Key Insights

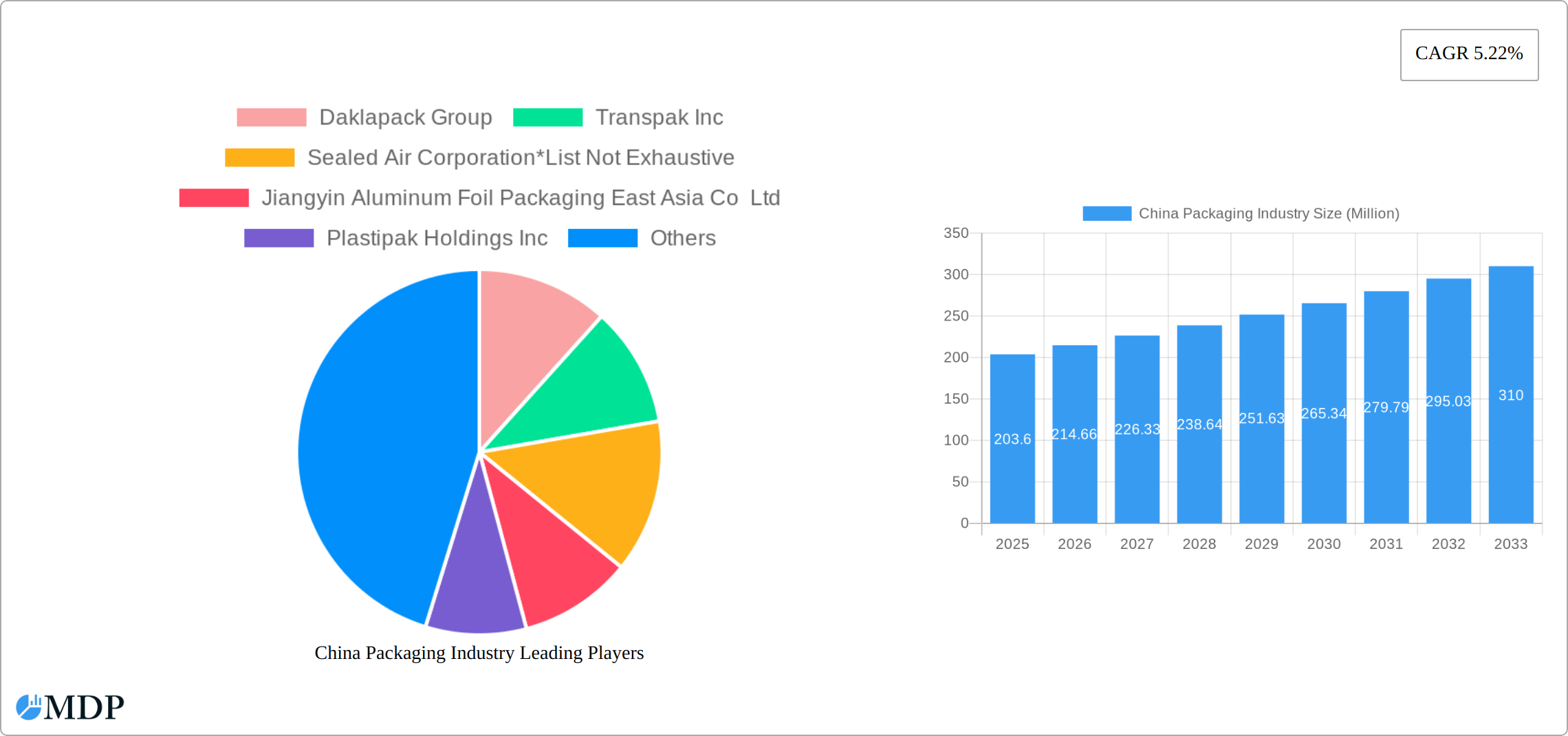

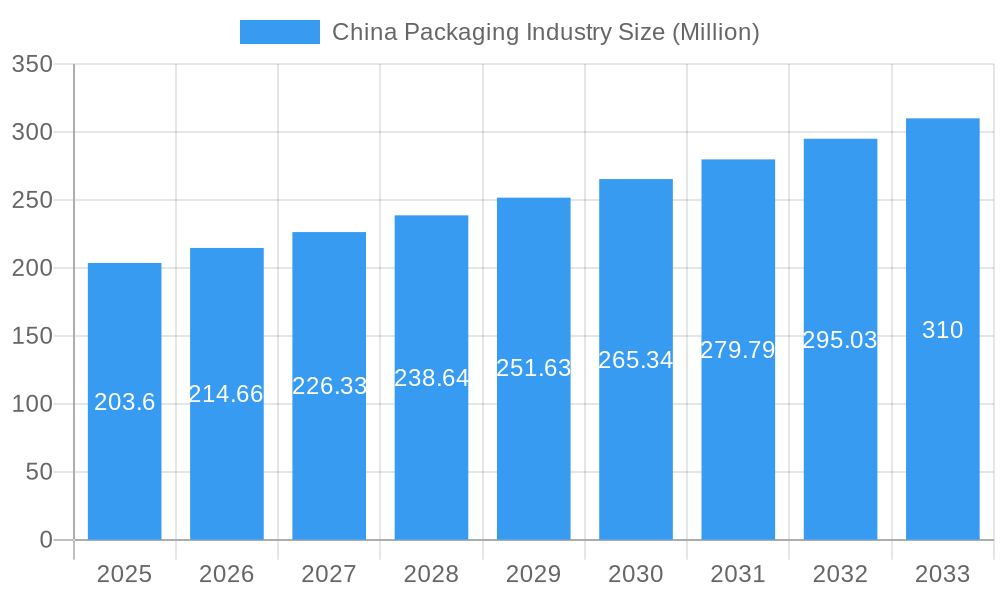

The China packaging industry, valued at $203.60 million in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 5.22% from 2025 to 2033. This expansion is fueled by several key drivers. The burgeoning e-commerce sector necessitates increased packaging for efficient delivery and product protection, significantly boosting demand. Simultaneously, rising consumer awareness of sustainability is driving the adoption of eco-friendly packaging materials like paper and biodegradable alternatives, replacing traditional plastics. Furthermore, the growth of the food and beverage, healthcare, and beauty and personal care sectors in China is directly correlated with increased packaging requirements. Government regulations promoting sustainable practices and improved supply chain efficiency also contribute to this positive market outlook. However, fluctuations in raw material prices, particularly for plastics and paper, pose a significant challenge, impacting profitability and potentially slowing growth. Competition among established players and the emergence of new entrants also present dynamic market conditions. The industry’s segmentation, encompassing various packaging materials (plastic, paper, glass, foam, metal), layering (primary, secondary, tertiary), and end-user industries, highlights the diverse opportunities and challenges within the sector. Regional variations in growth, with China representing a significant market share, will shape the overall landscape. This multifaceted industry landscape offers strategic possibilities for both established multinational corporations and emerging domestic players.

China Packaging Industry Market Size (In Million)

The competitive landscape is marked by both global giants like Amcor PLC and Mondi PLC, along with prominent regional players such as Daklapack Group, Jiangyin Aluminum Foil Packaging East Asia Co Ltd, and Guangzhou Yifeng Printing & Packaging Co Ltd. These companies are actively engaged in product innovation, strategic partnerships, and mergers and acquisitions to solidify their market position and cater to evolving consumer preferences and environmental concerns. The forecast period of 2025-2033 presents significant growth potential, particularly for companies that effectively leverage sustainable packaging solutions, optimize their supply chains, and effectively target the diverse end-user industries within China's dynamic market. Effective market segmentation and a strong understanding of consumer preferences will be crucial for success in this highly competitive yet rapidly growing sector.

China Packaging Industry Company Market Share

China Packaging Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the dynamic China packaging industry, offering invaluable insights for stakeholders seeking to navigate this rapidly evolving market. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report leverages extensive data and expert analysis to present a clear picture of market trends, opportunities, and challenges. The report covers key segments, leading players, and significant industry developments, empowering informed decision-making and strategic planning. Projected market value exceeds XX Million.

China Packaging Industry Market Dynamics & Concentration

The China packaging industry is characterized by a complex interplay of factors influencing market concentration, innovation, and regulatory landscapes. Market concentration is moderate, with several large players holding significant shares, but a substantial number of smaller, regional players also contributing significantly. The market share of the top 5 players is estimated at xx%, while the remaining market is fragmented among numerous smaller companies. M&A activity has been robust, with over xx deals recorded between 2019 and 2024, indicating a drive for consolidation and expansion.

- Market Concentration: Moderate, with top 5 players holding xx% market share.

- Innovation Drivers: Growing demand for sustainable packaging, e-commerce expansion, and technological advancements in packaging materials and design.

- Regulatory Framework: Stringent environmental regulations are driving the adoption of eco-friendly packaging solutions. Food safety regulations also significantly influence packaging choices.

- Product Substitutes: Biodegradable and compostable packaging materials are emerging as key substitutes for traditional materials.

- End-User Trends: Increasing demand for convenience, product safety, and attractive packaging designs are shaping consumer preferences.

- M&A Activity: A notable increase in mergers and acquisitions signals industry consolidation and expansion strategies. Between 2019 and 2024, xx deals were recorded.

China Packaging Industry Industry Trends & Analysis

The China packaging industry exhibits robust growth, driven by a surge in consumer spending, the expansion of e-commerce, and a rising middle class. The industry's CAGR during the historical period (2019-2024) was xx%, and it is projected to maintain a healthy CAGR of xx% during the forecast period (2025-2033). Technological advancements, particularly in automation and smart packaging, are significantly enhancing efficiency and creating new opportunities. Market penetration of sustainable packaging solutions is steadily increasing, driven by both consumer demand and government regulations. However, intense competition and fluctuating raw material prices present ongoing challenges for industry players. The shift towards e-commerce is fostering demand for protective and durable packaging, while evolving consumer preferences towards convenience and aesthetics are influencing packaging design and material choices.

Leading Markets & Segments in China Packaging Industry

China's packaging industry is characterized by a dynamic landscape, with a significant concentration of activity in the eastern coastal regions, including powerhouse provinces like Guangdong, Jiangsu, and Zhejiang. This dominance is not accidental, but rather a direct result of a highly developed manufacturing ecosystem, sophisticated logistics networks, and strategic proximity to major international shipping hubs. These factors collectively create a fertile ground for packaging innovation and production.

By Packaging Material: Plastic continues its reign as the leading packaging material, lauded for its unparalleled versatility, durability, and cost-effectiveness across a wide spectrum of applications. Following closely behind are paper and metal, each carving out significant market share in specific sectors. The ongoing pursuit of sustainable alternatives is also driving innovation in these material categories.

By Layers of Packaging: While primary packaging, which directly contains the product, still commands the largest share of market volume, there's a notable and accelerating trend towards growth in secondary and tertiary packaging. This surge is largely attributed to the exponential rise of e-commerce, which necessitates robust protection and efficient bundling for goods in transit.

By End-user Industry: The food and beverage sector stands as the undisputed titan, representing the largest end-user segment for packaging solutions, driven by high consumption volumes and evolving consumer preferences. The healthcare and pharmaceutical industries follow closely, reflecting the growing demand for safe, sterile, and precisely engineered packaging to protect vital medicines and medical devices.

- Key Drivers (Eastern Coastal Regions): The sustained strength of these regions is propelled by their deeply entrenched manufacturing base, state-of-the-art logistics infrastructure, advantageous port access, and a robust consumer market with increasing purchasing power.

- Food and Beverage Dominance: This sector's leadership is cemented by the escalating consumption of processed and convenience foods, coupled with increasingly stringent national and international regulations mandating high standards for food safety and product integrity.

- Growth in Healthcare Packaging: The rapid expansion of healthcare infrastructure, an ever-aging global population, and a concurrent rise in demand for pharmaceutical products are significant catalysts for the burgeoning healthcare packaging segment.

China Packaging Industry Product Developments

Recent product innovations include the integration of smart packaging technologies, such as RFID tags and QR codes, for enhanced product traceability and consumer engagement. The focus on sustainability is driving the adoption of biodegradable and compostable packaging materials, while advancements in barrier coatings are improving product preservation and shelf life. These innovations cater to growing consumer demands for convenience, safety, and environmental responsibility, creating competitive advantages for companies adopting them.

Key Drivers of China Packaging Industry Growth

Several factors propel the growth of China's packaging industry. Strong economic growth fuels increased consumer spending and industrial production, driving up demand for packaging materials. The booming e-commerce sector necessitates substantial investments in protective packaging, while government initiatives promoting sustainable packaging practices provide a significant push towards environmentally friendly solutions. Technological advancements continue to increase automation efficiency, impacting production costs and capacity.

Challenges in the China Packaging Industry Market

The vibrant China packaging industry navigates a complex terrain of challenges. The inherent volatility of raw material prices, particularly for petroleum-based plastics, introduces an element of unpredictability into production costs, demanding agile procurement strategies. Increasingly stringent environmental regulations worldwide necessitate significant investment in compliant technologies and processes, thereby elevating operational expenditures. The market is also characterized by intense competition from a multitude of domestic and international players, compelling a continuous drive for innovation, cost optimization, and enhanced product differentiation. Furthermore, the susceptibility of global supply chains to disruptions, especially during periods of economic or geopolitical uncertainty, poses a significant risk to production schedules and timely delivery, collectively impacting the industry's overall growth trajectory and requiring robust risk management frameworks.

Emerging Opportunities in China Packaging Industry

The China packaging market is a fertile ground for emerging opportunities, poised for substantial growth. The rapid advancement and increasing adoption of biodegradable and compostable packaging materials present a significant avenue to capitalize on the global and domestic demand for sustainable and environmentally conscious solutions. Strategic collaborations and partnerships between packaging manufacturers and brand owners are proving instrumental in developing and offering customized, eco-friendly packaging solutions that not only meet consumer expectations but also enhance brand value and market penetration. The exploration and penetration of niche markets, such as highly specialized pharmaceutical packaging for sensitive biologics or premium packaging for high-value consumer goods, offer opportunities for premium pricing strategies and welcomed revenue diversification. A forward-looking approach involving significant investment in advanced technologies, including sophisticated automation, robotics, and the integration of smart packaging features, is crucial for optimizing operational efficiencies, reducing waste, and establishing a formidable competitive advantage in this rapidly evolving landscape.

Leading Players in the China Packaging Industry Sector

- Daklapack Group

- Transpak Inc

- Sealed Air Corporation

- Jiangyin Aluminum Foil Packaging East Asia Co Ltd

- Plastipak Holdings Inc

- Amcor PLC

- Mondi PLC

- Wipak Group

- Guangzhou Yifeng Printing & Packaging Co Ltd

- Tetra Pak International SA

Key Milestones in China Packaging Industry Industry

- August 2022: Nippon Paint China and BASF collaborated to launch innovative eco-friendly industrial packaging solutions incorporating BASF's advanced water-based barrier coatings. This strategic initiative signifies a pivotal advancement in promoting sustainable packaging practices, particularly within the construction materials sector.

- March 2022: Datwyler significantly bolstered its presence in the Chinese pharmaceutical packaging market through the strategic acquisition of Yantai Xinhui Packing. This acquisition not only expands Datwyler's manufacturing footprint but also enhances its local customer service capabilities and strengthens its position in a critical market segment.

Strategic Outlook for China Packaging Industry Market

The China packaging industry’s future hinges on embracing sustainability, technological advancements, and strategic partnerships. Companies focusing on eco-friendly materials, innovative packaging designs, and efficient supply chains will be well-positioned to capture significant market share. Investing in automation and smart packaging technologies will optimize production processes, improve product quality, and enhance consumer experience. The long-term potential for growth remains substantial, particularly in the e-commerce and healthcare sectors.

China Packaging Industry Segmentation

-

1. Packaging Material

- 1.1. Plastic

- 1.2. Paper

- 1.3. Glass

- 1.4. Metal

- 1.5. Other Packaging Material

-

2. Types of Packaging

- 2.1. Primary Packaging

- 2.2. Secondary Packaging

- 2.3. Tertiary Packaging

-

3. End-user Industry

- 3.1. Food and Beverage

- 3.2. Healthcare and Pharmaceutical

- 3.3. Beauty and Personal Care

- 3.4. Industrial

- 3.5. Other End-user Industries

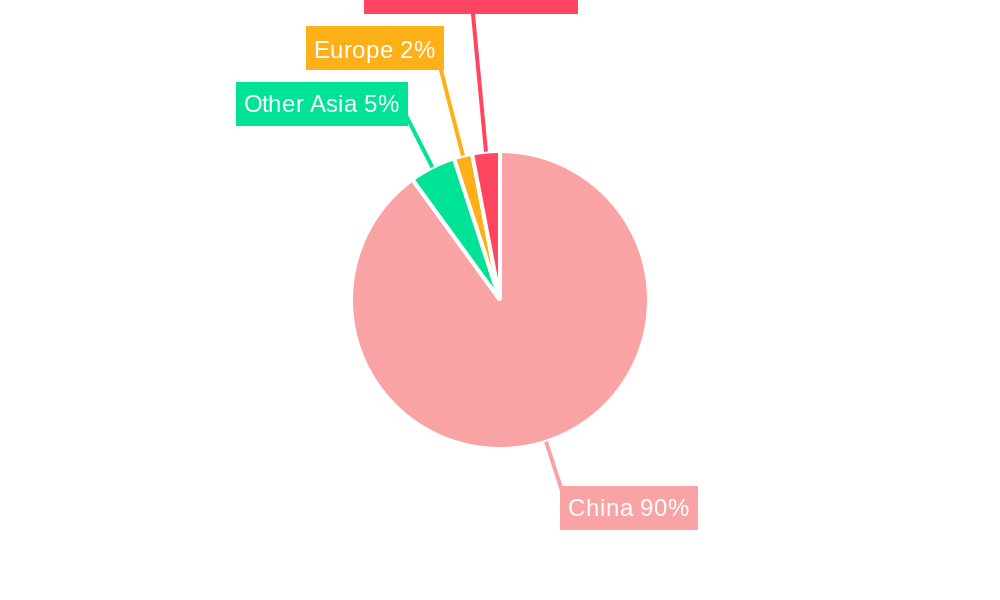

China Packaging Industry Segmentation By Geography

- 1. China

China Packaging Industry Regional Market Share

Geographic Coverage of China Packaging Industry

China Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.22% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 5.1.1. Plastic

- 5.1.2. Paper

- 5.1.3. Glass

- 5.1.4. Metal

- 5.1.5. Other Packaging Material

- 5.2. Market Analysis, Insights and Forecast - by Types of Packaging

- 5.2.1. Primary Packaging

- 5.2.2. Secondary Packaging

- 5.2.3. Tertiary Packaging

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food and Beverage

- 5.3.2. Healthcare and Pharmaceutical

- 5.3.3. Beauty and Personal Care

- 5.3.4. Industrial

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6. China Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6.1.1. Plastic

- 6.1.2. Paper

- 6.1.3. Glass

- 6.1.4. Metal

- 6.1.5. Other Packaging Material

- 6.2. Market Analysis, Insights and Forecast - by Types of Packaging

- 6.2.1. Primary Packaging

- 6.2.2. Secondary Packaging

- 6.2.3. Tertiary Packaging

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food and Beverage

- 6.3.2. Healthcare and Pharmaceutical

- 6.3.3. Beauty and Personal Care

- 6.3.4. Industrial

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Daklapack Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Transpak Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sealed Air Corporation*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Jiangyin Aluminum Foil Packaging East Asia Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Plastipak Holdings Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Amcor PLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mondi PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Wipak Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Guangzhou Yifeng Printing & Packaging Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Tetra Pak International SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Daklapack Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: China Packaging Industry Revenue Million Forecast, by Packaging Material 2020 & 2033

- Table 2: China Packaging Industry Revenue Million Forecast, by Types of Packaging 2020 & 2033

- Table 3: China Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: China Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: China Packaging Industry Revenue Million Forecast, by Packaging Material 2020 & 2033

- Table 6: China Packaging Industry Revenue Million Forecast, by Types of Packaging 2020 & 2033

- Table 7: China Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: China Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Packaging Industry?

The projected CAGR is approximately 5.22%.

2. Which companies are prominent players in the China Packaging Industry?

Key companies in the market include Daklapack Group, Transpak Inc, Sealed Air Corporation*List Not Exhaustive, Jiangyin Aluminum Foil Packaging East Asia Co Ltd, Plastipak Holdings Inc, Amcor PLC, Mondi PLC, Wipak Group, Guangzhou Yifeng Printing & Packaging Co Ltd, Tetra Pak International SA.

3. What are the main segments of the China Packaging Industry?

The market segments include Packaging Material, Types of Packaging, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 203.60 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise of E-commerce Giants; Increasing Demand for Longer Shelf Life of Packaged Goods.

6. What are the notable trends driving market growth?

Plastic Packaging is Expected to Witness a Slow Growth Owing to Ban on Plastics.

7. Are there any restraints impacting market growth?

Strict Rules and Regulations in the Packaging Industry; Environmental Concerns Restricting the Market Growth.

8. Can you provide examples of recent developments in the market?

August 2022: Nippon Paint China, a prominent coatings producer, and BASF jointly introduced eco-friendly industrial packaging, which Nippon Paint's dry-mixed mortar series products have since embraced. The innovative packaging material for Nippon Paint's construction dry mortar products is commercialized, using water-based acrylic dispersion Joncryl High-Performance Barrier (HPB) from BASF as the barrier material. China will be the first country where BASF's water-based barrier coatings are employed in industrial packaging.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Packaging Industry?

To stay informed about further developments, trends, and reports in the China Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence