Key Insights

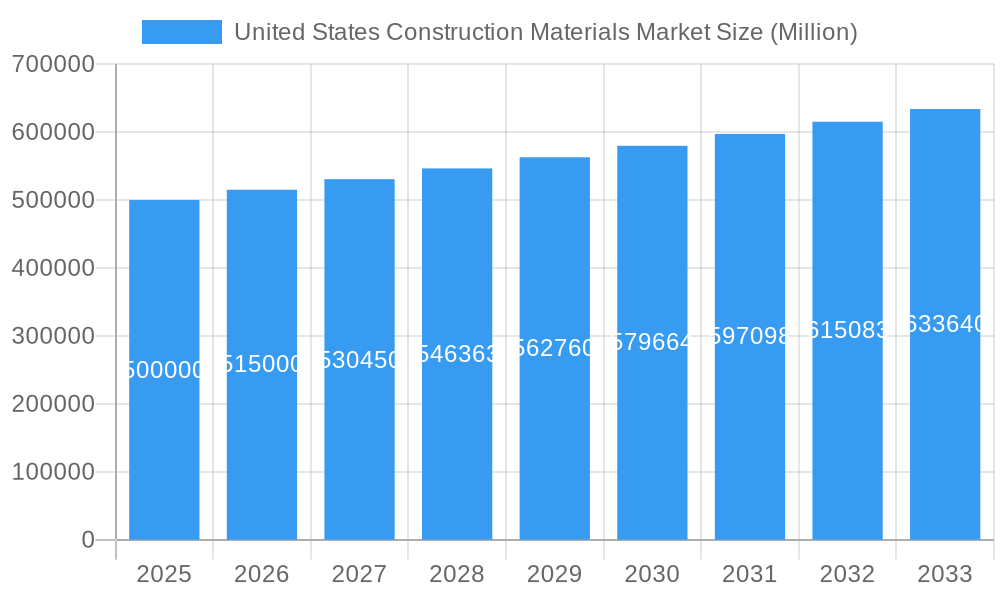

The United States Construction Materials Market is a robust and essential sector, estimated at $139.4 billion in 2024 and poised for consistent growth with a CAGR of 4% from 2025 to 2033. This expansion is primarily fueled by a confluence of factors including aggressive federal infrastructure spending initiatives, a steady demand for new residential and commercial construction, and significant investments in renovation and repair projects. The market encompasses a diverse range of materials, with Aggregates (like sand, gravel, and crushed stone), Cement & Concrete, and Metals forming the foundational pillars due to their extensive application across structural and infrastructural developments. The continuous evolution in urban landscapes, coupled with a national focus on upgrading aging infrastructure, provides a strong impetus for sustained demand across all key segments, from foundational materials to finishing elements like wood, glass, and bricks.

United States Construction Materials Market Market Size (In Billion)

Emerging trends are reshaping the competitive landscape, pushing for innovation in sustainable building materials, digital integration in supply chain management, and the adoption of advanced manufacturing techniques. While the market benefits from strong underlying demand, it navigates challenges such as fluctuating raw material costs, labor shortages, and rising interest rates, which can impact project feasibility. Leading players like Cemex Sab De CV, Heidelberg Materials, Holcim, Martin Marietta Materials, and Vulcan Materials Company are strategically investing in capacity expansion, technological advancements, and sustainable practices to maintain their competitive edge. The market's future outlook remains positive, driven by long-term demographic shifts, continued urbanization, and a growing emphasis on resilient and energy-efficient construction, ensuring a stable and expanding demand for construction materials across the residential, commercial, and industrial sectors.

United States Construction Materials Market Company Market Share

United States Construction Materials Market Research Report

Discover the Future of Building: United States Construction Materials Market Poised for Monumental Growth to Reach Over $xx Billion!

Unlock unparalleled insights into the dynamic United States Construction Materials Market with our comprehensive research report, meticulously designed for industry leaders, investors, and strategists. As the U.S. construction sector experiences a robust resurgence driven by massive infrastructure investments, booming residential development, and a strong commercial pipeline, the demand for essential building materials is skyrocketing. This report provides a critical analysis of market size, trends, and forecasts, offering an indispensable guide to navigate this rapidly evolving landscape.

Our expert analysis delves deep into the core components, including Aggregates (Sand, Gravel, Crushed Stone, M-Sand, Granite), Cement & Concrete, Metals, Bricks and Blocks, Wood, and Glass, covering their diverse applications across New Construction and Renovation & Repair. Understand the intricate demand patterns from Residential Construction, Commercial Construction, and Industrial Construction end-users, and explore how structural, envelope, interior, and site & landscaping applications are shaping material consumption.

With the market projected to exceed $xx billion by 2033, driven by innovation and strategic collaborations, staying ahead is paramount. Gain a competitive edge by understanding the strategies of key players like Cemex Sab De CV, CRH PLC, Heidelberg Materials, Holcim, Martin Marietta Materials, and Vulcan Materials Company. Discover the impact of recent industry developments, such as the July 2024 joint venture between CEMEX SAB de CV, Couch Aggregates, and Premier Holdings to bolster aggregate reserves in the Mid-South, and Heidelberg Materials' acquisition of Carver Sand & Gravel, significantly boosting its aggregates capacity in New York.

This report offers a granular view of market dynamics, competitive landscapes, technological advancements, and regulatory shifts, ensuring you're equipped with actionable intelligence.

Report Scope & Timelines:

- Study Period: 2019–2033

- Base Year: 2025

- Estimated Year: 2025

- Forecast Period: 2025–2033

- Historical Period: 2019–2024

Maximize your market potential. Invest in the definitive resource for the U.S. Construction Materials industry today!

United States Construction Materials Market Market Dynamics & Concentration

The United States Construction Materials Market exhibits a moderate to high degree of concentration, particularly within key segments like cement, aggregates, and certain specialized metals, where a few dominant players command substantial market share. Companies such as Holcim, Heidelberg Materials, Cemex Sab De CV, CRH PLC, Martin Marietta Materials, and Vulcan Materials Company are pivotal, leveraging extensive supply chain networks, large production capacities, and strategic acquisitions to maintain their competitive positions. Market share metrics for the top five players in aggregates and cement, for instance, collectively exceed 40%, indicating significant consolidation. Innovation drivers are increasingly centered on sustainability and efficiency. This includes the development of low-carbon cement, recycled aggregates, and advanced composite materials that offer enhanced durability and reduced environmental impact. Regulatory frameworks, such as strict environmental protection agency (EPA) guidelines and increasingly stringent building codes for energy efficiency and seismic resilience, significantly influence product development and market entry. These regulations often necessitate substantial R&D investments, favoring larger firms with the resources to comply and innovate.

Product substitutes, while not always direct, exert pressure on material choices. For example, mass timber is increasingly seen as an alternative to traditional steel and concrete in certain commercial applications, driven by sustainability goals and construction speed. Similarly, the availability and cost-effectiveness of local aggregates can dictate regional preferences over more distant, higher-cost alternatives. End-user trends heavily influence demand; for instance, the growing preference for green building certifications (e.g., LEED) drives demand for sustainable and locally sourced materials. Furthermore, the increasing adoption of prefabrication and modular construction methods is shifting demand towards standardized, lightweight, and high-performance materials that are easier to assemble off-site.

Mergers and acquisitions (M&A) remain a critical strategy for market expansion, consolidation of reserves, and technological integration. The construction materials sector saw approximately 50-70 significant M&A deals annually over the historical period, a trend expected to continue. Large players frequently acquire smaller, regional aggregate or concrete producers to expand geographic reach or secure vital raw material sources, thereby reducing transportation costs and strengthening regional supply chains. This continuous M&A activity contributes to increasing market concentration and strengthens the pricing power of larger entities. The total value of M&A deals in this sector consistently runs into billions of dollars each year, reflecting the strategic importance of scaling operations and integrating vertically.

United States Construction Materials Market Industry Trends & Analysis

The United States Construction Materials Market is undergoing transformative shifts, driven by a confluence of robust market growth factors, disruptive technological advancements, evolving consumer preferences, and dynamic competitive landscapes. A primary growth driver is the significant governmental investment in infrastructure, exemplified by the Infrastructure Investment and Jobs Act (IIJA), which allocates billions of dollars to roads, bridges, public transit, water systems, and broadband. This sustained spending creates a substantial and long-term demand for foundational materials like aggregates, cement, steel, and asphalt, underpinning the market's projected annual growth rate (CAGR) of around xx% from 2025 to 2033. Beyond public works, a strong residential housing market, fueled by population growth and shifting demographics, continues to drive demand for wood, bricks, concrete, and roofing materials. Commercial construction, including data centers, warehouses, and mixed-use developments, further contributes to market expansion, demanding specialized materials for efficiency and aesthetic appeal.

Technological disruptions are reshaping production, distribution, and material science. Digitalization, including Building Information Modeling (BIM) and advanced project management software, is enhancing material efficiency and reducing waste, improving overall project timelines and costs. Automation in manufacturing processes, such as AI-driven quality control for concrete mixes and automated aggregate sorting, boosts productivity and ensures consistent material quality. Furthermore, the emergence of advanced materials like self-healing concrete, transparent wood, and smart glass with tunable properties is opening new avenues for construction applications, albeit with lower market penetration currently, estimated at less than 5% for most cutting-edge innovations. These innovations promise enhanced durability, energy efficiency, and aesthetic versatility.

Consumer preferences, increasingly influenced by environmental consciousness and long-term cost savings, are accelerating the demand for sustainable and high-performance building materials. Green building certifications (e.g., LEED, Green Globes) are no longer niche but mainstream, pushing manufacturers to innovate in areas like low-carbon cement, recycled content materials (e.g., recycled aggregates, steel), and highly efficient insulation products. The desire for resilient construction, capable of withstanding extreme weather events, also drives demand for materials with superior strength, fire resistance, and moisture protection. This includes specialized concrete formulations and robust envelope materials.

The competitive dynamics of the market are characterized by a blend of global giants and numerous regional players. While large multinational corporations like Holcim, Cemex, and Heidelberg Materials dominate the cement and aggregates sectors, offering integrated solutions, smaller regional players provide localized supply and specialized services. This dynamic fosters both intense competition on price and a drive for differentiation through product innovation and customer service. Strategic partnerships and joint ventures, like the recent CEMEX collaboration, are common tactics to expand geographical reach and secure raw material supply. Furthermore, the market is subject to global supply chain volatility, impacting raw material costs and availability, and compelling companies to invest in resilient supply chain strategies and domestic sourcing where possible. The ongoing focus on operational efficiency and vertical integration remains crucial for maintaining competitive advantage and navigating potential economic downturns.

Leading Markets & Segments in United States Construction Materials Market

Within the multifaceted United States Construction Materials Market, the Aggregates segment, under Material Type, stands out as profoundly dominant, forming the foundational bedrock for nearly all construction activities across the nation. Aggregates, encompassing Sand, Gravel, and Crushed Stone, are indispensable for concrete production, asphalt paving, road bases, and numerous civil engineering projects. Their widespread application, from massive infrastructure developments to residential foundations and commercial structures, solidifies their leading position. The sheer volume required for construction makes aggregates the largest segment by tonnage and consistently one of the largest by value, with consumption reaching billions of metric tons annually and market value in the tens of billions of dollars.

- Infrastructure Spending: Significant government initiatives, such as the Infrastructure Investment and Jobs Act (IIJA), allocate billions of dollars towards repairing and building roads, bridges, airports, and public transit systems. Aggregates are the primary material for these projects, driving consistent and massive demand.

- Urbanization & Population Growth: Continual urbanization and population expansion in key metropolitan areas necessitate new housing, commercial spaces, and supporting infrastructure, all of which rely heavily on aggregates.

- Cost-Effectiveness & Availability: Aggregates are relatively low-cost and widely available across various regions of the U.S., making them economically viable for large-scale projects.

- Versatility: Their adaptability for use in concrete, asphalt, fill, and drainage systems makes them universally essential.

- Recycling & Sustainability Initiatives: While primary extraction remains significant, the increasing use of recycled concrete and asphalt as aggregates supports sustainable practices without diminishing overall demand for the segment, rather expanding the source base.

Following aggregates, Cement & Concrete represent another pivotal and closely related dominant segment due to concrete's universal application as a primary building material. The inseparable relationship between aggregates and cement for concrete production means their market trajectories are closely linked.

In terms of End User, Residential Construction often emerges as a dominant segment, particularly during periods of economic growth and low interest rates. The continuous demand for new housing units, driven by demographic shifts, household formation, and population mobility across the U.S., ensures robust consumption of a wide array of materials—from wood and bricks to concrete and roofing materials. While infrastructure and commercial projects involve large volumes of specific materials, the cumulative and recurring nature of residential builds, combined with renovation and repair activities in existing homes, often places it at the forefront of total material expenditure. This segment is highly sensitive to economic factors like mortgage rates, consumer confidence, and housing affordability, which directly impact the demand for construction materials. The widespread geographical distribution of residential projects across all states further underscores its broad impact on the entire supply chain.

For Construction Type, New Construction consistently accounts for the larger share of material consumption compared to Renovation & Repair. While renovation is a significant and stable segment, the sheer scale of material input for ground-up development of residential communities, major commercial complexes, and new infrastructure projects means that new construction drives the bulk of demand for foundational and structural materials.

Finally, regarding Application, the Structural segment (encompassing foundations, frames, load-bearing walls) dictates the largest portion of material usage, primarily for heavy-duty materials like concrete, steel, and substantial wood elements. These components are critical for the integrity and longevity of any building or infrastructure, thus leading to high demand for core construction materials.

United States Construction Materials Market Product Developments

The United States Construction Materials Market is witnessing a surge in product innovations, primarily driven by sustainability goals, enhanced performance requirements, and digitalization. A key trend is the development of low-carbon concrete and cement, incorporating supplementary cementitious materials (SCMs) like fly ash, slag, and calcined clay, or utilizing carbon capture technologies to significantly reduce CO2 emissions. These products offer competitive advantages by aligning with green building standards and reducing environmental footprints, making them highly attractive for environmentally conscious projects. Another area of innovation is in recycled and upcycled materials, such as recycled asphalt pavement (RAP) and recycled concrete aggregates (RCA), which divert waste from landfills while providing cost-effective and sustainable alternatives. Furthermore, the market is seeing advancements in smart materials, including self-healing concrete that can repair cracks automatically, and transparent wood, offering lightweight and strong alternatives with unique aesthetic properties. These innovations, though still niche, cater to an evolving market demanding high-performance, durable, and eco-friendly solutions that fit within the broader context of a circular economy and smart infrastructure development.

Key Drivers of United States Construction Materials Market Growth

The growth of the United States Construction Materials Market is propelled by several robust factors. Economic expansion and robust GDP growth fuel both private and public sector construction, directly increasing demand for materials. Major government infrastructure spending, notably through the Infrastructure Investment and Jobs Act (IIJA), allocates billions for roads, bridges, and utilities, creating sustained demand for aggregates, cement, and steel. The resurgent residential housing market, driven by population growth, urbanization, and the need for new housing units, especially in Sun Belt states, significantly boosts consumption of wood, concrete, and bricks. Technological advancements in material science, such as the development of high-performance and sustainable materials (e.g., low-carbon concrete, recycled aggregates), attract investment and foster innovation. Furthermore, the increasing adoption of green building practices and stringent energy efficiency codes across states mandates the use of advanced insulation, sustainable lumber, and eco-friendly concrete, thereby stimulating demand for specialized and environmentally responsible products.

Challenges in the United States Construction Materials Market Market

The United States Construction Materials Market faces several significant challenges impacting its growth and stability. Rising raw material costs for inputs like energy, limestone, and steel scrap, exacerbated by global supply chain disruptions and geopolitical events, directly increase production expenses, potentially impacting profit margins by 5-10% for manufacturers. Labor shortages, particularly for skilled trades in construction and manufacturing, continue to hamper production capacity and project timelines, leading to higher labor costs and delays. Stringent environmental regulations concerning quarry operations, emissions, and waste disposal, while necessary, can increase operational complexities and capital expenditure for compliance, affecting smaller players disproportionately. Intense competitive pressures from both established giants and emerging regional players often lead to price volatility and thinner margins in commodity segments like aggregates. Lastly, supply chain bottlenecks for critical components or transportation can lead to material scarcity and delayed project completions, causing disruptions across the construction value chain.

Emerging Opportunities in United States Construction Materials Market

Emerging opportunities in the United States Construction Materials Market are largely catalyzed by technological breakthroughs and a strong push towards sustainable practices. A key catalyst is the increasing investment in green building materials and circular economy principles, fostering demand for low-carbon concrete, recycled aggregates, and sustainable wood products. The drive for net-zero construction creates avenues for innovative insulations and energy-efficient envelope materials. Strategic partnerships and collaborations between material manufacturers, technology providers, and construction firms are facilitating the integration of advanced solutions, such as digital twins for material tracking and AI-driven quality control in production. Furthermore, market expansion into resilient infrastructure offers significant long-term growth. As climate change impacts necessitate more robust structures, demand for high-strength, weather-resistant materials for coastal defenses, enhanced drainage systems, and earthquake-resistant buildings will surge, presenting substantial opportunities for specialized material providers and innovators.

Leading Players in the United States Construction Materials Market Sector

- Cemex Sab De CV

- Colorado Stone Quarries Inc

- Buckman

- CRH PLC

- Heidelberg Materials

- Holcim

- Knife River Corporation

- Martin Marietta Materials

- Summit Materials Inc

- Kemira Oyj

- United States Lime & Minerals Inc

- Vulcan Materials Company

- Others

Key Milestones in United States Construction Materials Market Industry

- July 2024: CEMEX SAB de CV strategically entered a joint venture with Couch Aggregates, a prominent sand and gravel supplier, and Premier Holdings, a significant distributor of marine bulk products. This collaboration is designed to substantially bolster Cemex's aggregate reserves, with a focused emphasis on the production, distribution, and sale of essential sand, gravel, and limestone across the Mid-South United States. This move enhances Cemex's regional presence, allowing it to offer improved and expedited services to this rapidly growing region, thereby strengthening its market position and supply chain efficiency.

- July 2024: Heidelberg Materials completed the acquisition of Carver Sand & Gravel, the largest aggregates producer situated in Albany, New York. This strategic acquisition significantly amplified Heidelberg Materials' operational capabilities in the region. The integration expanded its portfolio to include crushed stone, sand and gravel, asphalt, and robust logistics infrastructure, resulting in a combined material capacity of approximately 3 million metric tons annually. This acquisition directly enhances Heidelberg's market footprint in a critical East Coast region, improving its ability to serve major construction projects and secure essential raw material supply.

Strategic Outlook for United States Construction Materials Market Market

The strategic outlook for the United States Construction Materials Market is characterized by several key growth accelerators, positioning it for robust future market potential. Continuous investment in infrastructure development, driven by federal mandates and state-level initiatives, will underpin long-term demand for foundational materials. This sustained public spending creates a stable pipeline for aggregates, cement, and steel, providing a resilient base for market expansion. Furthermore, the accelerating adoption of sustainable and low-carbon construction practices represents a significant strategic opportunity. Companies focusing on green materials, circular economy models, and energy-efficient solutions will gain a competitive edge, aligning with evolving regulatory frameworks and increasing client demand for environmentally responsible building. Technological integration, particularly in digitalization and automation across the value chain—from smart manufacturing to AI-driven logistics—will enhance operational efficiencies and foster product innovation. Strategic opportunities also lie in diversification into high-growth application segments like resilient infrastructure and advanced manufacturing facilities, requiring specialized, high-performance materials. The emphasis on supply chain resilience and localized production will also drive investment, mitigating future disruptions and securing stable material flow.

United States Construction Materials Market Segmentation

-

1. Material Type

-

1.1. Aggregates

- 1.1.1. Sand

- 1.1.2. Gravel

- 1.1.3. Crushed Stone

- 1.1.4. M-Sand

- 1.1.5. Granite

- 1.1.6. Others

- 1.2. Cement & Concrete

- 1.3. Metals

- 1.4. Bricks and Blocks

- 1.5. Wood

- 1.6. Glass

- 1.7. Others

-

1.1. Aggregates

-

2. Construction Type

- 2.1. New Construction

- 2.2. Renovation & Repair

-

3. Application

- 3.1. Structural

- 3.2. Envelope

- 3.3. Interior

- 3.4. Site & Landscaping

- 3.5. Others

-

4. End User

- 4.1. Residential Construction

- 4.2. Commercial Construction

- 4.3. Industrial Construction

United States Construction Materials Market Segmentation By Geography

- 1. United States

United States Construction Materials Market Regional Market Share

Geographic Coverage of United States Construction Materials Market

United States Construction Materials Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Aggregates

- 5.1.1.1. Sand

- 5.1.1.2. Gravel

- 5.1.1.3. Crushed Stone

- 5.1.1.4. M-Sand

- 5.1.1.5. Granite

- 5.1.1.6. Others

- 5.1.2. Cement & Concrete

- 5.1.3. Metals

- 5.1.4. Bricks and Blocks

- 5.1.5. Wood

- 5.1.6. Glass

- 5.1.7. Others

- 5.1.1. Aggregates

- 5.2. Market Analysis, Insights and Forecast - by Construction Type

- 5.2.1. New Construction

- 5.2.2. Renovation & Repair

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Structural

- 5.3.2. Envelope

- 5.3.3. Interior

- 5.3.4. Site & Landscaping

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Residential Construction

- 5.4.2. Commercial Construction

- 5.4.3. Industrial Construction

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. United States Construction Materials Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Aggregates

- 6.1.1.1. Sand

- 6.1.1.2. Gravel

- 6.1.1.3. Crushed Stone

- 6.1.1.4. M-Sand

- 6.1.1.5. Granite

- 6.1.1.6. Others

- 6.1.2. Cement & Concrete

- 6.1.3. Metals

- 6.1.4. Bricks and Blocks

- 6.1.5. Wood

- 6.1.6. Glass

- 6.1.7. Others

- 6.1.1. Aggregates

- 6.2. Market Analysis, Insights and Forecast - by Construction Type

- 6.2.1. New Construction

- 6.2.2. Renovation & Repair

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Structural

- 6.3.2. Envelope

- 6.3.3. Interior

- 6.3.4. Site & Landscaping

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Residential Construction

- 6.4.2. Commercial Construction

- 6.4.3. Industrial Construction

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Cemex Sab De CV

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Colorado Stone Quarries Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Buckman

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CRH PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Heidelberg Materials

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Holcim

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Knife River Corporation�

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Martin Marietta Materials

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Summit Materials Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Kemira Oyj

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 United States Lime & Minerals Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Vulcan Materials Company

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Others

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Cemex Sab De CV

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Construction Materials Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United States Construction Materials Market Share (%) by Company 2025

List of Tables

- Table 1: United States Construction Materials Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: United States Construction Materials Market Revenue billion Forecast, by Construction Type 2020 & 2033

- Table 3: United States Construction Materials Market Revenue billion Forecast, by Application 2020 & 2033

- Table 4: United States Construction Materials Market Revenue billion Forecast, by End User 2020 & 2033

- Table 5: United States Construction Materials Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: United States Construction Materials Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 7: United States Construction Materials Market Revenue billion Forecast, by Construction Type 2020 & 2033

- Table 8: United States Construction Materials Market Revenue billion Forecast, by Application 2020 & 2033

- Table 9: United States Construction Materials Market Revenue billion Forecast, by End User 2020 & 2033

- Table 10: United States Construction Materials Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Construction Materials Market?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the United States Construction Materials Market?

Key companies in the market include Cemex Sab De CV, Colorado Stone Quarries Inc, Buckman, CRH PLC, Heidelberg Materials, Holcim, Knife River Corporation�, Martin Marietta Materials, Summit Materials Inc, Kemira Oyj, United States Lime & Minerals Inc, Vulcan Materials Company, Others .

3. What are the main segments of the United States Construction Materials Market?

The market segments include Material Type, Construction Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 145 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Investments in the Infrastructure and Industrial Sectors; Growing Mining Activities and Increasing Popularity of Dimension Stones.

6. What are the notable trends driving market growth?

Rising Investments in the Infrastructure and Industrial Sectors Driving the Market.

7. Are there any restraints impacting market growth?

Rising Investments in the Infrastructure and Industrial Sectors; Growing Mining Activities and Increasing Popularity of Dimension Stones.

8. Can you provide examples of recent developments in the market?

July 2024: CEMEX SAB de CV entered a joint venture with Couch Aggregates, a sand and gravel supplier, and Premier Holdings, a distributor of marine bulk products. This collaboration aims to bolster Cemex's aggregate reserves by focusing on the production, distribution, and sale of sand, gravel, and limestone in the Mid-South United States. As a result, Cemex is set to enhance its presence and offer improved, expedited services to this burgeoning region.July 2024: Heidelberg Materials acquired Carver Sand & Gravel, the largest aggregates producer in Albany, New York. This acquisition boosted the company’s operations, including crushed stone, sand and gravel, asphalt, and logistics, with a combined material capacity of around 3 million metric tons annually.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Construction Materials Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Construction Materials Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Construction Materials Market?

To stay informed about further developments, trends, and reports in the United States Construction Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence