Key Insights

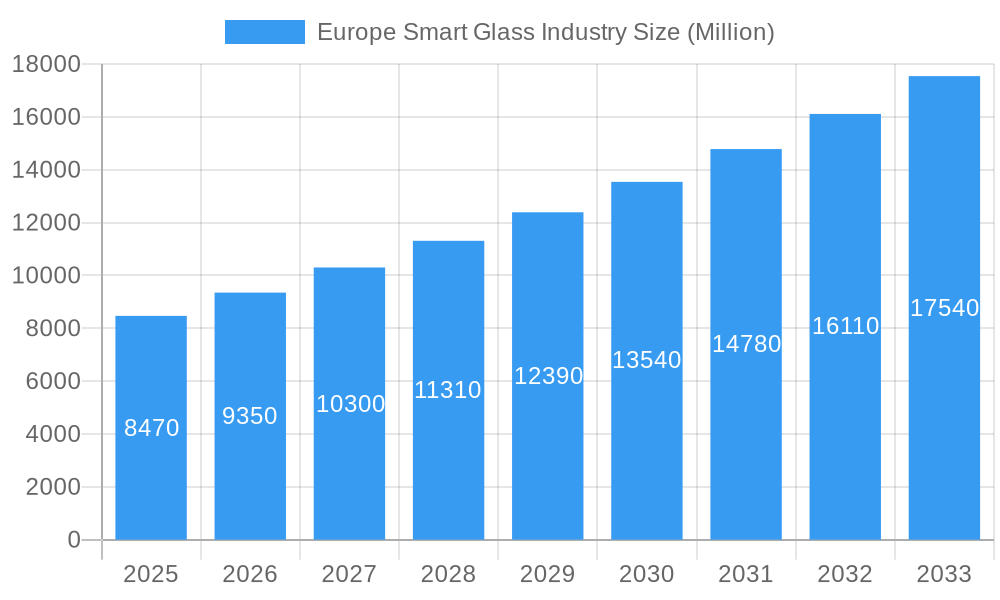

The European smart glass market is poised for significant expansion, projected to reach $8.47 billion in 2025, with a robust compound annual growth rate (CAGR) of 10.3% through 2033. This impressive growth is fueled by escalating demand across key sectors like construction and transportation. In construction, the integration of smart glass in residential and commercial buildings is driven by an increasing focus on energy efficiency, enhanced occupant comfort, and advanced aesthetic appeal. Architects and developers are increasingly recognizing the benefits of dynamic glazing for controlling solar heat gain, reducing reliance on artificial lighting, and improving acoustic insulation. Similarly, the transportation sector, encompassing aerospace, rail, and automotive, is witnessing a surge in smart glass adoption. This is largely attributed to its ability to provide adaptive shading, reduce glare, enhance privacy, and contribute to weight reduction in vehicles, ultimately improving fuel efficiency and passenger experience. The ongoing advancements in smart glass technologies, such as the development of more cost-effective and durable solutions, further bolster market penetration.

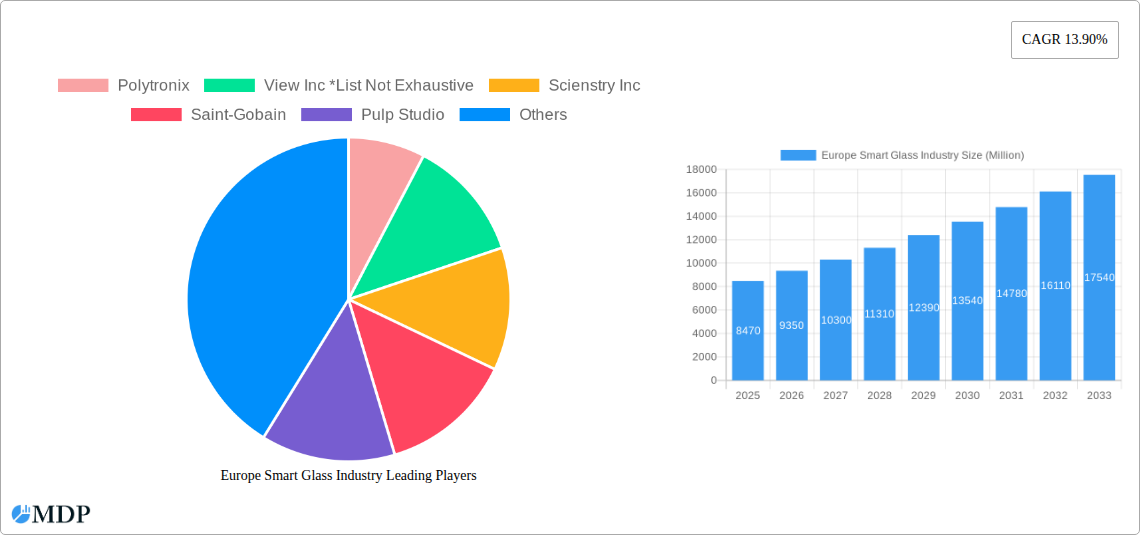

Europe Smart Glass Industry Market Size (In Billion)

While the market exhibits strong growth potential, certain factors could influence its trajectory. Restraints might include the initial high cost of installation compared to traditional glass and the need for greater consumer awareness and education regarding the long-term benefits and functionalities of smart glass. However, the prevailing trends of sustainability, technological innovation, and a growing preference for sophisticated building materials are expected to outweigh these challenges. The market segmentation reveals diverse opportunities, with technologies like Suspended Particle Devices (SPDs) and Liquid Crystals playing a crucial role in enabling dynamic opacity and tint control. Applications in energy efficiency initiatives and the burgeoning consumer electronics sector also represent significant growth avenues. Leading companies are actively investing in research and development to introduce next-generation smart glass solutions, fostering a competitive landscape that benefits end-users with improved performance and wider accessibility. Europe, with its strong emphasis on green building initiatives and advanced manufacturing capabilities, is expected to be a dominant region in this evolving market.

Europe Smart Glass Industry Company Market Share

Europe Smart Glass Industry Market: Comprehensive Analysis and Forecast 2025-2033

This in-depth report provides an exhaustive analysis of the Europe Smart Glass Industry, encompassing a detailed market overview, growth drivers, emerging trends, competitive landscape, and future projections. With a study period from 2019 to 2033 and a base year of 2025, this report is crucial for industry stakeholders seeking to understand and capitalize on the burgeoning opportunities within the European smart glass market. The market is projected to reach hundreds of billions by 2033, driven by advancements in technology, increasing demand for energy-efficient solutions, and evolving consumer preferences.

Europe Smart Glass Industry Market Dynamics & Concentration

The Europe Smart Glass Industry is characterized by a moderate to high market concentration, with key players actively investing in research and development to drive innovation. The primary innovation drivers include the pursuit of enhanced energy efficiency in buildings, the demand for advanced functionalities in architectural designs, and the growing integration of smart technologies into daily life. Regulatory frameworks, particularly those focused on sustainable construction and energy conservation, are indirectly fueling market growth by incentivizing the adoption of smart glass solutions. Product substitutes, such as traditional blinds and curtains, are becoming less competitive as the cost-effectiveness and performance benefits of smart glass become more apparent. End-user trends clearly indicate a strong preference for solutions that offer convenience, privacy control, and reduced energy consumption. Merger and acquisition (M&A) activities, while not at their peak, are observed as companies seek to expand their technological capabilities and market reach. For instance, strategic partnerships and acquisitions in the smart glass technology sector are expected to increase as companies aim to consolidate market share and accelerate product development. The estimated market share of leading players will continue to evolve based on their innovation pipeline and go-to-market strategies.

- Market Concentration: Moderate to High, with a few key players dominating specific technology segments.

- Innovation Drivers: Energy efficiency, architectural aesthetics, advanced functionality, smart home integration.

- Regulatory Frameworks: European Green Deal, building energy performance directives.

- Product Substitutes: Traditional blinds, curtains, films.

- End-User Trends: Demand for privacy, glare control, energy savings, aesthetic appeal, IoT integration.

- M&A Activities: Strategic acquisitions for technology integration and market expansion, with an estimated xx deal counts in the forecast period.

Europe Smart Glass Industry Industry Trends & Analysis

The Europe Smart Glass Industry is experiencing robust growth, fueled by a confluence of technological advancements, shifting consumer preferences, and increasing environmental consciousness. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period of 2025–2033. This sustained growth is largely attributed to the escalating demand for energy-efficient building solutions. Governments across Europe are implementing stringent regulations aimed at reducing carbon emissions and promoting sustainable development, which directly translates into a higher adoption rate for smart glass in both residential and commercial construction sectors. Furthermore, the integration of smart glass with the Internet of Things (IoT) ecosystem is opening up new avenues for automation and enhanced user experience. Consumers are increasingly seeking smart home solutions that offer convenience, comfort, and energy savings, making smart glass an attractive proposition. Technological disruptions, particularly in the development of more advanced and cost-effective smart glass technologies like electro-chromic and suspended particle devices, are also playing a pivotal role. These innovations are leading to improved performance characteristics such as faster switching times, better light transmission control, and enhanced durability. The competitive dynamics within the industry are intensifying, with established players investing heavily in R&D and new entrants focusing on niche applications and disruptive technologies. Market penetration is steadily increasing, particularly in Western European countries with a strong focus on sustainability and technological adoption. The rising disposable incomes in various European regions also contribute to the increasing affordability and demand for premium smart glass products in both new constructions and retrofitting projects. The energy sector's interest in smart glass for applications like solar energy harvesting and efficient lighting control further bolsters the industry's growth trajectory.

Leading Markets & Segments in Europe Smart Glass Industry

The European smart glass market is a dynamic landscape with distinct leaders across various geographical regions and technological segments. Germany and the United Kingdom are anticipated to be the dominant markets due to their strong focus on sustainable construction, advanced manufacturing capabilities, and significant investments in smart building technologies. France and the Nordic countries are also exhibiting substantial growth potential driven by favorable government incentives and a high propensity for adopting innovative solutions.

Within the technology segment, Electro-chromic Glass is poised to capture a significant market share owing to its excellent control over light and heat transmission, making it ideal for energy-efficient buildings. Liquid Crystals technology, while more mature, continues to offer a reliable and cost-effective solution for dynamic privacy and glare control. Suspended Particle Devices (SPD) are gaining traction for their rapid switching capabilities and suitability for applications requiring instant dimming. Active Smart Glass as a broader category, encompassing technologies that require an external power source for their functionality, will lead the market due to its versatility and advanced features. Passive Smart Glass, which operates without external power, will also maintain a steady market presence, particularly in cost-sensitive applications.

In terms of applications, Construction is the largest segment, further divided into:

- Commercial Buildings: This sub-segment is driven by the demand for energy efficiency, occupant comfort, and modern architectural aesthetics in office spaces, hotels, and retail environments.

- Residential Buildings: Increasing consumer awareness of energy savings and the desire for enhanced privacy and comfort are propelling the adoption of smart glass in homes.

The Transportation sector is another significant growth area, with:

- Automotive: The integration of smart glass for sunroofs, windows, and head-up displays to enhance driving experience, safety, and fuel efficiency is a key driver.

- Aerospace and Rail: Applications in aircraft windows and train interiors for glare reduction and passenger comfort are contributing to market expansion.

The Energy sector is exploring smart glass for its potential in building-integrated photovoltaics and smart window solutions for optimized energy harvesting and management. Consumer Electronics are also witnessing the emergence of smart glass in devices like smart displays and wearables, albeit at an earlier stage of development.

- Dominant Regions: Germany, United Kingdom, France, Nordic Countries.

- Key Drivers in Dominant Regions:

- Economic policies promoting green building certifications.

- Infrastructure development and smart city initiatives.

- High consumer spending power and adoption of premium technologies.

- Supportive government grants and tax incentives for energy-efficient solutions.

- Dominant Technology Segments: Electro-chromic Glass, Liquid Crystals, Suspended Particle Devices, Active Smart Glass.

- Dominant Application Segments: Construction (Commercial Buildings, Residential Buildings), Transportation (Automotive).

Europe Smart Glass Industry Product Developments

The Europe Smart Glass Industry is witnessing rapid product innovations focused on enhancing functionality, improving energy efficiency, and reducing costs. Key developments include the integration of smart glass with IoT platforms for seamless building automation, enabling remote control and personalized settings. Advanced electro-chromic technologies are offering faster switching speeds and wider temperature operating ranges, making them suitable for diverse European climates. The introduction of self-tinting and self-cleaning glass is further enhancing user convenience and reducing maintenance requirements. Innovations in SPD technology are leading to lighter and more energy-efficient solutions. Furthermore, advancements in manufacturing processes are driving down production costs, making smart glass more accessible for a wider range of applications, including mass-market residential buildings and automotive segments. The competitive advantage lies in offering integrated solutions that combine aesthetic appeal with superior performance and smart functionalities.

Key Drivers of Europe Smart Glass Industry Growth

The Europe Smart Glass Industry's growth is propelled by a multifaceted set of drivers. Foremost among these is the intensifying focus on sustainability and energy efficiency. European Union directives and national building codes mandating reduced energy consumption in buildings directly favor the adoption of smart glass technologies. Technological advancements in areas like electro-chromic and suspended particle devices are leading to more performant, cost-effective, and user-friendly products. The growing demand for smart homes and connected buildings is creating a significant pull for smart glass as an integral component of the IoT ecosystem, offering enhanced comfort, convenience, and security. Government incentives and subsidies for green building certifications and energy-saving retrofits further accelerate market penetration. Finally, the increasing awareness among consumers and businesses about the long-term cost savings and environmental benefits associated with smart glass is a crucial growth catalyst.

Challenges in the Europe Smart Glass Industry Market

Despite the promising growth, the Europe Smart Glass Industry faces several challenges. The high initial cost of smart glass compared to traditional glazing remains a significant barrier for widespread adoption, particularly in the residential sector. Complex installation processes and the need for specialized expertise can also deter some consumers and builders. Limited awareness and understanding of the technology's benefits among a broader audience can hinder market penetration. Furthermore, scalability of manufacturing processes to meet potentially high future demand and ensuring consistent product quality and reliability across different manufacturers are ongoing concerns. Fragmented regulatory landscapes across different European countries regarding building codes and energy standards can also create complexities for market expansion.

Emerging Opportunities in Europe Smart Glass Industry

The Europe Smart Glass Industry is ripe with emerging opportunities driven by technological breakthroughs and evolving market demands. The burgeoning field of augmented reality (AR) and virtual reality (VR) presents a significant opportunity for advanced smart glass functionalities, enabling immersive experiences. The increasing focus on healthy buildings and indoor air quality opens doors for smart glass solutions that can dynamically control sunlight and heat, thereby optimizing occupant comfort and reducing reliance on artificial lighting and HVAC systems. Strategic partnerships between smart glass manufacturers, smart home technology providers, and construction firms are crucial for developing integrated and holistic solutions. Market expansion into emerging European economies with growing construction sectors and increasing environmental awareness also offers substantial untapped potential. Furthermore, advancements in transparent solar technology integration within smart glass could revolutionize building-integrated photovoltaics.

Leading Players in the Europe Smart Glass Industry Sector

- Polytronix

- View Inc

- Scienstry Inc

- Saint-Gobain

- Pulp Studio

- Smartglass International

- Citala

- Pro Display

- Asahi Glass Corporation

- Gentex Corporation

- Nippon

- Ravenbrick

- Hitachi Chemical

- LTI Smart Glass

- PPG Industries

Key Milestones in Europe Smart Glass Industry Industry

- September 2021: Xiaomi launched its own smart glasses, which are capable of taking photos, displaying messages and notifications, making calls, providing navigation, and translating text right in real-time in front of eyes. The glasses also have an indicator light that shows when the 5-megapixel camera is in use.

- September 2021: Facebook Inc, in partnership with Ray-Ban, launched its first smart glasses named 'Ray-Ban Stories' that allow wearers to listen to music, take calls, or capture photos and short videos and share them across Facebook's services using a companion app.

Strategic Outlook for Europe Smart Glass Industry Market

The strategic outlook for the Europe Smart Glass Industry is exceptionally positive, driven by a clear trajectory towards smarter, more sustainable, and user-centric built environments. Growth accelerators include continued innovation in electro-chromic and SPD technologies, leading to enhanced performance and affordability. The increasing integration of smart glass with the broader smart home and building automation ecosystem will unlock new revenue streams and enhance product value propositions. Strategic emphasis on developing solutions for niche applications within the automotive and aerospace sectors, alongside the dominant construction market, will diversify revenue sources. Furthermore, collaborations with architectural firms and developers to incorporate smart glass from the initial design phase will streamline adoption and foster innovation. The push for net-zero buildings and ambitious energy efficiency targets across Europe will continue to be the most significant market driver, solidifying smart glass as an indispensable component of modern construction.

Europe Smart Glass Industry Segmentation

-

1. Technology

- 1.1. Suspended Particle Devices

- 1.2. Liquid Crystals

- 1.3. Electro-chromic Glass

- 1.4. Passive Smart glass

- 1.5. Active Smart glass

- 1.6. Others

-

2. Applications

-

2.1. Construction

- 2.1.1. Residential Buildings

- 2.1.2. Commercial Buildings

-

2.2. Transportation

- 2.2.1. Aerospace

- 2.2.2. Rail

- 2.2.3. Automotive

- 2.2.4. Others

- 2.3. Energy

- 2.4. Consumer Electronics

-

2.1. Construction

Europe Smart Glass Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Smart Glass Industry Regional Market Share

Geographic Coverage of Europe Smart Glass Industry

Europe Smart Glass Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Suspended Particle Devices

- 5.1.2. Liquid Crystals

- 5.1.3. Electro-chromic Glass

- 5.1.4. Passive Smart glass

- 5.1.5. Active Smart glass

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Applications

- 5.2.1. Construction

- 5.2.1.1. Residential Buildings

- 5.2.1.2. Commercial Buildings

- 5.2.2. Transportation

- 5.2.2.1. Aerospace

- 5.2.2.2. Rail

- 5.2.2.3. Automotive

- 5.2.2.4. Others

- 5.2.3. Energy

- 5.2.4. Consumer Electronics

- 5.2.1. Construction

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Europe Smart Glass Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Suspended Particle Devices

- 6.1.2. Liquid Crystals

- 6.1.3. Electro-chromic Glass

- 6.1.4. Passive Smart glass

- 6.1.5. Active Smart glass

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Applications

- 6.2.1. Construction

- 6.2.1.1. Residential Buildings

- 6.2.1.2. Commercial Buildings

- 6.2.2. Transportation

- 6.2.2.1. Aerospace

- 6.2.2.2. Rail

- 6.2.2.3. Automotive

- 6.2.2.4. Others

- 6.2.3. Energy

- 6.2.4. Consumer Electronics

- 6.2.1. Construction

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Polytronix

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 View Inc *List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Scienstry Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Saint-Gobain

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Pulp Studio

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Smartglass International

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Citala

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Pro Display

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Asahi Glass Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Gentex Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Nippon

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Ravenbrick

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Hitachi Chemical

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 LTI Smart Glass

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 PPG Industries

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Polytronix

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Smart Glass Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Smart Glass Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Smart Glass Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 2: Europe Smart Glass Industry Revenue billion Forecast, by Applications 2020 & 2033

- Table 3: Europe Smart Glass Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Smart Glass Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 5: Europe Smart Glass Industry Revenue billion Forecast, by Applications 2020 & 2033

- Table 6: Europe Smart Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Smart Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Smart Glass Industry?

The projected CAGR is approximately 8.4%.

2. Which companies are prominent players in the Europe Smart Glass Industry?

Key companies in the market include Polytronix, View Inc *List Not Exhaustive, Scienstry Inc, Saint-Gobain, Pulp Studio, Smartglass International, Citala, Pro Display, Asahi Glass Corporation, Gentex Corporation, Nippon, Ravenbrick, Hitachi Chemical, LTI Smart Glass, PPG Industries.

3. What are the main segments of the Europe Smart Glass Industry?

The market segments include Technology, Applications.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing focus on Energy Conservation and Environment Friendly Technologies; Government Regulations; Increasing demand for energy savings techniques.

6. What are the notable trends driving market growth?

Transportation industry is expected to have further growth opportunities in the market.

7. Are there any restraints impacting market growth?

Lack of Awareness of Smart Glass Benefits; Technical Issues with the Usage of Large Size Smart Glass.

8. Can you provide examples of recent developments in the market?

September 2021: Xiaomi launched its own smart glasses, which are capable of taking photos, displaying messages and notifications, making calls, providing navigation, and translating text right in real-time in front of eyes. The glasses also have an indicator light that shows when the 5-megapixel camera is in use.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Smart Glass Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Smart Glass Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Smart Glass Industry?

To stay informed about further developments, trends, and reports in the Europe Smart Glass Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence