Key Insights

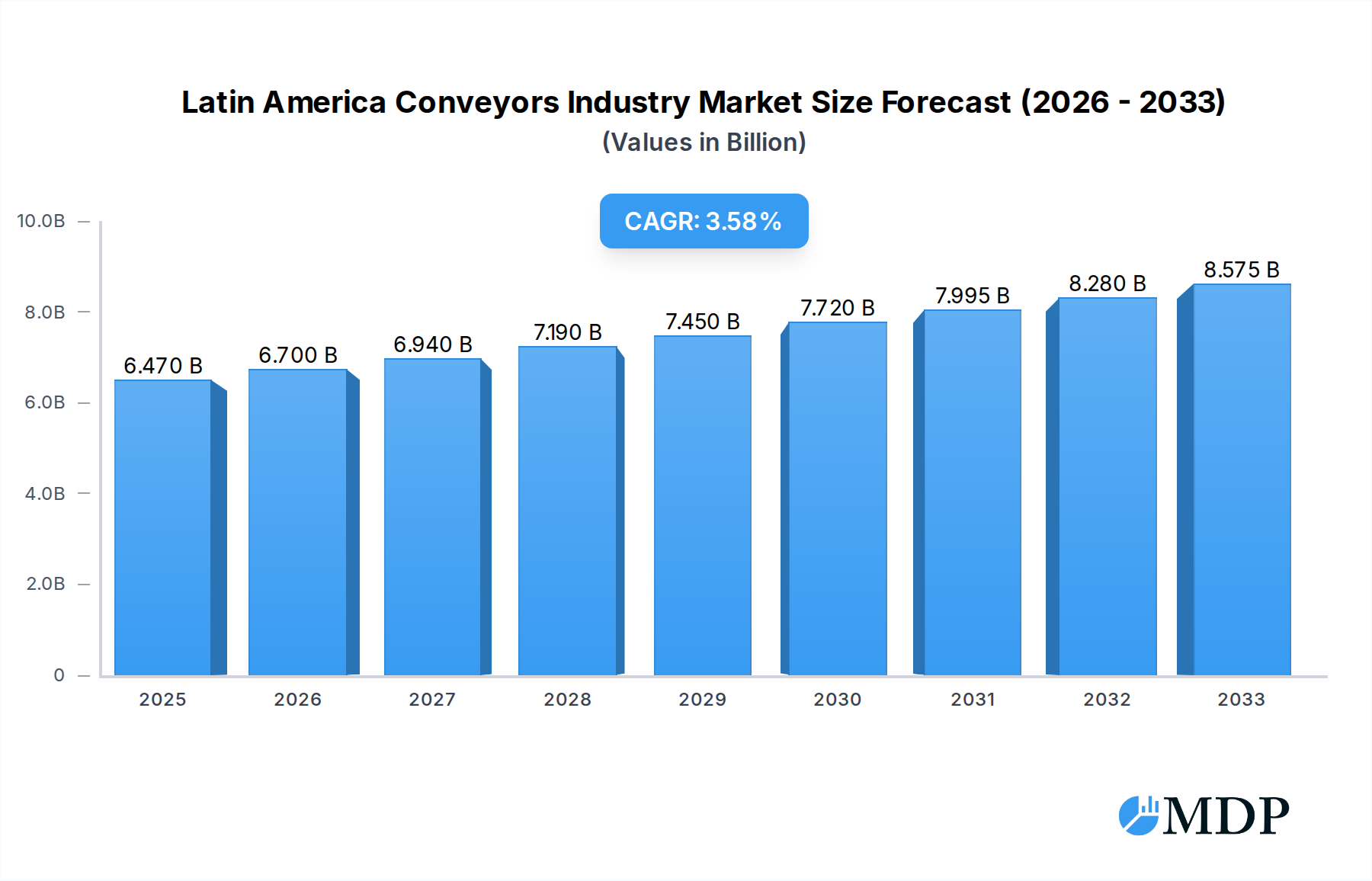

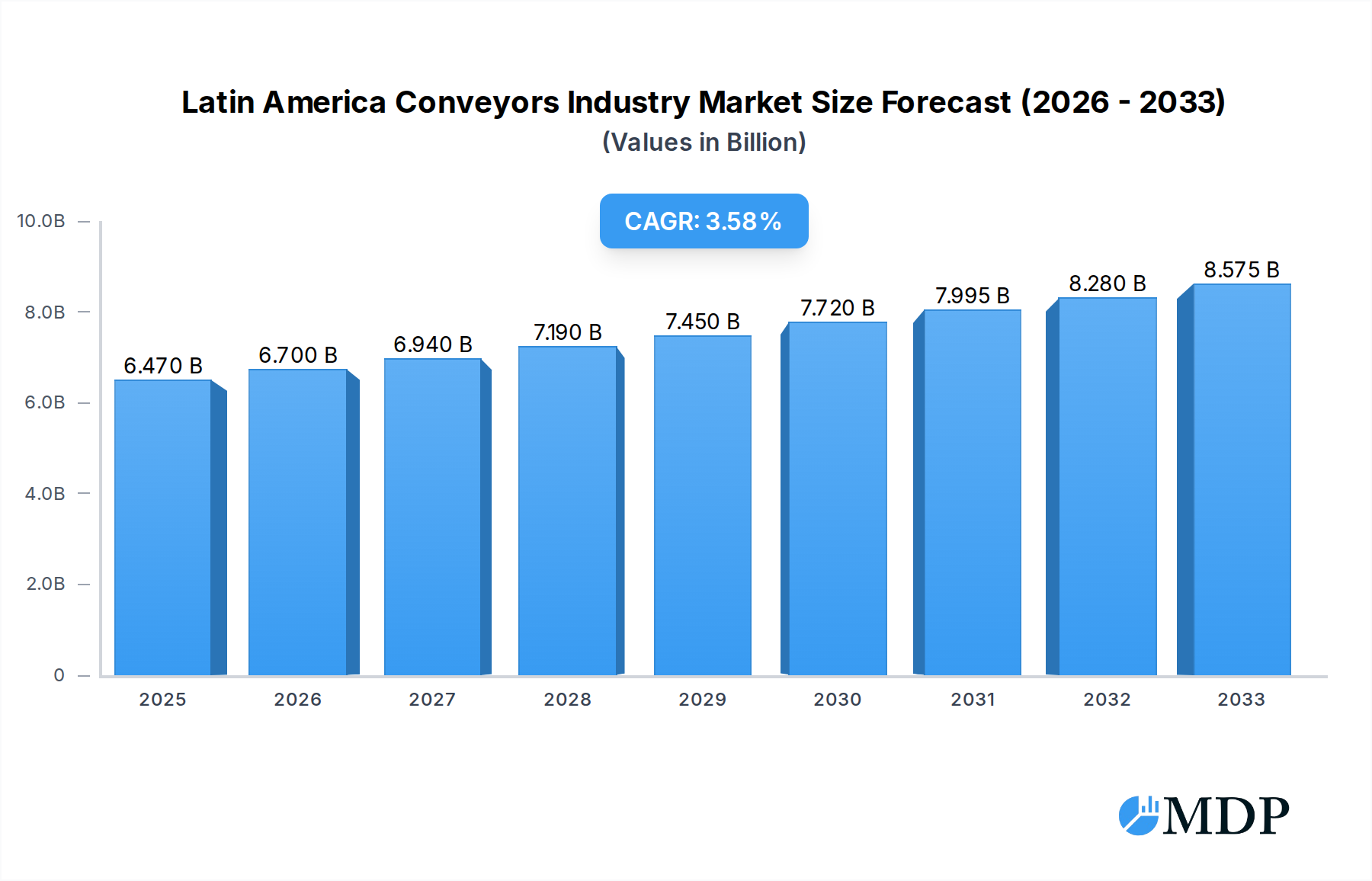

The Latin America conveyors industry is poised for robust growth, projected to reach USD 6.47 billion in 2025, with a Compound Annual Growth Rate (CAGR) of 3.74% from 2019 to 2033. This expansion is primarily fueled by the increasing adoption of automation and sophisticated material handling solutions across various end-user industries. Key growth drivers include the burgeoning e-commerce sector, demanding efficient order fulfillment and last-mile delivery, which in turn necessitates advanced conveyor systems in warehouses and distribution centers. The manufacturing sector's push for increased productivity, operational efficiency, and reduced labor costs further propels the demand for automated conveyor technologies. The automotive industry's ongoing investment in modern production lines and the food and beverage and pharmaceuticals sectors' stringent requirements for hygiene and contamination control also contribute significantly to market expansion. Latin America's developing infrastructure, coupled with government initiatives promoting industrialization and logistics modernization, creates a fertile ground for conveyor system integration.

Latin America Conveyors Industry Market Size (In Billion)

The market is segmented into various product types, including belt, roller, pallet, and overhead conveyors, each catering to specific material handling needs. Belt conveyors remain a dominant segment due to their versatility in handling a wide range of materials, while roller conveyors are favored for their suitability in unit load handling. Pallet and overhead conveyors are gaining traction in large-scale operations and complex facility layouts, respectively. End-user industries such as airports, retail, automotive, manufacturing, food and beverage, pharmaceuticals, and mining are the primary consumers of these conveyor systems. The competitive landscape features prominent global players like Metso Corporation, Murata Machinery Ltd, KUKA AG (Swisslog AG), BEUMER Group, and Daifuku Co Ltd, alongside regional specialists. These companies are focusing on developing innovative, energy-efficient, and integrated conveyor solutions to meet the evolving demands of the Latin American market, addressing challenges such as initial investment costs and the need for skilled maintenance personnel.

Latin America Conveyors Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Latin America Conveyors Industry, exploring market dynamics, key trends, leading segments, and future growth opportunities. With a study period spanning from 2019 to 2033, this report offers valuable insights for industry stakeholders, including manufacturers, suppliers, investors, and end-users. The global Latin America Conveyors Industry is projected to reach $XXX billion by 2033, growing at a CAGR of XX.XX% from 2025.

Latin America Conveyors Industry Market Dynamics & Concentration

The Latin America Conveyors Industry is characterized by a moderate to high market concentration, with key players like Metso Corporation, Murata Machinery Ltd, KNAAP AG, KUKA AG (Swisslog AG), BEUMER Group, Bastian Solutions Inc, SSI Schaefer AG, Kardex Group, Dorner Mfg Corp, Honeywell Intelligrated Inc, Daifuku Co Ltd, Mecalux SA, and Interroll Holding AG holding significant market share. Innovation drivers are primarily centered around automation, efficiency improvements, and integration of Industry 4.0 technologies, leading to enhanced product functionalities and operational benefits for end-users. Regulatory frameworks, while evolving, generally support industrial growth and automation adoption across various sectors. Product substitutes exist, particularly manual handling solutions in certain niche applications, but the demand for automated conveyor systems is steadily increasing due to their superior efficiency and scalability. End-user trends reveal a growing preference for smart, adaptable, and energy-efficient conveyor systems across diverse industries such as airports, retail, automotive, manufacturing, food and beverage, pharmaceuticals, and mining. Mergers and Acquisitions (M&A) activities are observed as companies seek to expand their product portfolios, geographical reach, and technological capabilities. Recent M&A deals, totaling XX in the historical period, indicate consolidation and strategic partnerships aimed at strengthening market positions. The estimated market share of leading players ranges from XX% to XX%.

Latin America Conveyors Industry Industry Trends & Analysis

The Latin America Conveyors Industry is experiencing robust growth, driven by a confluence of technological advancements, evolving consumer demands, and significant economic development across the region. The market is projected to reach $XXX billion by 2025, with a projected compound annual growth rate (CAGR) of XX.XX% during the forecast period of 2025–2033. This expansion is fueled by the increasing adoption of automation and robotics in warehousing, logistics, and manufacturing sectors. Technological disruptions, such as the integration of Artificial Intelligence (AI) for predictive maintenance, IoT for real-time monitoring, and advanced sensor technologies for enhanced safety and efficiency, are reshaping the conveyor system landscape. Consumer preferences are shifting towards faster delivery times and personalized shopping experiences, necessitating more efficient material handling and automated order fulfillment systems. This surge in e-commerce is a significant catalyst, particularly in the retail and food and beverage sectors, where conveyor systems play a pivotal role in managing high volumes of goods. Competitive dynamics are intensifying as both global and regional players vie for market dominance. Investments in research and development are focused on creating modular, flexible, and sustainable conveyor solutions. The market penetration of advanced conveyor technologies is estimated to be XX% in the base year of 2025, with projections to reach XX% by 2033. Key market drivers include government initiatives promoting industrialization, the need to reduce operational costs, and the continuous drive for enhanced productivity. The demand for specialized conveyor systems tailored to specific industry requirements, such as hygienic conveyors for food and pharmaceuticals or heavy-duty conveyors for mining, is also on the rise.

Leading Markets & Segments in Latin America Conveyors Industry

The Manufacturing segment is a dominant force within the Latin America Conveyors Industry, propelled by the region's growing industrial base and the increasing demand for efficient production lines and automated material handling solutions. Within the Product Type segmentation, Belt conveyors are anticipated to hold the largest market share, accounting for an estimated XX% of the market by 2025, due to their versatility and cost-effectiveness across various applications. However, Roller conveyors are also expected to witness significant growth, particularly in warehousing and logistics, driven by the boom in e-commerce. The End-User Industry segmentation sees Manufacturing and Retail as key growth engines.

- Manufacturing: Economic policies aimed at boosting domestic production, coupled with the need to enhance operational efficiency and reduce labor costs, are major drivers. Key economic policies supporting the manufacturing sector, such as tax incentives and investment promotion, are directly translating into higher demand for automated conveyor systems.

- Retail: The burgeoning e-commerce landscape across Latin America, fueled by increasing internet penetration and a growing middle class, is a significant catalyst. Retailers are investing heavily in sophisticated logistics and fulfillment centers, where advanced conveyor systems are indispensable for managing inventory, processing orders, and ensuring timely deliveries. Infrastructure development, including the expansion of warehousing and distribution networks, further supports this trend.

- Airport: With increasing air travel and cargo volumes, airports are investing in automated baggage handling and sorting systems, boosting demand for specialized conveyor solutions.

- Food and Beverage: Stringent hygiene regulations and the demand for efficient processing and packaging lines are driving the adoption of specialized food-grade conveyor systems.

- Automotive: The automotive sector's reliance on complex assembly lines and just-in-time manufacturing processes necessitates robust and integrated conveyor systems for material flow and vehicle movement.

The dominance of these segments is further amplified by substantial investments in infrastructure development and the ongoing pursuit of operational excellence by businesses across the region. The market penetration of advanced conveyor systems in the manufacturing and retail sectors is projected to be over XX% by 2033.

Latin America Conveyors Industry Product Developments

Product developments in the Latin America Conveyors Industry are increasingly focused on smart automation, enhanced safety features, and energy efficiency. Innovations include the integration of IoT sensors for real-time performance monitoring and predictive maintenance, AI-powered sorting and routing capabilities, and the development of modular and flexible conveyor designs that can be easily reconfigured to adapt to changing operational needs. Collaborative robots (cobots) are being integrated with conveyor systems to automate tasks such as picking and packing, further boosting efficiency. These advancements offer significant competitive advantages by reducing downtime, optimizing throughput, and minimizing operational costs for end-users across diverse sectors like warehousing, manufacturing, and food processing.

Key Drivers of Latin America Conveyors Industry Growth

The Latin America Conveyors Industry's growth is primarily propelled by several interconnected factors. Technological advancements, particularly in automation, robotics, and IoT, are driving the adoption of more sophisticated and efficient conveyor systems. The economic growth across the region, characterized by increasing industrialization and rising consumer demand, creates a fertile ground for material handling solutions. Furthermore, government initiatives aimed at boosting manufacturing output and improving logistics infrastructure are providing a significant impetus. For instance, investments in new industrial parks and free trade zones directly translate to increased demand for automated conveyor solutions. The growing e-commerce sector is also a major driver, necessitating faster and more efficient fulfillment processes.

Challenges in the Latin America Conveyors Industry Market

Despite the positive growth trajectory, the Latin America Conveyors Industry faces several challenges. High initial investment costs associated with advanced automated conveyor systems can be a barrier for some small and medium-sized enterprises (SMEs). Regulatory hurdles and complex import/export procedures in certain countries can also slow down market penetration and adoption. Skilled labor shortages for installation, maintenance, and operation of sophisticated systems pose another significant restraint. Supply chain disruptions, exacerbated by geopolitical factors and logistical complexities within the region, can impact project timelines and costs. The competitive pressure from lower-cost manual alternatives in less demanding applications also presents a challenge.

Emerging Opportunities in Latin America Conveyors Industry

Emerging opportunities in the Latin America Conveyors Industry are ripe for exploration. Technological breakthroughs in areas like AI-driven optimization, augmented reality for maintenance, and sustainable material handling solutions are creating new avenues for innovation and market differentiation. Strategic partnerships between conveyor manufacturers and logistics providers, as well as technology integrators, can unlock synergistic growth potential. Market expansion strategies, particularly into emerging economies within Latin America and catering to the specific needs of growing sectors like pharmaceuticals and mining, offer significant long-term growth prospects. The increasing focus on sustainability and energy efficiency presents an opportunity for companies developing eco-friendly conveyor solutions.

Leading Players in the Latin America Conveyors Industry Sector

- Metso Corporation

- Murata Machinery Ltd

- KNAAP AG

- KUKA AG (Swisslog AG)

- BEUMER Group

- Bastian Solutions Inc

- SSI Schaefer AG

- Kardex Group

- Dorner Mfg Corp

- Honeywell Intelligrated Inc

- Daifuku Co Ltd

- Mecalux SA

- Interroll Holding AG

Key Milestones in Latin America Conveyors Industry Industry

- 2019/2020: Increased adoption of automated guided vehicles (AGVs) and robotic arms integrated with conveyor systems to enhance warehouse efficiency.

- 2021/2022: Launch of advanced IoT-enabled conveyor systems for real-time monitoring and predictive maintenance, reducing downtime across various industries.

- 2023: Significant investments in sustainable conveyor technologies, focusing on energy-efficient motors and recyclable materials, driven by growing environmental concerns.

- 2024: Expansion of e-commerce logistics infrastructure across key Latin American countries, leading to increased demand for high-throughput conveyor solutions.

- Ongoing (2019-2033): Continuous mergers and acquisitions to consolidate market share and expand technological capabilities.

Strategic Outlook for Latin America Conveyors Industry Market

The strategic outlook for the Latin America Conveyors Industry is overwhelmingly positive, driven by a sustained demand for automation and efficiency. Growth accelerators include the continued digitalization of industries, the expansion of e-commerce, and proactive government support for industrial development. Companies that can offer intelligent, modular, and sustainable conveyor solutions, coupled with strong after-sales service and integration capabilities, are poised for significant success. Focusing on niche industry applications and leveraging emerging technologies will be crucial for maintaining a competitive edge. The market is expected to witness further consolidation and strategic alliances as players aim to capture a larger share of this expanding sector.

Latin America Conveyors Industry Segmentation

-

1. Product Type

- 1.1. Belt

- 1.2. Roller

- 1.3. Pallet

- 1.4. Overhead

-

2. End-User Industry

- 2.1. Airport

- 2.2. Retail

- 2.3. Automotive

- 2.4. Manufacturing

- 2.5. Food and Beverage

- 2.6. Pharmaceuticals

- 2.7. Mining

Latin America Conveyors Industry Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Conveyors Industry Regional Market Share

Geographic Coverage of Latin America Conveyors Industry

Latin America Conveyors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Belt

- 5.1.2. Roller

- 5.1.3. Pallet

- 5.1.4. Overhead

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Airport

- 5.2.2. Retail

- 5.2.3. Automotive

- 5.2.4. Manufacturing

- 5.2.5. Food and Beverage

- 5.2.6. Pharmaceuticals

- 5.2.7. Mining

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Latin America Conveyors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Belt

- 6.1.2. Roller

- 6.1.3. Pallet

- 6.1.4. Overhead

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Airport

- 6.2.2. Retail

- 6.2.3. Automotive

- 6.2.4. Manufacturing

- 6.2.5. Food and Beverage

- 6.2.6. Pharmaceuticals

- 6.2.7. Mining

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Metso Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Murata Machinery Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 KNAAP AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 KUKA AG (Swisslog AG)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BEUMER Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bastian Solutions Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 SSI Schaefer AG

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Kardex Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Dorner Mfg Corp

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Honeywell Intelligrated Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Daifuku Co Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Mecalux SA

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Interroll Holding AG

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Metso Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America Conveyors Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Latin America Conveyors Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Conveyors Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Latin America Conveyors Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 3: Latin America Conveyors Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Latin America Conveyors Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Latin America Conveyors Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 6: Latin America Conveyors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Brazil Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Argentina Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Chile Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Colombia Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Peru Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Venezuela Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Ecuador Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Bolivia Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Paraguay Latin America Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Conveyors Industry?

The projected CAGR is approximately 4.42%.

2. Which companies are prominent players in the Latin America Conveyors Industry?

Key companies in the market include Metso Corporation, Murata Machinery Ltd, KNAAP AG, KUKA AG (Swisslog AG), BEUMER Group, Bastian Solutions Inc, SSI Schaefer AG, Kardex Group, Dorner Mfg Corp, Honeywell Intelligrated Inc, Daifuku Co Ltd, Mecalux SA, Interroll Holding AG.

3. What are the main segments of the Latin America Conveyors Industry?

The market segments include Product Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.92 billion as of 2022.

5. What are some drivers contributing to market growth?

; Rising Industrial and Infrastructural Development Activities in the Region.

6. What are the notable trends driving market growth?

Mining is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

; High Initial Investments.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Conveyors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Conveyors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Conveyors Industry?

To stay informed about further developments, trends, and reports in the Latin America Conveyors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence