Key Insights

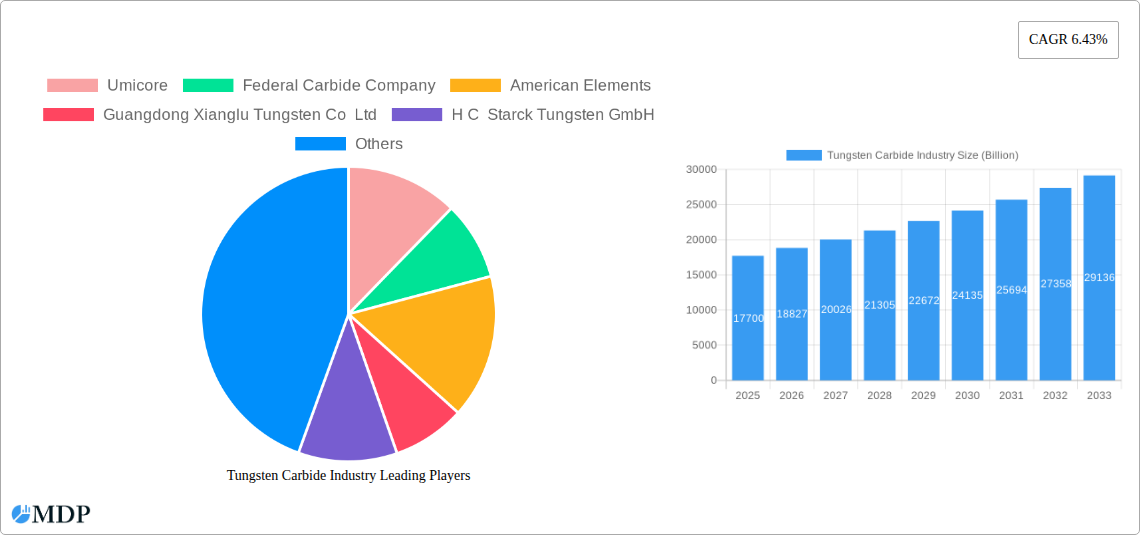

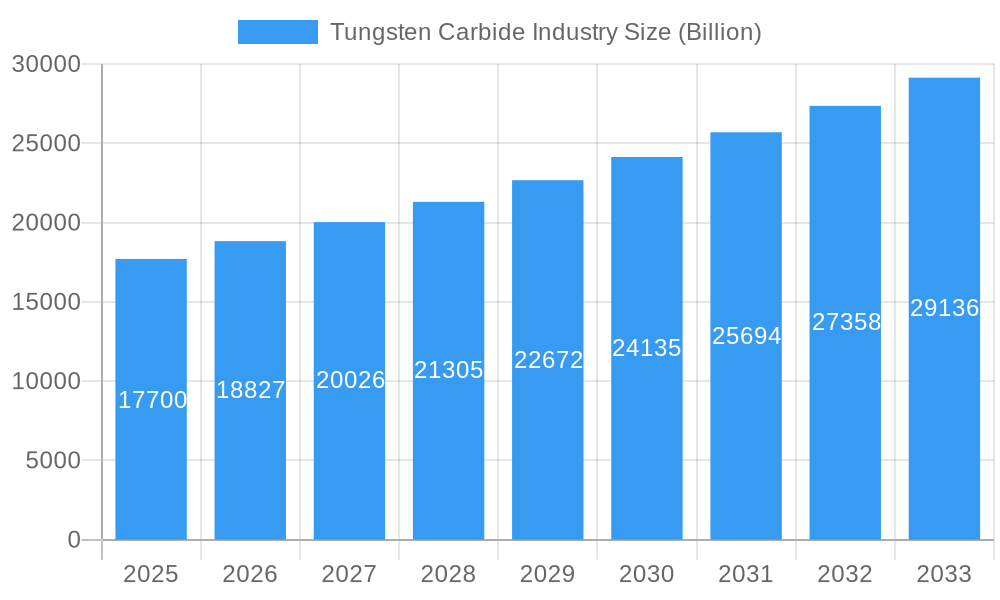

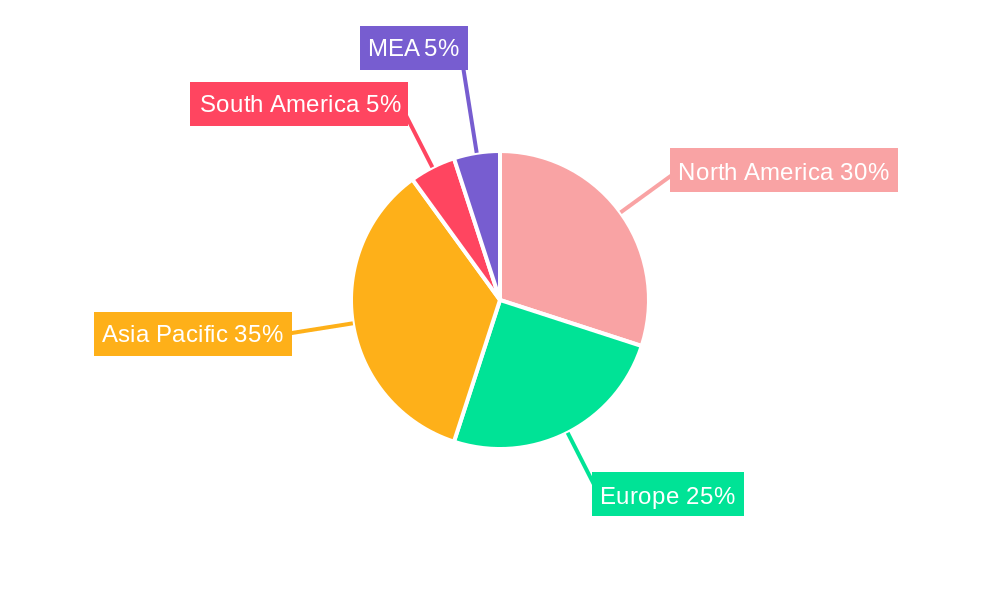

The global tungsten carbide market, valued at $17.70 billion in 2025, is projected to experience robust growth, driven by a compound annual growth rate (CAGR) of 6.43% from 2025 to 2033. This expansion is fueled by several key factors. The increasing demand for tungsten carbide in diverse applications, particularly within the aerospace & defense, automotive, and mining & construction sectors, is a major catalyst. Advancements in material science leading to improved wear resistance, hardness, and thermal conductivity of tungsten carbide components are also contributing to market growth. Furthermore, the rising adoption of tungsten carbide in precision engineering and electronics manufacturing, along with its use in medical implants and sporting goods, is further expanding the market's addressable scope. Competition within the industry is fierce, with major players like Umicore, Kennametal, and Sandvik constantly innovating and expanding their product portfolios to meet evolving customer needs. The geographic distribution of the market sees strong contributions from North America and Asia-Pacific, driven by substantial manufacturing activities and robust demand in these regions.

Tungsten Carbide Industry Market Size (In Billion)

The market's growth trajectory, however, faces certain challenges. Fluctuations in tungsten prices, a key raw material, can impact profitability. Stringent environmental regulations regarding tungsten mining and processing could potentially constrain production and increase operational costs. Additionally, the development and adoption of alternative materials with comparable properties pose a potential long-term threat to tungsten carbide's market dominance. Despite these challenges, the consistent demand from diverse end-use sectors, coupled with ongoing technological advancements, is anticipated to propel the global tungsten carbide market to significant heights over the forecast period. Strategic partnerships, mergers, and acquisitions among industry players are also expected to influence the market landscape in the coming years.

Tungsten Carbide Industry Company Market Share

Tungsten Carbide Industry Market Report: A Comprehensive Analysis (2019-2033)

This comprehensive report provides an in-depth analysis of the global Tungsten Carbide industry, projecting a market valuation exceeding $XX Billion by 2033. The report covers the period from 2019 to 2033, with a focus on the forecast period of 2025-2033 and a base year of 2025. It delves into market dynamics, leading players, key segments, and future growth opportunities, providing actionable insights for industry stakeholders, investors, and businesses operating within this dynamic sector.

Key Highlights:

- Market Size & Growth: The global Tungsten Carbide market is anticipated to reach $XX Billion by 2033, exhibiting a robust CAGR of XX% during the forecast period.

- Segment Analysis: Detailed analysis of key segments including Cemented Carbide, Coatings, and Alloys, alongside end-user applications across Aerospace & Defense, Automotive, Mining & Construction, Electronics, and Others (Medical, Sports, etc.).

- Competitive Landscape: In-depth profiles of leading players such as Umicore, Federal Carbide Company, American Elements, Guangdong Xianglu Tungsten Co Ltd, H C Starck Tungsten GmbH, Sandvik AB, Kennametal Inc, CERATIZIT S A, Jiangxi Yaosheng Tungsten Co Ltd, China Tungsten, Extramet Products LLC, CY Carbide Mfg Co Ltd, Buffalo Tungsten Inc, and Sumitomo Electric Industries Ltd, providing insights into their market share, strategies, and recent activities.

- Industry Trends & Developments: Comprehensive coverage of recent mergers & acquisitions (M&As), technological advancements, and regulatory changes impacting the industry.

Tungsten Carbide Industry Market Dynamics & Concentration

The Tungsten Carbide industry exhibits a moderately concentrated market structure, characterized by the presence of key global players who collectively command a substantial portion of the market share. This concentration is often a result of significant capital investment required for advanced manufacturing processes and the strategic importance of vertical integration, particularly in securing raw material supply chains. The driving force behind innovation within the industry is the relentless pursuit of enhanced material properties, such as superior hardness, exceptional wear resistance, and improved fracture toughness. This pursuit is directly linked to the demand for higher performance characteristics in increasingly demanding applications across various sectors. Furthermore, the industry is actively exploring and expanding into new and emerging applications, leveraging tungsten carbide's unique attributes. Regulatory frameworks, particularly those pertaining to environmental standards (e.g., waste management, emissions control) and material safety (e.g., handling and disposal of hazardous substances), are playing an increasingly pivotal role in shaping industry practices, influencing production methodologies and sourcing strategies. While direct substitutes for tungsten carbide in its core high-performance applications are limited, the evolution of substitute materials in niche areas and the evolving preferences of end-users contribute to the market's dynamic nature. For instance, the automotive industry's ongoing drive for lighter, stronger, and more fuel-efficient components necessitates materials that can withstand higher operating temperatures and stresses, creating opportunities for advanced tungsten carbide solutions. Mergers and acquisitions (M&A) activity has been a significant feature of the market landscape, with strategic acquisitions by leading companies aimed at bolstering market consolidation, expanding geographical reach, gaining access to proprietary technologies, and strengthening supply chain resilience.

Key Dynamics:

- Market Concentration: The global market remains moderately concentrated, with the top 5 players estimated to hold approximately 60-70% of the global market share (2024). This indicates a strong presence of established entities.

- Innovation Drivers: The primary innovation drivers are the persistent demand for superior wear resistance, the need for higher precision in machining and tooling, and the development of tailored material properties to meet specific application requirements.

- Regulatory Frameworks: Strict adherence to evolving environmental regulations (e.g., REACH, RoHS) and stringent safety standards significantly impacts production processes, material sourcing, and R&D investment.

- Product Substitutes: Direct substitutes with comparable performance characteristics are scarce for critical applications. However, in certain less demanding segments, alternative materials like high-speed steel or ceramics may offer competition.

- End-User Trends: There is a marked increase in demand across high-growth sectors including the automotive industry (for powertrain and tooling), aerospace & defense (for critical components), and the electronics sector (for precision tooling and components).

- M&A Activity: The industry has witnessed substantial M&A activity, with an estimated 10-15 major M&A deals recorded in the last 5 years (2019-2024), signaling a trend towards consolidation and strategic expansion.

Tungsten Carbide Industry Industry Trends & Analysis

The Tungsten Carbide industry is witnessing robust growth, propelled by several key factors. The increasing demand across various sectors like automotive, aerospace, and electronics, driven by technological advancements and increased production, is a primary growth driver. The global push for electric vehicles (EVs) presents a major opportunity, particularly with the development of tungsten-based cathode coatings for enhanced battery performance, as highlighted by the collaboration between ZSW and H.C. Starck Tungsten Powders. Technological disruptions are mainly focused on the development of advanced manufacturing techniques and the creation of customized Tungsten Carbide solutions for specific application requirements. Consumer preferences are shifting towards higher-performance, sustainable, and cost-effective materials, impacting the industry's innovation strategies. Competitive dynamics involve intense price competition, alongside efforts to differentiate products through enhanced properties and specialized applications. The industry exhibits a steady CAGR (XX%) with significant market penetration across various end-use applications.

Leading Markets & Segments in Tungsten Carbide Industry

The global Tungsten Carbide market exhibits a strong regional presence, with Asia-Pacific, particularly China, emerging as the dominant market. This dominance is a multifaceted phenomenon, stemming from a confluence of factors including significant domestic demand, robust manufacturing infrastructure, extensive mining operations for tungsten ore, and favorable government policies that support industrial growth and export competitiveness. The region has become a pivotal hub for both the production of raw tungsten materials and the manufacturing of finished tungsten carbide products.

- Cemented Carbide: This segment continues to command the largest market share, driven by its indispensable role in the manufacturing of cutting tools (e.g., for metalworking, woodworking), wear-resistant components (e.g., drill bits, nozzles, seals), and dies. Its exceptional hardness and wear resistance make it the material of choice for high-volume industrial applications.

- Coatings: This segment is experiencing robust growth, propelled by advancements in thin-film deposition technologies such as Physical Vapor Deposition (PVD) and Chemical Vapor Deposition (CVD). These technologies enable the application of ultra-thin, highly functional tungsten carbide coatings that significantly enhance the surface properties of various substrates, extending their lifespan and improving performance in applications ranging from industrial tooling to medical implants.

- Alloys: Tungsten carbide alloys, which incorporate tungsten carbide particles within a metal binder matrix, are gaining significant traction in specialized and high-performance industries. These alloys offer a tailored balance of properties, such as enhanced toughness, improved high-temperature strength, and superior corrosion resistance, making them suitable for demanding applications in aerospace, energy, and chemical processing.

Key Drivers by End-User:

- Automotive: Continued expansion of the automotive sector, coupled with the increasing demand for improved engine components (e.g., piston rings, valves), transmission parts, and high-precision manufacturing tooling for mass production, fuels consistent demand.

- Aerospace & Defense: The stringent requirements for high-performance materials in aerospace applications (e.g., engine components, landing gear) and the ongoing demand for robust defense systems drive the need for specialized tungsten carbide grades.

- Mining & Construction: The inherent properties of tungsten carbide, specifically its extreme wear resistance and durability, make it indispensable for mining and construction equipment such as drill bits, excavation tools, and crushing machinery operating in harsh environments.

- Electronics: The miniaturization and increasing complexity of electronic devices are driving the demand for specialized tungsten carbide components in electronics manufacturing, including fine-pitch tooling for semiconductor fabrication and precision components for consumer electronics.

- Others (Medical, Sports, etc.): This segment, encompassing applications in the medical industry (e.g., surgical instruments, dental tools), sports equipment (e.g., golf club inserts, cycling components), and other niche markets, presents significant, albeit smaller, growth potential due to the unique properties of tungsten carbide.

Regional Dominance Analysis (Asia-Pacific): The Asia-Pacific region, led by China, is the undisputed leader in the global tungsten carbide market. This dominance is underpinned by several critical factors. Firstly, China is the world's largest producer of tungsten ore, providing a secure and cost-effective supply of the primary raw material. Secondly, the region boasts a vast and well-established industrial ecosystem, encompassing extensive manufacturing capabilities, advanced research and development facilities, and a highly skilled workforce. The presence of a large domestic market, driven by rapid industrialization and infrastructure development, further fuels demand. Government initiatives promoting technological innovation, industrial upgrading, and export-oriented manufacturing have also played a crucial role in solidifying the region's leading position. Furthermore, significant investments in R&D by both domestic and international companies operating within the region have accelerated the development of new applications and enhanced product performance, cementing Asia-Pacific's strategic importance in the global tungsten carbide value chain.

Tungsten Carbide Industry Product Developments

Recent product innovations focus on enhancing the performance and properties of tungsten carbide materials. This includes developing materials with improved wear resistance, higher strength, and tailored compositions for specific applications. These innovations are driven by advancements in powder metallurgy, coating technologies, and advanced manufacturing processes. The market fit for these new materials is strong, driven by the ongoing demand for high-performance components across diverse industries. Key developments include advancements in nanostructured tungsten carbides and the integration of tungsten carbide with other materials to enhance properties.

Key Drivers of Tungsten Carbide Industry Growth

The growth of the Tungsten Carbide industry is driven by several key factors:

- Technological Advancements: Advancements in materials science and manufacturing techniques continually improve performance and expand applications.

- Economic Growth: Continued global economic growth drives demand across key end-use sectors.

- Regulatory Environment: Stringent environmental regulations are driving innovation in sustainable material solutions.

Challenges in the Tungsten Carbide Industry Market

The Tungsten Carbide industry, despite its robust growth prospects, navigates through several significant challenges that impact its operations and profitability:

- Raw Material Supply Volatility: The tungsten market is subject to considerable fluctuations in the supply and price of tungsten concentrate, which is a direct result of geopolitical factors, mining output variations, and global demand shifts. These price swings can significantly impact production costs and the profitability margins for manufacturers, necessitating robust supply chain management and hedging strategies.

- High Manufacturing Costs: The production of tungsten carbide involves complex and energy-intensive processes, including powder metallurgy, sintering, and grinding. These intricate manufacturing processes, coupled with the need for specialized equipment and stringent quality control, contribute to relatively high production costs compared to many other industrial materials.

- Intense Competition and Price Pressure: The global market features a considerable number of manufacturers, leading to intense competition. This competitive landscape often translates into price pressure, compelling companies to continuously focus on innovation, cost optimization through process improvements and efficiency gains, and differentiation through specialized product offerings to maintain market share and profitability.

- Environmental and Sustainability Concerns: Increasing global emphasis on sustainability and stricter environmental regulations related to mining, processing, and waste disposal of tungsten-containing materials pose ongoing challenges. Companies must invest in eco-friendly technologies and sustainable sourcing practices to meet regulatory requirements and evolving consumer expectations.

- Skilled Workforce Requirements: The specialized nature of tungsten carbide manufacturing requires a highly skilled and trained workforce. A shortage of experienced engineers, metallurgists, and skilled technicians can hinder production efficiency and technological advancement.

Emerging Opportunities in Tungsten Carbide Industry

The Tungsten Carbide market presents several emerging opportunities, including:

- Technological breakthroughs: Developments in additive manufacturing and nanomaterials offer potential for disruptive innovations.

- Strategic partnerships: Collaborations between materials producers and end-users accelerate product development and market penetration.

- Market expansion: Growing demand from emerging economies presents significant expansion opportunities.

Leading Players in the Tungsten Carbide Industry Sector

- Umicore

- Federal Carbide Company

- American Elements

- Guangdong Xianglu Tungsten Co Ltd

- H C Starck Tungsten GmbH

- Sandvik AB

- Kennametal Inc

- CERATIZIT S A

- Jiangxi Yaosheng Tungsten Co Ltd

- China Tungsten

- Extramet Products LLC

- CY Carbide Mfg Co Ltd

- Buffalo Tungsten Inc

- Sumitomo Electric Industries Ltd

Key Milestones in Tungsten Carbide Industry Industry

- September 2022: CERATIZIT S.A., a leading global provider of hard metal solutions, strategically acquired AgriCarb SAS. This acquisition significantly broadened CERATIZIT's presence in the agricultural wear parts sector, enhancing its market reach and diversifying its product portfolio within specialized industrial applications.

- June 2022: A pivotal research collaboration was established between the ZSW (Center for Solar Energy and Hydrogen Research Baden-Württemberg) and H.C. Starck Tungsten Powders. This partnership focuses on developing advanced tungsten-based cathode coatings for lithium-ion batteries, a development that directly supports the burgeoning electric vehicle (EV) market and underscores the critical role of tungsten in next-generation energy storage solutions.

- February 2022: CERATIZIT S.A. further solidified its supply chain and commitment to circular economy principles by acquiring the remaining 50% stake in Stadler Mettale. This move secured a key source of secondary raw materials for tungsten and tungsten carbide powders, bolstering its vertical integration and reinforcing its position in sustainable material sourcing.

- November 2021: Sandvik Coromant launched its new family of T-Max P inserts for turning, featuring advanced geometries and coating technologies designed to improve productivity and tool life in a wide range of steel machining applications. This launch highlights the continuous innovation in cutting tool performance driven by tungsten carbide.

- March 2020: Kennametal Inc. announced the acquisition of the remaining interest in their joint venture in China, Kennametal Yantai. This strategic move allowed Kennametal to gain full ownership and control over its operations in a key growth market, enabling more agile decision-making and market responsiveness.

Strategic Outlook for Tungsten Carbide Industry Market

The Tungsten Carbide industry is charting a course for sustained and robust growth, driven by a powerful synergy of continuous technological advancements and an escalating demand across a diverse spectrum of industrial sectors. The inherent superior properties of tungsten carbide—its unparalleled hardness, exceptional wear resistance, and high-temperature strength—continue to make it an indispensable material for critical applications. Strategic initiatives such as forming strategic partnerships, engaging in collaborative R&D efforts, and actively pursuing expansion into emerging markets will be paramount for capitalizing on future growth opportunities. Companies that prioritize and invest in cutting-edge innovation, embrace sustainability throughout their value chain, and relentlessly pursue cost optimization through process efficiencies and advanced manufacturing techniques will be exceptionally well-positioned for long-term success and market leadership. Furthermore, the ongoing development of specialized tungsten carbide materials tailored for niche, high-value applications, such as in advanced electronics, medical devices, and aerospace components, will be critical for achieving market differentiation and securing a competitive advantage in an evolving global landscape.

Tungsten Carbide Industry Segmentation

-

1. Application

- 1.1. Cemented carbide

- 1.2. Coatings

- 1.3. Alloys

-

2. End-user

- 2.1. Aerospace & Defense

- 2.2. Automotive

- 2.3. Mining & Construction

- 2.4. Electronics

- 2.5. Others (Medical, Sports, etc.)

Tungsten Carbide Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East

Tungsten Carbide Industry Regional Market Share

Geographic Coverage of Tungsten Carbide Industry

Tungsten Carbide Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.43% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Cemented carbide

- 5.1.2. Coatings

- 5.1.3. Alloys

- 5.2. Market Analysis, Insights and Forecast - by End-user

- 5.2.1. Aerospace & Defense

- 5.2.2. Automotive

- 5.2.3. Mining & Construction

- 5.2.4. Electronics

- 5.2.5. Others (Medical, Sports, etc.)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Tungsten Carbide Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Cemented carbide

- 6.1.2. Coatings

- 6.1.3. Alloys

- 6.2. Market Analysis, Insights and Forecast - by End-user

- 6.2.1. Aerospace & Defense

- 6.2.2. Automotive

- 6.2.3. Mining & Construction

- 6.2.4. Electronics

- 6.2.5. Others (Medical, Sports, etc.)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Asia Pacific Tungsten Carbide Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Cemented carbide

- 7.1.2. Coatings

- 7.1.3. Alloys

- 7.2. Market Analysis, Insights and Forecast - by End-user

- 7.2.1. Aerospace & Defense

- 7.2.2. Automotive

- 7.2.3. Mining & Construction

- 7.2.4. Electronics

- 7.2.5. Others (Medical, Sports, etc.)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. North America Tungsten Carbide Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Cemented carbide

- 8.1.2. Coatings

- 8.1.3. Alloys

- 8.2. Market Analysis, Insights and Forecast - by End-user

- 8.2.1. Aerospace & Defense

- 8.2.2. Automotive

- 8.2.3. Mining & Construction

- 8.2.4. Electronics

- 8.2.5. Others (Medical, Sports, etc.)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Tungsten Carbide Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Cemented carbide

- 9.1.2. Coatings

- 9.1.3. Alloys

- 9.2. Market Analysis, Insights and Forecast - by End-user

- 9.2.1. Aerospace & Defense

- 9.2.2. Automotive

- 9.2.3. Mining & Construction

- 9.2.4. Electronics

- 9.2.5. Others (Medical, Sports, etc.)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Rest of the World Tungsten Carbide Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Cemented carbide

- 10.1.2. Coatings

- 10.1.3. Alloys

- 10.2. Market Analysis, Insights and Forecast - by End-user

- 10.2.1. Aerospace & Defense

- 10.2.2. Automotive

- 10.2.3. Mining & Construction

- 10.2.4. Electronics

- 10.2.5. Others (Medical, Sports, etc.)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Umicore

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Federal Carbide Company

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 American Elements

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Guangdong Xianglu Tungsten Co Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 H C Starck Tungsten GmbH

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Sandvik AB

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Kennametal Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 CERATIZIT S A

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Jiangxi Yaosheng Tungsten Co Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 China Tungsten

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Extramet Products LLC

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 CY Carbide Mfg Co Ltd

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Buffalo Tungsten Inc

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 Sumitomo Electric Industries Ltd

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.1 Umicore

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Tungsten Carbide Industry Revenue Breakdown (Billion, %) by Region 2025 & 2033

- Figure 2: Global Tungsten Carbide Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Tungsten Carbide Industry Revenue (Billion), by Application 2025 & 2033

- Figure 4: Asia Pacific Tungsten Carbide Industry Volume (K Tons), by Application 2025 & 2033

- Figure 5: Asia Pacific Tungsten Carbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Tungsten Carbide Industry Volume Share (%), by Application 2025 & 2033

- Figure 7: Asia Pacific Tungsten Carbide Industry Revenue (Billion), by End-user 2025 & 2033

- Figure 8: Asia Pacific Tungsten Carbide Industry Volume (K Tons), by End-user 2025 & 2033

- Figure 9: Asia Pacific Tungsten Carbide Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 10: Asia Pacific Tungsten Carbide Industry Volume Share (%), by End-user 2025 & 2033

- Figure 11: Asia Pacific Tungsten Carbide Industry Revenue (Billion), by Country 2025 & 2033

- Figure 12: Asia Pacific Tungsten Carbide Industry Volume (K Tons), by Country 2025 & 2033

- Figure 13: Asia Pacific Tungsten Carbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Tungsten Carbide Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: North America Tungsten Carbide Industry Revenue (Billion), by Application 2025 & 2033

- Figure 16: North America Tungsten Carbide Industry Volume (K Tons), by Application 2025 & 2033

- Figure 17: North America Tungsten Carbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: North America Tungsten Carbide Industry Volume Share (%), by Application 2025 & 2033

- Figure 19: North America Tungsten Carbide Industry Revenue (Billion), by End-user 2025 & 2033

- Figure 20: North America Tungsten Carbide Industry Volume (K Tons), by End-user 2025 & 2033

- Figure 21: North America Tungsten Carbide Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 22: North America Tungsten Carbide Industry Volume Share (%), by End-user 2025 & 2033

- Figure 23: North America Tungsten Carbide Industry Revenue (Billion), by Country 2025 & 2033

- Figure 24: North America Tungsten Carbide Industry Volume (K Tons), by Country 2025 & 2033

- Figure 25: North America Tungsten Carbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Tungsten Carbide Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Tungsten Carbide Industry Revenue (Billion), by Application 2025 & 2033

- Figure 28: Europe Tungsten Carbide Industry Volume (K Tons), by Application 2025 & 2033

- Figure 29: Europe Tungsten Carbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Tungsten Carbide Industry Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Tungsten Carbide Industry Revenue (Billion), by End-user 2025 & 2033

- Figure 32: Europe Tungsten Carbide Industry Volume (K Tons), by End-user 2025 & 2033

- Figure 33: Europe Tungsten Carbide Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 34: Europe Tungsten Carbide Industry Volume Share (%), by End-user 2025 & 2033

- Figure 35: Europe Tungsten Carbide Industry Revenue (Billion), by Country 2025 & 2033

- Figure 36: Europe Tungsten Carbide Industry Volume (K Tons), by Country 2025 & 2033

- Figure 37: Europe Tungsten Carbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Tungsten Carbide Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Rest of the World Tungsten Carbide Industry Revenue (Billion), by Application 2025 & 2033

- Figure 40: Rest of the World Tungsten Carbide Industry Volume (K Tons), by Application 2025 & 2033

- Figure 41: Rest of the World Tungsten Carbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 42: Rest of the World Tungsten Carbide Industry Volume Share (%), by Application 2025 & 2033

- Figure 43: Rest of the World Tungsten Carbide Industry Revenue (Billion), by End-user 2025 & 2033

- Figure 44: Rest of the World Tungsten Carbide Industry Volume (K Tons), by End-user 2025 & 2033

- Figure 45: Rest of the World Tungsten Carbide Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 46: Rest of the World Tungsten Carbide Industry Volume Share (%), by End-user 2025 & 2033

- Figure 47: Rest of the World Tungsten Carbide Industry Revenue (Billion), by Country 2025 & 2033

- Figure 48: Rest of the World Tungsten Carbide Industry Volume (K Tons), by Country 2025 & 2033

- Figure 49: Rest of the World Tungsten Carbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Rest of the World Tungsten Carbide Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Tungsten Carbide Industry Revenue Billion Forecast, by Application 2020 & 2033

- Table 2: Global Tungsten Carbide Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 3: Global Tungsten Carbide Industry Revenue Billion Forecast, by End-user 2020 & 2033

- Table 4: Global Tungsten Carbide Industry Volume K Tons Forecast, by End-user 2020 & 2033

- Table 5: Global Tungsten Carbide Industry Revenue Billion Forecast, by Region 2020 & 2033

- Table 6: Global Tungsten Carbide Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Global Tungsten Carbide Industry Revenue Billion Forecast, by Application 2020 & 2033

- Table 8: Global Tungsten Carbide Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 9: Global Tungsten Carbide Industry Revenue Billion Forecast, by End-user 2020 & 2033

- Table 10: Global Tungsten Carbide Industry Volume K Tons Forecast, by End-user 2020 & 2033

- Table 11: Global Tungsten Carbide Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 12: Global Tungsten Carbide Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: China Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 14: China Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: India Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 16: India Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Japan Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 18: Japan Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: South Korea Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 20: South Korea Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: Global Tungsten Carbide Industry Revenue Billion Forecast, by Application 2020 & 2033

- Table 24: Global Tungsten Carbide Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 25: Global Tungsten Carbide Industry Revenue Billion Forecast, by End-user 2020 & 2033

- Table 26: Global Tungsten Carbide Industry Volume K Tons Forecast, by End-user 2020 & 2033

- Table 27: Global Tungsten Carbide Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 28: Global Tungsten Carbide Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 29: United States Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 30: United States Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Canada Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 32: Canada Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 33: Mexico Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 34: Mexico Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 35: Global Tungsten Carbide Industry Revenue Billion Forecast, by Application 2020 & 2033

- Table 36: Global Tungsten Carbide Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 37: Global Tungsten Carbide Industry Revenue Billion Forecast, by End-user 2020 & 2033

- Table 38: Global Tungsten Carbide Industry Volume K Tons Forecast, by End-user 2020 & 2033

- Table 39: Global Tungsten Carbide Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 40: Global Tungsten Carbide Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 41: Germany Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 42: Germany Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: United Kingdom Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 44: United Kingdom Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 45: Italy Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 46: Italy Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 47: France Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 48: France Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 49: Rest of Europe Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 50: Rest of Europe Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: Global Tungsten Carbide Industry Revenue Billion Forecast, by Application 2020 & 2033

- Table 52: Global Tungsten Carbide Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 53: Global Tungsten Carbide Industry Revenue Billion Forecast, by End-user 2020 & 2033

- Table 54: Global Tungsten Carbide Industry Volume K Tons Forecast, by End-user 2020 & 2033

- Table 55: Global Tungsten Carbide Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 56: Global Tungsten Carbide Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 57: South America Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 58: South America Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 59: Middle East Tungsten Carbide Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 60: Middle East Tungsten Carbide Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Tungsten Carbide Industry?

The projected CAGR is approximately 6.43%.

2. Which companies are prominent players in the Tungsten Carbide Industry?

Key companies in the market include Umicore, Federal Carbide Company, American Elements, Guangdong Xianglu Tungsten Co Ltd, H C Starck Tungsten GmbH, Sandvik AB, Kennametal Inc, CERATIZIT S A, Jiangxi Yaosheng Tungsten Co Ltd, China Tungsten, Extramet Products LLC, CY Carbide Mfg Co Ltd, Buffalo Tungsten Inc, Sumitomo Electric Industries Ltd.

3. What are the main segments of the Tungsten Carbide Industry?

The market segments include Application, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.70 Billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Applications of Tungsten Carbide in Various End-user Industries; Recylable Property of Tungsten carbide.

6. What are the notable trends driving market growth?

Cement Carbide to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Toxicity of Tungsten carbide; Other Restraints.

8. Can you provide examples of recent developments in the market?

September 2022: CERATIZIT S.A. announced the acquisition of all the shares of AgriCarb SAS, a global leader in tungsten carbide agricultural wear parts for over 35 years. This acquisition will help the company enter new markets. with the help of a high degree of added value and expertise in the field of hybrid tools made of steel and tungsten carbide.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Tungsten Carbide Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Tungsten Carbide Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Tungsten Carbide Industry?

To stay informed about further developments, trends, and reports in the Tungsten Carbide Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence