Key Insights

The agricultural containers market, valued at $163.5 billion in 2024, is projected for substantial growth, with a Compound Annual Growth Rate (CAGR) of 4.5% from 2024 to 2033. This expansion is driven by increasing global food demand and the adoption of advanced farming methods. Specialized containers are essential for the efficient handling and transportation of agricultural inputs like pesticides, fertilizers, and seeds. The market also benefits from the rising preference for sustainable packaging solutions, including biodegradable and recycled materials, spurred by environmental consciousness and regulatory mandates.

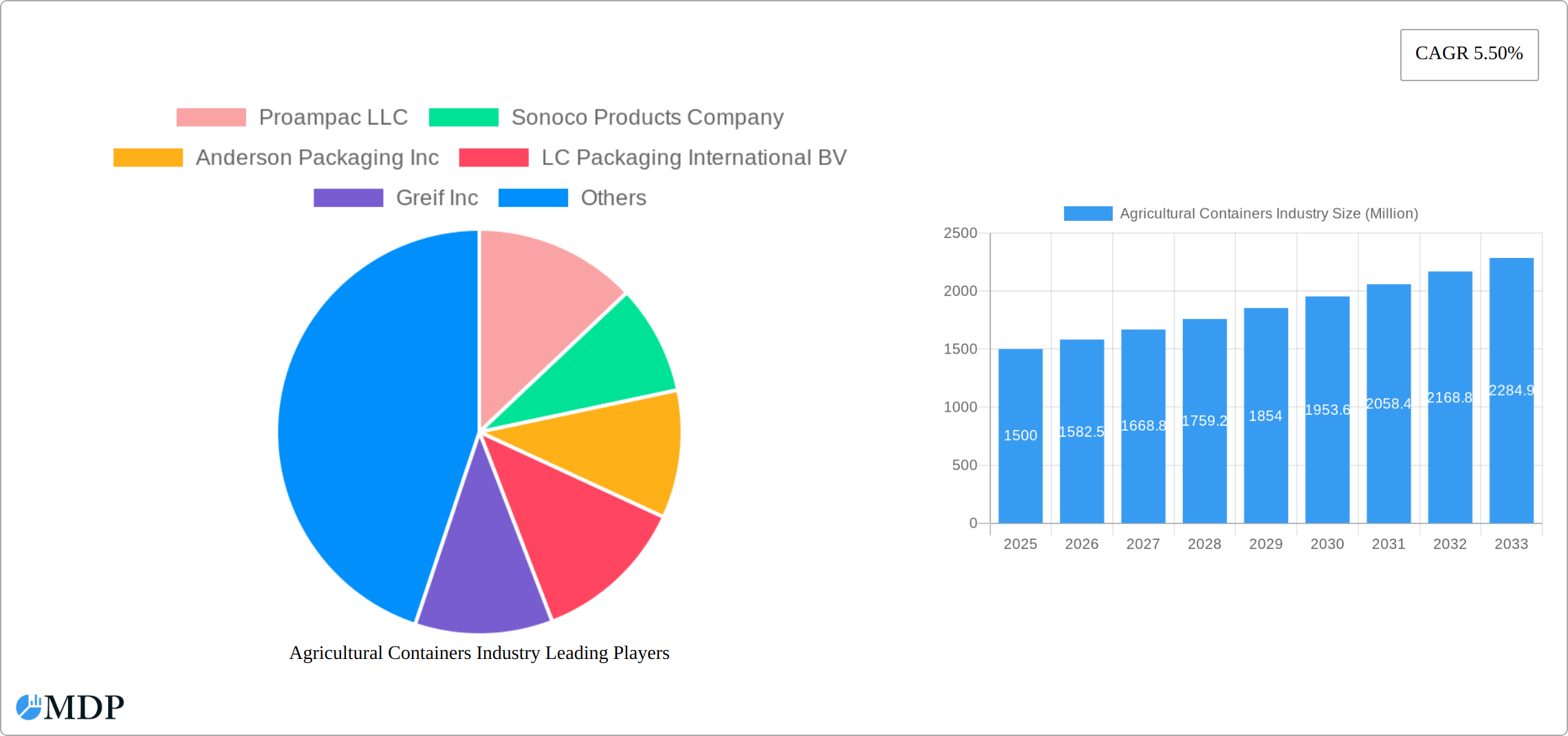

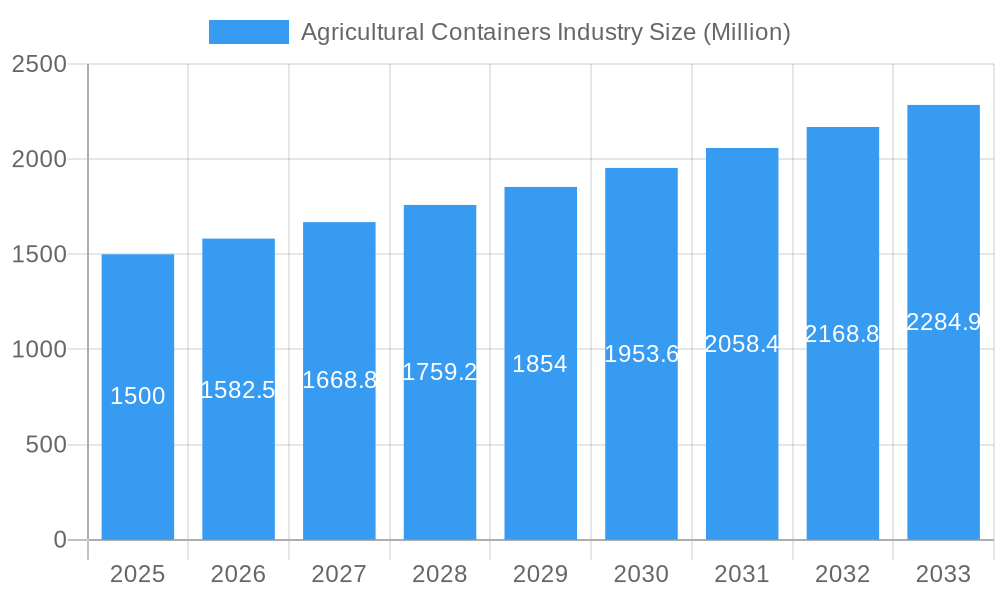

Agricultural Containers Industry Market Size (In Billion)

Market segmentation highlights opportunities in various material types, applications, and product categories. While plastic containers lead due to their cost-effectiveness, sustainable materials like paperboard and composites are gaining traction. Packaging for pesticides and fertilizers shows significant growth. Geographically, North America and Europe are key markets, with Asia-Pacific anticipated to experience rapid expansion driven by agricultural development and infrastructure investment. The competitive landscape features established global players and regional companies, fostering product innovation and strategic collaborations to enhance market position.

Agricultural Containers Industry Company Market Share

Agricultural Containers Industry: Market Report 2019-2033

This comprehensive report provides a detailed analysis of the Agricultural Containers Industry, covering market dynamics, leading players, key trends, and future growth prospects from 2019 to 2033. With a focus on actionable insights and data-driven forecasts, this report is an essential resource for industry stakeholders, investors, and businesses seeking to navigate this dynamic sector. The report incorporates a detailed analysis of market segments including By Material Type (Plastic, Metal, Paper and Paperboard, Composite Materials, Other Materials), By Application Type (Pesticides, Fertilizers, Seeds, Other Types), and By Product Type (Bags & Sacks, Bulk Containers, Pouches, Containers, Other Products). The study period is 2019-2033, with 2025 as the base and estimated year. The forecast period spans 2025-2033, and the historical period covers 2019-2024.

Agricultural Containers Industry Market Dynamics & Concentration

The agricultural containers market, valued at xx Million in 2024, is experiencing moderate consolidation. Market concentration is relatively high, with the top 10 players holding an estimated xx% market share in 2024. This is driven by economies of scale and increasing demand for specialized packaging solutions. Innovation is fueled by the need for sustainable and efficient packaging, alongside regulatory pressures towards reduced environmental impact. Stringent regulations concerning material safety and recyclability are shaping the market landscape. Key product substitutes include reusable containers and alternative packaging materials. End-user trends lean towards eco-friendly options and optimized supply chain solutions. The market has witnessed a significant number of mergers and acquisitions (M&A) in recent years, approximately xx deals between 2019 and 2024, reflecting strategic consolidation and expansion efforts.

- Market Share: Top 10 players hold approximately xx% (2024).

- M&A Activity: Approximately xx deals between 2019 and 2024.

- Innovation Drivers: Sustainability, efficiency, regulatory compliance.

- Regulatory Frameworks: Focus on material safety and recyclability.

Agricultural Containers Industry Industry Trends & Analysis

The agricultural containers market is projected to register a CAGR of xx% during the forecast period (2025-2033), driven by factors such as increasing agricultural production, rising demand for food globally, and the growing adoption of advanced packaging technologies. Technological advancements in material science are enabling the development of more durable, lightweight, and sustainable packaging solutions. Consumer preferences are shifting towards eco-friendly and recyclable options, pushing manufacturers to adopt sustainable practices. Intense competition among major players is driving innovation and efficiency improvements. Market penetration of sustainable packaging solutions is increasing at a rate of approximately xx% annually.

Leading Markets & Segments in Agricultural Containers Industry

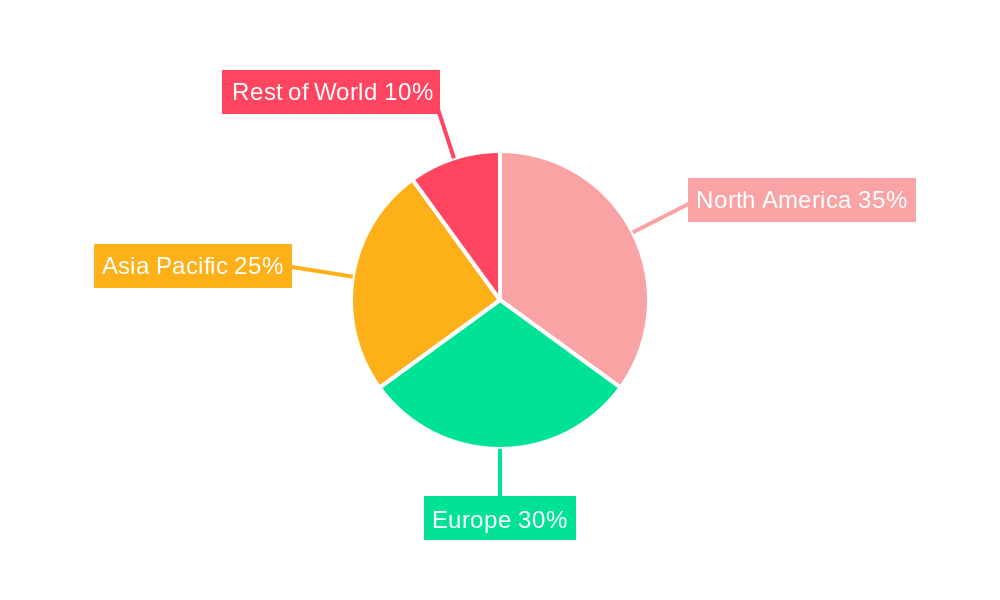

The North American region currently holds the largest market share, driven by factors including advanced agricultural practices, high agricultural output, and robust regulatory frameworks. Within segments:

By Material Type: Plastic dominates the market due to its versatility and cost-effectiveness. However, the demand for sustainable materials like paper and paperboard is rapidly increasing.

By Application Type: Fertilizers represent the largest application segment due to high volume usage.

By Product Type: Bags & sacks (plastic & paper) comprise the largest segment, followed by bulk containers (drums & IBCs).

Key Drivers:

- North America: High agricultural output, advanced farming practices, strong regulatory support.

- Europe: Growing demand for sustainable packaging, stringent environmental regulations.

- Asia-Pacific: Rapid agricultural expansion, rising food consumption.

Agricultural Containers Industry Product Developments

Recent product innovations focus on enhancing durability, improving barrier properties, and increasing sustainability. This includes the development of biodegradable and compostable materials, as well as improved designs that minimize material usage and optimize supply chain efficiency. Technological trends are focused on smart packaging solutions and integrated traceability systems. The market fit for these innovations is strong, driven by both consumer and regulatory demand.

Key Drivers of Agricultural Containers Industry Growth

The agricultural containers market is experiencing robust expansion, propelled by a confluence of critical factors that are reshaping how food and agricultural products are stored, transported, and protected. These drivers are indicative of a dynamic industry responding to global needs and technological evolution.

- Escalating Global Food Demand: With a continuously growing global population, the imperative to enhance agricultural output and minimize post-harvest losses is more pronounced than ever. This surge in demand directly translates to a heightened need for reliable, efficient, and protective packaging solutions that can maintain product integrity from farm to fork.

- Pioneering Technological Advancements: The industry is witnessing remarkable innovation fueled by breakthroughs in materials science and manufacturing processes. The development of advanced polymers, biodegradable materials, and intelligent packaging technologies is leading to containers that offer enhanced durability, improved barrier properties, extended shelf life, and reduced environmental impact.

- Supportive Government Policies and Sustainability Initiatives: Governments worldwide are increasingly recognizing the importance of sustainable practices in agriculture and supply chains. Favorable policies, incentives for eco-friendly packaging, and a growing emphasis on circular economy principles are actively promoting the adoption of recyclable, compostable, and reusable agricultural containers, thereby stimulating market growth.

- Focus on Supply Chain Efficiency and Traceability: The drive for greater efficiency and transparency throughout the agricultural supply chain is also a significant contributor. Advanced container designs that facilitate easier handling, stacking, and identification, coupled with the integration of tracking technologies, are becoming essential for optimizing logistics and ensuring product traceability.

Challenges in the Agricultural Containers Industry Market

Despite the promising growth trajectory, the agricultural containers industry faces a distinct set of hurdles that demand strategic navigation and innovative solutions. Addressing these challenges is crucial for sustained success and market leadership.

- Volatile Raw Material Prices: The industry's reliance on various raw materials, including plastics, paper, and metals, makes it susceptible to price fluctuations. Global economic conditions, geopolitical events, and supply chain disruptions can lead to unpredictable increases in input costs, impacting production expenses and profit margins for manufacturers.

- Stringent and Evolving Environmental Regulations: As environmental consciousness grows, so do the regulations governing packaging materials and disposal. Manufacturers must continually adapt to stricter standards for recyclability, biodegradability, and the reduction of single-use plastics, requiring significant investment in research, development, and compliant manufacturing processes.

- Intense Market Competition and Consolidation: The agricultural containers market is characterized by a high level of competition, with a mix of large multinational corporations, regional players, and emerging niche manufacturers. This competitive landscape can lead to price pressures and necessitates continuous innovation and cost optimization to maintain market share.

- Supply Chain Complexity and Infrastructure Limitations: The global nature of agricultural production and distribution presents complex logistical challenges. Inadequate infrastructure in certain regions, coupled with the need for specialized handling and transportation of agricultural goods, can pose significant operational difficulties for container providers.

- Consumer Demand for Sustainable and Safe Packaging: While a driver for innovation, evolving consumer preferences for sustainable and safe packaging also presents a challenge. Meeting these demands requires ongoing investment in research and development to offer a wider range of eco-friendly and food-grade compliant solutions.

Emerging Opportunities in Agricultural Containers Industry

Long-term growth is driven by opportunities in:

- Biodegradable and compostable packaging: Growing demand for environmentally friendly solutions.

- Smart packaging solutions: Integration of technology for traceability and supply chain optimization.

- Expansion into emerging markets: Untapped potential in developing economies with growing agricultural sectors.

Leading Players in the Agricultural Containers Industry Sector

- Proampac LLC

- Sonoco Products Company

- Anderson Packaging Inc

- LC Packaging International BV

- Greif Inc

- Amcor plc

- NNZ Group

- Mondi Group

- Pactiv LLC

- BAG Corporation

- Flexpack FIBC

- Western Packaging

- Novolex Holdings, LLC

- DS Smith plc

- Berry Global Group, Inc.

Key Milestones in Agricultural Containers Industry Industry

- May 2022: Zeus Packaging's strategic acquisition of Agri-Flex for approximately USD 36.88 Million significantly broadened its portfolio and market presence within the agricultural packaging sector, underscoring a trend of consolidation and expansion.

- March 2022: The collaborative efforts between StenCo LLC and Cargill Inc. to develop innovative biodegradable oxygen-excluding barrier packaging marked a significant step towards creating more sustainable and effective solutions for extending the shelf life of agricultural products.

- Late 2023: Introduction of advanced reusable and collapsible container systems designed for optimized logistics and reduced environmental footprint in bulk agricultural transport.

- Early 2024: Key manufacturers announce substantial investments in expanding production capacity for bio-based and compostable packaging materials to meet growing market demand and regulatory pressures.

Strategic Outlook for Agricultural Containers Industry Market

The agricultural containers market is strategically positioned for sustained and accelerated growth, fueled by a powerful convergence of global megatrends. The future landscape will be shaped by an increasing emphasis on sustainability, the relentless pursuit of technological innovation, and the fundamental need to feed a growing world population. Companies that can adeptly navigate the challenges while capitalizing on emerging opportunities will be best placed for success. Key strategic imperatives include a dedicated focus on developing cutting-edge, environmentally responsible packaging solutions that minimize waste and maximize resource efficiency. Furthermore, forging robust strategic partnerships across the value chain – from material suppliers to agricultural producers and retailers – will be essential for collaborative innovation and market penetration. Expanding into burgeoning high-growth geographical markets, particularly those with increasing agricultural output and evolving consumer demands for sustainable products, presents significant untapped potential. The market offers a rich environment for visionary companies committed to enhancing food security, reducing environmental impact, and driving operational excellence through superior packaging solutions.

Agricultural Containers Industry Segmentation

-

1. Material Type

- 1.1. Plastic

- 1.2. Metal

- 1.3. Paper and Paperboard

- 1.4. Composite Materials

- 1.5. Other Materials

-

2. Application Type

- 2.1. Pesticides

- 2.2. Fertilizers

- 2.3. Seeds

- 2.4. Other Types

-

3. Product Type

- 3.1. Bags & Sacks (Plastic & Paper)

- 3.2. Bulk Containers (Drums & IBC)

- 3.3. Pouches

- 3.4. Containers (Metal & Plastic)

- 3.5. Other Products (Boxes, Caps & Lids, etc.)

Agricultural Containers Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. France

- 2.2. Germany

- 2.3. United Kingdom

- 2.4. The Netherlands

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Indonesia

- 3.4. Rest of Asia Pacific

- 4. Rest of the World

Agricultural Containers Industry Regional Market Share

Geographic Coverage of Agricultural Containers Industry

Agricultural Containers Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand from the Agro-chemical Segment; Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging

- 3.3. Market Restrains

- 3.3.1. ; High Inventory Costs and Premium Pricing

- 3.4. Market Trends

- 3.4.1. Plastic Packaging to Hold a Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Plastic

- 5.1.2. Metal

- 5.1.3. Paper and Paperboard

- 5.1.4. Composite Materials

- 5.1.5. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Application Type

- 5.2.1. Pesticides

- 5.2.2. Fertilizers

- 5.2.3. Seeds

- 5.2.4. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Product Type

- 5.3.1. Bags & Sacks (Plastic & Paper)

- 5.3.2. Bulk Containers (Drums & IBC)

- 5.3.3. Pouches

- 5.3.4. Containers (Metal & Plastic)

- 5.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. North America Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Plastic

- 6.1.2. Metal

- 6.1.3. Paper and Paperboard

- 6.1.4. Composite Materials

- 6.1.5. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Application Type

- 6.2.1. Pesticides

- 6.2.2. Fertilizers

- 6.2.3. Seeds

- 6.2.4. Other Types

- 6.3. Market Analysis, Insights and Forecast - by Product Type

- 6.3.1. Bags & Sacks (Plastic & Paper)

- 6.3.2. Bulk Containers (Drums & IBC)

- 6.3.3. Pouches

- 6.3.4. Containers (Metal & Plastic)

- 6.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Europe Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Plastic

- 7.1.2. Metal

- 7.1.3. Paper and Paperboard

- 7.1.4. Composite Materials

- 7.1.5. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by Application Type

- 7.2.1. Pesticides

- 7.2.2. Fertilizers

- 7.2.3. Seeds

- 7.2.4. Other Types

- 7.3. Market Analysis, Insights and Forecast - by Product Type

- 7.3.1. Bags & Sacks (Plastic & Paper)

- 7.3.2. Bulk Containers (Drums & IBC)

- 7.3.3. Pouches

- 7.3.4. Containers (Metal & Plastic)

- 7.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Asia Pacific Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Plastic

- 8.1.2. Metal

- 8.1.3. Paper and Paperboard

- 8.1.4. Composite Materials

- 8.1.5. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by Application Type

- 8.2.1. Pesticides

- 8.2.2. Fertilizers

- 8.2.3. Seeds

- 8.2.4. Other Types

- 8.3. Market Analysis, Insights and Forecast - by Product Type

- 8.3.1. Bags & Sacks (Plastic & Paper)

- 8.3.2. Bulk Containers (Drums & IBC)

- 8.3.3. Pouches

- 8.3.4. Containers (Metal & Plastic)

- 8.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Rest of the World Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Plastic

- 9.1.2. Metal

- 9.1.3. Paper and Paperboard

- 9.1.4. Composite Materials

- 9.1.5. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by Application Type

- 9.2.1. Pesticides

- 9.2.2. Fertilizers

- 9.2.3. Seeds

- 9.2.4. Other Types

- 9.3. Market Analysis, Insights and Forecast - by Product Type

- 9.3.1. Bags & Sacks (Plastic & Paper)

- 9.3.2. Bulk Containers (Drums & IBC)

- 9.3.3. Pouches

- 9.3.4. Containers (Metal & Plastic)

- 9.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Competitive Analysis

- 10.1. Global Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Proampac LLC

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Sonoco Products Company

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Anderson Packaging Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 LC Packaging International BV

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Greif Inc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Amcor plc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 NNZ Group

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Mondi Group

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Pactiv LLC

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 BAG Corporation

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Flexpack FIBC

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Western Packagin

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.1 Proampac LLC

List of Figures

- Figure 1: Global Agricultural Containers Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 3: North America Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 5: North America Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 6: North America Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 7: North America Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 8: North America Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 11: Europe Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 12: Europe Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 13: Europe Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 14: Europe Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 15: Europe Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Europe Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 19: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 20: Asia Pacific Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 21: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 22: Asia Pacific Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 23: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 24: Asia Pacific Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 27: Rest of the World Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Rest of the World Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 29: Rest of the World Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 30: Rest of the World Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 31: Rest of the World Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 32: Rest of the World Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Rest of the World Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 3: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 4: Global Agricultural Containers Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 7: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 12: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 13: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: France Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: The Netherlands Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Rest of Europe Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 21: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 22: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 23: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: China Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: India Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Indonesia Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 29: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 30: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 31: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Agricultural Containers Industry?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Agricultural Containers Industry?

Key companies in the market include Proampac LLC, Sonoco Products Company, Anderson Packaging Inc, LC Packaging International BV, Greif Inc, Amcor plc, NNZ Group, Mondi Group, Pactiv LLC, BAG Corporation, Flexpack FIBC, Western Packagin.

3. What are the main segments of the Agricultural Containers Industry?

The market segments include Material Type, Application Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 163.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand from the Agro-chemical Segment; Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging.

6. What are the notable trends driving market growth?

Plastic Packaging to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

; High Inventory Costs and Premium Pricing.

8. Can you provide examples of recent developments in the market?

May 2022 - Zeus, a global packaging solutions firm with Irish ownership, announced the acquisition of Canadian agricultural supplies company Agri-Flex. This acquisition represents the next stage of the company's EUR 35 million (nearly USD 36.88 million) investment strategy. It positions Zeus as one of the top distributors of agricultural crop packaging products worldwide.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Agricultural Containers Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Agricultural Containers Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Agricultural Containers Industry?

To stay informed about further developments, trends, and reports in the Agricultural Containers Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence