Key Insights

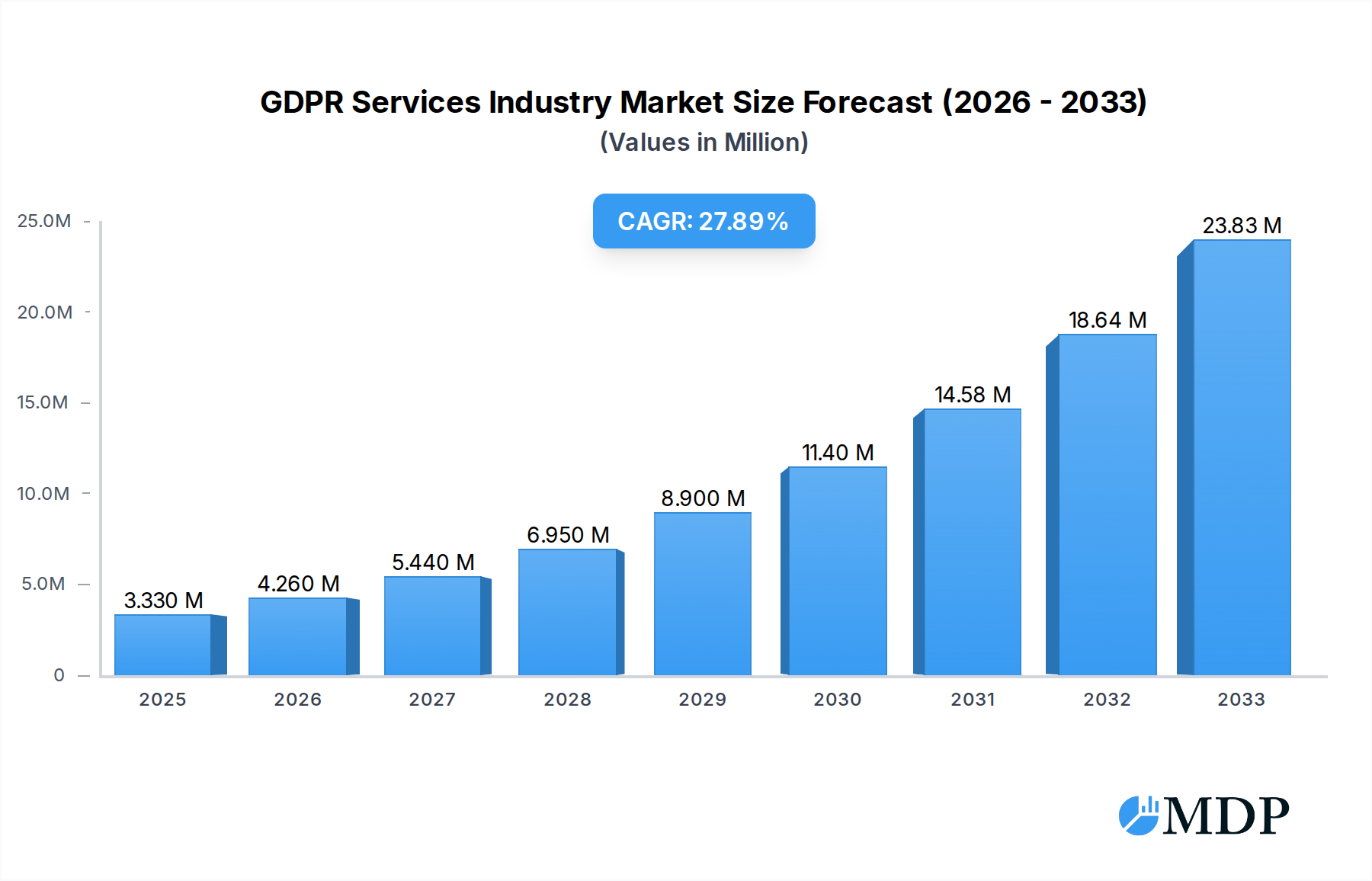

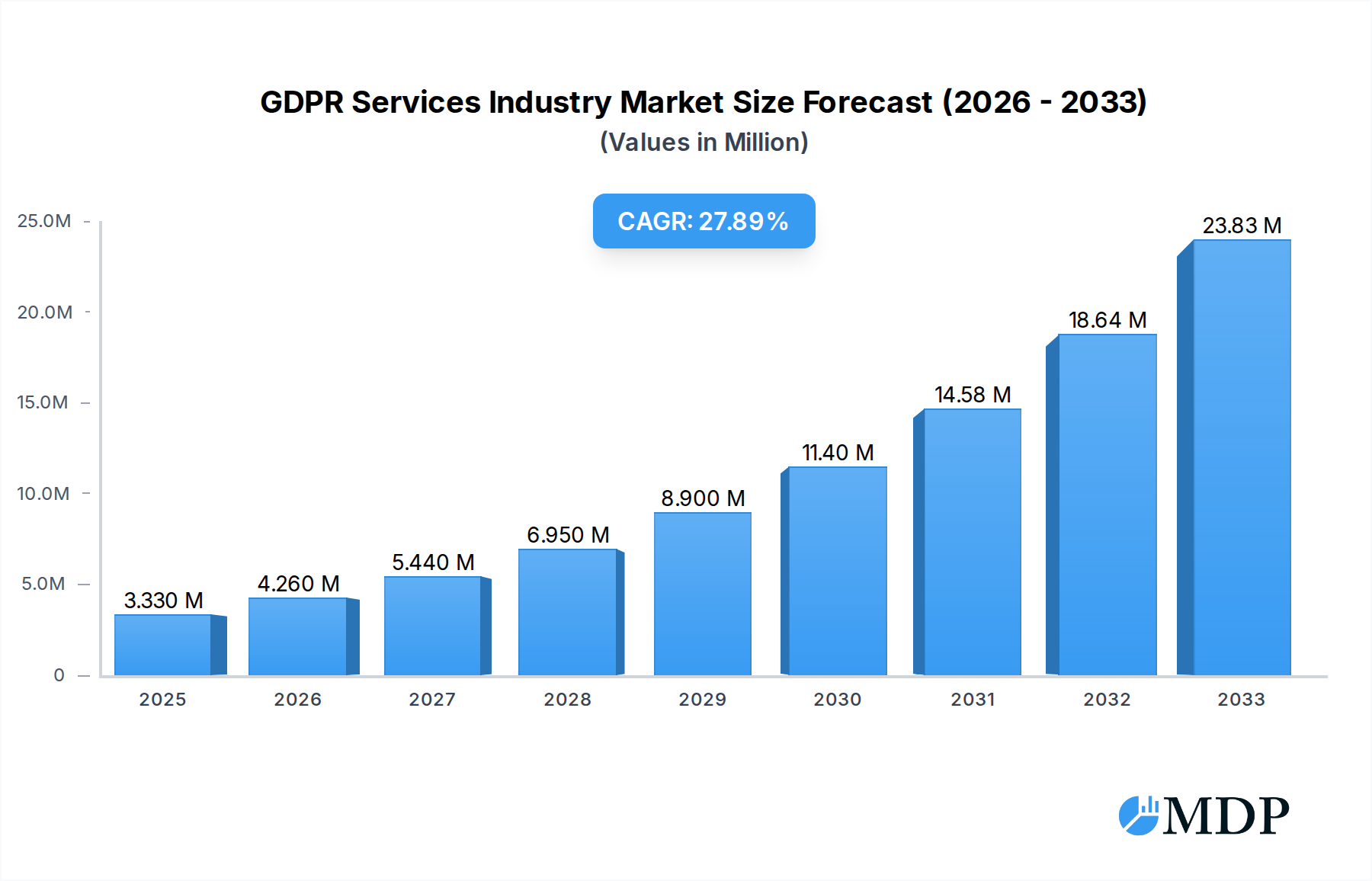

The GDPR Services market is experiencing robust expansion, projected to reach a significant valuation of $3.33 Million in 2025, with an impressive Compound Annual Growth Rate (CAGR) of 27.66% expected through 2033. This rapid ascent is propelled by an increasing emphasis on data privacy regulations and the growing need for organizations to achieve and maintain compliance with evolving data protection laws like GDPR. Key market drivers include the escalating volume of data generated globally, the rising threat of data breaches and associated penalties, and the growing consumer awareness regarding data privacy rights. Furthermore, the proliferation of cloud adoption across enterprises, while offering scalability and flexibility, simultaneously introduces new data security challenges that necessitate specialized GDPR services for effective management and protection.

GDPR Services Industry Market Size (In Million)

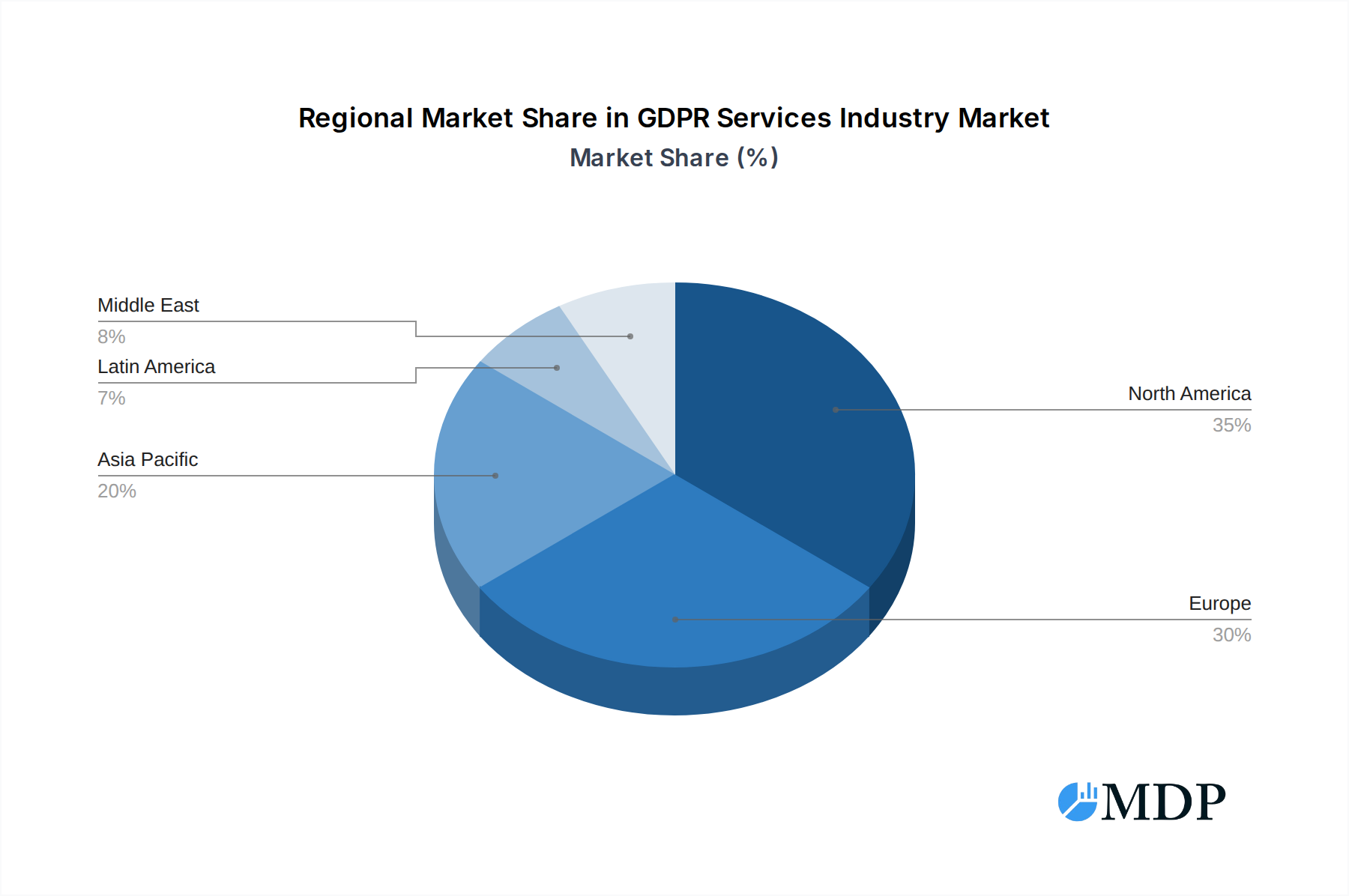

The market segmentation reveals a diverse landscape of opportunities. In terms of deployment, both on-premise and cloud solutions are critical, reflecting the varied infrastructure strategies of organizations. The offerings are comprehensive, spanning essential areas like Data Management, Data Discovery and Mapping, robust Data Governance frameworks, and API Management for secure data exchange. Large enterprises and Small and Medium-sized Enterprises (SMEs) alike are investing in these services, demonstrating the universal applicability of GDPR compliance. The Banking, Financial Services, and Insurance (BFSI) sector, along with Telecom and IT, Healthcare, Retail, and Manufacturing industries, represent the primary end-users, underscoring the pervasive impact of data privacy regulations across critical economic verticals. Geographically, North America and Europe are anticipated to lead the market due to their stringent regulatory environments and early adoption of data protection measures. However, the Asia Pacific region is poised for substantial growth, driven by increasing digitalization and a growing awareness of privacy concerns.

GDPR Services Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global GDPR Services Industry, a critical sector for businesses navigating complex data privacy regulations. With a study period spanning from 2019 to 2033, this report leverages data from the base year 2025, estimated year 2025, forecast period 2025–2033, and historical period 2019–2024 to offer unparalleled insights. The GDPR Services market is projected to witness significant growth, driven by increasing data breaches, evolving privacy laws, and the imperative for robust data protection. This analysis caters to a wide array of industry stakeholders, including IT professionals, legal advisors, compliance officers, and business strategists seeking to optimize their data privacy frameworks and capitalize on market opportunities.

GDPR Services Industry Market Dynamics & Concentration

The GDPR Services Industry is characterized by a dynamic interplay of innovation, regulatory mandates, and evolving end-user needs. Market concentration is moderately fragmented, with a few dominant players holding substantial market share, estimated to be around 35% collectively. Innovation drivers are primarily propelled by the increasing sophistication of cyber threats and the need for advanced data protection solutions. Regulatory frameworks, such as the GDPR itself, remain the cornerstone, dictating market entry and operational standards, while also fostering demand for compliance services. Product substitutes, though emerging in niche areas, are largely unable to replicate the comprehensive security and compliance offered by dedicated GDPR services. End-user trends reveal a heightened awareness and prioritization of data privacy across all sectors, leading to increased investment in GDPR-related solutions. Mergers and acquisitions (M&A) activities are moderately prevalent, with an estimated 25 deals in the historical period 2019-2024, indicating a consolidation drive among service providers seeking to expand their offerings and market reach.

- Market Share Concentration: Top 5 players hold approximately 35% of the market.

- M&A Deal Count (2019-2024): Estimated at 25 deals.

- Innovation Drivers: AI-powered data security, privacy-enhancing technologies, automated compliance workflows.

- Regulatory Landscape: GDPR, CCPA, LGPD, and other regional data protection laws.

- End-User Prioritization: Growing emphasis on data privacy and consumer trust.

GDPR Services Industry Industry Trends & Analysis

The GDPR Services Industry is experiencing robust growth, driven by an escalating global demand for data privacy and security solutions. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 18.5% from 2025 to 2033. This expansion is fueled by several key trends. Firstly, the increasing volume and complexity of data being generated and processed by businesses necessitate sophisticated GDPR services for compliance. Secondly, the rising frequency and impact of data breaches across various industries, from BFSI to healthcare, have heightened awareness and spurred investment in preventative measures. Technological disruptions, particularly in areas like artificial intelligence (AI) and machine learning (ML), are revolutionizing how GDPR compliance is achieved, enabling more efficient data discovery, mapping, and governance. Cloud adoption continues to be a significant trend, with organizations increasingly migrating their data and operations to the cloud, thus requiring cloud-specific GDPR solutions. Consumer preferences are also shifting, with individuals becoming more conscious of their data privacy rights and demanding greater transparency and control over their personal information. This paradigm shift is compelling businesses to adopt proactive GDPR compliance strategies to maintain customer trust and brand reputation. Competitive dynamics are intensifying, with both established technology giants and specialized GDPR service providers vying for market share. This competition fosters innovation and drives down costs, making GDPR compliance more accessible to a wider range of organizations. The penetration of GDPR services is expected to reach approximately 70% of large enterprises and 45% of SMEs by 2030.

Leading Markets & Segments in GDPR Services Industry

The GDPR Services Industry exhibits strong performance across various geographical regions and specific market segments. The Cloud deployment type is emerging as the dominant category, accounting for an estimated 65% of the market share, driven by the scalability, flexibility, and cost-effectiveness of cloud-based solutions. Within the Offering segment, Data Management services represent the largest share, estimated at 30%, followed closely by Data Governance at 25%, and Data Discovery and Mapping at 20%. API Management is a rapidly growing segment, projected to capture a significant portion of the market in the coming years due to the increasing use of APIs for data exchange.

Dominant Deployment Type:

- Cloud: Estimated 65% market share. This is attributed to its inherent flexibility, scalability, and the widespread adoption of cloud infrastructure by organizations seeking agile and cost-efficient data management solutions. Key drivers include the ability to easily integrate GDPR compliance tools with existing cloud ecosystems and leverage advanced cloud-native security features.

Dominant Offerings:

- Data Management: Estimated 30% market share. This encompasses a broad range of services crucial for GDPR compliance, including data protection, data minimization, and secure data storage.

- Data Governance: Estimated 25% market share. This segment focuses on establishing policies and procedures for data handling, ensuring data accuracy, integrity, and availability while adhering to privacy regulations.

- Data Discovery and Mapping: Estimated 20% market share. This critical offering helps organizations identify and locate personal data across their systems, a fundamental step for compliance.

- API Management: Rapidly growing segment, driven by the increasing reliance on APIs for interconnectivity and data sharing, necessitating robust security and privacy controls.

Dominant Organization Size:

- Large Enterprises: Currently hold the largest market share, estimated at 55%, due to their extensive data processing activities and higher susceptibility to regulatory penalties.

Dominant End User Industries:

- Banking, Financial Services, and Insurance (BFSI): This sector leads in GDPR services adoption, accounting for an estimated 28% of the market. The highly sensitive nature of financial data and stringent regulatory oversight make BFSI organizations prime candidates for comprehensive GDPR solutions. Key drivers include preventing financial fraud, protecting customer financial information, and meeting regulatory compliance demands from bodies like the FCA and ESMA.

- Telecom and IT: Constituting approximately 20% of the market, this sector is a significant adopter of GDPR services, given their extensive collection and processing of customer data.

- Retail and Consumer Goods: With increasing online transactions and personalized marketing efforts, this sector is also a major user of GDPR services, estimated at 15% of the market.

- Healthcare and Life Sciences: Holding an estimated 12% share, this industry's reliance on sensitive patient data makes GDPR compliance paramount.

- Manufacturing: An emerging sector for GDPR services, with an estimated 8% market share, as industrial IoT and data analytics become more prevalent.

- Other End-user Industries: Account for the remaining market share, demonstrating the pervasive need for GDPR compliance across diverse business landscapes.

GDPR Services Industry Product Developments

The GDPR Services Industry is witnessing continuous innovation in product development, aiming to enhance data security, streamline compliance, and offer greater automation. Key product developments include AI-powered tools for automated data discovery and classification, advanced encryption techniques for data at rest and in transit, and integrated platforms that offer end-to-end data governance and privacy management. These innovations provide competitive advantages by reducing manual effort, minimizing human error, and ensuring real-time adherence to evolving privacy regulations. For instance, solutions now offer predictive analytics for identifying potential privacy risks before they materialize, and robust consent management platforms that provide granular control to end-users.

Key Drivers of GDPR Services Industry Growth

The growth of the GDPR Services Industry is propelled by a confluence of powerful factors. The ever-increasing volume and complexity of personal data being generated globally necessitate robust compliance frameworks. Heightened awareness of data privacy rights among consumers and citizens worldwide acts as a significant demand driver. Stringent regulatory mandates, such as GDPR, CCPA, and others, impose legal obligations on organizations, compelling them to invest in compliance solutions. Furthermore, the escalating frequency and impact of data breaches and cyberattacks underscore the critical need for advanced data protection measures. Technological advancements, including AI and ML, are enabling more efficient and automated GDPR services, making them more accessible and effective.

Challenges in the GDPR Services Industry Market

Despite its robust growth, the GDPR Services Industry faces several challenges. The complexity and ever-evolving nature of global data privacy regulations create a significant compliance hurdle for organizations. Keeping pace with these dynamic legal frameworks requires continuous monitoring and adaptation of services. The substantial cost associated with implementing and maintaining comprehensive GDPR compliance can be a deterrent, particularly for small and medium-sized enterprises (SMEs). Securing adequately skilled professionals in data privacy and cybersecurity remains a persistent challenge, leading to a talent gap. Furthermore, the risk of data breaches, despite significant investments in security, continues to pose a threat, necessitating ongoing vigilance and robust incident response planning.

Emerging Opportunities in GDPR Services Industry

The GDPR Services Industry is ripe with emerging opportunities. The increasing adoption of hybrid and multi-cloud environments creates a demand for specialized GDPR services that can manage data privacy across distributed infrastructure. The growing use of the Internet of Things (IoT) devices generates vast amounts of data, opening avenues for GDPR solutions focused on securing and managing consent for IoT data. Furthermore, the development of privacy-enhancing technologies (PETs), such as homomorphic encryption and differential privacy, presents opportunities for service providers to offer cutting-edge solutions that enable data utilization while preserving individual privacy. Strategic partnerships between GDPR service providers and cloud vendors, cybersecurity firms, and legal consultancies can further expand market reach and service offerings.

Leading Players in the GDPR Services Industry Sector

- Infosys Limited

- Micro Focus International PLC

- Wipro Limited

- Accenture PLC

- SecureWorks Inc

- IBM Corporation

- Capgemini SE

- Veritas Technologies LLC

- Microsoft Corporation

- Larsen & Toubro Infotech Limited

- Tata Consultancy Services Limited

- Amazon Web Services Inc

- DXC Technology Company

- Atos SE

- Oracle Corporation

- SAP SE

Key Milestones in GDPR Services Industry Industry

- November 2022: Informatica announced its Intelligent Data Management Cloud (IDMC) platform's availability for state and local governments, aiming to enhance public service efficiency. This development highlights the expanding reach of enterprise cloud data management solutions into public sector compliance.

- October 2022: Gravitee.io and Solace formed a strategic alliance to offer a unified API management experience for both synchronous RESTful and asynchronous event-driven APIs. This milestone underscores the growing importance of robust API management in the digital enterprise landscape, directly impacting data security and accessibility under GDPR.

Strategic Outlook for GDPR Services Industry Market

The strategic outlook for the GDPR Services Industry remains exceptionally strong, driven by an unwavering global focus on data privacy and security. Future growth will be accelerated by the continued evolution of data privacy regulations, prompting ongoing demand for compliance solutions. The increasing sophistication of cyber threats will necessitate more advanced and proactive security measures, creating opportunities for innovative service providers. The ongoing digital transformation across all industries, coupled with the widespread adoption of cloud and AI technologies, will further embed the need for integrated GDPR services. Strategic opportunities lie in developing specialized solutions for emerging sectors and technologies, expanding geographical reach, and fostering deeper integration with existing business workflows to offer a seamless and comprehensive compliance experience. The market is poised for sustained expansion as organizations worldwide prioritize building trust through robust data protection.

GDPR Services Industry Segmentation

-

1. Type of Deployment

- 1.1. On-premise

- 1.2. Cloud

-

2. Offering

- 2.1. Data Management

- 2.2. Data Discovery and Mapping

- 2.3. Data Governance

- 2.4. API Management

-

3. Organization size

- 3.1. Large Enterprises

- 3.2. Small and Medium-sized Enterprises

-

4. End User

- 4.1. Banking, Financial Services, and Insurance (BFSI)

- 4.2. Telecom and IT

- 4.3. Retail and Consumer Goods

- 4.4. Healthcare and Life Sciences

- 4.5. Manufacturing

- 4.6. Other End-user Industries

GDPR Services Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

GDPR Services Industry Regional Market Share

Geographic Coverage of GDPR Services Industry

GDPR Services Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 27.66% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 5.1.1. On-premise

- 5.1.2. Cloud

- 5.2. Market Analysis, Insights and Forecast - by Offering

- 5.2.1. Data Management

- 5.2.2. Data Discovery and Mapping

- 5.2.3. Data Governance

- 5.2.4. API Management

- 5.3. Market Analysis, Insights and Forecast - by Organization size

- 5.3.1. Large Enterprises

- 5.3.2. Small and Medium-sized Enterprises

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Banking, Financial Services, and Insurance (BFSI)

- 5.4.2. Telecom and IT

- 5.4.3. Retail and Consumer Goods

- 5.4.4. Healthcare and Life Sciences

- 5.4.5. Manufacturing

- 5.4.6. Other End-user Industries

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 6. Global GDPR Services Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 6.1.1. On-premise

- 6.1.2. Cloud

- 6.2. Market Analysis, Insights and Forecast - by Offering

- 6.2.1. Data Management

- 6.2.2. Data Discovery and Mapping

- 6.2.3. Data Governance

- 6.2.4. API Management

- 6.3. Market Analysis, Insights and Forecast - by Organization size

- 6.3.1. Large Enterprises

- 6.3.2. Small and Medium-sized Enterprises

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Banking, Financial Services, and Insurance (BFSI)

- 6.4.2. Telecom and IT

- 6.4.3. Retail and Consumer Goods

- 6.4.4. Healthcare and Life Sciences

- 6.4.5. Manufacturing

- 6.4.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 7. North America GDPR Services Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 7.1.1. On-premise

- 7.1.2. Cloud

- 7.2. Market Analysis, Insights and Forecast - by Offering

- 7.2.1. Data Management

- 7.2.2. Data Discovery and Mapping

- 7.2.3. Data Governance

- 7.2.4. API Management

- 7.3. Market Analysis, Insights and Forecast - by Organization size

- 7.3.1. Large Enterprises

- 7.3.2. Small and Medium-sized Enterprises

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Banking, Financial Services, and Insurance (BFSI)

- 7.4.2. Telecom and IT

- 7.4.3. Retail and Consumer Goods

- 7.4.4. Healthcare and Life Sciences

- 7.4.5. Manufacturing

- 7.4.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 8. Europe GDPR Services Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 8.1.1. On-premise

- 8.1.2. Cloud

- 8.2. Market Analysis, Insights and Forecast - by Offering

- 8.2.1. Data Management

- 8.2.2. Data Discovery and Mapping

- 8.2.3. Data Governance

- 8.2.4. API Management

- 8.3. Market Analysis, Insights and Forecast - by Organization size

- 8.3.1. Large Enterprises

- 8.3.2. Small and Medium-sized Enterprises

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Banking, Financial Services, and Insurance (BFSI)

- 8.4.2. Telecom and IT

- 8.4.3. Retail and Consumer Goods

- 8.4.4. Healthcare and Life Sciences

- 8.4.5. Manufacturing

- 8.4.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 9. Asia Pacific GDPR Services Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 9.1.1. On-premise

- 9.1.2. Cloud

- 9.2. Market Analysis, Insights and Forecast - by Offering

- 9.2.1. Data Management

- 9.2.2. Data Discovery and Mapping

- 9.2.3. Data Governance

- 9.2.4. API Management

- 9.3. Market Analysis, Insights and Forecast - by Organization size

- 9.3.1. Large Enterprises

- 9.3.2. Small and Medium-sized Enterprises

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Banking, Financial Services, and Insurance (BFSI)

- 9.4.2. Telecom and IT

- 9.4.3. Retail and Consumer Goods

- 9.4.4. Healthcare and Life Sciences

- 9.4.5. Manufacturing

- 9.4.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 10. Latin America GDPR Services Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 10.1.1. On-premise

- 10.1.2. Cloud

- 10.2. Market Analysis, Insights and Forecast - by Offering

- 10.2.1. Data Management

- 10.2.2. Data Discovery and Mapping

- 10.2.3. Data Governance

- 10.2.4. API Management

- 10.3. Market Analysis, Insights and Forecast - by Organization size

- 10.3.1. Large Enterprises

- 10.3.2. Small and Medium-sized Enterprises

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Banking, Financial Services, and Insurance (BFSI)

- 10.4.2. Telecom and IT

- 10.4.3. Retail and Consumer Goods

- 10.4.4. Healthcare and Life Sciences

- 10.4.5. Manufacturing

- 10.4.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 11. Middle East GDPR Services Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 11.1.1. On-premise

- 11.1.2. Cloud

- 11.2. Market Analysis, Insights and Forecast - by Offering

- 11.2.1. Data Management

- 11.2.2. Data Discovery and Mapping

- 11.2.3. Data Governance

- 11.2.4. API Management

- 11.3. Market Analysis, Insights and Forecast - by Organization size

- 11.3.1. Large Enterprises

- 11.3.2. Small and Medium-sized Enterprises

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Banking, Financial Services, and Insurance (BFSI)

- 11.4.2. Telecom and IT

- 11.4.3. Retail and Consumer Goods

- 11.4.4. Healthcare and Life Sciences

- 11.4.5. Manufacturing

- 11.4.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infosys Limite

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Micro Focus International PLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Wipro Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Accenture PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 SecureWorks Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 IBM Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Capgemini SE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Veritas Technologies LLC

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Microsoft Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Larsen & Toubro Infotech Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Tata Consultancy Services Limited

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Amazon Web Services Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 DXC Technology Company

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Atos SE

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Oracle Corporation

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 SAP SE

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Infosys Limite

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global GDPR Services Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 3: North America GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 4: North America GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 5: North America GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 6: North America GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 7: North America GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 8: North America GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 9: North America GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 13: Europe GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 14: Europe GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 15: Europe GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 16: Europe GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 17: Europe GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 18: Europe GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 19: Europe GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 20: Europe GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 23: Asia Pacific GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 24: Asia Pacific GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 25: Asia Pacific GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 26: Asia Pacific GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 27: Asia Pacific GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 28: Asia Pacific GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 29: Asia Pacific GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Asia Pacific GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 33: Latin America GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 34: Latin America GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 35: Latin America GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 36: Latin America GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 37: Latin America GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 38: Latin America GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 39: Latin America GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: Latin America GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 43: Middle East GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 44: Middle East GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 45: Middle East GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 46: Middle East GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 47: Middle East GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 48: Middle East GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 49: Middle East GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 50: Middle East GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 2: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 3: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 4: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 5: Global GDPR Services Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 7: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 8: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 9: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 12: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 13: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 14: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 15: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 17: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 18: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 19: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 20: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 22: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 23: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 24: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 25: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 27: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 28: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 29: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 30: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the GDPR Services Industry?

The projected CAGR is approximately 27.66%.

2. Which companies are prominent players in the GDPR Services Industry?

Key companies in the market include Infosys Limite, Micro Focus International PLC, Wipro Limited, Accenture PLC, SecureWorks Inc, IBM Corporation, Capgemini SE, Veritas Technologies LLC, Microsoft Corporation, Larsen & Toubro Infotech Limited, Tata Consultancy Services Limited, Amazon Web Services Inc, DXC Technology Company, Atos SE, Oracle Corporation, SAP SE.

3. What are the main segments of the GDPR Services Industry?

The market segments include Type of Deployment, Offering , Organization size, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.33 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Digital Transformation in the Financial Service Sector; Robust Roll Out of 5G.

6. What are the notable trends driving market growth?

Need for data security and privacy in the wake of a data breach.

7. Are there any restraints impacting market growth?

Lack of Awareness among Professionals.

8. Can you provide examples of recent developments in the market?

November 2022: Informatica, an enterprise cloud data management player, said the Intelligent Data Management Cloud (IDMC) platform is now available for state and local governments during the Informatica World Tour in Washington, DC. Informatica's IDMC platform, which currently processes over 44 trillion cloud transactions monthly, is intended to assist state and local government agencies in providing timely and efficient public services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "GDPR Services Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the GDPR Services Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the GDPR Services Industry?

To stay informed about further developments, trends, and reports in the GDPR Services Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence