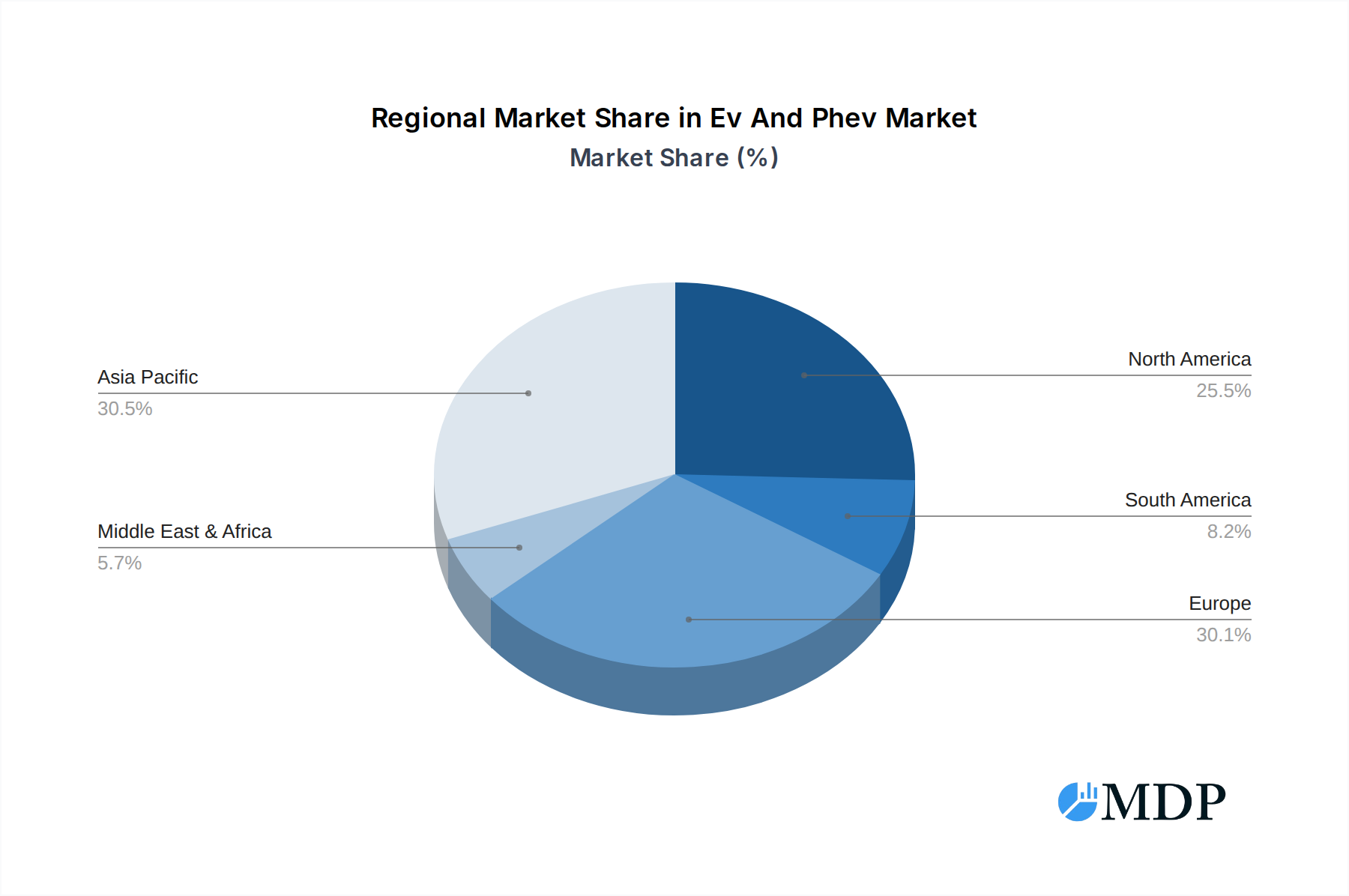

The global EV and PHEV market is experiencing pronounced leadership in specific regions and segments, driven by a combination of robust economic policies, extensive infrastructure development, and evolving consumer demands.

- Dominant Region: North America, particularly the United States, and Europe, spearheaded by countries like Germany, the UK, and Norway, are at the forefront of EV and PHEV adoption. Asia Pacific, with China leading the charge, is the largest market globally and is expected to continue its dominance due to aggressive government support, a vast manufacturing base, and a rapidly growing consumer market.

- Dominant Country: China's market share in the global EV and PHEV sector is substantial, accounting for over 50% of global sales in recent years. This is attributed to strong government subsidies, ambitious production targets, and a wide array of affordable EV models.

- Dominant Application: The Passenger Vehicle segment currently holds the largest market share, driven by increasing consumer awareness of environmental benefits, lower running costs, and a growing number of attractive EV and PHEV models available. However, the Commercial Vehicle segment is poised for significant growth, fueled by fleet electrification initiatives aimed at reducing operational expenses and meeting corporate sustainability goals.

- Dominant Type: The EV (Battery Electric Vehicle) segment is witnessing exponential growth and is expected to outpace PHEV adoption in the long term due to advancements in battery technology and expanding charging infrastructure. However, PHEVs continue to play a crucial role in bridging the gap for consumers who require flexibility and are concerned about range anxiety, especially in regions with less developed charging networks.

Key drivers for this dominance include:

- Economic Policies: Government incentives such as tax credits, purchase subsidies, and preferential registration policies significantly influence consumer purchasing decisions and manufacturer investments.

- Infrastructure Development: The rapid expansion of charging infrastructure, including public charging stations, home charging solutions, and faster charging technologies, is critical for widespread adoption.

- Technological Advancements: Continuous improvements in battery technology, motor efficiency, and overall vehicle performance make EVs and PHEVs increasingly competitive with traditional vehicles.

- Environmental Regulations: Stringent emission standards and mandates for zero-emission vehicles are compelling manufacturers and consumers to transition to electric mobility.

- Consumer Awareness and Demand: Growing environmental consciousness, coupled with the appeal of innovative technology and lower operating costs, is driving robust consumer demand.

EV And Phev Product Developments

Product innovation in the EV and PHEV sector is relentless, focusing on enhancing performance, extending range, and improving charging convenience. Companies are launching new models with advanced battery chemistries offering higher energy densities and faster charging capabilities, with some aiming for over 500 miles of range. Applications are diversifying beyond passenger cars to include electric buses, trucks, and delivery vans, catering to the growing demand for sustainable logistics. Competitive advantages are being cultivated through integrated software solutions, advanced driver-assistance systems (ADAS), and unique design elements that appeal to tech-savvy consumers. The trend towards electrification of vehicle architectures and the development of dedicated EV platforms are enabling more efficient and spacious vehicle designs.

Key Drivers of EV And Phev Growth

The growth of the EV and PHEV market is propelled by a powerful synergy of factors. Technologically, advancements in battery energy density, charging speeds, and powertrain efficiency are making electric vehicles more practical and desirable. Economically, declining battery costs, government subsidies, and lower operational expenses (fuel and maintenance) are making EVs and PHEVs increasingly affordable and cost-effective over their lifetime. Regulatory tailwinds, including stringent emission standards, zero-emission vehicle mandates in key markets, and ICE vehicle phase-out targets, are compelling both manufacturers and consumers to embrace electric mobility.

Challenges in the EV And Phev Market

Despite the promising outlook, the EV and PHEV market faces significant challenges. Regulatory hurdles can arise from inconsistent policy implementation across regions and the evolving landscape of charging standards. Supply chain issues, particularly concerning the availability and ethical sourcing of critical raw materials like lithium and cobalt, pose a substantial risk to production volumes and cost stability. Competitive pressures are immense, with both legacy automakers and new entrants vying for market share, leading to price wars and increased R&D investments. Range anxiety, though diminishing, remains a concern for some consumers, and the availability of widespread, reliable charging infrastructure, especially in rural areas, is still a work in progress.

Emerging Opportunities in EV And Phev

Emerging opportunities in the EV and PHEV market are numerous and transformative. Technological breakthroughs in solid-state batteries promise enhanced safety, faster charging, and increased energy density, potentially revolutionizing EV performance and adoption rates. Strategic partnerships between automakers, battery manufacturers, and charging infrastructure providers are crucial for building robust ecosystems and accelerating deployment. Market expansion into developing economies, where the transition to electric mobility offers a chance to leapfrog traditional fossil fuel infrastructure, presents a significant growth avenue. The development of vehicle-to-grid (V2G) technology, allowing EVs to supply power back to the grid, opens up new revenue streams and grid stability benefits.

Leading Players in the EV And Phev Sector

- Tesla

- BYD

- Volkswagen

- Toyota

- General Motors (Chevrolet)

- Ford

- BMW

- Nissan

- Hyundai

- Kia

- Honda

- Audi

- Porsche

- Volvo

- Mitsubishi

- Fiat

Key Milestones in EV And Phev Industry

- 2019: Significant increase in global EV and PHEV sales driven by new model launches and expanding government incentives.

- 2020: Tesla surpasses 1 million EVs produced globally, marking a significant milestone for the company and the industry.

- 2021: Major automakers announce ambitious electrification targets, committing billions of dollars to EV development and production.

- 2022: Battery costs continue to decline, making EVs more competitive. Charging infrastructure expansion accelerates globally.

- 2023: China solidifies its position as the world's largest EV market, with BYD emerging as a dominant force in electric vehicle sales.

- 2024: Increased focus on EV charging reliability and standardization. Growing interest in electric commercial vehicles.

- 2025 (Base Year): Projected significant increase in EV and PHEV market share, with widespread adoption of new battery technologies.

- 2026: Further advancements in autonomous driving capabilities integrated into electric vehicles.

- 2028: Potential for widespread adoption of solid-state batteries in premium EV models.

- 2030: Many countries and regions set targets for phasing out the sale of new internal combustion engine vehicles.

- 2033 (Forecast End): Projections indicate electric vehicles will constitute a substantial majority of new vehicle sales globally.

Strategic Outlook for EV And Phev Market

The strategic outlook for the EV and PHEV market is exceptionally strong, driven by sustained technological innovation, supportive government policies, and a growing global consciousness towards sustainable transportation. The continued reduction in battery costs, coupled with advancements in charging infrastructure and vehicle range, will further accelerate consumer adoption across all vehicle segments, including commercial vehicles. Key growth accelerators include the development of more affordable EV models, expansion into emerging markets, and the integration of smart technologies that enhance the ownership experience. Strategic partnerships and consolidation within the industry will continue to shape the competitive landscape, fostering efficiency and driving further innovation. The future market potential is vast, promising a significant shift towards an all-electric automotive future.

Ev And Phev Segmentation

-

1. Application

- 1.1. Commercial Vehicle

- 1.2. Passenger Vehicle

-

2. Type

- 2.1. EV

- 2.2. PHEV

Ev And Phev Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ev And Phev Regional Market Share

Geographic Coverage of Ev And Phev

Ev And Phev REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ev And Phev Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicle

- 5.1.2. Passenger Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. EV

- 5.2.2. PHEV

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ev And Phev Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicle

- 6.1.2. Passenger Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. EV

- 6.2.2. PHEV

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ev And Phev Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicle

- 7.1.2. Passenger Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. EV

- 7.2.2. PHEV

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ev And Phev Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicle

- 8.1.2. Passenger Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. EV

- 8.2.2. PHEV

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ev And Phev Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicle

- 9.1.2. Passenger Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. EV

- 9.2.2. PHEV

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ev And Phev Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicle

- 10.1.2. Passenger Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. EV

- 10.2.2. PHEV

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Volvo

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Volkswagen

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Toyota

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Tesla

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 BMW

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Porsche

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Nissan

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Mitsubishi

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Kia

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Hyundai

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Honda

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Ford

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Fiat

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Chevrolet

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Audi

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 BYD

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Volvo

List of Figures

- Figure 1: Global Ev And Phev Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Ev And Phev Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Ev And Phev Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ev And Phev Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Ev And Phev Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ev And Phev Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Ev And Phev Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ev And Phev Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Ev And Phev Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ev And Phev Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Ev And Phev Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ev And Phev Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Ev And Phev Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ev And Phev Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Ev And Phev Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ev And Phev Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Ev And Phev Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ev And Phev Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Ev And Phev Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ev And Phev Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ev And Phev Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ev And Phev Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ev And Phev Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ev And Phev Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ev And Phev Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ev And Phev Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Ev And Phev Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ev And Phev Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Ev And Phev Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ev And Phev Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Ev And Phev Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ev And Phev Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Ev And Phev Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Ev And Phev Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Ev And Phev Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Ev And Phev Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Ev And Phev Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Ev And Phev Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Ev And Phev Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Ev And Phev Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Ev And Phev Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Ev And Phev Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Ev And Phev Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Ev And Phev Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Ev And Phev Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Ev And Phev Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Ev And Phev Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Ev And Phev Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Ev And Phev Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ev And Phev Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ev And Phev?

The projected CAGR is approximately 20%.

2. Which companies are prominent players in the Ev And Phev?

Key companies in the market include Volvo, Volkswagen, Toyota, Tesla, BMW, Porsche, Nissan, Mitsubishi, Kia, Hyundai, Honda, Ford, Fiat, Chevrolet, Audi, BYD.

3. What are the main segments of the Ev And Phev?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ev And Phev," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ev And Phev report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ev And Phev?

To stay informed about further developments, trends, and reports in the Ev And Phev, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence