Key Insights

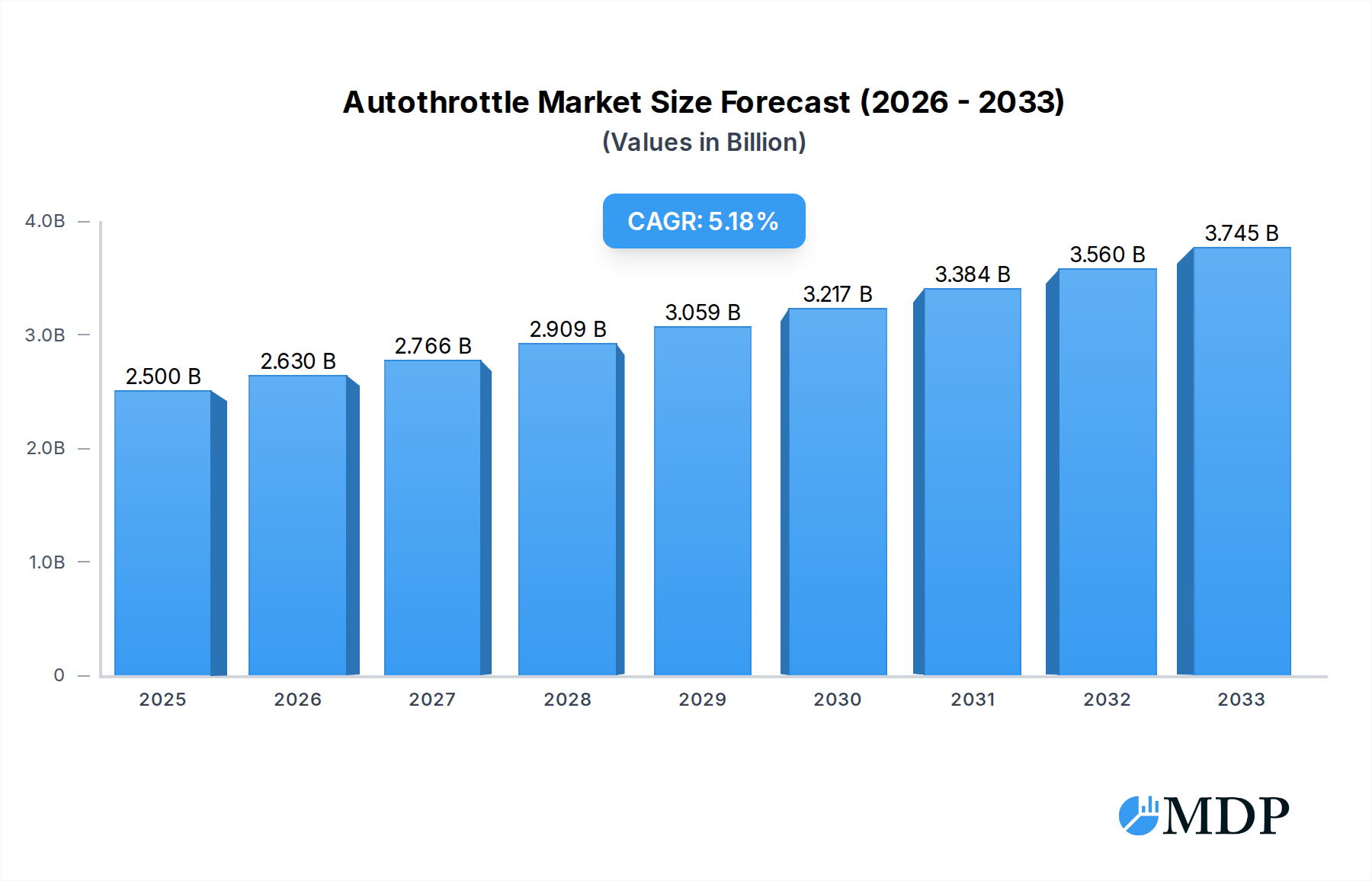

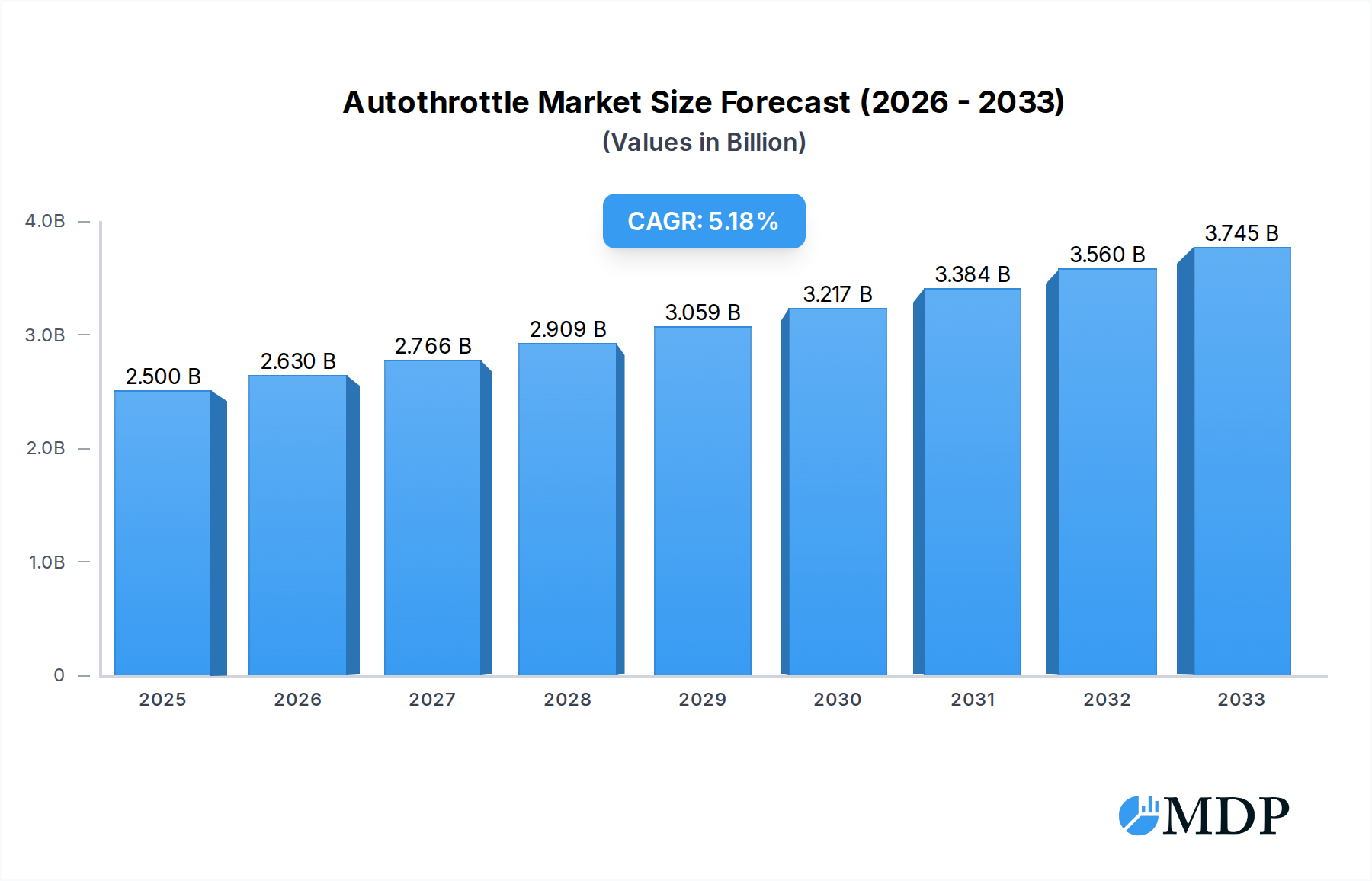

The global Autothrottle market is poised for robust expansion, estimated to reach USD 2.5 billion in 2025. Driven by a projected Compound Annual Growth Rate (CAGR) of 5.2% from 2025 to 2033, this market will witness significant growth in value. This upward trajectory is primarily fueled by increasing demand for advanced safety features and operational efficiency in aviation. The rising complexity of modern aircraft and the continuous pursuit of enhanced pilot workload reduction are key catalysts. Furthermore, advancements in automation technology and the integration of sophisticated flight management systems are creating new opportunities for autothrottle systems. The growing fleet of high-end piston aircraft and turboprop aircraft, particularly in emerging aviation markets, will also contribute to market expansion as manufacturers increasingly adopt these systems as standard or optional equipment.

Autothrottle Market Size (In Billion)

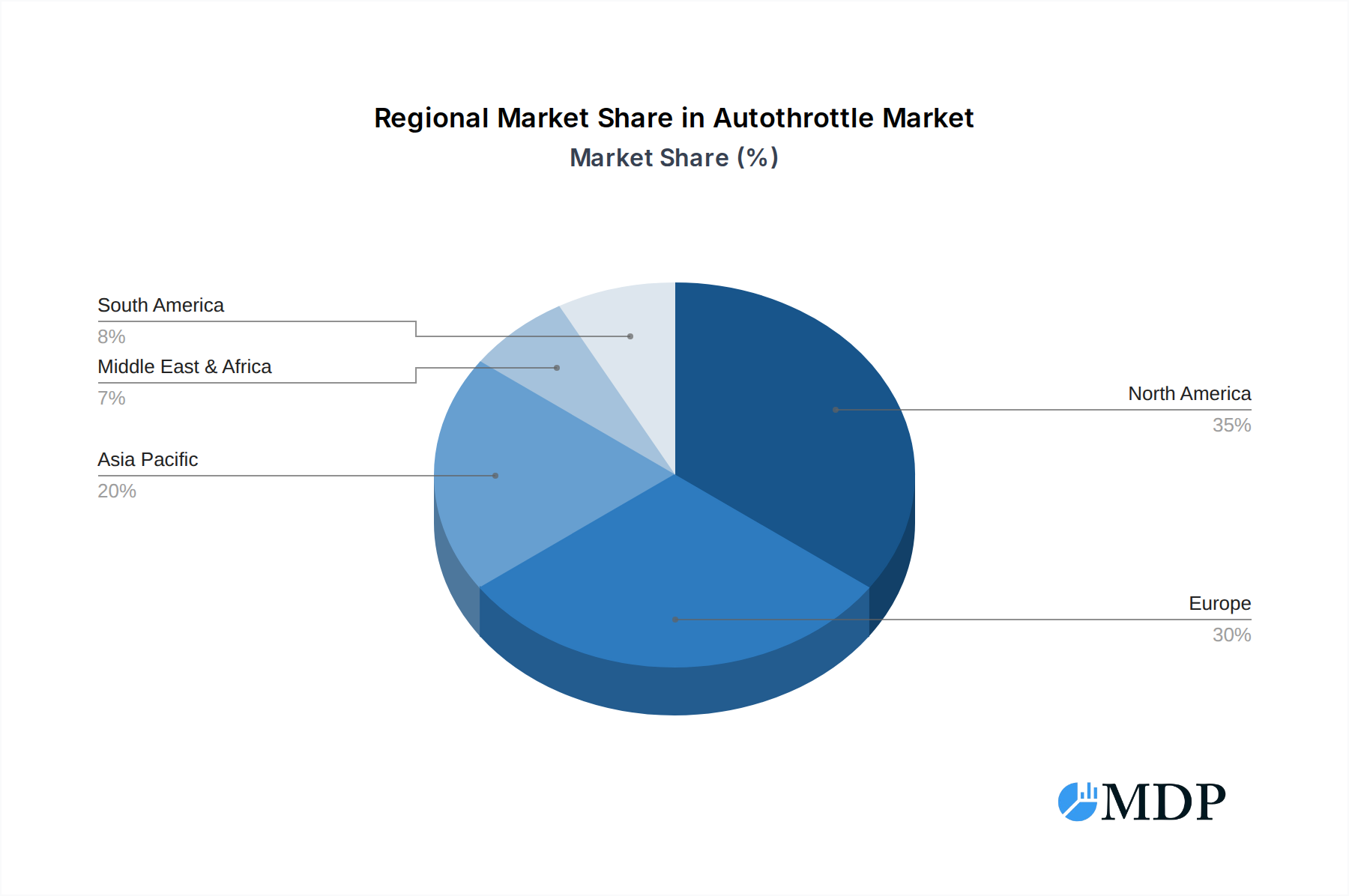

The market is segmented into front drive systems and rear drive systems, catering to diverse aircraft architectures and operational needs. While the adoption of autothrottle systems is a global phenomenon, certain regions are expected to lead in market penetration. North America and Europe, with their mature aviation industries and stringent safety regulations, are anticipated to maintain dominant market shares. However, the Asia Pacific region presents substantial growth potential due to the rapid expansion of its aviation sector, increasing aircraft production, and a growing emphasis on upgrading existing fleets with advanced technologies. Innovations in sensor technology, control algorithms, and predictive maintenance are expected to further enhance the performance and reliability of autothrottle systems, addressing potential market restraints related to integration complexity and initial investment costs.

Autothrottle Company Market Share

Autothrottle Market Analysis: A Comprehensive Report (2019-2033)

This in-depth report provides a definitive analysis of the global autothrottle market, projecting its trajectory from 2019 to 2033. We delve into the intricate dynamics, emerging trends, leading players, and pivotal milestones shaping this crucial aviation technology sector. With a base year of 2025 and a forecast period extending to 2033, this study offers unparalleled insights for industry stakeholders, investors, and decision-makers. The report leverages high-traffic keywords such as "aviation technology," "flight automation," "aircraft systems," "aerospace market," and "pilot assistance" to maximize search visibility.

Autothrottle Market Dynamics & Concentration

The global autothrottle market exhibits a moderate concentration, driven by a complex interplay of technological innovation, stringent regulatory frameworks, and evolving end-user preferences. The increasing demand for enhanced flight safety and operational efficiency continues to fuel innovation, with companies like Innovative Solutions & Support, Inc. (IS&S) and Sensata at the forefront of developing advanced autothrottle systems. The market is characterized by continuous research and development in areas such as predictive engine management and enhanced pilot interfaces. Regulatory bodies are actively involved in setting standards for autothrottle performance and safety, influencing product development cycles and market entry barriers. While direct product substitutes are limited, advancements in fully autonomous flight systems represent a long-term disruptive threat. End-user trends, particularly within the high-end piston and turboprop aircraft segments, are increasingly emphasizing user-friendliness and seamless integration. Mergers and acquisitions (M&A) activities, while not dominant, play a role in market consolidation and the acquisition of specialized technologies. For instance, there have been approximately XX M&A deals observed during the historical period (2019-2024), contributing to the evolving competitive landscape. The estimated market share of the top five players is expected to hover around XX% by 2025, indicating a degree of competitive fragmentation.

Autothrottle Industry Trends & Analysis

The autothrottle industry is poised for significant expansion, driven by a confluence of factors that underscore the growing importance of automation in aviation. The primary growth drivers include the relentless pursuit of enhanced flight safety, the imperative to optimize fuel efficiency, and the increasing need to reduce pilot workload, especially during critical flight phases. Technological disruptions are rapidly transforming the sector, with the integration of artificial intelligence (AI) and machine learning (ML) into autothrottle algorithms promising more sophisticated and adaptive flight control. These advancements enable autothrottles to anticipate engine performance deviations and proactively adjust thrust, thereby minimizing the risk of engine exceedances and improving overall engine lifespan. Consumer preferences are shifting towards more intuitive and user-friendly interfaces, demanding autothrottle systems that offer seamless integration with existing cockpit avionics and provide clear, actionable information to pilots. The competitive dynamics are intensifying, with established aerospace manufacturers and specialized avionics providers vying for market share. Market penetration for advanced autothrottle systems is steadily increasing across both new aircraft production and retrofitting of existing fleets. The projected Compound Annual Growth Rate (CAGR) for the autothrottle market is estimated to be XX% during the forecast period (2025–2033), a testament to its robust growth trajectory. This growth is underpinned by a projected market size of over $XX billion by 2025, with a further expansion to exceed $XX billion by 2033. The increasing sophistication of aircraft design and the growing complexity of air traffic management also contribute to the demand for advanced autothrottle capabilities. Furthermore, the ongoing evolution of flight management systems (FMS) and their integration with autothrottle technology are creating synergistic benefits, further bolstering market expansion.

Leading Markets & Segments in Autothrottle

The autothrottle market's dominance is characterized by the strong performance of specific geographical regions and application segments. North America currently stands as the leading market, propelled by its robust aerospace manufacturing base, extensive fleet of high-end piston and turboprop aircraft, and a strong regulatory environment that prioritizes safety and technological adoption. The United States, in particular, represents a significant portion of this market due to the high concentration of general aviation activity and a substantial aftermarket for aircraft upgrades and retrofits.

Key Drivers of Dominance in North America:

- Economic Policies: Favorable government incentives and investment in aerospace R&D foster innovation and market growth.

- Infrastructure: A well-developed network of airports and maintenance facilities supports the adoption and servicing of advanced aircraft systems.

- Technological Adoption: A culture of early adoption of new technologies in the general aviation sector drives demand for sophisticated autothrottle systems.

- Regulatory Framework: Strict safety regulations implemented by the FAA (Federal Aviation Administration) mandate and encourage the use of advanced safety features, including autothrottles.

Within the application segments, High-End Piston Aircraft exhibit particularly strong demand. These aircraft, often utilized for private aviation, business travel, and flight training, benefit significantly from the enhanced safety, reduced workload, and improved fuel efficiency that autothrottles provide. The pilot assistance capabilities offered by autothrottles are highly valued by private pilots and those operating in complex airspace.

The Turboprop Aircraft segment also represents a substantial and growing market. These aircraft, widely used for regional airline operations, corporate transport, and special mission roles, are increasingly equipped with advanced autothrottle systems to enhance operational efficiency and safety on longer flights and at higher altitudes. The ability of autothrottles to precisely manage engine power in varying atmospheric conditions is a critical advantage for turboprop operations.

In terms of Types, the Front Drive System is currently the more prevalent configuration, particularly in legacy aircraft and certain new designs. However, the Rear Drive System is gaining traction due to its potential for improved weight distribution and aerodynamic efficiency in specific aircraft designs. The choice between these systems often depends on the specific aircraft architecture and the manufacturer's design philosophy. The continuous evolution of aircraft design and the demand for optimized performance will likely see increased innovation and adoption of both front and rear drive systems.

Autothrottle Product Developments

Recent product developments in the autothrottle market are centered on enhancing precision, reliability, and pilot interface. Innovations include advanced predictive algorithms that anticipate engine needs, leading to smoother operations and reduced wear. The integration of AI and machine learning is enabling autothrottles to adapt to a wider range of flight conditions and pilot inputs, offering superior performance. Competitive advantages are being gained through smaller, lighter, and more energy-efficient system designs, as well as improved diagnostics and self-monitoring capabilities. These technological advancements directly address the increasing demand for enhanced safety and operational efficiency in both new aircraft and retrofit applications.

Key Drivers of Autothrottle Growth

The autothrottle market's growth is primarily propelled by several interconnected factors. Technologically, advancements in digital control systems, AI, and sensor technology are enabling more precise and reliable autothrottle performance. Economically, the increasing volume of air traffic and the persistent focus on operational cost reduction, particularly fuel efficiency, make autothrottles a vital component. Regulatory mandates and recommendations from aviation authorities worldwide, aimed at enhancing flight safety and reducing pilot error, act as significant catalysts. For example, the continuous push for IFR (Instrument Flight Rules) proficiency and safety enhancements in general aviation directly supports the adoption of autothrottle systems.

Challenges in the Autothrottle Market

Despite its growth potential, the autothrottle market faces several challenges. Regulatory hurdles, while driving safety, can also lead to extended certification processes for new technologies, increasing development costs and time-to-market. Supply chain disruptions, as evidenced by recent global events, can impact the availability of critical components and lead to production delays. Intense competitive pressures among established players and emerging technology providers can drive down profit margins. The cost of integrating advanced autothrottle systems, especially for older aircraft during retrofitting, can also be a barrier for some operators. The estimated impact of these challenges on market growth could be a reduction of XX% in projected revenue if not adequately addressed.

Emerging Opportunities in Autothrottle

The autothrottle sector is ripe with emerging opportunities, driven by technological breakthroughs and strategic market expansion. The increasing trend towards electric and hybrid-electric aircraft presents a significant avenue for innovation, requiring specialized autothrottle solutions for these novel propulsion systems. Strategic partnerships between autothrottle manufacturers and aircraft OEMs (Original Equipment Manufacturers) are crucial for seamless integration and co-development. Furthermore, the growing demand for enhanced flight training simulators that accurately replicate autothrottle functionality offers a niche but important market expansion strategy. The global expansion into emerging aviation markets, with their increasing adoption of modern aircraft, also represents a substantial long-term growth catalyst.

Leading Players in the Autothrottle Sector

- Innovative Solutions & Support, Inc. (IS&S)

- Sensata

- Honeywell International Inc.

- Garmin Ltd.

- BendixKing

- Collins Aerospace

Key Milestones in Autothrottle Industry

- 2019: Introduction of AI-enhanced autothrottle algorithms by leading manufacturers.

- 2020: Increased integration of autothrottles in newly designed turboprop aircraft.

- 2021: Focus on developing lighter and more power-efficient autothrottle systems.

- 2022: Advancements in predictive engine monitoring capabilities integrated with autothrottles.

- 2023: Enhanced pilot interface designs to improve intuitiveness and reduce workload.

- 2024 (Expected): Further exploration of autothrottle integration in electric and hybrid-electric aircraft prototypes.

Strategic Outlook for Autothrottle Market

The strategic outlook for the autothrottle market is overwhelmingly positive, driven by sustained demand for enhanced aviation safety and operational efficiency. Growth accelerators include the ongoing evolution of flight automation technologies, such as AI and advanced sensor fusion, which will enable even more sophisticated and predictive autothrottle functions. The increasing adoption of these systems in the general aviation segment, particularly for high-end piston and turboprop aircraft, will continue to be a key growth driver. Strategic opportunities lie in the development of modular and scalable autothrottle solutions that can be adapted to a wide range of aircraft types and retrofitting needs, as well as exploring partnerships for integration into emerging aircraft technologies. The market is expected to witness continuous innovation, leading to more integrated and intelligent flight control systems.

Autothrottle Segmentation

-

1. Application

- 1.1. High-End Piston Aircraft

- 1.2. Turboprop Aircraft

-

2. Types

- 2.1. Front Drive System

- 2.2. Rear Drive System

Autothrottle Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Autothrottle Regional Market Share

Geographic Coverage of Autothrottle

Autothrottle REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Autothrottle Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. High-End Piston Aircraft

- 5.1.2. Turboprop Aircraft

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Front Drive System

- 5.2.2. Rear Drive System

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Autothrottle Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. High-End Piston Aircraft

- 6.1.2. Turboprop Aircraft

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Front Drive System

- 6.2.2. Rear Drive System

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Autothrottle Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. High-End Piston Aircraft

- 7.1.2. Turboprop Aircraft

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Front Drive System

- 7.2.2. Rear Drive System

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Autothrottle Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. High-End Piston Aircraft

- 8.1.2. Turboprop Aircraft

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Front Drive System

- 8.2.2. Rear Drive System

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Autothrottle Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. High-End Piston Aircraft

- 9.1.2. Turboprop Aircraft

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Front Drive System

- 9.2.2. Rear Drive System

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Autothrottle Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. High-End Piston Aircraft

- 10.1.2. Turboprop Aircraft

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Front Drive System

- 10.2.2. Rear Drive System

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Innovative Solutions & Support

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Inc. (IS&S)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sensata

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.1 Innovative Solutions & Support

List of Figures

- Figure 1: Global Autothrottle Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Autothrottle Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Autothrottle Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Autothrottle Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Autothrottle Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Autothrottle Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Autothrottle Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Autothrottle Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Autothrottle Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Autothrottle Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Autothrottle Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Autothrottle Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Autothrottle Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Autothrottle Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Autothrottle Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Autothrottle Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Autothrottle Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Autothrottle Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Autothrottle Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Autothrottle Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Autothrottle Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Autothrottle Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Autothrottle Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Autothrottle Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Autothrottle Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Autothrottle Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Autothrottle Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Autothrottle Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Autothrottle Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Autothrottle Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Autothrottle Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autothrottle Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Autothrottle Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Autothrottle Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Autothrottle Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Autothrottle Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Autothrottle Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Autothrottle Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Autothrottle Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Autothrottle Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Autothrottle Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Autothrottle Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Autothrottle Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Autothrottle Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Autothrottle Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Autothrottle Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Autothrottle Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Autothrottle Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Autothrottle Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Autothrottle Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autothrottle?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Autothrottle?

Key companies in the market include Innovative Solutions & Support, Inc. (IS&S), Sensata.

3. What are the main segments of the Autothrottle?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autothrottle," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autothrottle report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autothrottle?

To stay informed about further developments, trends, and reports in the Autothrottle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence